Healthcare Market Report Scope & Overview:

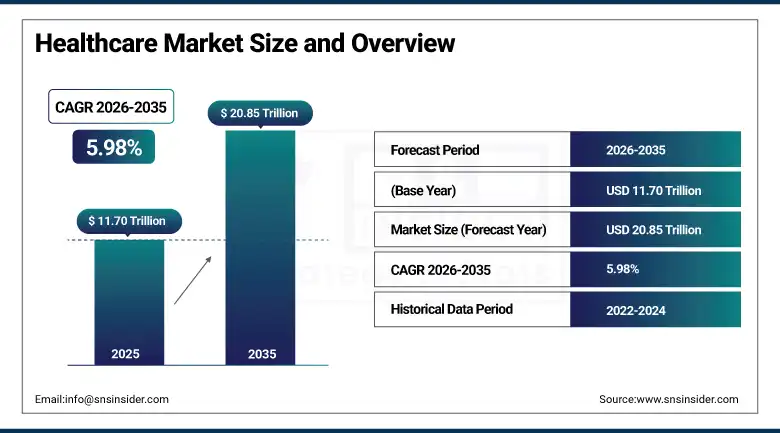

The Healthcare Market was estimated at USD 11.70 Trillion in 2025 and is expected to reach USD 20.85 Trillion by 2035, growing at a CAGR of 5.98% over the forecast period of 2026-2035.

The Healthcare Market is experiencing growth due to the increasing prevalence of chronic diseases around the globe, including cardiovascular diseases, diabetes, cancer, respiratory issues, among others. Aging populations and high life expectancy are contributing to increased use of healthcare services. The fast rate of digitization, such as the use of telehealth technologies, artificial intelligence diagnostics, and electronic health record systems, is enhancing access to these services. Increased spending on healthcare, healthcare initiatives by governments, and increased insurance coverages are other factors that are boosting the growth of the market. Finally, innovations in the field of medical technology are helping to expand the market even more.

According to the World Health Organization (WHO), NCDs kill nearly 41 million people annually worldwide and represent more than 74% of all deaths reported each year, underscoring the massive challenge posed by such diseases to healthcare systems globally. WHO also reports that cardiovascular diseases alone are responsible for around 17.9 million deaths per year, making them the leading cause of mortality globally. Additionally, cancer accounts for nearly 10 million deaths annually, further increasing the demand for advanced diagnostics, treatment infrastructure, and long-term care services. These high disease burdens continue to drive sustained growth in the global healthcare market.

Market Size and Forecast:

-

Market Size in 2026E: USD 12.40 Trillion

-

Market Size by 2035: USD 20.85 Trillion

-

CAGR: 5.98% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Healthcare Market - Request Free Sample Report

Healthcare Market Trends:

-

AI is transforming healthcare through diagnostics, decision support, and early patient deterioration detection systems.

-

Telehealth and remote monitoring are expanding access to care and enabling continuous chronic disease management.

-

Precision medicine is improving treatment outcomes through genetic, molecular, and patient-specific therapy customization.

-

Preventive healthcare programs are growing through wellness platforms, digital therapeutics, and population health management.

-

Public-private partnerships are increasing to expand healthcare infrastructure in emerging markets.

U.S. Healthcare Market Size Outlook:

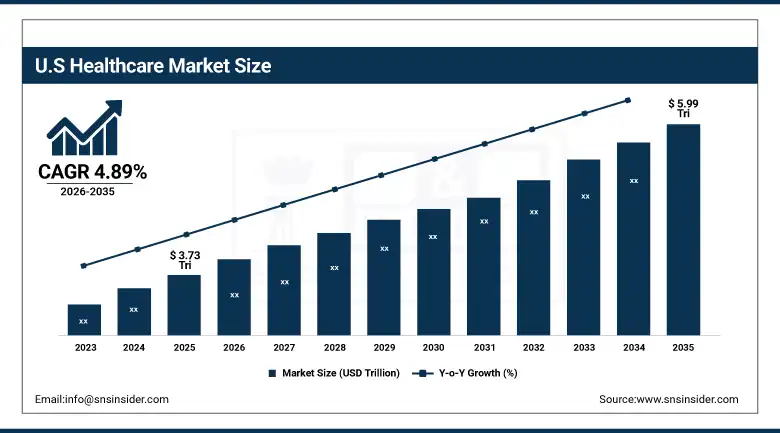

The U.S. Healthcare Market was valued at approximately USD 3.73 Trillion in 2025 and is expected to reach approximately USD 5.99 Trillion by 2035, growing at a CAGR of 4.89%.

