Nitrogen Market Report Scope & Overview:

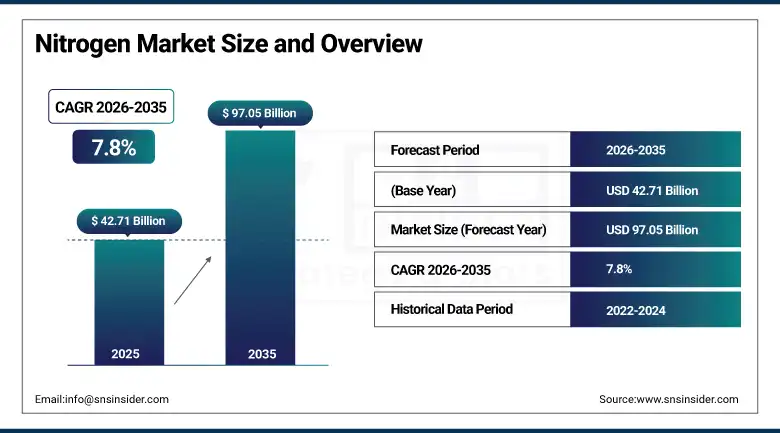

The Nitrogen Market was valued at USD 42.71 Billion in 2025 and is expected to reach USD 97.05 Billion by 2035, growing at a CAGR of 7.8% from 2026–2035.

The global nitrogen market is growing at an exceptional pace. Nitrogen is the most abundant gas in Earth's atmosphere and serves as a foundational industrial gas across petrochemical processing, food packaging, electronics manufacturing, healthcare cryogenics, and metal fabrication. The market is driven by rising demand across food and beverages for packaging and shelf-life extension, increasing demand for cryogenics in healthcare, and extensive use in electronics and semiconductor manufacturing where ultra-high-purity nitrogen creates inert atmospheres preventing oxidation.

In July 2024, researchers at Sydney University published research highlighting that nitrogen emissions could have a net cooling effect on the atmosphere, contrary to conventional views. This scientific development is shifting the regulatory narrative around nitrogen management and creating commercial opportunities for nitrogen producers who can position their products within a more favourable environmental policy context. Industrial gas companies including Air Liquide and Linde are incorporating this emerging science into their sustainability communications as governments review nitrogen emission regulations.

Market Size and Forecast

-

Market Size in 2026E: USD 46.04 Billion

-

Market Size by 2035: USD 97.05 Billion

-

CAGR: 7.8% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Nitrogen Market - Request Free Sample Report

Nitrogen Market Trends

-

Ultra-high-purity nitrogen demand from semiconductor wafer fabrication is increasing with global semiconductor manufacturing expansion.

-

Food and beverage nitrogen packaging adoption is accelerating as modified atmosphere packaging extends product shelf life.

-

Healthcare applications of cryogenic nitrogen are expanding across biological sample storage, cryosurgery, and vaccine cold-chain management.

-

On-site nitrogen generation using pressure swing adsorption and membrane technologies is gaining traction among industrial operators.

-

Green nitrogen production using renewable energy-powered air separation units is emerging as a sustainable alternative.

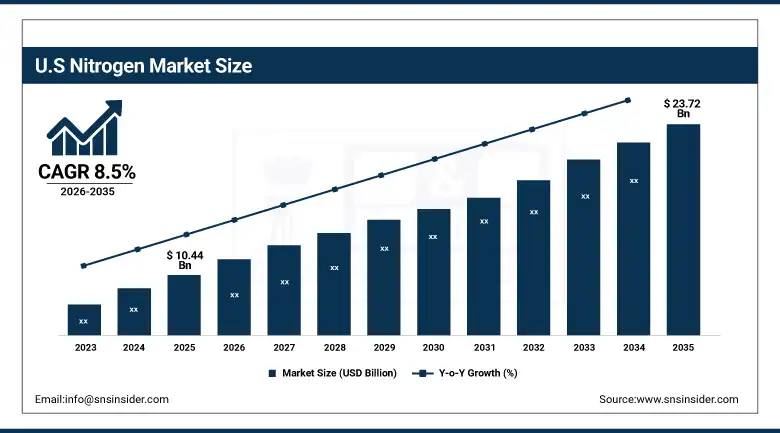

U.S. Nitrogen Market Outlook

The U.S. Nitrogen Market was valued at approximately USD 10.44 Billion in 2025 and is expected to reach approximately USD 23.72 Billion by 2035, growing at a CAGR of approximately 8.5%.

