Integrated Passive Devices Market Report Scope & Overview:

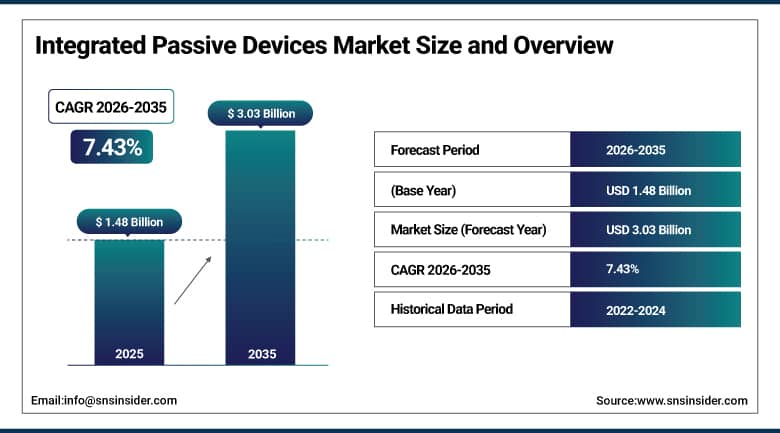

The Integrated Passive Devices Market size was USD 1.48 Billion in 2025 and is expected to reach USD 3.03 Billion by 2035, growing at a CAGR of 7.43% from 2026–2035.

The miniaturization of electronic devices in consumer electronics, automotive, telecommunications, and healthcare industries is driving the growth of the integrated passive devices market. The increasing use of 5G technology has raised the demand for RF modules that have a smaller form factor and higher performance, thus resulting in the integration of IPDs. The developments in semiconductor fabrication process, such as AI-based automation and improved fabrications processes, are making the IPDs efficient and reducing manufacturing costs. As more and more electronics become energy-conscious, there is an increasing need for IPDs in circuit design due to their low power and high performance. The trend towards electric and autonomous cars in the automotive industry is also increasing the demand for IPDs.

Market Size and Forecast:

-

Market Size in 2026E: USD 1.59 Billion

-

Market Size by 2035: USD 3.03 Billion

-

CAGR: 7.43% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

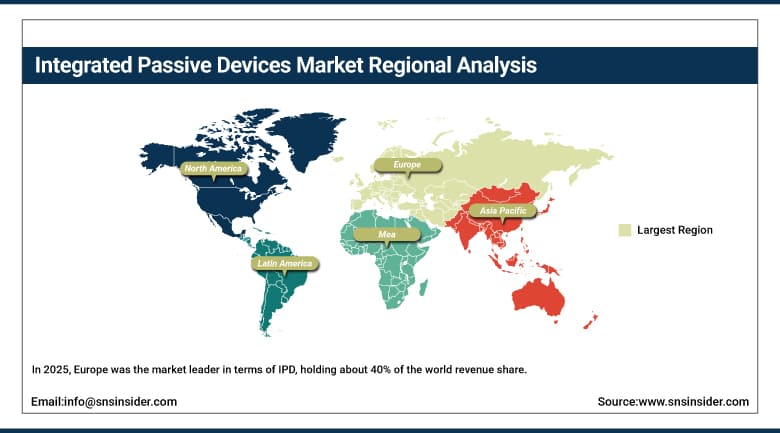

Largest Region: Europe

To Get More Information On Integrated Passive Devices Market - Request Free Sample Report

Integrated Passive Devices Market Trends:

-

5G rollout keeps driving demand for high-frequency, miniaturized RF IPD modules for base stations and mobile devices.

-

EV adoption is accelerating IPD integration in power management, ADAS, and battery management systems.

-

Wearable and implantable medical device growth is expanding healthcare applications for miniaturized IPD components.

-

Advanced packaging techniques including wafer-level packaging and flip-chip bonding are improving IPD performance.

-

AI-assisted IPD design automation is reducing development cycles and improving component integration density.

-

Growing IoT device proliferation is expanding demand for compact, low-power EMI protection IPDs.

-

Growing IoT device proliferation is expanding demand for compact, low-power EMI protection IPDs.

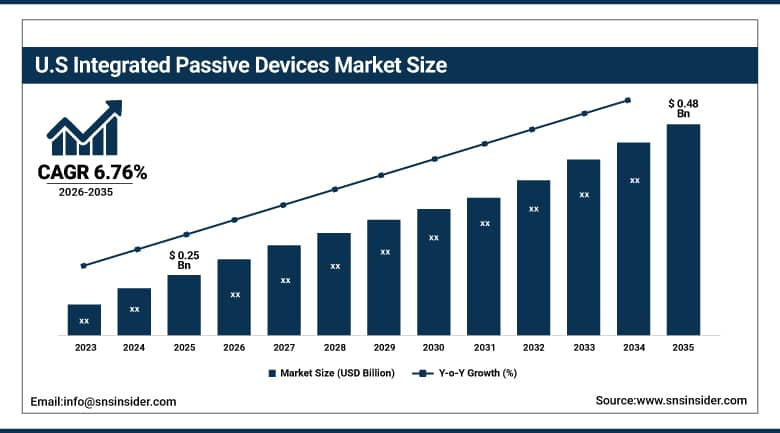

U.S. Integrated Passive Devices Market Outlook:

The U.S. Integrated Passive Devices Market was valued at approximately USD 0.25 Billion in 2025. It is expected to reach approximately USD 0.48 Billion by 2035, growing at a CAGR of approximately 6.76%.

