Halogen-Free Flame Retardants Market Report Scope & Overview:

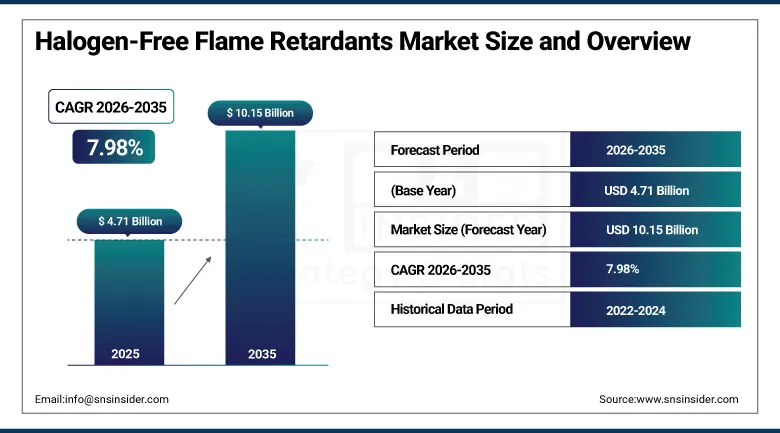

The Halogen-Free Flame Retardants Market size was USD 4.71 Billion in 2025 and is expected to reach USD 10.15 Billion by 2035, growing at a CAGR of 7.98% from 2026–2035.

The halogen-free flame retardant protects any material against fire threats through the absence of halogen-containing compounds that could be toxic. The requirement for such products will only grow due to regulations on other hazardous options. There are some significant differences in production and application depending on the area of manufacturing. Prices for raw materials and trends of supply chains affect price fluctuations. Regulations like RoHS and REACH push companies to restructure their products.

There is a growing focus on such sustainability indicators as carbon footprint decrease among the manufacturers' innovation goals. Innovation in phosphorus flame retardants and intumescent flame retardants will help provide more choices for customers. Electrical, automotive, and construction industries are still driving adoption growth. Recycling is another trend for manufacturers to consider.

Market Size and Forecast

-

Market Size in 2026E: USD 5.09 Billion

-

Market Size by 2035: USD 10.15 Billion

-

CAGR: 7.98% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Halogen-Free Flame Retardants Market - Request Free Sample Report

Halogen-Free Flame Retardants Market Trends

-

Phosphorus- and nitrogen-based flame retardant formulations are gaining share as halogenated alternatives face restrictions.

-

Bio-based and sustainable flame retardant development is expanding manufacturer R&D investment significantly.

-

Growing electric vehicle production is creating fresh demand for fire-resistant battery and component materials.

-

Nanotechnology integration is improving thermal stability and fire protection while reducing environmental impact.

-

Expanding 5G infrastructure deployment is driving demand for fire-resistant connectors and enclosure materials.

-

Recyclable and biodegradable flame retardant formulations are gaining traction across construction and electronics.

-

Strategic capacity expansions across Asia are positioning manufacturers closer to fast-growing electronics demand.

The U.S. Halogen-Free Flame Retardants Market Outlook

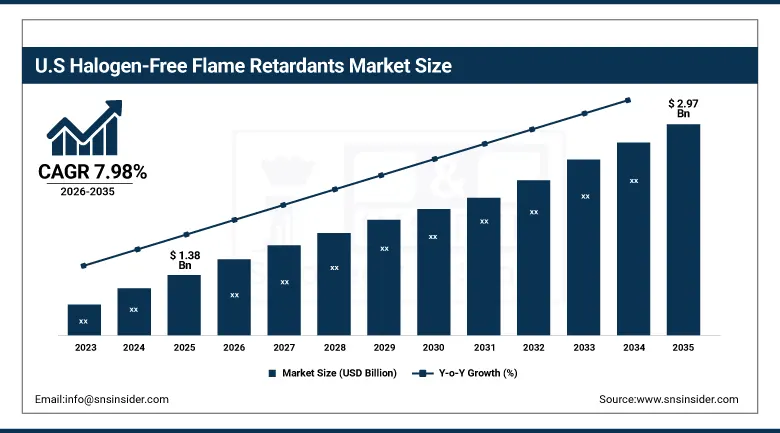

The U.S. Halogen-Free Flame Retardants Market was valued at approximately USD 1.38 Billion in 2025. It is expected to reach approximately USD 2.97 Billion by 2035, growing at a CAGR of approximately 7.98%.

