Protein Ingredients Market Report Scope & Overview:

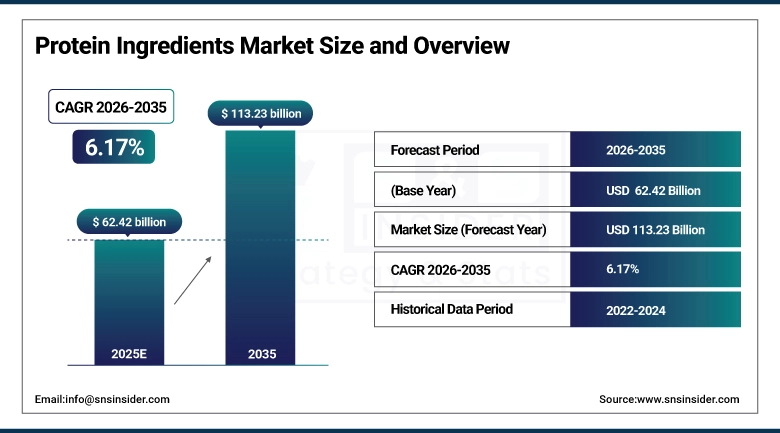

The Protein Ingredients Market size was valued at USD 62.42 Billion in 2025 and is projected to reach USD 113.23 Billion by 2035, growing at a CAGR of 6.17% during 2026–2035.

Protein has gone from being a background macronutrient in food formulation to one of the most visible and commercially influential claims on product packaging across food, beverage, supplement, and pet nutrition categories. What changed is not the nutritional science protein's role in muscle synthesis, satiety, and metabolic function has been understood for decades but the breadth of the consumer population that now actively seeks protein-enriched products as part of a daily routine.

Protein Ingredients Market Size and Forecast:

-

Market Size in 2025: USD 62.42 Billion

-

Market Size by 2035: USD 113.23 Billion

-

CAGR: 6.17% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Protein Ingredients Market - Request Free Sample Report

Key Protein Ingredients Market Trends:

-

Plant-based protein expands beyond soy to diverse sources, improving taste, texture, and amino acid profiles.

-

Precision fermentation produces animal-identical dairy proteins, attracting investment bridging animal and plant protein performance.

-

Protein sourcing faces sustainability scrutiny, with brands factoring land, water, and emissions alongside cost.

-

Insect protein gains regulatory and commercial acceptance, used in pet food, aquafeed, and specialty nutrition.

-

Protein hydrolysates grow in infant, clinical, and sports nutrition, offering faster absorption and better solubility.

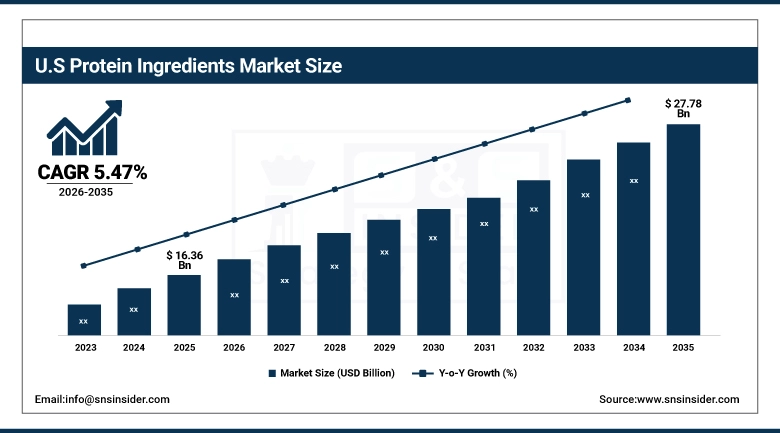

The U.S. Protein Ingredients Market was valued at USD 16.36 Billion in 2025 and is projected to reach USD 27.78 Billion by 2035, growing at a CAGR of 5.47% during 2026–2035. The United States hosts the world's most developed functional food and sports nutrition commercial infrastructure, where protein content claims have been commercially standard long enough that the market has moved past early adoption into a phase of product category maturation and format diversification.

