Healthcare Waste Management Market Size:

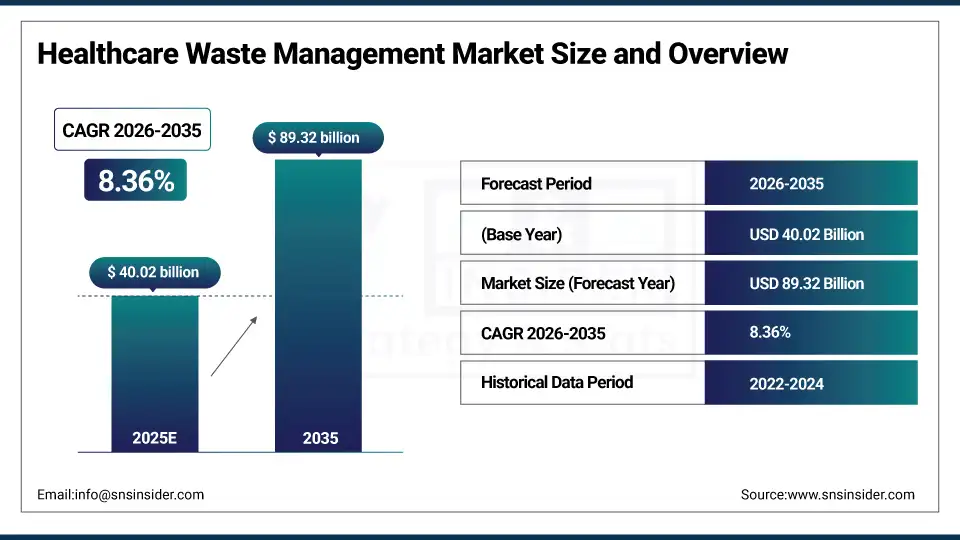

The Healthcare Waste Management Market size is estimated at USD 40.02 billion in 2025 and is expected to reach USD 89.32 billion by 2035, growing at a CAGR of 8.36% over the forecast period of 2026-2035.

The global healthcare waste management market trend is a growing demand for medical waste disposal solutions such as infectious waste treatment systems, sharps disposal containers, and pharmaceutical waste management services. The growth of the market is driven by increasing healthcare facility expansion, stringent environmental regulations for biomedical waste, and rising awareness about infection control and public health safety. Also driven by a growing adoption of sustainable waste treatment technologies and the growing focus on circular economy principles in healthcare as healthcare organizations become more focused on reducing environmental impact and are more willing to invest in comprehensive waste segregation and treatment infrastructure, resulting in growth in the domestic and international market for offsite and onsite waste management solutions.

For instance, in March 2024, growing awareness and improved regulatory compliance drove a 24% increase in healthcare waste management service contracts for hospital systems in North America, boosting proper medical waste disposal and environmental safety practices.

Healthcare Waste Management Market Size and Forecast:

-

Market Size in 2025: USD 40.02 billion

-

Market Size by 2035: USD 89.32 billion

-

CAGR: 8.36% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

Get More Information on Healthcare Waste Management Market - Request Sample Report

Healthcare Waste Management Market Trends

-

Healthcare waste management solutions are being adopted because healthcare facilities demand efficient infectious waste disposal, sharps container management, and pharmaceutical waste destruction services.

-

Customized waste segregation programs based on facility size, waste generation patterns, and regulatory jurisdiction to improve environmental compliance outcomes.

-

The development of advanced sterilization technologies, microwave treatment systems, and chemical disinfection methods to improve the safety of biomedical waste processing and reduce environmental contamination.

-

Automated waste tracking systems, RFID-enabled containers, and digital waste manifest documentation are all available to ensure regulatory compliance and waste disposal chain of custody.

-

Increased demand for sustainable disposal alternatives, waste-to-energy conversion technologies and medical plastic recycling programs to help minimize landfill burden and environmental impact.

-

Collaboration between healthcare providers, waste management companies and environmental agencies to develop standardized waste handling protocols and improve treatment infrastructure.

-

EPA, WHO and national health ministries promoting standards for biomedical waste classification, treatment technology approval, disposal site licensing, and healthcare worker safety protection.

The U.S. Healthcare Waste Management Market is estimated at USD 15.84 billion in 2025 and is expected to reach USD 35.36 billion by 2035, growing at a CAGR of 8.42% from 2026-2035. The United States represents the largest market for healthcare waste management, primarily driven by the stringent EPA and state-level regulations, extensive hospital infrastructure, and well-developed medical waste disposal networks. Government enforcement of biomedical waste standards, high levels of healthcare service utilization and increased provider spending on infection control and environmental compliance programs help to drive growth in the market.