The U.S. is the most commercially significant single-country nitrogen market within the fastest-growing North American region. The U.S. chemical manufacturing sector's petrochemical and polymer production, the semiconductor industry's ultra-high-purity nitrogen requirements, and the food and beverage industry's modified atmosphere packaging adoption collectively sustain above-average domestic nitrogen demand. Air Products, Linde, and Air Liquide's Americas operations define the U.S. merchant nitrogen market whose distribution infrastructure serves the broadest range of industrial and healthcare customer segments.

Air Products and Chemicals signed a landmark USD 15 billion hydrogen and industrial gas supply agreement with Saudi Arabia's NEOM project in 2024, reflecting the scale at which industrial gas companies including nitrogen producers are committing to long-term supply infrastructure investment. The commitment demonstrates the commercial logic of integrated industrial gas supply whose nitrogen, oxygen, and hydrogen production share air separation infrastructure whose capital efficiency sustains competitive pricing across all three product streams simultaneously.

Nitrogen Market Segment Analysis

-

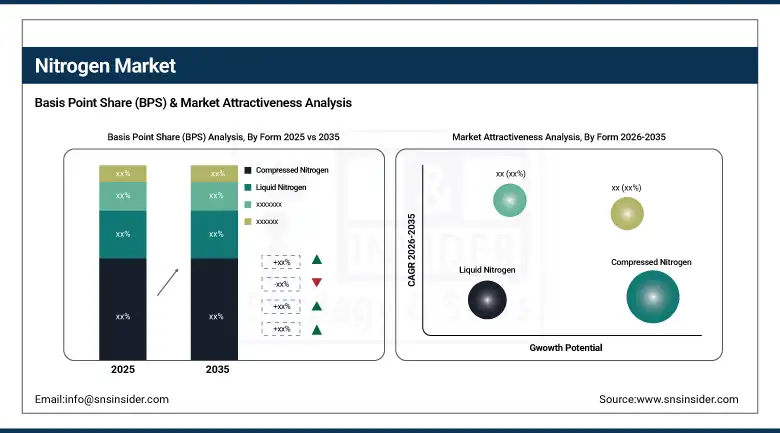

By Form, the Compressed Nitrogen segment dominated the Nitrogen Market with approximately 70% share in 2025, while the Liquid Nitrogen segment is the fastest growing.

-

By Application, the Petrochemical segment dominated the Nitrogen Market with approximately 35% share in 2025, while the Electronics & Semiconductors segment is the fastest growing with a CAGR of approximately 10.2%.

-

By Distribution Channel, the Direct Sales segment dominated the Nitrogen Market in 2025, while the Cylinder & Packaged Gas segment is the fastest growing.

-

By End User, the Chemical Industry segment dominated the Nitrogen Market with approximately 28% share in 2025, while the Healthcare & Pharmaceuticals segment is the fastest growing with a CAGR of approximately 11.5%.

By Form, compressed nitrogen dominates, liquid grows fastest

Compressed nitrogen retained the dominant form position with approximately 70% of the nitrogen market in 2025. Its commercial primacy reflects the universal accessibility of compressed gas cylinder and tube trailer delivery whose infrastructure compatibility with the broadest range of industrial, food, and laboratory applications creates the most commercially versatile nitrogen delivery format. Industrial blanketing and purging applications across chemical plants, refineries, and metal fabrication facilities require nitrogen delivery at ambient temperature and controlled pressure whose compressed gas format serves with established safety infrastructure and handling procedures. Food and beverage modified atmosphere packaging's nitrogen flushing requirement, where compressed nitrogen displaces oxygen from product packaging at high throughput rates, creates consistent large-volume procurement across food manufacturing.

