Cluster Headache Market Report Scope & Overview:

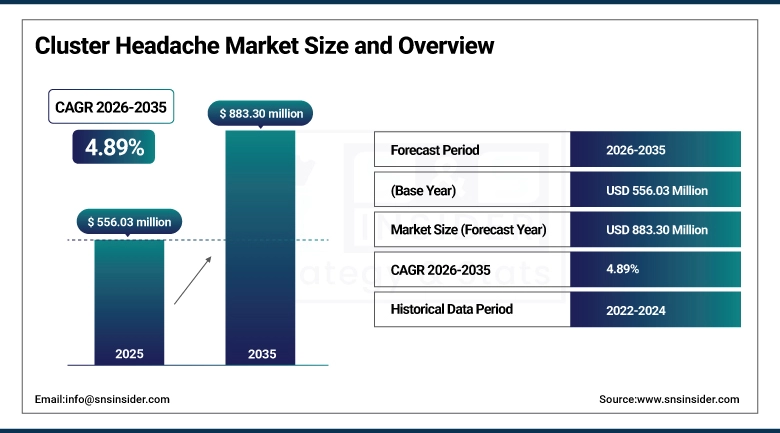

The Cluster Headache Market size is valued at USD 556.03 Million in 2025 and is projected to reach USD 883.30 Million by 2035, growing at a CAGR of 4.89% from 2026-2035.

The Cluster Headache Market analysis report provides a detailed analysis of market dynamics, treatment innovations, and changing therapeutic strategies in the field of acute and preventive treatments. The increasing awareness of rare neurological disorders, diagnostic capabilities, and advanced treatment strategies such as CGRP-targeting drugs and neuromodulation therapy are boosting the Cluster Headache Market growth.

The Cluster Headache Market is expected to grow due to an increasing incidence of episodic and chronic cluster headaches, improving healthcare infrastructure, and an increasing preference for preventive treatments.

Market Size and Forecast:

-

Market Size in 2025: USD 556.03 Million

-

Market Size by 2035: USD 883.30 Million

-

CAGR: 4.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Cluster Headache Market - Request Free Sample Report

Cluster Headache Market Trends:

-

Elevating cluster headache prevalence and diagnosis are the factors contributing to the rising need for cluster headache treatment.

-

Emerging CGRP-targeted therapy use is revolutionizing preventive cluster headache treatment.

-

Emerging neuromodulation devices and oxygen therapy systems are providing patients with additional non-pharmacological options.

-

Emerging acute and preventive cluster headache treatments are providing patients with better options for managing episodic and chronic cluster headache disorders.

-

Emerging specialty neurology practices and infrastructure are providing patients with better access to cluster headache diagnosis and treatment.

-

Emerging patient and physician awareness is driving cluster headache diagnosis and treatment.

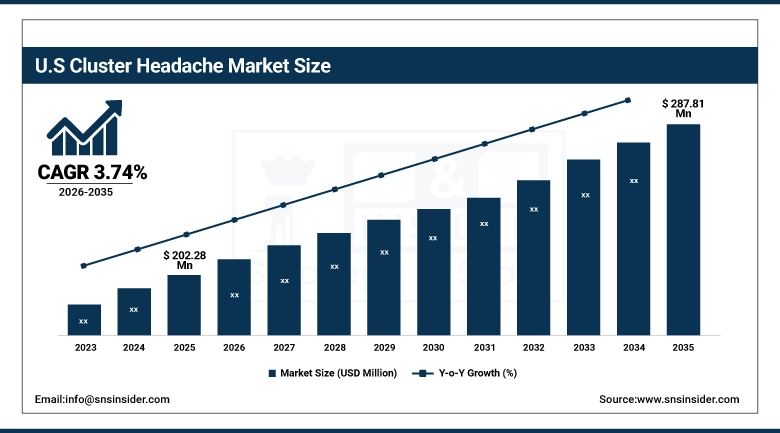

U.S. Cluster Headache Market Insights:

The U.S. Cluster Headache Market is expected to grow at a CAGR of 3.74% during the forecast period, from USD 202.28 million in 2025 to USD 287.81 million in 2035. The growth in the market is due to the increasing number of diagnosed cluster headache cases, the rising awareness of cluster headache patients and their physicians, the high adoption rates of CGRP-targeted therapy, the rising use of neuromodulation and oxygen therapy, and the ongoing growth in neurology services in hospitals and specialty clinics.

Cluster Headache Market Growth Drivers:

-

Rise in prevalence rate of cluster headache patient populations and increase in adoption of advanced treatments.