Strictly regulated fire safety standards under NFPA and EPA guidelines continue reinforcing U.S. market leadership. High penetration across construction, automotive, and electronics sectors keeps requiring compliant flame-retardant materials. The presence of leading manufacturers, including DuPont, Dow, and Avient Corporation, drives continuous innovation. Growing demand for eco-friendly materials keeps pushing investment toward phosphorus and nitrogen-based alternatives. Rising electric vehicle production is also adding fresh demand for fire-resistant battery materials domestically.

In May 2024, SABIC unveiled findings on its thermoplastic-based thermal runaway barrier solutions for EV batteries. The company's battery module box, built from long glass fiber polypropylene resin, showed strong thermal barrier performance. This kind of innovation reflects growing demand for fire-resistant materials across the expanding electric vehicle sector. Battery safety requirements continue tightening as EV production volumes keep climbing worldwide. Manufacturers investing early in proven thermal barrier technology should gain meaningful competitive advantage. Similar thermal management innovations are likely to emerge from other major specialty chemical producers.

Halogen-Free Flame Retardants Market Segment Analysis

-

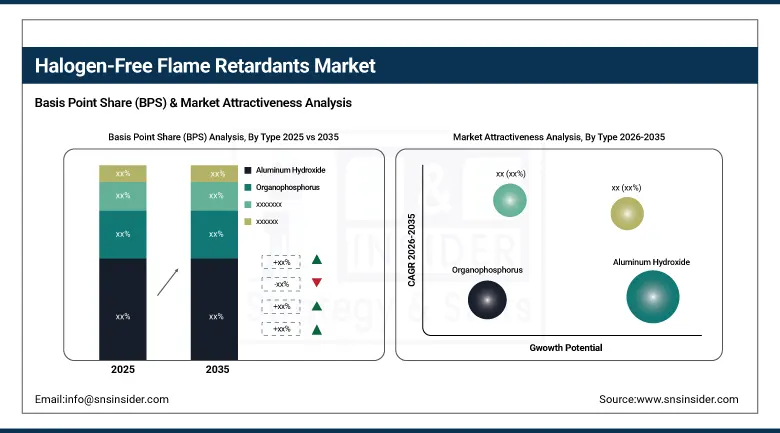

By Type, the Aluminum Hydroxide segment dominated the Halogen-Free Flame Retardants Market with approximately 72% share in 2025, while organophosphorus-based flame retardants is expected to grow progressively.

-

By Application, the polyolefins segment dominated the halogen-free flame retardants market with approximately 28% share in 2025, while engineering thermoplastics is expected to grow progressively

-

By End-Use Industry, the electrical & electronics segment dominated the halogen-free flame retardants market with approximately 44% share in 2025, while transportation is expected to grow progressively

By Type, aluminum hydroxide dominates on cost and performance

The aluminum hydroxide emerged dominant among types in the year 2025, accounting for about 72% of the total revenue share. Wide-ranging use cases, low cost, and effective flame retardancy features all contribute to the dominance of this material. The construction, electrical and electronics, and automotive sectors mainly use this material due to the following benefits: excellent thermal stability, low toxicity, and smokes suppression. Thermal decomposition of the material at 180 to 200 degrees Celsius releases water vapor, resulting in surface cooling effect. This feature helps prevent the spread of flames within a wide range of polymer blend materials. In addition, the aluminum hydroxide is easier to obtain and cheaper than the organophosphorus retardants. The particle size optimization helps improve the dispersion of this material within various polymer matrices. The ongoing regulations against the halogenated flame retardants will ensure that this material maintains its prominent position.

The organophosphorus flame retardants form the main alternative products in the type category. Synthetic processes used in manufacturing these products are complicated and costly. Manufacturers still produce the organophosphorus materials for specific application requirements. The increasing demand for engineering plastics with higher performance levels increases the importance of this category of flame retardants.

By Application, polyolefins dominate on cost and processability

Polyolefin was the leading application type in 2025, accounting for about 28% share in total revenue generation. Industries such as packaging, construction, automobiles, and electrical & electronics depend greatly on these materials. Polyethylene and polypropylene are among the most common polyolefins due to their economical nature. Light weight and ease of processing are other factors that have increased the usage of these materials. As the polyolefin is combustible, halogen-free flame retardants are mandatory for fire resistance requirements. Increasing demand for green flame-retardant products in wire & cables, and roof industries strengthens this segment. Key players in the market have been constantly working on producing new halogen-free products for this segment.

