Hyperpigmentation Treatment Market Report Scope & Overview:

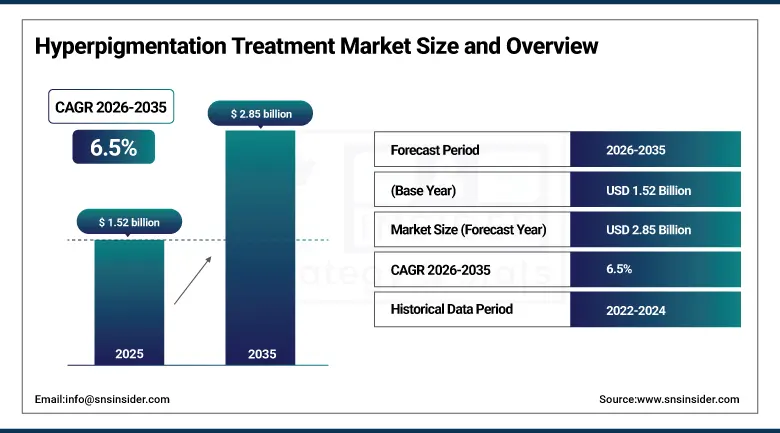

The Hyperpigmentation Treatment Market was valued at USD 1.52 billion in 2025 and is expected to reach USD 2.85 billion by 2035, growing at a CAGR of 6.5% from 2026-2035.

The Hyperpigmentation Treatment Market is witnessing steady growth owing to increasing awareness among consumers about skin aesthetics along with an increased demand for sophisticated dermatological treatments. The increase in incidence of melasma, acne scars, sunspots, and age-related hyperpigmentations is further driving the adoption of hyperpigmentation treatments worldwide. An increase in the number of medical aesthetic centers, advances in technology for laser and energy-based treatments, and increased usage of cosmeceuticals are driving the growth of the hyperpigmentation treatment market.

Hyperpigmentation Treatment Market Size and Forecast

-

Market Size in 2025: USD 1.52 Billion

-

Market Size by 2035: USD 2.85 Billion

-

CAGR: 6.5% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Hyperpigmentation Treatment Market - Request Free Sample Report

Hyperpigmentation Treatment Market Trends

-

Rising prevalence of skin disorders and increasing aesthetic consciousness are driving the hyperpigmentation treatment market.

-

Growing adoption of dermatological procedures and over-the-counter skincare products is boosting market growth.

-

Expansion of dermatology clinics, medspas, and cosmetic treatment centers is fueling service demand.

-

Increasing focus on skin tone correction, anti-aging solutions, and sun damage repair is shaping adoption trends.

-

Advancements in laser therapies, chemical peels, topical formulations, and combination treatments are improving efficacy and safety.

-

Rising influence of social media, beauty awareness, and dermatology consultations is supporting market expansion.

-

Collaborations between pharmaceutical companies, skincare brands, and dermatology professionals are accelerating innovation and global adoption.

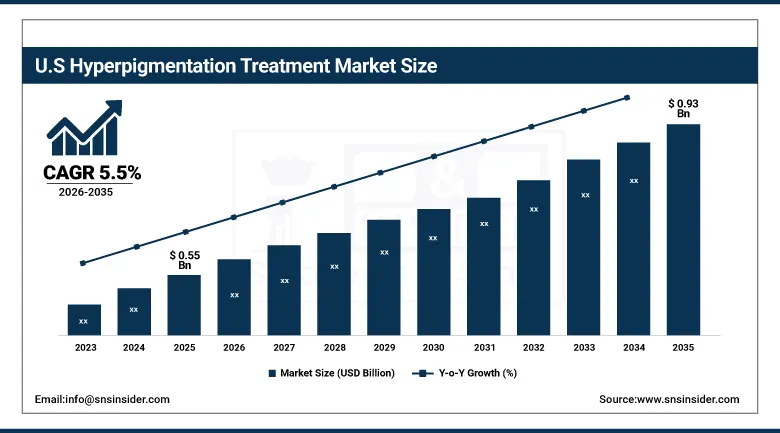

U.S. Hyperpigmentation Treatment Market was valued at USD 0.55 billion in 2025 and is expected to reach USD 0.93 billion by 2035, growing at a CAGR of 5.5% from 2026-2035.

U.S. Hyperpigmentation Treatment Market to Witness Growth Due to High Consumer Expenditure on Aesthetic Skincare Products and Growing Demand for Advanced Dermatological Treatments. Increasing incidence rates of melasma, age spots, and acne-induced pigmentation disorders, coupled with high usage of lasers, high-end skincare products, and dermatological recommendations, will fuel growth in the market.

