Mobile C-arm Market Report Scope & Overview:

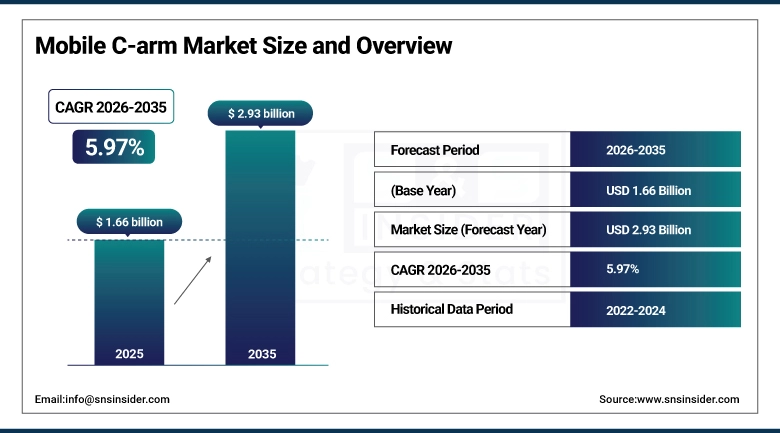

The Mobile C-arm Market size is valued at USD 1.66 Billion in 2025 and is projected to reach USD 2.93 Billion by 2035, growing at a CAGR of 5.97% during the forecast period 2026–2035.

The Mobile C-Arm Market analysis report offers an overview of market dynamics, product developments, and clinical applications. The increasing demand for minimally invasive procedures, an increase in orthopaedic and cardiovascular procedures, the use of flat panel detector technology, and an increase in surgical infrastructure are driving the market for the period 2026-2035.

The use of mobile C-arms crossed 2 million in 2025, with increasing surgical volumes and the adoption of advanced imaging technologies in hospitals and surgical centers.

Market Size and Forecast:

-

Market Size in 2025: USD 1.66 Billion

-

Market Size by 2035: USD 2.93 Billion

-

CAGR: 5.97% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Mobile C-arm Market - Request Free Sample Report

Mobile C-arm Market Trends:

-

High adoption rate of flat panel detectors replacing image intensifiers.

-

Increasing requirement for 3D/4D imaging in neurosurgery cases and orthopaedic reconstruction.

-

Increasing preference for mini C-arms in outpatient orthopaedic settings and ambulatory surgical facilities.

-

Strong growth in portable and modular C-arms for smaller hospitals and regional facilities.

-

Increasing adoption of dose optimization technologies to lower patient dose.

-

Increasing adoption of AI technologies in imaging for precision in surgery.

-

Increasing significance of hybrid operating rooms with integrated C-arms.

-

Increasing adoption of low-dose imaging systems due to regulatory and safety concerns.

-

Increasing adoption of digital connectivity and monitoring technologies.

U.S. Mobile C-arm Market Insights:

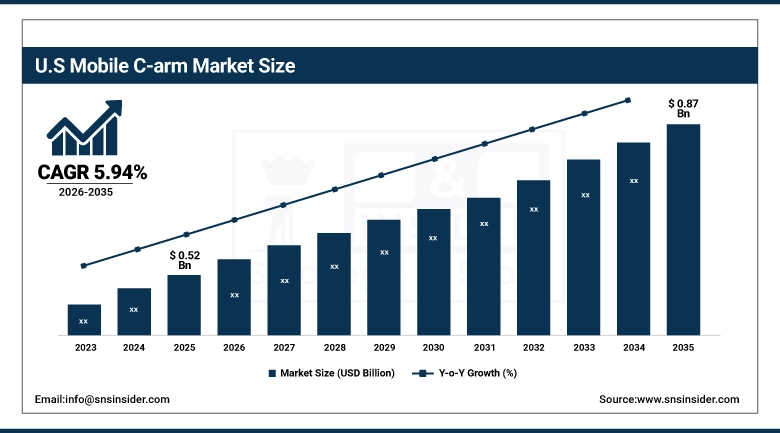

The U.S. Mobile C-arm market is projected to grow from USD 0.52 billion in 2025 to USD 0.87 billion by 2035, registering a CAGR of 5.94%. Growth is fueled by the rising number of surgical procedures, increasing demand for minimally invasive treatments, and strong adoption of flat-panel detector technology. Growing emphasis on patient safety, dose optimization, and AI-driven imaging analytics is enhancing clinical outcomes, reinforcing the U.S. as a leading market for Mobile C-arm systems.

