House Call Market Report Scope & Overview:

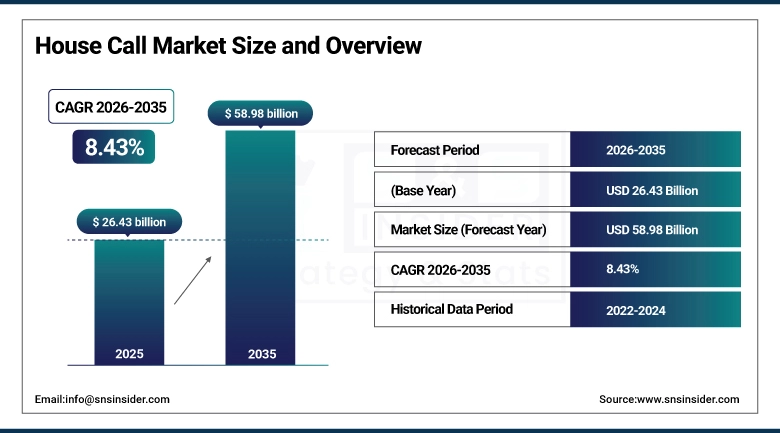

The House Call Market size is valued at USD 26.43 Billion in 2025 and is projected to reach USD 58.98 Billion by 2035, growing at a CAGR of 8.43% during the forecast period 2026–2035.

The House Call Healthcare Market report offers in-depth analysis of market dynamics, service innovations, and therapeutic uses. The demand for elderly care services, prevalence of lifestyle disorders, increasing trend of telemedicine-based house calls, and development of healthcare infrastructure are contributing to strong growth in the market during 2026-2035.

House call services have recorded more than 500 million users in 2025, driven by increasing elderly populations, lifestyle disorders, and personalized healthcare services.

Market Size and Forecast:

-

Market Size in 2025: USD 26.43 Billion

-

Market Size by 2035: USD 58.98 Billion

-

CAGR: 8.43% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on House Call Market - Request Free Sample Report

House Call Market Trends:

-

A rise in demand for home-based care services due to patients’ desire for convenience and personalized care.

-

Swift integration of telemedicine services with house call services.

-

A rise in demand for elderly care services due to an increase in aging populations.

-

The availability of more portable diagnostic kits with point-of-care testing during house calls.

-

The integration of mobile health apps in scheduling, monitoring, and follow-up care services.

-

A strong focus on chronic care management with regular house call check-ups.

-

The development of AI-based tools for more efficient triage services.

-

A high rate of patient satisfaction with house call services compared to traditional clinic visits.

-

A shortage of trained professionals in rural and underserved areas.

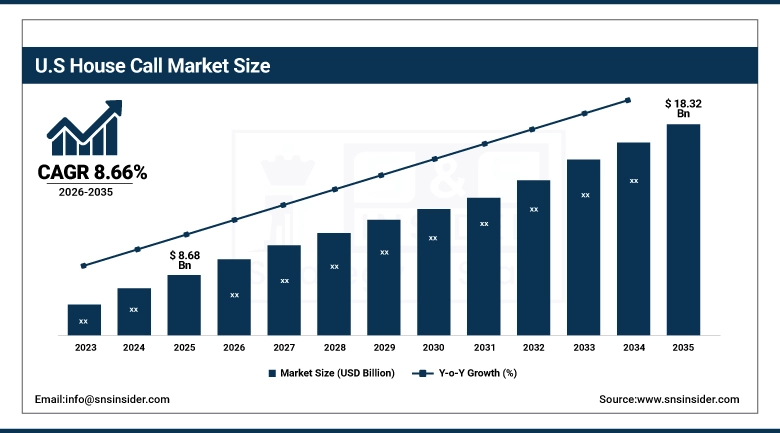

U.S. House Call Market Insights:

The U.S. House Call Healthcare Market size is expected to grow from USD 8.68 Billion in 2025 to USD 18.32 Billion in 2035, growing at a CAGR of 8.66%. The growth of the market is primarily attributed to the increasing need for elderly care, the rise of chronic and lifestyle diseases, and the adoption of telemedicine-based house calls, along with investments in cutting-edge mobile health platforms, portable diagnostic kits, and hybrid care models in hospital, clinic, and home-based settings.

House Call Market Growth Drivers:

-

Rising patient preference for personalized, home‑based care and the growing burden of chronic diseases are key drivers of House Call Market growth.

Hospitals, specialty clinics, and home healthcare facilities are increasingly embracing a new form of hybrid care that brings together telemedicine, mobile health, and in-person interactions. The evolution of portable diagnostic tools, EHR integration, and AI-based scheduling tools is not only boosting efficiency and lowering costs but also augmenting patient compliance. The innovations are speeding up adoption, clinical success, and growth of house calls in a wide range of healthcare facilities.