Liquid nitrogen is the fastest-growing form because healthcare cryogenic storage, semiconductor manufacturing cryogenic cooling, and food processing blast freezing are creating above-average demand for nitrogen delivered at cryogenic temperatures whose thermal energy characteristics make liquid delivery the most practical format for large-volume cryogenic applications. Each new biobank installation, cryogenic cell storage programme, and liquid nitrogen-cooled semiconductor process chamber creates procurement that compounds with healthcare infrastructure expansion and semiconductor capacity growth. The coolant application dominates liquid nitrogen use with approximately 61% share as healthcare, biotechnology, food processing, and metal treatment sectors collectively sustain consistent cryogenic nitrogen demand.

By Application, petrochemical dominates, electronics grows fastest

Petrochemical retained the dominant application position with approximately 35% of the nitrogen market in 2025. Nitrogen's critical safety role in petrochemical operations, where its inert atmosphere prevents explosive oxidation in hydrocarbon processing environments, creates non-discretionary procurement whose volume scales with petrochemical plant production capacity. Each refinery, cracker, and polymer plant operates with continuous nitrogen purging and blanketing systems whose safety-critical function creates procurement that is independent of commodity price cycles. The concentration of global petrochemical capacity in the Middle East, Asia Pacific, and the U.S. Gulf Coast creates the geographic procurement density that industrial gas infrastructure investment most efficiently serves.

Electronics and semiconductors is the fastest-growing application at approximately 10.2% CAGR because semiconductor manufacturing's ultra-high-purity nitrogen requirements create premium demand whose per-unit commercial value substantially exceeds commodity industrial nitrogen applications. Each new semiconductor fab commissioned under CHIPS Act and equivalent programmes creates defined ultra-high-purity nitrogen supply contracts whose delivery reliability, purity specification, and on-site generation or pipeline delivery requirements create long-duration commercial relationships between industrial gas suppliers and fab operators.

By Distribution, direct sales dominates, packaged gas grows fastest

Direct sales retained the dominant distribution channel position in the nitrogen market in 2025. High-volume industrial users in chemical manufacturing, petrochemical processing, and pharmaceutical production procure nitrogen through long-term direct supply agreements with industrial gas companies whose pipeline delivery, on-site storage infrastructure, and dedicated supply management create commercial relationships whose switching cost sustains contract continuity. Direct sales contracts typically encompass multi-year volume commitments whose combined take-or-pay provisions create commercially predictable revenue for nitrogen producers. Air Liquide, Linde, and Air Products's pipeline nitrogen networks serving industrial clusters demonstrate the capital investment logic of direct supply whose infrastructure cost is recovered over decade-scale contract durations.

Cylinder and packaged gas is the fastest-growing distribution channel because the expanding laboratory, hospital, specialty manufacturing, and small industrial customer segments require nitrogen in quantities and delivery formats that bulk pipeline supply cannot economically serve. Each new laboratory, hospital nitrogen system, and specialty gas application creates packaged gas procurement whose per-unit margin substantially exceeds commodity bulk nitrogen economics. The convenience premium that cylinder delivery commands over bulk alternatives sustains consistent above-market revenue growth for the packaged gas segment.

By End User, chemical industry dominates, healthcare grows fastest

The chemical industry retained the dominant end user position with approximately 28% of the nitrogen market in 2025. The petrochemical, polymer, and specialty chemical manufacturing sectors collectively represent the highest per-facility nitrogen consumption of any end user category whose continuous process operations, safety-critical inert atmosphere requirements, and large-volume procurement create the most commercially significant industrial gas customer relationships. Chemical plant nitrogen demand is structurally non-discretionary whose production safety requirements create procurement that continues through commodity and economic cycle variation, sustaining consistent revenue that industrial gas suppliers prioritise in supply infrastructure investment decisions.