The United States accounts for the largest single national share of global healthcare expenditure, exceeding 17% of the country's GDP and representing a market whose scale and sophistication set the standard that pharmaceutical, medical device, and health information technology companies optimise their products and business models to serve before exporting globally. The hospital sector, anchored by major not-for-profit integrated health systems including Mayo Clinic, Cleveland Clinic, Mass General Brigham, and Kaiser Permanente alongside large for-profit chains including HCA Healthcare, CommonSpirit Health, and Tenet Healthcare, drives the largest share of U.S. healthcare expenditure.

According to the U.S. Centers for Disease Control and Prevention (CDC), about 6 in 10 adults in the United States live with at least one chronic disease, significantly increasing long-term healthcare demand and utilization of medical services.

Healthcare Market Segment Analysis

-

By Type, Pharmaceuticals segment dominated the market in 2025 with 29.4% share; Biotechnology segment is the fastest growing segment.

By Type, pharmaceuticals segment dominates the healthcare market, while biotechnology segment is the fastest-growing segment

The pharmaceuticals segment dominated the Healthcare Market owing to its widespread usage to treat various types of diseases and medical conditions. The increasing demand for prescription drugs, OTC drugs, and therapies for chronic illnesses has helped make this segment dominant in the market. The segment has been able to sustain its dominance owing to its strong manufacturing capability, global reach, and innovations in drug manufacturing. Diseases becoming more common, the aging population, and better access to medications will keep this market dominated by the pharmaceutical sector.

The biotechnology segment is the fastest growing because of the quick technological progress in the area of genetic engineering, biological products, and precision medicines. Growing demands for more targeted medicines, immuno-therapies, and personalized medicines increase market demand for these services. Research investments in R&D and clinical trials in this sector boost the growth even further. Modern technologies enable treating diseases that previously could not be cured, making it one of the most promising segments of healthcare today.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.2% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

Saudi Arabia |

31.7% |

|

Latin America |

Brazil |

42.3% |

North America Healthcare Market Insights

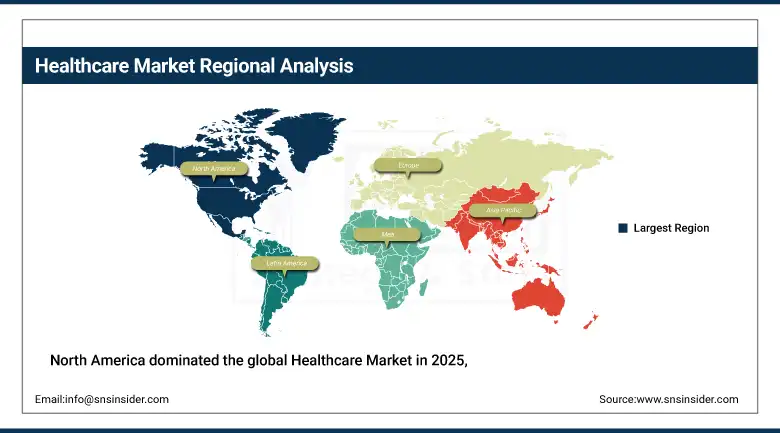

North America dominated the global Healthcare Market in 2025, with the United States accounting for approximately 85.2% of North American revenues. The region's market leadership reflects the combination of the healthcare expenditure at over USD 3.73 Trillion in the U.S. alone in 2025, a multi-payer insurance system that sustains premium pricing for innovative therapies and technologies, and the highest concentration of academic medical centres and clinical research infrastructure. Canada contributes the remaining approximately 14.8% of North American revenues through its universal single-payer provincial health insurance systems.

The Centers for Medicare & Medicaid Services (CMS) reports that the United States spends nearly 18% of its GDP on healthcare, the highest among major economies, reflecting substantial investment in healthcare infrastructure and services. Additionally, the National Cancer Institute notes that around 2 million new cancer cases are diagnosed annually in the U.S., further reinforcing the need for advanced oncology care, diagnostic services, and specialized treatment facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Healthcare Market Insights

Europe is a comprehensive healthcare market characterised by universal health coverage systems for pharmaceutical, device, and health IT products subject to health technology assessment and national reimbursement processes. Germany accounts for approximately 24.6% of European healthcare revenues with a statutory health insurance system covering approximately 90% of the population that is supplemented by a substantial private insurance sector providing faster access and broader coverage for a professionally active and internationally mobile demographic.