The rise in diagnosis rates of cluster headache and increased awareness of cluster headache among patients and healthcare providers are some of the factors that are contributing to the growth of Cluster Headache Market. There is a rise in adoption of cluster headache treatments by hospitals and clinics for managing cluster headache attacks and preventive treatments. In addition to this, advancements in pharmacological treatments and cluster headache treatments are also contributing to the growth of Cluster Headache Market.

More than 55% of hospitals, clinics, and homecare facilities adopted advanced cluster headache treatments for managing cluster headache attacks and preventive treatments in 2025.

Cluster Headache Market Restraints:

-

High treatment costs and insurance issues are acting as major hindrances for the widespread adoption of cluster headache treatments.

The high-cost factor associated with advanced treatments such as CGRP-targeting drugs, neuromodulation therapy, and oxygen therapy is acting as one of the key restraining factors for the Cluster Headache Market. In addition, limited insurance coverage in various regions is another factor hindering cluster headache treatments. In addition, dependence on cluster headache treatment, lack of standardization in cluster headache treatment, and affordability issues in cluster headache treatment for patients also act as key hindrances for cluster headache treatments.

Cluster Headache Market Opportunities:

-

Increased adoption of advanced CGRP therapies and neuromodulation devices is offering significant market growth opportunities in the Cluster Headache Market.

The development and commercialization of therapies targeting CGRP and the increased adoption of non-invasive and implantable neuromodulation devices are offering significant market growth opportunities in the Cluster Headache Market. Healthcare providers, such as hospitals and neurology clinics, are increasingly incorporating advanced therapies and neuromodulation devices in the management of cluster headaches. Ongoing innovations in drug delivery systems and the development of new therapies through clinical research studies are offering effective and long-acting therapies for the management of cluster headaches. These innovations are likely to boost the adoption of cluster headache management therapies in the coming years in the healthcare systems of developed and emerging nations.

More than 45% of healthcare providers are incorporating advanced CGRP therapies and neuromodulation devices in 2025 to manage cluster headaches effectively.

Cluster Headache Market Segmentation Analysis:

-

By Type, Chronic Cluster Headache (CCH) held the largest market share of 58.25% in 2025, while Episodic Cluster Headache (ECH) is expected to grow at the fastest CAGR of 6.41% during 2026–2035.

-

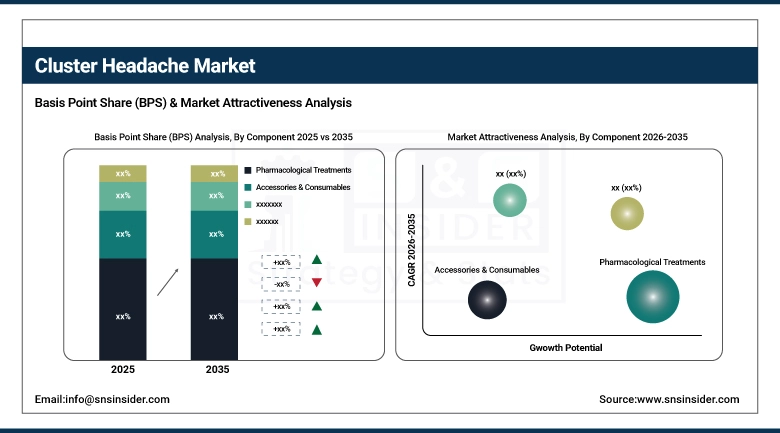

By Component, Pharmacological Treatments dominated with 65.21% market share in 2025, whereas Pharmacological Treatments are expected to grow at the fastest CAGR of 10.54% during 2026–2035.

-

By Technology, Conventional Drug Therapies accounted for the highest market share of 60.25% in 2025, while Neuromodulation Technologies are expected to grow at the fastest CAGR of 10.47% during 2026–2035.

-

By Application / End Use, Acute Attack Management dominated with a 55.12% share in 2025, while Preventive Treatment is anticipated to expand at the fastest CAGR of 9.41% during 2026–2035.

-

By End-User Industry, Hospitals held the largest share of 50.25% in 2025, while Homecare Settings are expected to grow at the fastest CAGR of 7.89% during the forecast period.

By Component, Pharmacological Treatments Dominate While Devices & Therapeutic Equipment Grow Rapidly:

The Pharmacological Treatments segment held the highest share in the market due to the widespread adoption of conventional drugs, CGRP-targeting drugs, and preventive drugs as an initial line of treatment for cluster headache. In 2025, this segment held a share of 65.21% in the market. The segment is fueled by strong adoption rates in hospitals, specialty clinics, and ambulatory care settings, along with strong recommendations from clinical guidelines for drug-based interventions.