Healthcare and pharmaceuticals is the fastest-growing end user at approximately 11.5% CAGR because healthcare infrastructure expansion globally, biological medicine's cryogenic storage requirements, and pharmaceutical manufacturing's inert atmosphere and cryogenic processing needs are creating above-average nitrogen demand growth across multiple simultaneous procurement categories. mRNA vaccine manufacturing's cryogenic storage, cell therapy's liquid nitrogen biobanking, and hospital liquid nitrogen systems are each high-growth healthcare nitrogen applications whose combined procurement growth compounds with global healthcare investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

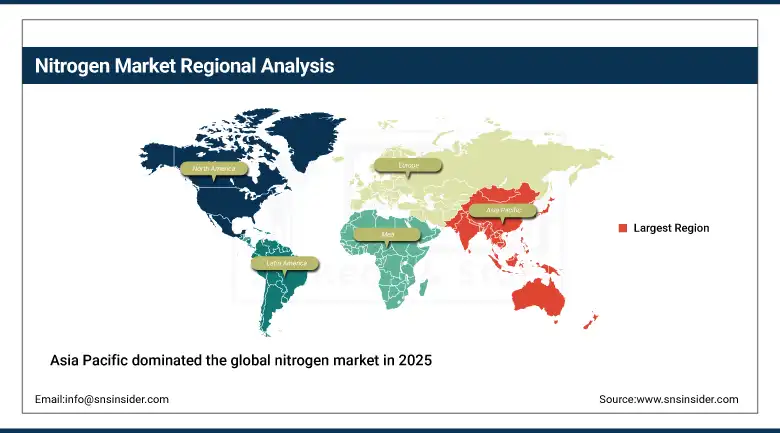

Asia Pacific Nitrogen Market Insights

Asia Pacific dominated the global nitrogen market in 2025 as the world's largest regional market driven by rapid industrialisation, the largest petrochemical and semiconductor manufacturing concentration globally, and the fastest-growing food and beverage industry. China accounts for approximately 54.6% of Asia Pacific revenues through its extraordinary manufacturing scale across chemicals, electronics, and food processing whose combined nitrogen procurement creates the largest single-country market globally. Japan and South Korea's advanced semiconductor manufacturing and India's rapidly expanding pharmaceutical and food processing sectors represent significant secondary markets whose combined procurement reinforces Asia Pacific's commercial dominance.

The region's fastest-growing market dynamic reflects the compounding of above-average industrial nitrogen demand with the expansion of healthcare and semiconductor applications whose commercial growth rates substantially exceed the mature market averages of established European and North American industrial nitrogen consumption.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Nitrogen Market Insights

North America is the fastest-growing regional nitrogen market at above-average CAGR, driven by U.S. semiconductor fab expansion under the CHIPS Act, the chemical manufacturing sector's above-average nitrogen intensity, and the healthcare sector's growing cryogenic nitrogen requirements. The United States accounts for approximately 87.4% of North American revenues through Air Products, Linde Americas, and Air Liquide Americas's commercial dominance across industrial, food, and healthcare nitrogen supply.

Canada contributes approximately 12.6% of North American revenues through its oil sands industry's nitrogen requirements, pharmaceutical manufacturing sector, and food processing industry's modified atmosphere packaging adoption. Mexico's growing manufacturing sector creates increasing nitrogen procurement for automotive, electronics, and food processing applications whose combined demand is expanding the Mexican nitrogen market at above-average regional growth rates.

Europe Nitrogen Market Insights

Europe is a technically sophisticated nitrogen market where the chemical industry's above-average nitrogen consumption, EU environmental standards driving efficient production technology adoption, and the food and beverage industry's modified atmosphere packaging adoption collectively sustain consistent procurement. Germany accounts for approximately 22.3% of European revenues through Linde's German headquarters, BASF's chemical complex nitrogen demand, and the automotive manufacturing sector's metal fabrication nitrogen consumption.