According to Eurostat, around 21% of the European Union population is aged 65 or older, significantly increasing healthcare demand due to age-related chronic conditions and long-term care requirements.

Additionally, OECD data indicates that European countries spend an average of approximately 9–11% of GDP on healthcare, reflecting strong institutional investment in healthcare systems, infrastructure, and medical services. These demographic and expenditure trends continue to support sustained growth in healthcare utilization and service expansion across the region.

Asia Pacific Healthcare Market Insights

Asia Pacific is the fastest-growing healthcare market, growing at a CAGR of 7.89%, driven by the China's investment under its successive Five Year Plans, India's rapidly growing middle-class insurance penetration and hospital sector privatisation, Japan and South Korea's advanced ageing demographics, and the healthcare infrastructure development boom across Southeast Asian nations.

According to the World Health Organization (WHO), Asia accounts for over 60% of the global population, creating a massive base for healthcare demand and service utilization across both urban and rural regions.

China accounts for approximately 38.5% of Asia Pacific healthcare revenues and represents the single market expansion opportunity in global healthcare, as its health insurance coverage has extended to over 95% of the population through the Urban Employee Basic Medical Insurance, Urban Resident Basic Medical Insurance, and New Rural Cooperative Medical Scheme programmes, creating a financially eligible patient population of 1.4 billion for whom pharmaceutical, device, and service companies are now competing across an innovation-receptive market.

China, with a population exceeding 1.4 billion, is also witnessing rapid expansion of healthcare infrastructure, including hospitals and insurance coverage systems, which is further strengthening access to medical services and supporting sustained healthcare market growth across the region.

Middle East & Africa and Latin America Healthcare Market Insights

Latin America and the Middle East and Africa are growing healthcare markets where expanding insurance coverage, rising chronic disease prevalence, and government-led healthcare system strengthening are creating sustained demand growth for healthcare products, services, and infrastructure. Brazil accounts for approximately 42.3% of Latin American healthcare revenues through its combination of a large public healthcare system under the Sistema Unico de Saude providing universal coverage and a substantial private supplementary insurance sector serving approximately 50 million Brazilians with faster access to specialists and elective procedures.

Saudi Arabia leads MEA healthcare revenues at approximately 31.7% of the regional total, driven by the Kingdom's Vision 2030 healthcare transformation programme targeting quality improvement, private sector expansion, and domestic manufacturing development in pharmaceuticals and medical devices as part of its economic diversification strategy.

Market Dynamics:

Growth Drivers: Demographic ageing, chronic diseases, biopharmaceutical innovation, and digital transformation are driving global healthcare market growth.

The primary structural growth drivers for the Healthcare Market are the demographically inevitable and globally universal expansion of the elderly population that is generating rising per-capita healthcare utilisation, simultaneously increasing the absolute number of patients requiring complex multi-morbidity management, combined with a biopharmaceutical innovation pipeline of unprecedented richness.

The United Nations' projection that the global population aged sixty and above will reach 2.1 billion by 2050 from approximately 1.0 billion in 2020, with the most rapid growth occurring in the same Asia Pacific countries currently experiencing the fastest healthcare market expansion, provides the single most powerful structural demand guarantee in any major economic sector. Digital health transformation is simultaneously expanding the growth by enabling care delivery models, including continuous remote monitoring of high-risk patients in home environments, AI-powered population health analytics identifying high-risk patients for targeted preventive intervention before expensive acute care episodes occur, and telehealth consultations bringing specialist expertise to geographically remote populations.

Restraints: Rising healthcare costs, limited reimbursement, workforce shortages, and regulatory delays are constraining healthcare market expansion globally.

A significant restraint on the healthcare market is the fundamental tension between the rising cost of innovative pharmaceutical and medical technology therapies and the limited fiscal capacity of national healthcare systems. Gene therapies and CAR-T cell therapies with list prices ranging from USD 400,000 to over USD 3 million per patient treatment are testing the absorption capacity of even the most generously funded healthcare systems, and the health technology assessment methodologies used by national reimbursement bodies in Europe and elsewhere are increasingly struggling to apply conventional cost-effectiveness frameworks to transformative one-time treatments with complex long-term benefit profiles.