The shift to electric and self-driving vehicles in the automotive sector has created a surge in demand for IPDs for ADAS and power management applications. In the healthcare industry, there is growth in terms of wearable and implantable devices for the patients, which has led to increased usage of IPDs. Improvements in semiconductor technology, along with AI-based design automation, have enhanced the performance of IPDs while reducing their costs. American firms such as Broadcom, Texas Instruments, Qorvo, and ON Semiconductor remain committed to investing in IPD platforms for 5G and automotive sectors.

In August 2024, Broadcom advanced its optical connectivity for GPUs by integrating co-packaged optics (CPO) into AI accelerators, achieving 1.6 TB/sec bandwidth. The company showcased its latest optical engine at Hot Chips, demonstrating error-free data transfer with a test chip.

Integrated Passive Devices Market Segment Analysis:

-

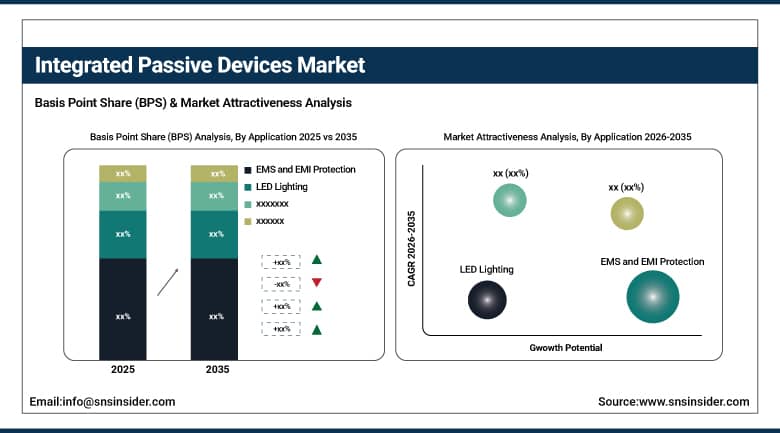

By Application, the EMS and EMI Protection segment dominated the integrated passive devices market with approximately 40% share in 2025. The LED Lighting segment is expected to register the fastest CAGR through the forecast period.

-

By End Use, the Automotive segment dominated the integrated passive devices market with approximately 45% share in 2025. The Consumer Electronics segment is expected to register the fastest CAGR through the forecast period.

By Application, EMS and EMI Protection dominates, LED Lighting grows fastest

The EMS & EMI Protection category held around 40% share of revenue in integrated passive devices market in 2025. This is because of rising demand for electromagnetic shielding in consumer electronics, automotive, and telecommunication industries. With the increase in miniaturization and efficiency of devices, there will be chances of more interference of electromagnetic and this calls for the requirement of IPDs. With the growth of 5G network and rising use of electric vehicles, the need for EMI protection will increase rapidly. Other industries like aerospace, healthcare also require shielding from EMI to avoid any disturbances in their processes. Radio Frequency Protection and Digital Mixed Signal applications also make up a large portion of demand.

The LED Lighting segment is the fastest-growing application in integrated passive devices market between 2026 and 2035. Growing trend toward energy-efficient and sustainable lighting systems is the key factor behind the rise in demand.

By End Use, automotive dominates, consumer electronics grows fastest

The automotive sector was the leading end-user segment for the integrated passive devices market, accounting for around 45% share in 2025. The extensive use of ADAS technology, infotainment system, and electrical system has led to its dominance. As the demand for EV and hybrid cars rises, there is a need for smaller, energy-efficient, and high-performance electronic components. IPD is becoming very significant in enhancing signal integrity, reducing EMI and maximizing power efficiency in automotive applications. Further, the European legislation on safety and energy efficiency is boosting the use of IPD among automotive makers.