Protein Ingredients Market Growth Drivers:

-

Mainstream Consumer Demand for High-Protein Food and Beverage Products Has Created a Sustained Procurement Pull Across the Entire Protein Ingredient Supply Chain

The broadening of protein's consumer appeal from a specialist athletic nutrition category into everyday food purchasing behavior is the structural driver underneath most of the growth in this market. It does not require new technology or regulatory change to sustain it just requires that the food manufacturing industry continues to respond to what consumers are asking for at retail, and the signals have been consistent for long enough that protein inclusion has become a standard formulation objective rather than a brand differentiator in many categories. Snack bars, ready-to-drink beverages, dairy and dairy-alternative yogurts, cereals, and meal replacement formats have all normalized protein content as a primary nutritional claim

Protein Ingredients Market Restraints:

-

Raw Material Supply Concentration, Commodity Price Volatility, and Allergen Management Complexity Are Creating Structural Constraints on Market Expansion Pace

Two of the market's three largest volume protein sources whey and soy carry supply concentration and commodity exposure that create recurring procurement challenges for food manufacturers. Whey protein is a co-product of cheese manufacturing, so its availability is determined by dairy industry production decisions that protein ingredient buyers have no influence over. When cheese production contracts in response to dairy market dynamics, whey supply tightens and prices rise regardless of demand conditions in the protein ingredient market. Soy protein supply is geographically concentrated in a small number of producing countries, creating exposure to weather, trade policy, and logistics disruption that has materialized in real procurement impact during multiple periods over the past decade.

Protein Ingredients Market Opportunities:

-

Precision Fermentation Technology, Emerging Market Demand Growth, and the Premiumization of Pet Nutrition Are Creating Commercial Pathways That Extend Well Beyond the Core Human Food Channel

Precision fermentation is the most commercially consequential development in protein ingredient production in the current decade, and its importance lies in what it resolves rather than what it adds. The two main limitations of plant-based protein incomplete amino acid profiles relative to animal protein and functional performance shortfalls in applications where protein network formation matters are addressed directly by fermentation-produced whey and casein proteins that are biologically identical to their conventional dairy counterparts but produced without any animal input. Companies including Perfect Day and Remilk have taken these proteins from laboratory demonstration to commercial ingredient supply, and established ingredient companies are licensing the technology and building out fermentation capacity that will bring production costs toward parity with conventional dairy protein over the forecast period. The pet nutrition channel represents a distinct and fast-growing opportunity that is changing the competitive dynamics in several animal protein ingredient categories.

Protein Ingredients Market Segment Analysis:

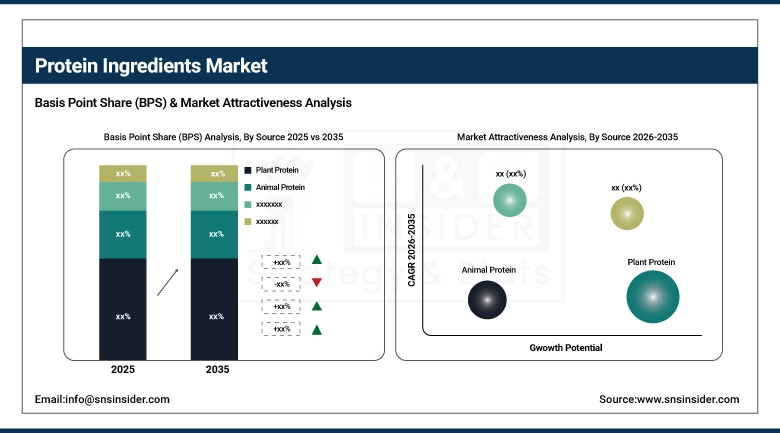

By Source: Plant Protein Leads While Insect Protein Drives the Fastest Growth Through 2035

Plant Protein dominated with a 42.15% share in 2025, valued at approximately USD 26.31 Billion, while Insect Protein is expected to grow at the fastest CAGR of approximately 8.94% through 2035.