Over 60% of hospitals, specialty clinics, and home healthcare facilities used house call services in 2025.

House Call Market Restraints:

-

Limited reimbursement frameworks and inconsistent insurance coverage are major restraints for the House Call Market.

Currently, most payers do not consider it essential and offer partial reimbursement. This hinders the adoption of the services by patients and providers. The high costs of operations, such as logistics, human resources, and technology integration, are also issues that hinder the expansion of the services. The issues of data security and patient privacy regarding digital health technologies are also issues that hinder the expansion of the services. In addition, the cultural values of some populations in the country are hospital-based. This hinders the adoption of the services.

More than 40% of healthcare organizations experienced reimbursement and/or regulatory issues in 2025.

House Call Market Opportunities:

-

Expanding digital health infrastructure and rising consumer demand for personalized care present significant opportunities for the House Call Market.

The rising trend of smartphone, health apps, and wearable devices is facilitating integration with home visits, which is creating new models of preventive and chronic management. Increasing investment in AI-based diagnosis, portable imaging, and point of care testing is creating an opportunity for home-based healthcare delivery. Various initiatives in home-based healthcare are opening doors for its adoption. These trends are creating accessibility, reducing healthcare costs, and positioning house call services as an essential part of healthcare delivery.

More than 65% of healthcare organizations in 2025 have recognized digital health integration and portable diagnostics as an opportunity for house call service delivery.

House Call Market Segmentation Analysis:

-

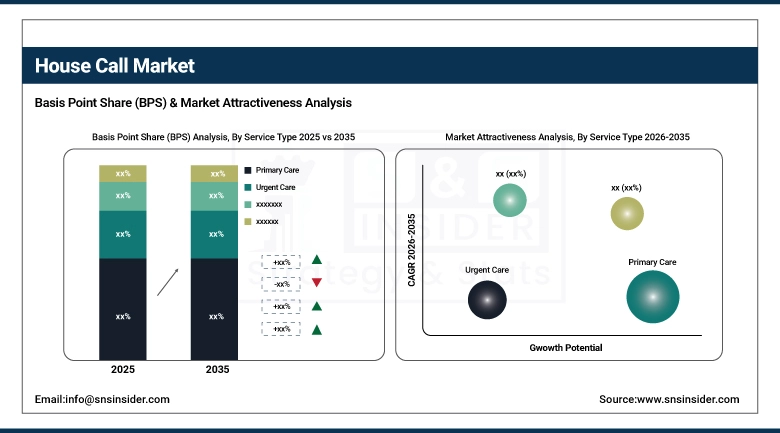

By Service Type, Primary Care held the largest market share of 34.28% in 2025, while Telemedicine + Hybrid House Calls are expected to grow at the fastest CAGR of 9.45% during 2026–2035.

-

By Provider Type, Physicians dominated with 41.54% market share in 2025, whereas Nurse Practitioners are projected to record the fastest CAGR of 11.64% through 2026–2035.

-

By Payment Mode, Insurance (Private + Medicare/Medicaid) accounted for the highest market share of 72.82% in 2025, while Out-of-Pocket are expected to grow at the fastest CAGR of 5.89 during the forecast period.

-

By Age Group, Adults (19–64) held the largest share of 41.85% in 2025, while Geriatric (65+) are expected to grow at the fastest CAGR of 16.02% during the forecast period.

By Service Type, Primary Care Dominates While Telemedicine & Hybrid House Calls Grow Rapidly:

Primary Care segment accounted for the dominated share in the market due to its importance in handling routine check-ups, preventive measures, and monitoring of chronic conditions. In 2025, millions of patients benefited from house call primary care services, which indicated strong consumer preference for personalized treatment in the comfort of their own home.

The Telemedicine & Hybrid House Calls segment recorded fastest growth in the market due to increasing digital health technologies and artificial intelligence triage. Utilization of these house call services recorded strong growth due to consumer adoption of these models for urgent care, chronic condition management, and follow-up visits.

By Provider Type, Physicians Dominate While Nurse Practitioners Grow Rapidly:

Physicians dominated the market share due to their established position in providing extensive medical care, diagnosis, treatment planning, and managing complex conditions through house calls. In the year 2025, the majority of home visits were performed by physicians, indicating the trust and confidence that patients had in their abilities to provide care for their acute and chronic conditions.

Nurse Practitioners were the fastest-growing segment, primarily due to the increasing need for accessible, cost-effective, and patient-centered care. There was a surge in the utilization of nurse practitioners in the year 2025, who were providing care through home visits.

By Payment Mode, Insurance Dominates While Out‑of‑Pocket Expands Rapidly:

The Insurance (Private + Medicare/Medicaid) segment was the dominant market leader, with strong institutional support for reimbursing home-based care services. Primary care visits, chronic condition management, and recovery from surgery through house calls encouraged widespread adoption of the service.