Mobile C-arm Market Growth Drivers:

-

The U.S. Mobile C-arm market is experiencing rapid expansion, driven by rising surgical volumes in orthopedics, cardiovascular, and neurosurgery.

Hospitals and surgical centers are increasingly adopting Mobile C-arm systems to enhance precision and efficiency in complex procedures. The growing preference for minimally invasive surgeries is accelerating demand, as these systems provide real-time imaging that supports safer and faster interventions. Expanding use of hybrid operating rooms and portable modular systems is further driving adoption, particularly in outpatient and regional facilities with in flat-panel detector technology, integration of 3D/4D reconstruction, and AI-powered workflow optimization.

By 2025, more than 58% of hospitals and surgical centers had already installed advanced Mobile C-arm systems, indicating the market’s robust growth trajectory.

Mobile C-arm Market Restraints:

-

Despite strong growth prospects, the U.S. Mobile C-arm market faces several restraints that could slow adoption.

The high capital costs of advanced imaging technologies are an important factor for hospitals and clinics. Regulatory requirements, such as FDA approvals, can also affect product development, leading to higher costs. The availability of skilled personnel to operate the advanced imaging systems, coupled with the requirement for special training, can affect the efficient use of such technologies. The issues of radiation exposure, despite the availability of dose optimization technologies, have also been an area of concern.

In 2025, financial or operational issues were identified by 42% of hospitals and clinics, which affected their ability to use advanced Mobile C-Arm systems.

Mobile C-arm Market Opportunities:

-

The U.S. Mobile C-arm market presents significant opportunities as healthcare systems increasingly invest in advanced imaging technologies to support minimally invasive and complex surgical procedures.

The increasing demand for hybrid operating rooms, and the integration of robotic-assisted surgery systems, is creating new market growth opportunities. Expanding use cases for portable and modular C-arms are creating opportunities in smaller hospitals, outpatient facilities, and regional hospitals. Advances in AI imaging, 3D/4D reconstruction and dose optimization are improving the precision of surgical procedures, creating new market growth opportunities for premium product offerings.

There exists significant growth potential in the market, as in 2025, about 47% of hospitals and surgical centers are expected to increase their investment in Mobile C-Arm systems.

Mobile C-arm Market Segmentation Analysis:

-

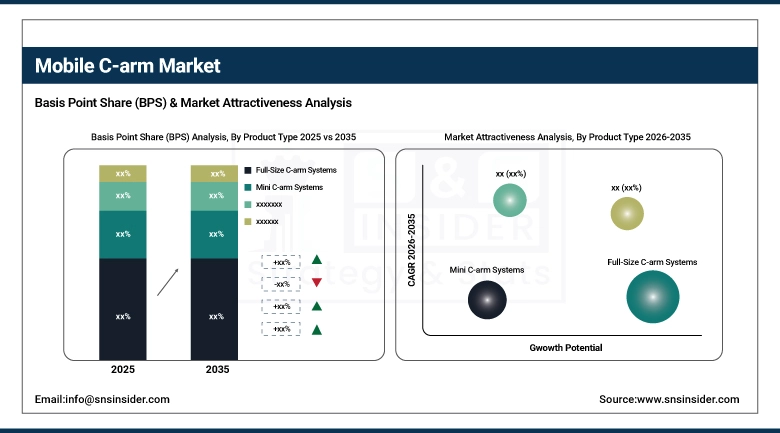

By Product Type, Full-Size C-arm Systems held the largest market share of 70.63% in 2025, while Mini C-arm Systems are expected to grow at the fastest CAGR of 6.22% during 2026–2035.

-

By Application, Orthopaedic Surgeries dominated with 38.54% market share in 2025, whereas Cardiovascular Surgeries are projected to record the fastest CAGR of 4.66% through 2026–2035.

-

By Technology, Flat Panel Detectors (FPD) accounted for the highest market share of 62.53% in 2025, while Low-Dose Systems are expected to grow at the fastest CAGR of 7.19% during the forecast period.