Healthcare Waste Management Market Growth Drivers:

-

Stringent Environmental Regulations and Compliance Requirements are Driving the Healthcare Waste Management Market Growth

Stringent environmental regulations and compliance requirements take the center stage as a growth driver for the healthcare waste management market share, and are driven by the implementation of biomedical waste management rules, hazardous waste disposal mandates, and international guidelines for infectious waste treatment for increased environmental protection and public health safety. These solutions for proper medical waste segregation and treatment are driving the base of the market, the penetration of offsite & onsite treatment markets, and adding to the overall market share globally.

For instance, in June 2024, automated and technology-enabled healthcare waste management solutions accounted for ~58% of the total global hospital environmental services investments, reflecting growing institutional preference and expanding market share.

Healthcare Waste Management Market Restraints:

-

High Implementation Costs and Infrastructure Limitations are Hampering the Healthcare Waste Management Market Growth

High implementation costs & infrastructure limitations of healthcare waste management systems also restrict the healthcare waste management market growth, as a large number of small healthcare facilities and medical clinics in developing regions face difficulties establishing compliant waste treatment infrastructure and affording specialized disposal services. This might lead to improper waste handling, environmental contamination risks, and reduced adoption of best practice waste management protocols. As a result, public health safety suffers, and market growth is stunted in regions where healthcare budgets are limited and waste treatment facility availability is scarce.

Healthcare Waste Management Market Opportunities:

-

Sustainable Technologies and Circular Economy Integration Drive Future Growth Opportunities for the Healthcare Waste Management Market

The opportunity in the sustainable technologies and circular economy integration in healthcare waste management market is in the form of waste-to-energy conversion systems, medical plastic recycling initiatives, and resource recovery from treated waste streams. These solutions provide for reduced environmental footprint, cost savings through material recovery, and alignment with corporate sustainability goals. Through enhanced regulatory compliance, operational efficiency improvements, and environmental stewardship, particularly in areas with growing emphasis on green healthcare practices, these technologies may improve waste diversion rates, decrease carbon emissions, and expand the market.

For instance, in April 2024, the WHO reported that 71% of healthcare facilities in developed nations implemented advanced waste segregation and treatment protocols, highlighting rising environmental awareness and increasing demand for comprehensive medical waste management solutions.

Healthcare Waste Management Market Segment Analysis

-

By service, treatment & disposal services held the largest share of around 46.82% in 2025E, and the recycling services segment is expected to register the highest growth with a CAGR of 9.24%.

-

By type of waste, the hazardous waste segment dominated the market with approximately 63.47% share in 2025E, while the non-hazardous waste is expected to register the highest growth with a CAGR of 8.76%.

-

By treatment site, offsite treatment accounted for the leading share of nearly 68.93% in 2025E, and is expected to register the highest growth with a CAGR of 8.52%.

By Service, Treatment & Disposal Services Leads the Market, While Recycling Services Registers Fastest Growth

The treatment & disposal services segment accounted for the highest revenue share of approximately 46.82% in 2025, owing to critical regulatory requirements for proper infectious waste neutralization, the necessity for specialized sterilization equipment, and strong healthcare provider preference for compliant disposal methods. Emerging trends, including increasing implementation of advanced thermal treatment technologies and regulatory emphasis on pathogen elimination. In comparison, the recycling services segment is anticipated to achieve the highest CAGR of nearly 9.24% during the 2026–2035 period, driven by the increasing focus on sustainable healthcare practices, growing demand for medical plastic recovery, and cost reduction opportunities through material reprocessing. Drivers include rising adoption of circular economy principles, the preference for environmentally responsible waste management.

By Type of Waste, the Hazardous Waste Segment dominates, while the Non-Hazardous Waste Segment Shows Rapid Growth

By 2025, the hazardous waste segment contributed the largest revenue share of 63.47% due to stringent handling requirements, specialized treatment infrastructure needs and higher disposal costs associated with infectious, pathological, and pharmaceutical waste streams. Growing concerns about bloodborne pathogen exposure coupled with regulatory penalties for non-compliance, healthcare facilities are increasingly prioritizing proper hazardous waste management. The non-hazardous waste segment is projected to grow at the highest CAGR of about 8.76% between 2026 and 2035 due to the growing volume of general medical waste generation and improved segregation practices. Some of the reasons include better waste classification training, enhanced recycling program implementation, and healthcare organizations' preference for comprehensive waste stream management.