Plant protein holds its leading share because it serves the broadest range of product applications and consumer segments simultaneously it is the default protein source for vegan and vegetarian product formulations, the dominant source in much of the emerging market food manufacturing sector where animal protein ingredient costs are prohibitive, and an increasingly accepted option in mainstream food and beverage products where label cleanliness and sustainability positioning matter to the target consumer. Pea protein has been the category's growth engine, moving from niche plant-based product applications into mainstream usage across dairy alternatives, meat analogues, snack bars, and ready-to-drink beverages.

By Product Type: Protein Concentrates Lead While Protein Hydrolysates Register Fastest CAGR Through 2035

Protein Concentrates dominated with a 40.72% share in 2025, valued at approximately USD 25.42 Billion, while Protein Hydrolysates are expected to grow at the fastest CAGR of approximately 7.37% through 2035.

Protein concentrates retain leadership because they represent the most accessible entry point for protein ingredient inclusion across cost-sensitive food manufacturing applications they deliver meaningful protein content at a lower per-kilogram cost than isolates or hydrolysates, and their production process is well established across both animal and plant protein sources. For emerging market food manufacturers and mid-market brands where ingredient cost is the primary constraint, concentrates are where protein inclusion begins.

By Application: Food & Beverages Leads While Animal Feed & Pet Food Drives Fastest Growth Through 2035

Food & Beverages dominated with a 48.36% share in 2025, valued at approximately USD 30.18 Billion, while Animal Feed & Pet Food is expected to grow at the fastest CAGR of approximately 7.28% through 2035.

Food and beverage applications hold the commanding share because they represent the most diverse and highest-volume channel for protein ingredient consumption, spanning infant formula, clinical and medical nutrition, sports nutrition, functional beverages, dairy and dairy alternatives, meat analogues, snack formats, and bakery applications that collectively absorb protein ingredients at a scale no single other channel approach. The breadth of the food and beverage category means it captures volume growth across virtually every protein source and form factor simultaneously.

By Form: Dry / Powder Leads While Liquid Form Registers Fastest CAGR Through 2035

Dry / Powder dominated with a 78.64% share in 2025, valued at approximately USD 49.08 Billion, while Liquid format is expected to grow at the fastest CAGR of approximately 7.17% through 2035.

Powder's dominant share reflects the most fundamental logistics reality of the protein ingredient market: it is the most economical form to ship and store over the long distances that typically separate protein ingredient production and food manufacturing locations. Powder dissolves or disperses readily in most manufacturing processes, tolerates ambient storage without cold chain requirements, and can be used across dry blending, wet processing, and extrusion applications without form-specific handling infrastructure. The manufacturing base for powdered protein ingredient handling is universal across global food processing.

Protein Ingredients Market Regional Analysis:

North America Protein Ingredients Market Insights

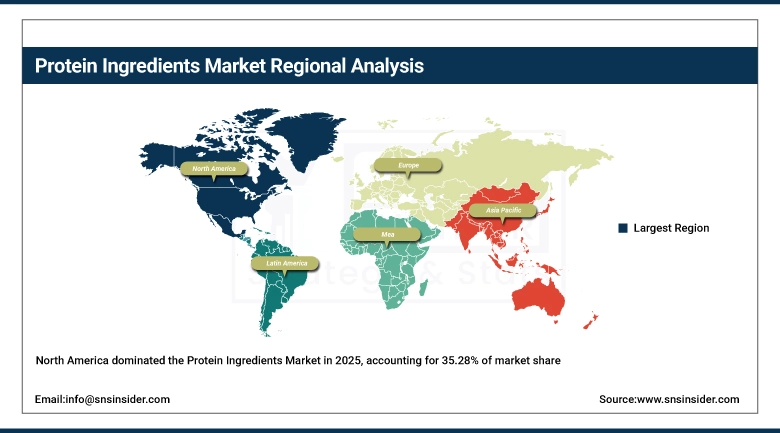

North America dominated the Protein Ingredients Market in 2025, accounting for 35.28% of market share, valued at USD 22.02 Billion, and is projected to reach USD 37.83 Billion by 2035 at a CAGR of 5.59% during the forecast period.