The Out-of-Pocket payment type witnessed the fastest growth as a segment, with increasing consumer willingness to pay for customized, on-demand healthcare services. Patients are seeking urgent care visits, wellness visits, and house calls outside of insurance, which encouraged widespread adoption of the service in 2025.

By Age Group, Adults Dominate While Geriatric Patients Grow Rapidly:

Adults (19-64) segment had the dominated share in 2025, driven by high demand for preventive care services, management of chronic conditions, and urgent medical services provided at home. This group of patients also used house call services due to their busy lifestyle, which reduced hospital visits.

The geriatric (65+) patients' segment recorded the fastest growth rate. This is attributed to the increase in the number of elderly patients with co-morbid conditions. In 2025, there was high utilization of home-based care services by elderly patients due to their inability to move around.

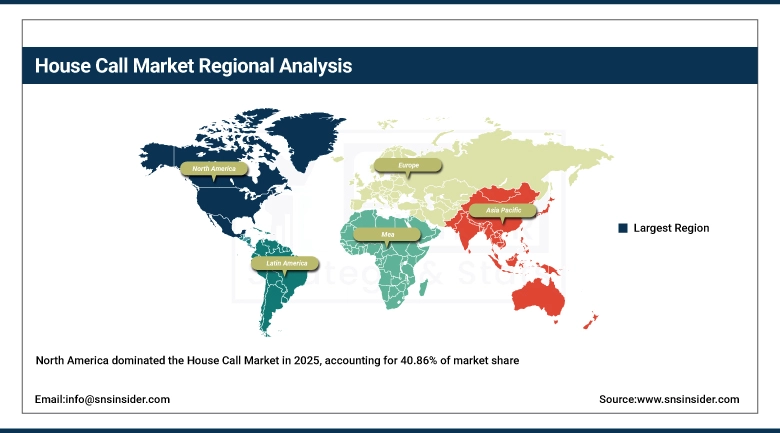

House Call Market Regional Analysis:

North America House Call Market Insights:

The North America House Call Market retained its position in 2025 with 40.86% market share, backed by advanced healthcare facilities and strong integration of telemedicine solutions in the US and Canadian regions. Increasing needs for chronic disease management, elderly care, and emergency medical services in home settings boosted the market. Ongoing advancements in portable diagnostic solutions, AI-based scheduling, and supportive reimbursement models have further helped North America sustain its strong position. Established companies and increasing patient preference for personalized healthcare also helped North America emerge as an evolved market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. House Call Market Insights:

The market in the United States is driven by high demand due to patients seeking convenience, high penetration of digital health platforms, and strong provider networks that offer hybrid models of care. The increase in lifestyle-related disorders, coupled with an aging population, is also contributing to the growth of house call services. Policy efforts in supporting home-based care, insurance reforms, and high adoption rates of portable diagnostic kits have further cemented the United States as the largest market in North America.

Asia-Pacific House Call Market Insights:

The Asia Pacific House Call Market is the fastest growing segment with a CAGR of 12.24%, and this is due to the rapid growth in urbanization and the increasing healthcare spend. Countries such as India, China, and Japan are experiencing high demand for home-based care services, especially for the management of chronic conditions and geriatric care. The increasing penetration of mobile health services and the increasing government initiatives to improve access to healthcare services are also contributing to the growth.

China House Call Market Insights:

The China House Call Market is witnessing tremendous growth with increasing urbanization, healthcare expenditure, and government initiatives in enhancing healthcare services. The demand for chronic disease management and elderly care services is fueling the adoption of home-based healthcare services. The integration of mobile healthcare services, telemedicine, and AI-based diagnostics is revolutionizing the way healthcare services are delivered.

Europe House Call Market Insights:

The Europe House Call Market is driven by home health programs backed by governments, an increasing geriatric population, and an emphasis on preventive healthcare. Countries such as Germany, the U.K., and France are driving the market in terms of home healthcare providers and the inclusion of teleconsultation. Patient demands for fewer hospital visits and cost-effective models are contributing to the adoption of house call models. Government support and digital health investments are further contributing to the steady growth of the European market.

Germany House Call Market Insights:

The Germany House Call Market is marked by an established healthcare system, focus on preventive healthcare, and government backing for home healthcare programs. The demand for house call services is fueled by an aging population and the prevalence of chronic conditions. The integration of teleconsultation tools, portable diagnostic tools, and electronic health records is also helping in making house call services more efficient.

Latin America House Call Market Insights:

The Latin America House Call Market is growing steadily with an increasing healthcare infrastructure and patient need for affordable and accessible healthcare. Brazil and Mexico are leading in house call adoption, with an increasing reliance on house calls for chronic disease management and urgent care. There are challenges in terms of workforce availability and reimbursement models, but patient education and digital health are key growth drivers.