Hyperpigmentation Treatment Market Segment Highlights

-

By Indication, Melasma segment dominated the Hyperpigmentation Treatment Market in 2025 with 38% share; Post-Inflammatory Hyperpigmentation (PIH) segment fastest growing (CAGR).

-

By Treatment, Energy-based Therapy segment dominated the Hyperpigmentation Treatment Market in 2025 with 42% share; Microneedling segment fastest growing (CAGR).

-

By Skin Tone, Fitzpatrick skin type III & IV segment dominated the Hyperpigmentation Treatment Market in 2025 with 41% share; Fitzpatrick skin type V & VI segment fastest growing (CAGR).

-

By End Use, Dermatology Clinics segment dominated the Hyperpigmentation Treatment Market in 2025 with 46% share; Aesthetic Centers segment fastest growing (CAGR).

Hyperpigmentation Treatment Market Segment Analysis

By Indication, Melasma segment dominates the Hyperpigmentation Treatment Market, Post-Inflammatory Hyperpigmentation segment expected to grow fastest

Melasma holds the largest share within the market of hyperpigmentation treatment owing to the high occurrence rate amongst adults, especially among females, and its recurring nature that necessitates continuous treatment by dermatologists. The disease is caused by hormonal changes, exposure to the sun, and genetics; hence, the treatment of the ailment continues steadily. Furthermore, the cosmetic concern regarding the face appearance brought about by the disease motivates patients to explore treatments that include lasers, peeling, and topical drugs.

Post-inflammatory hyperpigmentation is experiencing fast growth due to an increase in the prevalence of acne, eczema, and skin damage. There is also an increase in consumer awareness about skincare products and treatments, which is promoting the use of PIH treatments. An increase in pollution exposure and skin problems caused by the lifestyle are contributing to a wider range of patients requiring these treatment solutions.

By Treatment, Energy-based Therapy segment dominates the Hyperpigmentation Treatment Market, Microneedling segment expected to grow fastest

Energy-based therapy dominates the market because of its clinically validated efficacy in treating deep pigmentation with pinpoint accuracy and rapid results. Lasers and intense pulsed light devices have become popular in dermatological clinics owing to their capability to treat difficult cases of pigmentation without any downtime. The high degree of patient satisfaction, need for repeat treatments, and innovations in terms of product safety and efficacy further solidify its dominance in the market.

Microneedling is a rapidly growing technology owing to its low invasiveness, cost-effectiveness, and applicability on different types of skin. This treatment facilitates skin regeneration and improves the penetration of topical agents, thus proving effective in addressing a range of issues related to pigmentation. The growing inclination towards combination therapy and minimally invasive cosmetic procedures is driving its popularity.

By Skin Tone, Fitzpatrick Skin Type III & IV segment dominates the Hyperpigmentation Treatment Market, Fitzpatrick Skin Type V & VI segment expected to grow fastest

Fitzpatrick skin types III and IV are dominant owing to their high population prevalence across the globe as well as the higher susceptibility to develop moderate hyperpigmentation upon exposure to sunlight or inflammatory response. People with these Fitzpatrick skin types are more susceptible to pigmentation disorders. Hence, such patients use many dermatological procedures on a regular basis to improve skin appearance. Moreover, high aesthetic consciousness along with easy access to dermatology services increases the demand for treatment among the populations under discussion.

Fitzpatrick skin types V & VI are growing rapidly in treatment demand because of greater understanding regarding safe pigment treatments. These types have been historically ignored, but now they are taking advantage of the latest technology that ensures minimal chances of risks such as those associated with post-treatment problems. Increasing aesthetic awareness coupled with access to dermatologists and safer treatment approaches is making it more common.

By End Use, Dermatology Clinics segment dominates the Hyperpigmentation Treatment Market, Aesthetic Centers segment expected to grow fastest

The dermatology clinic segment is dominating owing to the presence of skilled professionals, advanced diagnostic technology, and availability of multiple prescription drugs and procedures. Patients are increasingly favoring clinics for precise diagnosis and customized treatment options for complex pigmentation disorders. Furthermore, clinics provide combination therapy along with follow-up services, which ensures better results. The high level of trust in licensed dermatologists and standard treatment protocols strengthens their leadership in the market.

Aesthetic centers is expanding at a rapid pace because of the increasing popularity of cosmetic-based, minimally-invasive skin care procedures. Aesthetic centers deliver quick, personalized, and convenient treatment procedures that require lesser waiting time than conventional clinics. Increasing awareness about beauty, social media, and non-medical cosmetic environment preferences are fueling patient visits. Moreover, advancements in aesthetic technology and cost-effective treatment plans are accelerating their market growth.