The region's market leadership reflects a food manufacturing sector that has been incorporating protein content claims across product categories for longer than any other geography, a sports and active nutrition retail infrastructure of unmatched commercial depth, and a protein ingredient supply chain from Midwestern soy processing through whey protein production concentrated in the dairy belts of Wisconsin and California that gives U.S. food manufacturers a domestic sourcing option with logistics advantages over imported ingredients. Consumer protein literacy is high and continues to deepen, with awareness extending across demographic segments that were not previously active protein ingredient consumers.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Protein Ingredients Market Insights

The United States accounts for 74.3% of North American demand in 2025. The U.S. Protein Ingredients Market was valued at USD 16.36 Billion in 2025 and is projected to reach USD 27.78 Billion by 2035, growing at a CAGR of 5.47% during 2026–2035. The depth of the U.S. market reflects procurement activity across a uniquely broad set of channels: mainstream grocery reformulation, specialty nutrition retail, foodservice protein enrichment, clinical nutrition procurement through hospital and healthcare networks, and precision fermentation startups entering commercial ingredient supply are all simultaneously active in ways that sustain demand growth across multiple protein source and product type categories at once.

Europe Protein Ingredients Market Insights

Europe held a 27.64% share of the Protein Ingredients Market in 2025, valued at USD 17.25 Billion, and is expected to reach USD 29.58 Billion by 2035 at a CAGR of 5.57% during the forecast period. European demand is shaped by strong consumer preference for clean-label, sustainably sourced ingredients, a regulatory environment through EFSA novel food approvals and EU food labeling rules that creates both constraints and commercial clarity for new protein source introductions, and an active plant-based food sector in the Netherlands, Germany, and the UK that has been consuming pea, soy, and specialty plant protein ingredients in growing volumes.

Germany Protein Ingredients Market Insights

Germany leads the European protein ingredients market, anchored by one of the continent's largest food processing industries, a deeply established dairy sector that generates significant whey protein production capacity, and a consumer market that is among Europe's most active in adopting plant-based food products. German food manufacturers are sophisticated ingredient buyers with high specification standards, and the country's concentration of food ingredient distributors and application development centers makes it the natural entry point for new protein ingredient suppliers seeking European commercial traction.

Asia Pacific Protein Ingredients Market Insights

Asia Pacific is expected to grow at the fastest CAGR of approximately 7.24% from 2026 to 2035, rising from USD 15.71 Billion in 2025 to USD 31.51 Billion by 2035. The region's growth leadership reflects rising incomes expanding consumer access to protein-enriched products, rapid growth of domestic food and beverage manufacturing industries in China, India, and Southeast Asia building protein ingredient procurement capability, and a sports and active nutrition market in China, South Korea, and Japan that is growing faster than any comparable segment in established Western markets. Government nutrition improvement programs in China and India are also creating structured demand for protein fortification across processed food categories at national scale.

China Protein Ingredients Market Insights

China is the dominant national market within Asia Pacific, driven by the scale of its domestic food manufacturing industry, a rapidly expanding sports and fitness culture in urban populations, and a government nutrition agenda that has actively promoted protein consumption improvements across the Chinese diet through both public education programs and food manufacturing incentive frameworks.