By Treatment Site, Offsite Treatment Leads, and Registers Fastest Growth

The offsite treatment segment accounted for the largest share of the healthcare waste management market with about 68.93%, owing to centralized treatment facility economies of scale, reduced capital investment requirements for individual healthcare facilities, and access to advanced treatment technologies. Reasons driving the offsite treatment segment include regulatory approval for specialized waste processing centers and transportation logistics efficiency. In addition, it is slated to grow at the fastest rate with a CAGR of around 8.52% throughout the forecast period of 2026–2035, as healthcare providers, hospitals, and medical centers seek cost-effective waste disposal solutions, consolidated service contracts, and compliance assurance from specialized waste management companies. Increased focus on outsourcing non-core services and risk transfer contribute to their adoption, while improved environmental performance and reduced liability exposure drive continued investment.

Healthcare Waste Management Market Regional Highlights:

North America Healthcare Waste Management Market Insights:

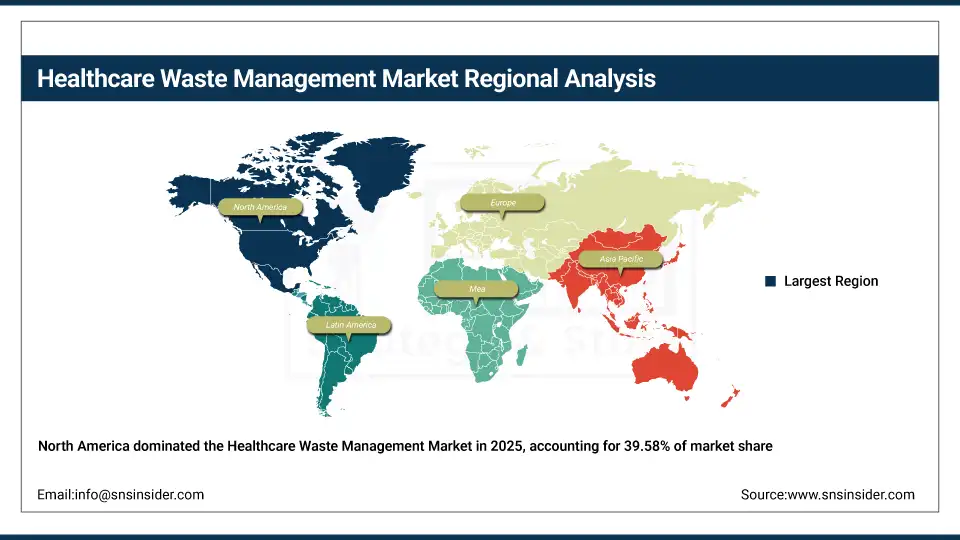

North America held the largest revenue share of over 39.58% in 2025 of the healthcare waste management market due to an established healthcare delivery infrastructure, comprehensive EPA and state regulatory frameworks, and increased healthcare provider awareness regarding the importance of compliant waste disposal. Drivers include ubiquitous use of standardized sharps containers, an advanced waste treatment facility network, growing hospital waste generation and greater acceptance of outsourced waste management services stemming from liability concerns. At the same time, various government enforcement actions, OSHA bloodborne pathogen standards and enormous investments in environmental compliance from healthcare systems are anchoring medical waste management services in the market, and ensuring multibillion dollar revenues around the world.

Need any customization research on Healthcare Waste Management Market - Enquiry Now

Asia Pacific Healthcare Waste Management Market Insights:

Asia Pacific is the fastest-growing segment in the healthcare waste management market with a CAGR of 9.68%, as the awareness about proper biomedical waste disposal, government regulatory framework development, and healthcare infrastructure expansion in developing nations is growing. Factors including rapid hospital construction, rising medical tourism with increased waste generation, and growing adoption of international waste management standards are stimulating the market growth. Public health initiatives and environmental protection campaigns have been instrumental in improving waste segregation practices, especially in countries with emerging healthcare systems. Government investment in treatment facility development and private sector partnerships also help in advancing waste management capabilities and regulatory enforcement. Increase in demand in Asia Pacific region owing to rising healthcare expenditure against historical spending levels and growing affordability and accessibility of professional waste management services.