Healthcare workforce shortages represent a structural supply constraint that is limiting the capacity of healthcare systems to meet rising service demand in virtually every high-income country, as physician retirement rates exceed medical school graduation rates in several specialties, nursing vacancies persist despite wage increases, and allied health professional shortages in physiotherapy, pharmacy, and diagnostic imaging constrain outpatient care capacity.

Opportunities: Emerging markets, digital health adoption, and precision medicine are creating significant opportunities for healthcare market growth.

The progressive formalisation of healthcare systems in Africa, Southeast Asia, and South Asia through the expansion of national health insurance programmes, public hospital network investment, and pharmaceutical and medical device manufacturing capacity represents the consequential long-term market development opportunity. Nigeria, with 220 million people and healthcare spending at approximately 3.5% of GDP, Indonesia with 280 million people and a National Health Insurance programme now covering over 96% of the population, and Vietnam with 100 million people and rapidly expanding healthcare infrastructure investment represent the type of large emerging market transitions that are creating the next generation of significant healthcare commercial opportunities beyond the China and India success stories of the previous two decades.

Digital health platform scaling is creating cost reduction opportunities throughout healthcare delivery, as telehealth consultations delivered at a fraction of in-person visit cost, AI-powered diagnostic image analysis reducing radiologist review time per study without reducing accuracy, and automated administrative workflows eliminating labour cost from revenue cycle management collectively contribute to improved unit economics that expand the commercially viable service scope of healthcare organisations operating at scale.

Recent Developments:

-

2025: UnitedHealth Group expanded its Optum Health value-based care platform with new AI-powered risk stratification tools enabling primary care physicians to identify high-risk patients for preventive intervention, adding over 500,000 patients to proactive care management programmes.

-

2025: Roche launched its integrated diagnostics and therapeutics data platform connecting companion diagnostic results with treatment selection algorithms for oncology patients, enabling personalised therapy sequencing decisions informed by real-time molecular tumour profiling data.

-

2025: Pfizer advanced its pipeline of next-generation mRNA therapeutics beyond COVID-19 applications into influenza, respiratory syncytial virus, and shingles vaccine programmes, investing over USD 1 billion in expanded mRNA manufacturing capacity to support the launch of multiple mRNA-based vaccine.

-

2025: Siemens Healthineers expanded its AI-powered imaging informatics platform with new deep learning algorithms for automated cardiac MRI analysis, diabetic retinopathy screening, and pulmonary nodule characterisation.

-

2025: Epic Systems expanded its electronic health record platform with new patient-facing digital engagement tools, AI-driven clinical documentation automation, and interoperability enhancements enabling seamless patient data exchange across healthcare organisations using competing EHR platforms.

Healthcare Market Key Players are:

-

UnitedHealth Group

-

CVS Health Corporation

-

McKesson Corporation

-

AmerisourceBergen (Cencora)

-

Cardinal Health

-

Johnson & Johnson

-

Pfizer Inc.

-

Roche Holding AG

-

Novartis AG

-

Merck & Co., Inc.

-

AstraZeneca PLC

-

Sanofi

-

Abbott Laboratories

-

Medtronic plc

-

Siemens Healthineers

-

GE HealthCare

-

Becton, Dickinson and Company (BD)

-

Fresenius SE & Co. KGaA

-

HCA Healthcare

-

Philips Healthcare

Healthcare Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.70 Trillion |

| Market Size by 2035 | USD 20.85 Trillion |

| CAGR | CAGR of 5.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Pharmaceuticals, Healthcare Services, Medical Devices, Biotechnology, Pharmacy and Retail, Home Healthcare, Diagnostics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | UnitedHealth Group, CVS Health Corporation, McKesson Corporation, AmerisourceBergen (Cencora), Cardinal Health, Johnson & Johnson, Pfizer Inc., Roche Holding AG, Novartis AG, Merck & Co., Inc., AstraZeneca PLC, Sanofi, Abbott Laboratories, Medtronic plc, Siemens Healthineers, GE HealthCare, Becton, Dickinson and Company (BD), Fresenius SE & Co. KGaA, HCA Healthcare, Philips Healthcare |

Frequently Asked Questions

The Healthcare Market is expected to grow at a CAGR of 5.98% from 2026 to 2035.

The Healthcare Market was valued at USD 11.70 trillion in 2025.

Ageing populations, rising chronic diseases, biopharmaceutical innovation, and digital health transformation are driving healthcare market growth globally.

Pharmaceuticals segment dominated with approximately 38.2% of revenues in 2025.

North America dominated the Healthcare Market in 2025, with the United States as the leading national market.

Get in Touch