Devices & Therapeutic Equipment is another segment in the cluster headache treatment market, which is expected to grow at the highest rate. The segment is fueled by increasing adoption rates for oxygen therapy systems and neuromodulation therapy for both acute and preventive treatment. The increasing preference for non-invasive and adjunctive treatments is driving the adoption rates for cluster headache treatment.

By Type, Chronic Cluster Headache (CCH) Dominates While Episodic Cluster Headache (ECH) Grows Rapidly:

The Chronic Cluster Headache segment has dominated the market, owing to its chronic and long-duration nature, thus requiring continued medical intervention, prevention, and frequent consultation. As of 2025, this segment has a share of 58.25%, owing to higher intensity of treatment, repeat consultation, and utilization of pharmacological and neuromodulatory interventions.

The Episodic Cluster Headache segment is observed to be growing at a higher rate, owing to higher diagnosis rates, patient and physician awareness, and utilization of acute and prevention therapies. An increase in CGRP therapies is seen to be supporting this segment, thus expanding the overall market.

By Technology, Conventional Drug Therapies Dominate While Neuromodulation Technologies Grow Rapidly:

The segment of conventional drug therapies held the largest market size in the segment of the market owing to their long history of usage and their effectiveness in the management of cluster headaches. In the year 2025, the segment of conventional drug therapies held a market share of 60.25%, owing to the widespread usage of conventional drug therapies in the management of cluster headaches in healthcare systems across the globe.

The segment of neuromodulation technologies is the fastest-growing segment of the market owing to the rising usage of non-pharmacological management options such as nerve stimulation devices in the management of cluster headaches.

By Application / End Use, Acute Attack Management Dominates While Preventive Treatment Grows Rapidly:

The Acute Attack Management segment held the highest market share due to the immediate and severe nature of acute attacks associated with cluster headaches. These acute attacks need immediate management using oxygen therapy, triptans, and other immediate pharmacological interventions. In 2025, this segment held a 55.12% market share due to the high dependence of patients on acute management. The recurring nature of acute attacks also increases the need for immediate pain relief, which makes this segment dominate the market.

The Preventive Treatment segment is growing rapidly due to the increasing preference for CGRP-targeting treatments and awareness about long-term management of cluster headaches. In 2025, preventive treatment is witnessing increased usage in clinical settings for chronic cluster headache patients.

By End-User Industry, Hospitals Dominate While Homecare Settings Grow Rapidly:

Hospitals segment has been a major contributor to this market due to their role in diagnosing and treating cluster headache patients. For instance, this segment has been a major contributor to the market in terms of managing acute attacks and oxygen therapy and injectable treatments. In 2025, this segment has a share of 50.25%, and this is attributed to high patient volumes and their reliance on hospital-based treatment approaches.

Homecare Settings is another segment that is growing at a high rate and is attributed to the increased rate of adoption of portable oxygen therapy systems and self-administered medications and telemedicine-based neurology care. In 2025, this segment gained traction due to patient preferences for a convenient and cost-effective solution for managing cluster headache conditions.

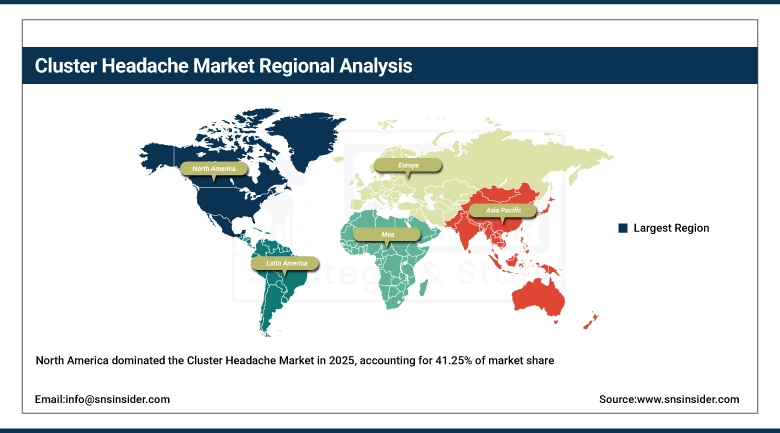

Cluster Headache Market Regional Analysis:

North America Cluster Headache Market Insights:

The North America Cluster Headache Market is dominated by the region with a market share of 41.25% in 2025. This is due to the high number of diagnosed cases of cluster headaches and the well-equipped healthcare infrastructure in the region. In addition, the availability of well-equipped headache clinics in the region is also a major reason for the dominance of the North America Cluster Headache Market. Therefore, the region is the largest market in the cluster headache market and is likely to remain the same in the coming years.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Cluster Headache Market Insights:

The U.S. Cluster Headache Market is driven by the large number of diagnosed cases of cluster headaches and the well-equipped healthcare infrastructure in the region. In addition, the region is also witnessing the adoption of various innovative therapies such as CGRP inhibitors and neuromodulators in the management of cluster headaches. Moreover, the increasing adoption of acute oxygen therapy and the preference for preventive therapies in the management of cluster headaches are also driving the Cluster Headache Market in the region. In addition, the region is also witnessing an improvement in healthcare infrastructure and the accessibility of healthcare services in the region.

Asia-Pacific Cluster Headache Market Insights:

The Asia-Pacific Cluster Headache Market is observed to be the fastest-growing market, with an expected growth rate of 6.36% from 2026-2035. The growth is attributed to increasing awareness of neurological disorders, improvement in diagnostic capabilities, and expansion in healthcare infrastructure in various nations such as China, India, Japan, and South Korea. The increasing adoption of advanced pharmacological treatments, improvement in specialty neurology services, and increasing investments in hospital infrastructure are further driving the growth in the cluster headache market. In addition, increasing patient access, urbanization, and gradual improvements in reimbursement systems are also contributing to the growth in cluster headache in the Asia-Pacific region.

China Cluster Headache Market Insights:

The China Cluster Headache Market is observed to be growing in response to increasing awareness of neurological disorders, improvement in diagnostic rates, and expansion in availability of specialty neurology services. The growth in China is further fueled by increasing availability of CGRP-targeting treatments, gradual adoption of neuromodulation treatments, and increasing adoption rates for oxygen therapy. The expansion in availability of hospital infrastructure, increasing investments in healthcare services, and improvement in specialty clinic services are further driving growth in cluster headache in China.

Europe Cluster Headache Market Insights:

The Europe Cluster Headache Market is influenced by well-established healthcare infrastructure, high diagnosis rates, and a strong neurology specialist base in countries such as Germany, France, and the UK. High adoption rates of CGRP inhibitors, neuromodulation devices, and standardized treatment approaches across all hospitals and clinics are also responsible for the growth of this market. High emphasis is being placed on preventive treatment approaches and therapeutic options, and this is further adding to the growth of this market. High research and development activities and high emphasis on rare neurology conditions are making Europe a major contributor to the cluster headache market.

Germany Cluster Headache Market Insights:

Germany is a major contributor to the Europe cluster headache market and is influenced by factors including high healthcare infrastructure and high awareness levels. High access to neurology specialists is also responsible for the growth of this market. High adoption rates of CGRP-based treatments and oxygen therapy for acute attacks are making this a major contributor to the growth of this market. High emphasis is being placed on early diagnosis and personalized treatment approaches, and this is making this a high growth market.

Latin America Cluster Headache Market Insights:

The Latin America Cluster Headache Market is growing due to the development in healthcare infrastructure, increasing awareness of neurological conditions, and gradual development in diagnosis and treatment access. Countries such as Brazil, Mexico, and Argentina are experiencing growth in the adoption of pharmacological treatment and oxygen therapy in the management of cluster headache conditions. The growth in the Cluster Headache Market in the region is due to the development in healthcare infrastructure, increasing awareness of neurological conditions, and gradual development in diagnosis and treatment access.

Middle East & Africa Cluster Headache Market Insights:

The Middle East & Africa Cluster Headache Market is growing due to the development in healthcare infrastructure, increasing awareness of neurological conditions, and gradual development in diagnosis and treatment access. Increasing adoption of pharmacological treatment and oxygen therapy, along with limited adoption of neuromodulation devices, is supporting the growth in the Cluster Headache Market in the region.

Cluster Headache Market Competitive Landscape:

One of the most well-known pharmaceutical companies is Novartis AG, which has a strong footprint in cluster headache treatments, especially through its CGRP pathway-targeting products such as galcanezumab (Emgality), which is a commonly used medication for preventing episodic and chronic cluster headaches. The company’s leadership is also supported by its strong neurology portfolio, research and clinical capabilities, and commitment to investing in treatments for migraine and headache disorders. It has a strong network and a strong footprint in innovative biologics that help it compete favorably in the neurology therapeutic arena.