The applications such as engineering thermoplastic and other special applications are emerging along with electronics & EV. These applications often need the flame retardants that can cope with stringent mechanical and thermal properties. The miniaturization of the electronic devices has increased the chance of overheating in compact devices. With increasing production of advanced electronics and electric vehicles, demand in these applications will be high.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

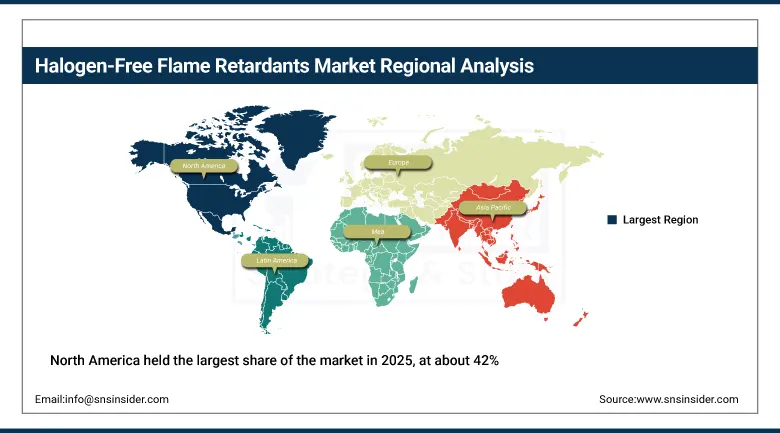

North America Halogen-Free Flame Retardants Market Insights

North America held the largest share of the market in 2025, at about 42%. Rising demand for sustainable materials and strong industrial growth across multiple sectors support this lead. Strict regulations including the TSCA system and halogenated retardant bans drive this transition. Growing electric vehicle adoption and expanding 5G infrastructure keep adding further regional demand. Canada is also tightening its own chemical safety regulations in line with U.S. standards.

The United States accounts for approximately 82.5% of North American revenue. Major companies, including ICL Group, Clariant, and LANXESS, continue investing in non-halogenated formulations domestically. Supportive government initiatives around sustainable practices and circular economy principles further reinforce this regional position.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Halogen-Free Flame Retardants Market Insights

Europe held a significant market share in 2025, supported by stringent environmental regulations. The EU REACH regulation and RoHS Directive continue encouraging production and use of environmentally friendly alternatives. Germany, France, and the UK represent mature markets where halogen-free solutions are gaining ground steadily. Italy and Spain are also showing rising adoption across their domestic construction sectors.

Germany accounts for approximately 24.6% of European revenue. Market leaders, including BASF, Clariant, and LANXESS, continue investing heavily in phosphorus and aluminum hydroxide-based formulations. Expanding electric vehicle and renewable energy projects across Europe keep stimulating further regional demand.

Asia Pacific Halogen-Free Flame Retardants Market Insights

Asia Pacific shows strong growth potential in this market, driven by expanding electronics and EV manufacturing. China's large-scale electronics production base keeps driving rising demand for compliant flame-retardant materials. Growing regional electric vehicle production is also adding meaningful fresh demand for fire-resistant battery materials. India and South Korea are also emerging as meaningful growth markets through expanding manufacturing capacity.

China accounts for approximately 40.6% of Asia Pacific revenue. Expanding manufacturing capacity and rising environmental regulation across the region both support continued growth. As electronics and EV production keep scaling regionally, this growth trajectory should continue strengthening.

MEA & Latin America Halogen-Free Flame Retardants Market Insights

The UAE leads MEA revenue, growing construction and infrastructure investment across the region supports rising demand for fire-safe materials. Saudi Arabia is also expanding its industrial base, adding further regional demand.

Brazil leads Latin American revenue, growing construction and automotive manufacturing activity keeps driving regional demand higher. Mexico and Argentina contribute secondary demand through their own expanding manufacturing sectors.

Market Dynamics

Growth Drivers: Stringent fire safety regulations and environmental concerns propelling growth

Fire safety regulations and environmental sustainability are becoming increasingly important as another major factor for the development of the market. Halogen-based flame retardants are being banned across the world because of their negative effects on health and the environment. The implementation of laws such as RoHS, REACH, and EPA recommendations makes it happen. Phosphorus and nitrogen-based materials become more popular in construction, automotive, and electronics industries. The insurance underwriters consider the issue of fire safety more carefully now.

The growing demand for safe and environmentally friendly materials from consumers is one more reason why the market develops dynamically. It is caused by increased awareness of the risks related to fire hazards. Innovation and improvement of the composition of flame-retardant compounds become more rapid. The trade organizations promote the development of unified standards across the world. In the insurance and building codes, there are more mentions of compliance with the halogen-free compounds. The growth will continue during the forecast period due to the increasing regulation pressure.