Europe Healthcare Waste Management Market Insights:

The healthcare waste management market in Europe is the second-dominating region after North America on account of an increase in the adoption of EU waste framework directives, robust environmental protection regulations including clinical waste management laws, and increasing sustainability initiatives across healthcare systems. Rising implementation of extended producer responsibility programs, advanced waste treatment technology deployment, favorable government funding for green healthcare projects, and cross-border waste shipment regulations are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Healthcare Waste Management Market Insights:

In Latin America, and Middle East & Africa, the growing healthcare sector modernization and increase in regulatory framework establishment with international standard adoption support the healthcare waste management market growth. The rising popularity of affordable waste treatment solutions and regional waste management company development, along with public health awareness campaigns, will aid environmental protection and infection control. The increasing urban population and improving healthcare access in these regions are continuing to encourage market growth.

Healthcare Waste Management Market Competitive Landscape:

Stericycle, Inc. (est. 1989) is a leading medical waste management and compliance services provider that focuses on integrated healthcare environmental solutions for safe waste disposal. It uses its comprehensive service network and regulatory expertise to produce cutting-edge waste management technology with seamless healthcare facility operations integration.

-

In February 2025, it expanded its sustainable healthcare waste management capabilities with advanced recycling programs and waste-to-energy conversion services, aiming to improve environmental performance and circular economy integration across its healthcare client base.

Veolia Environnement S.A. (est. 1853) is a well-known global environmental services company focused on water management, waste treatment, and energy services. It invests in comprehensive medical waste disposal platforms and sustainable treatment technologies with the hopes of revolutionizing healthcare environmental management with secure, efficient, and environmentally responsible waste solutions.

-

In May 2024, launched an enhanced healthcare waste tracking and treatment system featuring digital waste manifest technology and automated compliance reporting capabilities across European healthcare markets, enhancing waste chain of custody, regulatory compliance, and environmental protection.

Clean Harbors, Inc. (est. 1980) is a leading environmental and industrial services provider in the fields of hazardous waste management, emergency response, and recycling services. The company's healthcare waste management product portfolio focuses on comprehensive disposal solutions and regulatory compliance support, and features a strong commitment to safety and continuous innovation to complement the strong market presence in both hospital and pharmaceutical settings.

-

In September 2024, introduced advanced pharmaceutical waste destruction and controlled substance disposal services for its healthcare waste management platform, strengthening specialized treatment capabilities and expanding adoption among hospitals and long-term care facilities.

Healthcare Waste Management Market Key Players:

-

Stericycle, Inc.

-

Veolia Environnement S.A.

-

Clean Harbors, Inc.

-

SUEZ SA

-

Waste Management, Inc.

-

Republic Services, Inc.

-

Sharps Compliance Corp.

-

BioMedical Waste Solutions, LLC

-

Daniels Sharpsmart Inc.

-

Remondis SE & Co. KG

-

BWS Incorporated

-

GRP & Associates, Inc.

-

MedPro Disposal

-

Triumvirate Environmental

-

Gamma-Service Recycling GmbH

-

PHS Group

-

Initial Medical Services (Rentokil Initial)

-

SRCL Limited

-

EcoMed Services

-

Advanced Disposal Services (acquired by Waste Management)

-

MedWaste Management

-

WM Healthcare Solutions

-

Citiwaste

-

EnviroServ Holdings

-

Fluence Corporation Limited

| Report Attributes | Details |

|---|---|

|

Market Size in 2025 |

US$ 40.02 Billion |

|

Market Size by 2035 |

US$ 89.32 Billion |

|

CAGR |

CAGR of 8.36% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Service (Collection, transport and storage services, Treatment & disposal services and Recycling services) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe[ Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Stericycle, Inc., Veolia Environnement S.A., Clean Harbors, Inc., SUEZ SA, Waste Management, Inc., Republic Services, Inc., Sharps Compliance Corp., BioMedical Waste Solutions, LLC, Daniels Sharpsmart Inc., Remondis SE & Co. KG, BWS Incorporated, GRP & Associates, Inc., MedPro Disposal, Triumvirate Environmental, Gamma-Service Recycling GmbH, PHS Group, Initial Medical Services (Rentokil Initial), SRCL Limited, EcoMed Services, Advanced Disposal Services (acquired by Waste Management), MedWaste Management, WM Healthcare Solutions, Citiwaste, EnviroServ Holdings, Fluence Corporation Limited. |

Frequently Asked Questions

Ans: The Healthcare Waste Management Market was valued at USD 40.02 Billion in 2025.

Ans: The expected CAGR of the Global Healthcare Waste Management Market during the forecast period is 8.36%

Ans: Offsite Treatment held the largest share in the Healthcare Waste Management Market in 2025.

Ans: The Healthcare Waste Management Market will be valued at USD 89.32 Billion in 2035.

Ans: The North America led Healthcare Waste Management Market.

Get in Touch