Hyperpigmentation Treatment Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90.7% |

|

Europe |

United Kingdom |

22.4% |

|

Asia Pacific |

Australia |

11.8% |

|

Middle East & Africa |

UAE |

14.6% |

|

Latin America |

Brazil |

48.3% |

North America Hyperpigmentation Treatment Market Insights

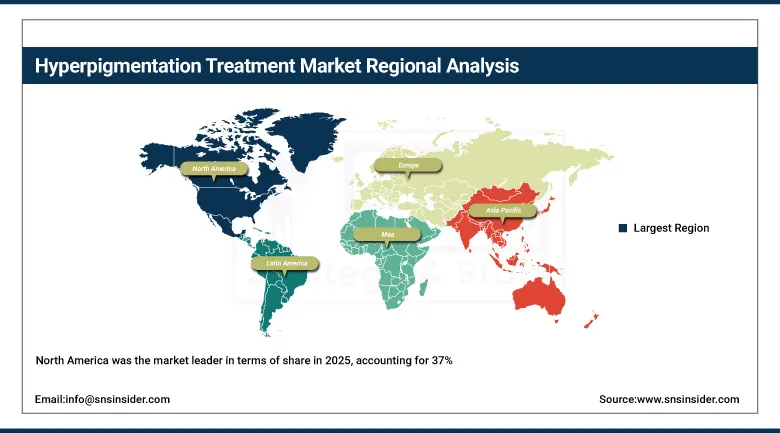

North America was the market leader in terms of share in 2025, accounting for 37%. Factors such as greater consumer awareness, advanced dermatological setups, and adoption of aesthetic techniques have favored North America. North America has a large number of qualified dermatologists, FDA-approved medications, and increasing popularity of skin enhancement techniques. Growing geriatric population and increasing incidence of pigmentation problems like melasma and age spots in women fuel market demand. Presence of major cosmetic and pharmaceutical firms in addition to growing influence of social media stars is driving market demand in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Hyperpigmentation Treatment Market Insights

Asia Pacific will become the fastest-growing region due to higher disposable incomes, a beauty-conscious urban population, and increased awareness about dermatological treatments. Melasma and PIH cases have become increasingly common in India, China, South Korea, and Japan because society is obsessed with having an attractive appearance. In addition, the occurrence of melasma and PIH is very common in the Asia Pacific region because of various environmental and genetic reasons. Therefore, the demand for these therapies has been increasing in recent years. An increasing number of aesthetic clinics, availability of low-cost solutions, and rising trend of K-beauty have helped drive market growth in the region since 2025.

Europe Hyperpigmentation Treatment Market Insights

The Europe Hyperpigmentation Treatment Market is showing stable growth owing to an increase in awareness about the latest treatments and technologies in skin care and a rise in demand for non-surgical cosmetic treatments. The high incidence rate of conditions like melasma, age spots, and post-inflammatory hyperpigmentation in elderly patients is expected to fuel market growth. The availability of specialized dermatology clinics, cosmetic centers, and high-end skin care brands in countries like Germany, France, Italy, and the United Kingdom is aiding market growth.

Middle East & Africa and Latin America Hyperpigmentation Treatment Market Insights

The Middle East & Africa and Latin America Hyperpigmentation Treatment Market is growing steadily owing to high awareness about cosmetic treatments of the skin as well as growing popularity for dermatological services. High urbanization, increased disposable income, and increased preference for skin brightening treatments are some key factors driving the market's growth in both geographies. Geographies including the UAE, Saudi Arabia, Brazil, and Mexico are witnessing an increase in the use of laser treatments and other minimally invasive cosmetic procedures.

Hyperpigmentation Treatment Market Growth Drivers:

-

Rising demand for dermatology-driven cosmetic procedures and advanced skin brightening solutions worldwide

Awareness regarding skin condition and aesthetic well-being is driving high demand for treatment options for hyperpigmentation among both medical as well as consumer skincare products. Increasing inclination toward even skin tones, anti-aging products, and acne scars correction is fostering the use of topical creams, chemical peelings, lasers, and hybrid treatments. The impact of social media and beauty standards is also driving people to seek medical assistance for dermatological procedures. Urbanization and increasing disposable income levels are also adding strength to expenditure on luxurious skincare products. An influx of customers into dermatological clinics and medspa clinics is bolstering the market dynamics for both prescription and OTC-based pigmentation correction solutions worldwide.