The United Kingdom, France, and the Netherlands are significant secondary markets where chemical manufacturing, food processing, and pharmaceutical production create consistent institutional nitrogen procurement. Air Liquide's European network and Messer Group's regional distribution infrastructure collectively serve the majority of European industrial nitrogen demand across diverse application categories.

MEA & Latin America Nitrogen Market Insights

The Middle East and Africa and Latin America are growing nitrogen markets where petrochemical development, oil and gas exploration, and food processing expansion create structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through its extraordinary petrochemical complex nitrogen demand, SABIC's chemical manufacturing, and ARAMCO's refinery operations whose combined nitrogen procurement creates one of the most commercially concentrated regional industrial gas demand concentrations globally.

Brazil leads Latin American revenues at approximately 44.2% through its large food processing industry's modified atmosphere packaging, the chemical manufacturing sector's nitrogen requirements, and the growing healthcare sector's cryogenic nitrogen demand. Linde and Air Liquide's Brazilian operations serve the domestic merchant nitrogen market whose diverse industrial customer base sustains consistent commercial procurement.

Market Dynamics

Growth Drivers: Semiconductor fab expansion creating ultra-high-purity demand and food packaging nitrogen adoption extending product shelf life globally

Semiconductor manufacturing capacity expansion is the nitrogen market's most commercially premium near-term growth driver. Each new semiconductor fab commissioned under the CHIPS Act in the U.S., European Chips Act, and equivalent programmes in Japan, South Korea, and Taiwan creates defined ultra-high-purity nitrogen supply infrastructure whose commercial value per unit substantially exceeds commodity industrial nitrogen. The semiconductor industry's requirement for nitrogen purity at parts-per-billion impurity levels, combined with the continuous high-volume consumption of multiple fab processes, creates premium long-duration supply contracts whose aggregate commercial value compounds with the extraordinary pace of global fab construction investment.

Food and beverage nitrogen packaging adoption is simultaneously creating the most geographically distributed new nitrogen demand across the widest range of commercial customer sizes. Modified atmosphere packaging's nitrogen flushing, inert atmosphere creation, and product freshness preservation applications across fresh produce, snack foods, beverages, and prepared meals collectively represent a growing procurement pool whose adoption is still in early stages in many emerging markets. Each percentage point increase in global food packaging nitrogen adoption creates proportional demand that compounds with food processing industry growth.

Restraints: On-site nitrogen generation competition reducing merchant market demand and energy cost sensitivity in cryogenic production

On-site nitrogen generation through pressure swing adsorption and membrane separation technologies is progressively enabling large industrial consumers to self-supply nitrogen at costs that reduce merchant procurement dependency. Each industrial operator who installs on-site nitrogen generation creates permanent merchant market demand displacement whose cumulative effect limits merchant nitrogen revenue growth relative to total industrial nitrogen consumption growth. PSA systems held approximately 54% of the industrial nitrogen generator market in 2023, whose continued adoption will progressively convert merchant demand to captive generation.

Cryogenic liquid nitrogen production's high energy intensity creates cost sensitivity that makes liquid nitrogen pricing responsive to electricity price variation in ways that compressed gas alternatives are less affected by. Energy price spikes that increase air separation unit operating cost create margin compression for liquid nitrogen producers whose fixed supply contracts limit short-term price recovery. This energy cost sensitivity creates financial risk management requirements for industrial gas companies whose liquid nitrogen supply commitments extend across multi-year contract periods.

Opportunities: Healthcare cryogenic expansion and ultra-high-purity semiconductor nitrogen premium market

Healthcare cryogenic infrastructure expansion represents the most commercially compelling growth opportunity combining above-average volume growth with premium pricing. mRNA vaccine storage at cryogenic temperatures, CAR-T cell therapy biobanking, reproductive medicine cryopreservation, and hospital liquid nitrogen systems are each healthcare nitrogen applications whose adoption is accelerating with medical technology advancement. Each new mRNA vaccine manufacturing facility creates liquid nitrogen procurement requirements that did not exist in the pre-COVID commercial landscape, demonstrating how medical technology advancement creates new nitrogen demand categories.