-

By End User, Hospitals held the largest share of 66.74% in 2025, while Ambulatory Surgical Centers (ASCs) are expected to grow at the fastest CAGR of 6.34% during the forecast period.

By Product Type, Full-Size C-arm Systems Lead While Mini C-arm Systems Accelerate Rapidly:

Full-size C-arm systems have led the way as dominant position in the US market in 2025, as these devices are commonly used for complex surgeries in hospital settings and specialty surgical centers. The reliability and quality imaging capabilities of full-size C-arm systems have led to a significant clinical adoption rate.

Mini C-arm systems are expected to be the fastest-growing segment of the C-arm market, as there is a growing need for these devices in outpatient orthopaedic clinics and ambulatory surgical centers. The need for extremity imaging and the lower costs of these devices is expected to increase the adoption rate of these devices.

By Application, Orthopaedic Surgeries Lead While Cardiovascular Surgeries Expand Rapidly:

Orthopaedic surgeries were the most dominant type in the Mobile C-Arm market, which is due to their wide use in trauma cases, joint replacements, and extremity imaging. Hospitals, and specialty clinics, depend on full-size and mini C-Arm systems for accurate, real-time imaging, which enhances the precision of the surgery.

Cardiovascular surgeries, on the other hand, are expected to grow significantly in the market. The prevalence of heart diseases is increasing, and there is an increase in the number of minimally invasive procedures for such cases, which demands better imaging facilities with advanced C-Arm systems.

By Technology, Flat Panel Detectors Lead While Low-Dose Systems Gain Momentum:

Flat Panel Detector (FPD) technology is said to have been the dominant technology in the Mobile C-arm market in 2025. This is attributed to its capacity for delivering high-quality images, faster processing, and reduced radiation doses in comparison with image intensifiers. The hospital and specialty clinic segments have been using FPD technology in complex orthopaedic, cardiovascular, and neurosurgical procedures, further enhancing its popularity.

Low-dose systems have been recognized as the fastest-growing technology in the Mobile C-arm market. This is attributed to the increasing regulatory focus on patient safety, concerns regarding radiation risks, and the need for safer solutions in outpatient and paediatric environments.

By End User, Hospitals Lead While Ambulatory Surgical Centers Expand Rapidly:

Hospitals emerged as the dominated end-user market in 2025, given their heavy dependence on full-size Mobile C-arm systems in complex procedures in orthopaedic, cardiovascular, and neurosurgical cases. Their capacity to spend on advanced imaging technologies and integrate them in hybrid ORs has further solidified their position as the largest end-user market.

Ambulatory Surgical Centers (ASCs) are also expected to emerge as the fastest-growing end-user market in the near future, given the rising trend of outpatient procedures, the need for cost-effective imaging solutions, and the increasing uptake of mini and portable C-arm systems.

Mobile C-arm Market Regional Analysis:

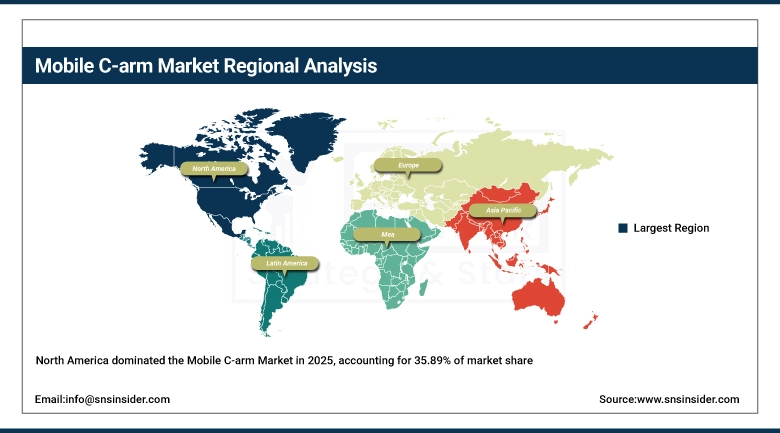

North America Mobile C-arm Market Insights:

The North American Mobile C-Arm Market retained its position in the industry in 2025 with share of 35.89%. The region has an established healthcare infrastructure and high surgical volumes in the United States and Canada. The region also has high adoption rates for flat-panel detector systems and the integration of 3D and 4D imaging. The hospitals and clinics segment are the primary users of the equipment, and ambulatory surgical centers are growing at a rapid rate. The innovations in the product and reimbursement policies are adding strength to the North American market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Mobile C-arm Market Insights:

The U.S. Mobile C-Arm Market is the largest in the North American region. The country has the highest volume of orthopaedic procedures, cardiovascular procedures, and neurosurgeries. The hospitals segment holds the largest share in the U.S. Mobile C-Arm Market. The segment is also expanding in ambulatory surgical centers and outpatient clinics. The increasing demand for hybrid operating rooms and the preference for flat-panel detector technology are fueling the growth of the U.S. Mobile C-Arm Market.

Asia-Pacific Mobile C-arm Market Insights:

The Asia Pacific is the fastest-growing market with CAGR of 7.47%, driven by the increasing healthcare infrastructure, rising surgical cases, and increasing investment in high-end imaging equipment. Countries such as China, India, and Japan are key markets, where demand is high for full-size and mini C-arms. This region is witnessing the adoption of portable and modular C-arm systems in smaller hospitals and clinics. Increasing cases of trauma, orthopaedic disorders, and cardiovascular conditions are also supporting the market.

China Mobile C-arm Market Insights:

China is one of the fastest-growing markets in the Mobile C-Arm industry. The country is witnessing rapid development in healthcare infrastructure. Government spending in modernizing hospitals and the increasing need for minimally invasive procedures is creating opportunities for the adoption of advanced imaging technologies. Both full and mini C-Arm systems are becoming popular in the country. The mini variant is popular in regional hospitals and clinics. The increasing incidence of trauma cases, orthopaedic conditions, and cardiovascular conditions is also contributing to the growth of the market.

Europe Mobile C-arm Market Insights:

The Mobile C-Arm Market in Europe is marked by the adoption of advanced imaging technologies and high levels of regulatory compliance. Countries such as Germany, France, and the U.K. are the highest in terms of installations in orthopaedic and cardiovascular procedures. The demand for dose optimization systems and portable devices in outpatient settings is creating growth opportunities. Government initiatives for modernizing healthcare and patient safety are adding to the positive growth prospects in the region.

Germany Mobile C-arm Market Insights:

Germany is also at the forefront in terms of market share in the European mobile C-arm market. This is mainly due to its highly developed healthcare system. A strong focus on innovative technologies is also an advantage in Germany. Hospitals and specialty clinics form key markets in Germany. Flat panel detectors and dose optimization solutions have been widely accepted in Germany. Orthopaedic procedures, cardiovascular procedures, and neurosurgical procedures also form key markets in Germany. The regulatory standards in Germany ensure high-quality products.

Latin America Mobile C-arm Market Insights:

The Latin America mobile C-arm system market is witnessing a steady growth rate, primarily fueled by the up-gradation of healthcare facilities and the need for cost-effective imaging solutions. Brazil and Mexico are the leading markets for Latin America, where there is a significant adoption of C-arm systems in various hospitals and specialty clinics for precision in surgical procedures. Orthopedic and trauma-related surgeries are the major contributors, whereas cardiovascular and neurological cases are slowly picking up.

Middle East and Africa Mobile C-arm Market Insights:

Middle East & Africa's Mobile C-arm market is growing steadily. The growth of surgical cases and investments in the modernization of the healthcare industry are contributing factors. The countries that are contributing to this growth are Saudi Arabia, UAE, and South Africa. Hospitals are increasingly acquiring full-size C-arms for complex surgeries. The popularity of portable and low-dose C-arms is increasing in hospitals and specialty clinics, especially where cost and patient safety are of primary concern.

Mobile C-arm Market Competitive Landscape:

Siemens Healthineers, a German medical device manufacturer, dominates the Mobile C-arm industry, especially in the area of premium imaging technologies, as seen in products such as the Cios line. The company's key advantages stem from its expertise in precision imaging, its commitment to patient safety, and its ability to streamline workflow. The investments that Siemens makes in flat panel detectors, dose optimization, and artificial intelligence-based imaging analytics are expected to drive growth for the company in the surgical imaging industry.