Middle East & Africa House Call Market Insights:

Middle East & Africa House Call Market is in an emerging state with more investments in healthcare infrastructure. There is also an increase in demand for personalized care solutions. Gulf countries, including Saudi Arabia and the UAE, have high adoption rates with strong government initiatives. However, in Africa, adoption is low due to infrastructure constraints. Mobile health platforms have created opportunities for expansion.

House Call Market Competitive Landscape:

DispatchHealth is an urgent medical care provider based in the United States, which specializes in providing in-home urgent medical care services to patients and serves as an alternative to emergency room visits. The investment firm’s portfolio is characterized by convenience, cost-effectiveness, and quality of care, and its services include acute illness management and transitional care, among others. The investment in expanding operations and care coordination makes DispatchHealth a strong competitor in the house call healthcare market.

-

In September 2025, DispatchHealth expanded its hospital-at-home partnerships with major health systems, enhancing access to acute care at home and reducing ER utilization.

Heal is a California-based healthcare technology firm that specializes in house calls and telehealth for adults and children. The firm, which was founded in 2014, primarily focuses on primary care, preventive care, and elder care, especially for Medicare and Medicare Advantage patients. The firm’s technology-enabled model incorporates telemedicine, telehealth monitoring, and mobile technology to provide personalized care. The firm’s focus on elder care and its expansion into new states highlight its contribution to house call healthcare.

-

In August 2025, Heal expanded its service footprint to Illinois, Louisiana, North Carolina, and South Carolina, strengthening its national presence and Medicare-focused offerings.

Teladoc Health is a New York-based virtual care and telehealth leader that covers over 175 countries. Although it is most recognized in the digital health industry, it offers house call services via partnerships and hybrid models. The services provided by Teladoc range across primary care, chronic condition management, mental health services, dermatology, and expert medical opinions. The organization has focused on data-based personalization and clinical quality and global reach. The acquisition of Livongo and BetterHelp has been strategic in positioning the organization as the leader in the house call and telehealth industry.

-

In May 2025, Teladoc advanced its chronic care programs, expanding GLP‑1 prescription support for diabetes and obesity management, while enhancing hybrid models that combine virtual and in-home care.

House Call Market Key Players:

Some of the House Call Market Companies are:

-

DispatchHealth

-

Heal

-

Teladoc Health

-

Visiting Physicians Association (VPA, part of U.S. Medical Management)

-

Housecall Providers (CareOregon)

-

SOS Doctors

-

TruDoc HealthCare

-

AT HOME DOCTORS

-

Heally

-

HealWell24

-

Home Doctor 24h

-

House Call Doctor

-

Med2U Inc.

-

MedHouseCall

-

My Doctor Medical Group

-

Doctor On Demand

-

Pager

-

MDLIVE

-

Amwell

-

Homedoctor24

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 26.43 Billion |

| Market Size by 2035 | USD 58.98 Billion |

| CAGR | CAGR of 8.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Primary Care, Urgent Care, Telemedicine + Hybrid House Calls, Specialty Care, Palliative Care, Others), • By Provider Type (Physicians, Nurse Practitioners, Physician Assistants, Physical Therapists, Mental Health Professionals, Others), • By Payment Mode (Insurance (Private + Medicare/Medicaid), Out-of-Pocket, Government-funded Programs, Employer-sponsored & HSAs, Others), • By Age Group (Adults (19–64), Geriatric (65+), Paediatric (0–18)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DispatchHealth, Heal, Teladoc Health, Visiting Physicians Association (VPA, part of U.S. Medical Management), Housecall Providers (CareOregon), SOS Doctors, TruDoc HealthCare, AT HOME DOCTORS, Heally, HealWell24, Home Doctor 24h, House Call Doctor, Med2U Inc., MedHouseCall, My Doctor Medical Group, Doctor On Demand, Pager, MDLIVE, Amwell, Homedoctor24. |

Frequently Asked Questions

Key innovations include AI-driven care coordination, mobile health apps, remote monitoring devices, and digital platforms that streamline scheduling, diagnostics, and follow-up care, making house calls more efficient and scalable.

Telemedicine-integrated house calls are the fastest-growing segment, with a CAGR of 9.45%, as hybrid models combining virtual consultations with in-person visits gain popularity.

Primary care services dominate, representing 34.28% of the market by 2035, as routine checkups, chronic disease management, and preventive care are the most common reasons for house calls.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 12.24% (2025–2035). Urbanization, rising middle-class healthcare spending, and rapid adoption of telemedicine-enabled house calls fuel this growth.

North America holds the largest share, accounting for about 40.86% of the market by 2035, driven by strong insurance coverage, advanced infrastructure, and high demand for elderly and chronic care services.

Get in Touch