Latin America and Middle East & Africa Protein Ingredients Market Insights

Latin America held approximately 6.48% of the global Protein Ingredients Market in 2025, valued at USD 4.04 Billion, and is expected to reach USD 7.84 Billion by 2035 at a CAGR of 6.87% during the forecast period. Brazil and Mexico are the primary markets, supported by large domestic food processing sectors, active sports nutrition retail channels serving growing urban fitness culture, and Brazil's position as a major soy producer that gives domestic food manufacturers cost-competitive access to plant protein ingredients. Middle East & Africa held approximately 5.43% of market share in 2025, valued at USD 3.39 Billion, and is expected to reach USD 6.48 Billion by 2035 at a CAGR of 6.72% during the forecast period. Gulf state food manufacturers and the region's growing sports nutrition retail sector are the primary demand drivers. The UAE and Saudi Arabia are the most commercially developed markets, with South Africa leading African continent adoption within a primarily formal food retail and processing environment that is expanding its protein ingredient procurement as product reformulation activity accelerates.

Competitive Landscape for Protein Ingredients Market:

Cargill operates one of the world's most integrated protein ingredient businesses, with supply chain positions spanning soy protein processing in North and South America, whey protein production through its dairy ingredient operations, and plant-based textured protein manufacturing that serves the growing demand for meat analogue ingredients from food manufacturers reformulating across retail and foodservice channels.

In February 2025, Cargill announced the commissioning of a new pea protein isolation line at its Fort Dodge, Iowa facility, adding capacity specifically configured for non-GMO yellow pea processing to serve food and beverage manufacturer demand for North American-origin plant protein with traceability documentation.

Kerry Group approaches the protein ingredients market from an application expertise position rather than a commodity ingredient supply position. The company's protein offering spans dairy proteins from its Nutritional Ingredients division native whey, whey protein concentrates and isolates, milk protein concentrates, and caseins alongside plant and fermentation-derived proteins that are formulated into functional systems addressing the specific performance challenges that high-protein product development creates.

In April 2025, Kerry Group launched an expanded range of protein ingredient systems under its Tegral and ProDiem platforms targeting the active aging nutrition segment, incorporating a combination of whey protein isolate, plant-sourced leucine-enriched amino acid fractions, and collagen peptides designed to address the dual requirements of muscle protein synthesis and joint support that are clinically relevant for consumers over sixty.

Protein Ingredients Market Key Players:

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Kerry Group plc

-

Ingredion Incorporated

-

International Flavors & Fragrances Inc.

-

Roquette Frères

-

Glanbia plc

-

Arla Foods Ingredients Group

-

Fonterra Co-operative Group

-

FrieslandCampina

-

CHS Inc.

-

Bunge Limited

-

The Scoular Company

-

Gelita AG

-

Leprino Foods Company

-

Burcon NutraScience Corporation

-

Fuji Oil Holdings Inc.

-

Wilmar International Limited

-

Axiom Foods Inc.

-

Corbion N.V.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 62.42 Billion |

| Market Size by 2035 | USD 113.23 Billion |

| CAGR | CAGR of 6.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Plant Protein, Animal Protein, Microbial Protein, and Insect Protein) • By Product Type (Protein Concentrates, Protein Isolates, Protein Hydrolysates, and Textured Protein) • By Application (Food & Beverages, Dietary Supplements & Sports Nutrition, Animal Feed & Pet Food, and Pharmaceuticals & Personal Care) • By Form (Dry / Powder and Liquid) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cargill Incorporated, Archer Daniels Midland Company, Kerry Group plc, Ingredion Incorporated, International Flavors & Fragrances Inc., Roquette Frères, Glanbia plc, Arla Foods Ingredients Group, Fonterra Co-operative Group, FrieslandCampina, CHS Inc., Bunge Limited, The Scoular Company, Gelita AG, Leprino Foods Company, Burcon NutraScience Corporation, Fuji Oil Holdings Inc., Wilmar International Limited, Axiom Foods Inc., Corbion N.V. |

Frequently Asked Questions

North America dominated the Protein Ingredients Market in 2025.

Plant Protein dominated the Protein Ingredients Market.

Rising demand for high-protein diets, plant-based nutrition, and functional foods is driving market growth.

The Protein Ingredients Market size was USD 62.42 Billion in 2025 and is expected to reach USD 113.23 Billion by 2035.

The Protein Ingredients Market is expected to grow at a CAGR of 6.17% from 2026-2035.

Get in Touch