-

In May 2025, Siemens Healthineers launched the Cios Flow system, designed to enhance flexibility and efficiency in routine surgical imaging, expanding its portfolio for hospitals and outpatient centers.

The GE Healthcare is medical technology company, which is based in the USA, is an important player in the market for Mobile C-arms with their OEC line of surgical imaging systems. The product line from GE is centered on reliability, portability, and imaging quality, which are all widely used in hospitals and ambulatory surgical centers. GE’s investment in low-dose imaging, portable modular systems, and digital connectivity platforms only strengthens their leadership in surgical imaging solutions.

-

In July 2025, GE Healthcare introduced upgrades to its OEC Elite C-arm platform, integrating enhanced dose management and connectivity features to improve patient safety and surgical workflow efficiency.

Philips Healthcare, with its headquarters in the Netherlands, is a leader in providing medical imaging and surgical solutions. Philips has a strong presence in the Mobile C-Arm Market. Philips' product portfolio is focused on delivering innovations in hybrid operating room solutions, advanced flat panel detector solutions, and digital surgical solutions. Philips' emphasis on AI-assisted imaging and real-time analytics helps the company sustain its competitive advantage in complex surgical procedures.

-

In September 2025, Philips Healthcare expanded its Zenition Mobile C-arm series, introducing AI-powered workflow enhancements and improved imaging quality to support orthopaedic and cardiovascular procedures.

Mobile C-arm Market Key Players:

Some of the Mobile C-arm Market Companies are:

-

Siemens Healthineers

-

GE Healthcare

-

Philips Healthcare

-

Ziehm Imaging

-

Canon Medical Systems

-

Hologic Inc.

-

Shimadzu Corporation

-

Medtronic

-

Carestream Health

-

Fujifilm Holdings Corporation

-

Orthoscan Inc.

-

Toshiba Medical Systems (now Canon Medical)

-

Hitachi Medical Systems

-

Varian Medical Systems

-

Eurocolumbus S.r.l.

-

Allengers Medical Systems Ltd.

-

Trivitron Healthcare

-

Mindray Medical International

-

United Imaging Healthcare

-

BMI Biomedical International

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.66 Billion |

| Market Size by 2035 | USD 2.93 Billion |

| CAGR | CAGR of 5.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Full-Size C-arm Systems, Mini C-arm Systems, Hybrid / Advanced Systems, Others), • Application (Orthopaedic Surgeries, Cardiovascular Surgeries, Neurosurgeries, Gastrointestinal Surgeries, Others), • Technology (Flat Panel Detectors (FPD), Image Intensifiers, 2D Imaging, 3D/4D Imaging, Low-Dose Systems, Others), • End User (Hospitals, Ambulatory Care Centers, Specialty Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens Healthineers, GE Healthcare, Philips Healthcare, Ziehm Imaging, Canon Medical Systems, Hologic Inc., Shimadzu Corporation, Medtronic, Carestream Health, Fujifilm Holdings Corporation, Orthoscan Inc., Toshiba Medical Systems (now Canon Medical), Hitachi Medical Systems, Varian Medical Systems, Eurocolumbus S.r.l., Allengers Medical Systems Ltd., Trivitron Healthcare, Mindray Medical International, United Imaging Healthcare, BMI Biomedical International. |

Frequently Asked Questions

Flat Panel Detector (FPD) systems offering superior image quality and reduced radiation exposure, while low-dose systems are emerging as the fastest-growing technology due to rising patient safety concerns.

Cardiovascular surgeries are the fastest-growing application with 4.66% CAGR, fueled by increasing prevalence of heart disease and adoption of minimally invasive cardiac procedures.

Orthopaedic surgeries hold the largest share of 38.54%, reflecting high utilization in trauma cases, joint replacements, and extremity imaging.

Mini C-arm systems are the fastest-growing with CAGR of 6.22%, driven by rising demand in outpatient orthopaedic clinics and ambulatory surgical centers for extremity imaging and routine procedures.

Full-size C-arm systems dominate with market share of 70.63% due to their extensive use in hospitals and specialty clinics for complex procedures such as orthopaedics, cardiovascular interventions, and neurosurgery.

Get in Touch