-

In March 2025, Novartis expanded the clinical and commercial adoption of its CGRP therapies across multiple regions, supporting increased utilization in preventive cluster headache management and reinforcing its leadership in headache-related indications.

Eli Lilly and Company is another notable company in the cluster headache market, which is mainly attributed to its CGRP monoclonal antibodies, such as galcanezumab, which has shown impressive results in controlling cluster headache attacks. The company is also benefiting from its strong research and development pipeline for neurological disorders. In addition, it has a strong presence in both acute and preventive cluster headache treatment. The company is also focusing on biologics, trials, and collaborations to meet unmet needs in cluster headache therapy.

-

In June 2025, Eli Lilly expanded the real-world adoption and clinical usage of its CGRP therapies across neurology centers and specialty clinics, strengthening its position in preventive treatment of cluster headaches and supporting broader guideline-based usage.

Teva Pharmaceutical Industries Ltd. is a prominent player in the cluster headache market due to its legacy, specialty, and sumatriptan-based treatments, and other migraine and headache medicines used to treat acute cluster headache. The company's experience in generics, specialty medicines, and neurology-focused treatments helps it stay competitive in the market, especially in the context of acute cluster headache. The company's manufacturing and distribution capabilities make it easier for patients in developed and emerging markets to access their medicines

-

In April 2025, Teva continued strengthening its neurology portfolio by optimizing its triptan-based therapies and expanding access to acute treatment options for migraine and cluster headache management, maintaining its relevance in immediate symptom relief across healthcare systems.

Cluster Headache Market Key Players:

Some of the Cluster Headache Market Companies are:

-

Novartis AG

-

Eli Lilly and Company

-

AstraZeneca Plc.

-

GlaxoSmithKline plc

-

Sun Pharmaceutical Industries Ltd.

-

Teva Pharmaceutical Industries Ltd.

-

Takeda Pharmaceutical Company Limited

-

Sanofi S.A.

-

AbbVie Inc.

-

Merck & Co., Inc.

-

Allergan plc

-

Bayer AG

-

Lundbeck Seattle BioPharmaceutical

-

Winston Laboratories

-

Zosano Pharma

-

ElectroCore Medical LLC

-

Autonomic Technologies, Inc.

-

Dr. Reddy’s Laboratories Ltd.

-

Grünenthal GmbH

-

F. Hoffmann-La Roche Ltd

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 556.03 Million |

| Market Size by 2035 | USD 886.30 billion |

| CAGR | CAGR of 4.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Episodic Cluster Headache (ECH), Chronic Cluster Headache (CCH), Others) • By Component (Pharmacological Treatments, Devices & Therapeutic Equipment, Accessories & Consumables, Supporting Services, Others) • By Technology (CGRP-targeted Therapies, Neuromodulation Technologies, Oxygen Therapy Systems, Conventional Drug Therapies, Others) • By Application (Acute Attack Management, Preventive Treatment, Transitional Therapy, Diagnosis & Monitoring, Others) • By End-User (Hospitals, Specialty Clinics (Neurology / Pain Clinics), Homecare Settings, Ambulatory Care Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novartis AG, Eli Lilly and Company, Teva Pharmaceutical Industries Ltd., Pfizer Inc., Merck & Co., Inc., Sanofi S.A., AbbVie Inc., GlaxoSmithKline plc, AstraZeneca plc, Bayer AG, Johnson & Johnson, Takeda Pharmaceutical Company Limited, Lundbeck Seattle BioPharmaceutical, Grünenthal GmbH, Dr. Reddy’s Laboratories Ltd., Sun Pharmaceutical Industries Ltd., Cipla Ltd., Lupin Limited, ElectroCore Medical LLC, Autonomic Technologies, Inc. |

Frequently Asked Questions

North America dominated with the largest market share with 41.25% in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at the highest CAGR of 6.36% during 2026–2035.

Pharmacological Treatments dominated with a 65.21% market share in 2025, while it is also projected to grow at the fastest rate of 10.54% during 2026–2035.

Growth is driven by rising prevalence of neurological disorders, increasing awareness and diagnosis rates, expanding use of CGRP-targeted therapies, and advancements in preventive and acute treatment options.

The market is valued at USD 556.03 Million in 2025 and is projected to reach USD 883.30 Million by 2035.

The Cluster Headache Market is projected to grow at a CAGR of 4.89% during 2026–2035.

Get in Touch