Ultra-high-purity semiconductor nitrogen represents the most commercially value-accretive market segment whose per-unit pricing premium over industrial nitrogen creates above-average margin contribution for qualified producers. The technical barrier to supplying semiconductor-grade nitrogen whose purity must be verified and maintained through dedicated purification, distribution, and quality assurance infrastructure creates competitive differentiation that sustains premium pricing for established semiconductor gas suppliers whose fab qualification history creates commercial advantage.

Recent Developments:

-

2024: Air Products and Chemicals signed a landmark USD 15 billion industrial gas supply agreement with Saudi Arabia's NEOM project in 2024, reflecting the commercial scale at which industrial gas companies are committing to long-term integrated supply infrastructure investment combining nitrogen, oxygen, and hydrogen production.

-

2024: July 2024 research by Sydney University highlighting nitrogen emissions' net cooling effect created regulatory and commercial narrative opportunities for industrial nitrogen producers seeking to position their products within a more favourable environmental policy context globally.

-

2024: Linde plc expanded its on-site nitrogen generation service offering in 2024 with new modular PSA systems for mid-scale industrial customers, enabling operators to self-supply nitrogen from air at costs below merchant alternatives while Linde retains revenue through equipment supply, installation, and maintenance service contracts.

Nitrogen Market Key Players

-

Air Liquide S.A.

-

Linde plc

-

Air Products and Chemicals Inc.

-

Praxair Inc. (Linde)

-

Messer Group GmbH

-

Taiyo Nippon Sanso Corporation

-

Gulf Cryo

-

Matheson Tri-Gas Inc.

-

INOX Air Products

-

Yingde Gases Group

-

SOL Group

-

Universal Industrial Gases

-

Luxfer Gas Cylinders

-

Coregas Pty Ltd.

-

Air Water Inc.

-

Nippon Gases

-

Ellenbarrie Industrial Gases

-

PGS Gas

-

Siad S.p.A.

-

Buzwair Industrial Gases

Nitrogen Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 42.71 Billion |

| Market Size by 2035 | USD 97.05 Billion |

| CAGR | CAGR of 6.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Form (Compressed Nitrogen, Liquid Nitrogen, Others) • by Application (Petrochemical, Food & Beverage, Electronics & Semiconductors, Healthcare, Metal Manufacturing, Oil & Gas, Others) • by Distribution Channel (Direct Sales, Merchant/Distributor, Cylinder & Packaged Gas) • by End User (Chemical Industry, Food Processing, Healthcare & Pharmaceuticals, Electronics, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Air Liquide S.A., Linde plc, Air Products and Chemicals Inc., Praxair Inc. (Linde), Messer Group GmbH, Taiyo Nippon Sanso Corporation, Gulf Cryo, Matheson Tri-Gas Inc., INOX Air Products, Yingde Gases Group, SOL Group, Universal Industrial Gases, Luxfer Gas Cylinders, Coregas Pty Ltd., Air Water Inc., Nippon Gases, Ellenbarrie Industrial Gases, PGS Gas, Siad S.p.A., Buzwair Industrial Gases |

Frequently Asked Questions

The Nitrogen Market is expected to grow at a CAGR of 7.8% from 2026 to 2035.

The Nitrogen Market was valued at USD 42.71 Billion in 2025.

Rising demand across food and beverages for packaging and shelf-life extension, increasing demand for cryogenics in healthcare and pharmaceutical manufacturing, and semiconductor fab capacity expansion creating premium ultra-high-purity nitrogen demand growing proportionally with wafer production output.

Compressed Nitrogen dominated the Nitrogen Market with approximately 70% share in 2025, while Liquid Nitrogen is the fastest growing form.

Asia Pacific dominated the Nitrogen Market in 2025 as the world's largest regional market, with China accounting for approximately 54.6% of Asia Pacific revenues.

Get in Touch