Restraints: High production costs and complex manufacturing limiting expansion

The substitution of halogenated flame retardants by phosphorus, nitrogen, and inorganic flame retardants demands sophisticated processes from a chemical standpoint. The need for such specific processes results in higher costs of production in general. Sourcing raw materials needed for these environmentally friendly flame retardants is still rather costly.

Introduction of halogen-free flame retardants into polymers may impact mechanical characteristics and thermal stability. Businesses encounter genuine difficulties when it comes to increasing production in an economically viable manner. All these constraints hamper the market development, especially in developing countries which prefer inexpensive fire protection. End-use markets with price concerns tend to lag behind.

Opportunities: Bio-based flame retardant innovation creating new growth potential

Rising bio-based and sustainable flame retardant solutions present a significant market opportunity. Leading manufacturers are investing in R&D for high-performance, environmentally safe formulations specifically. Companies including Clariant, BASF, and FRX Polymers are exploring renewable-source flame retardant alternatives actively. Bio-based formulations derived from agricultural byproducts are also gaining early-stage commercial interest.

Nanotechnology integration is enhancing thermal stability and fire protection while reducing environmental impact further. Rising demand for recyclable, biodegradable materials across construction and electronics keeps driving this opportunity. Manufacturers focusing on sustainable, halogen-free solutions should gain meaningful competitive advantage as this trend continues. Circular economy partnerships are also opening new collaborative pathways for sustainable formulation development.

Recent Developments:

-

2024: SABIC unveiled findings on its thermoplastic-based thermal runaway barrier solutions for EV batteries, using STAMAX 30YH570 long glass fiber polypropylene resin.

-

2023: Avient Corporation broadened its Thermoplastic Elastomer portfolio with new halogen-free, flame-retardant grades incorporating recycled and bio-based resins.

-

2023: Clariant launched its halogen-free flame retardant production plant in Daya Bay, Huizhou, China, with a USD 67 million investment supplying Exolit OP formulations.

Halogen-Free Flame Retardants Market Key Players are:

-

BASF SE

-

Songwon Industrial Co., Ltd.

-

SI Group, Inc.

-

Clariant AG

-

Solvay S.A.

-

Adeka Corporation

-

Everspring Chemical Co., Ltd.

-

Dover Chemical Corporation

-

Milliken & Company

-

Sumitomo Chemical Co., Ltd.

-

Trigon Antioxidants Pvt. Ltd.

-

Double Bond Chemical Ind., Co., Ltd.

-

Lycus Ltd.

-

Valtris Specialty Chemicals

-

Omnova Solutions Inc.

-

ICL Group

-

Albemarle Corporation

-

Nabaltec AG

-

Italmatch Chemicals

-

J.M. Huber Corporation

Halogen-Free Flame Retardants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.71 Billion |

| Market Size by 2035 | USD 10.15 Billion |

| CAGR | CAGR of 7.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Aluminum Hydroxide, Organophosphorus) • By Application (Polyolefins, UPE, ETP, Styrenics, Others) • By End-Use Industry (Electrical & Electronics, Construction, Transportation) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Songwon Industrial Co., Ltd., SI Group, Inc., Clariant AG, Solvay S.A., Adeka Corporation, Everspring Chemical Co., Ltd., Dover Chemical Corporation, Milliken & Company, Sumitomo Chemical Co., Ltd., Trigon Antioxidants Pvt. Ltd., Double Bond Chemical Ind., Co., Ltd., Lycus Ltd., Valtris Specialty Chemicals, Omnova Solutions Inc., ICL Group, Albemarle Corporation, Nabaltec AG, Italmatch Chemicals, and J.M. Huber Corporation. |

Frequently Asked Questions

The Halogen-Free Flame Retardants Market is expected to grow at a CAGR of 7.98% from 2026 to 2035.

The Halogen-Free Flame Retardants Market was valued at USD 4.71 Billion in 2025.

Stringent fire safety regulations, growing environmental restrictions on halogenated alternatives, and rising electric vehicle production are the primary growth factors. Expanding 5G infrastructure deployment is also adding meaningful incremental demand.

The Aluminum Hydroxide segment dominated the Halogen-Free Flame Retardants Market with approximately 72% share in 2025.

North America dominated the Halogen-Free Flame Retardants Market with approximately 42% revenue share in 2025.

Get in Touch