Hyperpigmentation Treatment Market Restraints:

-

High treatment costs and limited affordability of advanced dermatological procedures restricting widespread adoption

High-priced treatments used to treat hyperpigmentation conditions such as laser treatment, chemical peelings, and dermatological prescription treatment are usually expensive, making them inaccessible to cost-conscious consumers. The need for more than one session to see results adds up to even more expense. Many insurance companies do not cover costs related to cosmetic treatments. Expensive skincare and dermatologist appointments may also contribute to the high costs involved. This makes adoption extremely difficult in developing countries and by middle-class people despite increased awareness of and demand for hyperpigmentation correction treatments in the global skincare market.

Hyperpigmentation Treatment Market Opportunities:

-

Growing demand for personalized dermatology and AI-driven skin analysis creating new treatment innovation pathways

The growing adoption of AI and digital dermatology products is presenting new possibilities in developing customized hyperpigmentation treatment plans. The use of AI for skin assessment makes it easier to determine the nature, degree, and even the depth of pigmentation to enable customized treatment plans. Dermatology products and telemedicine technologies will be used extensively to provide consultations and even treatments regardless of geography. In addition, custom skincare regimens that incorporate genetics and lifestyle considerations are becoming increasingly common. Precision dermatology brings numerous benefits, thus motivating companies to invest in innovative dermatological diagnostics and skincare products.

Recent Developments:

-

2023: AbbVie (Allergan Aesthetics) launched the SkinMedica Even & Correct Collection in January 2023 to target hyperpigmentation and uneven skin tone. The collection included Advanced Brightening Treatment, Dark Spot Cream, and Brightening Pads for professional-grade skincare solutions.

-

2024: L’Oréal Groupe introduced Melasyl, a breakthrough molecule designed to treat localized pigmentation issues including age spots and post-acne marks. The ingredient debuted in La Roche-Posay Mela B3 products after 18 years of research.

-

2025: Galderma S.A. strengthened its dermatology and pigmentation-treatment portfolio in 2025 through strong skincare growth and expanded dermatological innovation activities. The company reported continued momentum in dermatological skincare and aesthetic dermatology categories globally.

-

2026: Galderma S.A. announced that L’Oréal Groupe increased its equity investment in the company to strengthen collaboration in dermatology and skincare innovation, including pigmentation-related treatments and advanced dermatological research initiatives.

Key Players

Some of the Hyperpigmentation Treatment Market Companies

-

L’Oréal Groupe

-

Galderma S.A.

-

Beiersdorf AG

-

Johnson & Johnson

-

Procter & Gamble

-

Unilever

-

Shiseido Company Limited

-

AbbVie (Allergan Aesthetics)

-

Bayer AG

-

Obagi Medical Products

-

SkinCeuticals

-

La Roche-Posay (L’Oréal division)

-

Pierre Fabre Dermo-Cosmetique

-

Candela Medical

-

Lumenis

-

Vivier Pharma

-

Paula’s Choice

-

ISDIN

-

Bausch Health

-

Allergan Aesthetics

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.52 Billion |

| Market Size by 2035 | USD 2.85 Billion |

| CAGR | CAGR of 6.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Indication [Age spots, Melasma, Post-inflammatory hyperpigmentation (PIH), Others] • By Treatment [Energy-based Therapy, Chemical Peels, Microdermabrasion, Microneedling] • By Skin Tone [Fitzpatrick skin type I & II, Fitzpatrick skin type III & IV, Fitzpatrick skin type V & VI] • By End Use [Dermatology Clinics, Aesthetic Centers, Hospitals & Specialty Clinics] |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | L’Oréal Groupe, Galderma S.A., Beiersdorf AG, Johnson & Johnson, Procter & Gamble, Unilever, Shiseido Company Limited, AbbVie (Allergan Aesthetics), Bayer AG, Obagi Medical Products, SkinCeuticals, La Roche-Posay, Pierre Fabre Dermo-Cosmetique, Candela Medical, Lumenis, Vivier Pharma, Paula’s Choice, ISDIN, Bausch Health, Allergan Aesthetics |

Frequently Asked Questions

North America dominated the Hyperpigmentation Treatment Market in 2025.

The Melasma segment dominated the Hyperpigmentation Treatment Market in 2025.

Rising demand for dermatology-driven cosmetic procedures and advanced skin brightening solutions worldwide.

The Hyperpigmentation Treatment Market was valued at USD 1.52 billion in 2025.

The Hyperpigmentation Treatment Market is expected to grow at a CAGR of 6.5% from 2026 to 2035.

Get in Touch