The consumer electronics segment is projected to be the fastest-growing end-use sector during 2026 to 2035. Rising demand for smartphones, wearable devices, tablets, and smart home appliances is contributing to the growth of this sector. IPD plays an important role in managing power consumption, noise, and signal integrity in sophisticated electronic systems due to miniaturization and functional improvement by the manufacturers. The shift towards 5G mobile communication and the advent of AI and IoT applications are driving the development of high-frequency and low-power IPD components.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

Europe Integrated Passive Devices Market Insights

In 2025, Europe was the market leader in terms of IPD, holding about 40% of the world revenue share. This dominance can be attributed to the thriving semiconductor industry, increasing demands for automotive electronics, and growth of 5G connectivity. In addition, European countries such as Germany, France, and the UK are among the leading manufacturers in automotive sector due to their efforts towards electric vehicles and ADAS technologies. The strict regulation of energy efficiency in the region has played an essential role in IPD adoption in consumer electronics and telecom industries.

Germany held a share of about 24.6% in Europe's revenues. Investments in automotive and industrial manufacturing continue to drive demand for IPD in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Integrated Passive Devices Market Insights

North America is an important integrated passive devices market, owing to the presence of strong semiconductor research and development as well as increasing investments made into 5G networks. IPD vendors in the region include Broadcom, Texas Instruments, Qorvo, and ON Semiconductor, among others, while increased demand for electronics in the automobiles of electric vehicle manufacturers in the region supports the strong position of this market.

The United States generates about 82.5% of North American revenue. Wearable healthcare devices and defense electronics also add important demand for IPDs, apart from consumer electronics and vehicles.

Asia Pacific Integrated Passive Devices Market Insights

Asia Pacific emerges to be the fastest-growing region in the integrated passive devices market during the forecast period due to industrialization and increased production of consumer electronics and increased usage of 5G and IoT technologies. China, Japan, South Korea, and Taiwan are among the leading regions where there is an emergence of semiconductor manufacturing, thus the need for highly efficient miniature devices. The government investment in smart manufacturing and domestic semiconductors increases the adoption rate.

China constitutes approximately 40.6% of Asia Pacific revenue. The government funding in manufacturing and increasing consumer electronics market in the country continue to boost the adoption rate. With the continued increase in semiconductor manufacturing capability in the region, the trend will continue to grow.

MEA & Latin America Integrated Passive Devices Market Insights

UAE has top revenue in MEA at about 22.8%. Increased electronics manufacturing investments and growing 5G infrastructure both fuel regional IPD demand. Saudi Arabia is also increasing its capacity to manufacture technology products.

Brazil has top revenue in Latin America at around 43.8%. Consumer electronics and automotive manufacturing expansion are both responsible for the region’s demand. Mexico and Argentina also provide second-level demand due to expansion in electronics.

Market Dynamics:

Growth Drivers: Rising demand for energy efficiency and miniaturization across 5G, EV, and IoT

The rising trend towards energy efficiency in devices such as smart devices, automotive electronics, and telecommunications is another major factor behind this phenomenon. In telecommunications, due to the expected increase in mobile traffic by three times until 2030, telecommunication operators will need to enhance the energy efficiency and performance of their networks. For instance, passive antennas for on-ground 5G networks showed 11% improvement in beam efficiency, 18% increase in downlink throughput, 21% uplink throughput improvement, and 7.5% improvement in energy efficiency. The growing application of AI electronics calls for low-power circuits and further enhances the trend of IPDs adoption.

With respect to automobiles, the shift towards EVs and self-driving cars leads to increased IPD adoption in ADAS and power management systems. Given the forecast that EV production will be more than 40 million cars per year globally until 2030, it is safe to say that the need for IPDs is to be expanded. Rising number of IoT devices contributes to the increase in the addressable market for low-power EMI protection IPDs.

Restraints: Limited standardization hampering compatibility and slowing adoption

The lack of uniformity in design specifications is a major hindrance in the market potential of IPDs owing to compatibility problems. Every industry sector like consumer electronics, automotive and telecommunication industry has different size, performance and material specifications that make it hard to set any standard designs. The rapid advancement in semiconductor technology makes it necessary for companies to regularly update design specifications.

Moreover, the process of testing and certification adds to the difficulty in getting regulatory approval which causes delay in commercializing the products. It is quite hard for companies to incorporate the IPD into the electronic system due to different industry specific protocols. Small companies find it hard to bear the burden of customization costs in the absence of standardization.

Opportunities: EV and ADAS integration creating major new IPD demand

There are huge demands in the market for IPDs due to the fast electrification of the auto sector. IPDs help to optimize energy consumption and avoid the problem of electromagnetic interference. The improvement in performance for radar and lidar technologies in ADAS and sensors can be attributed to the use of IPDs. IPDs are a preferred choice for electronics used in automobiles because of their durability and reliability.

As the number of electric vehicle sales increases and ADAS becomes more commonplace, there will be a significant increase in the demand for IPDs. Smart homes, wearables and Industrial IoT are other markets where we see parallel growth of demand. First-movers who come up with an optimal IPD platform for the new generation of EV will have a definite competitive advantage.

Recent Developments:

-

2024: Broadcom integrated co-packaged optics (CPO) into GPUs in August 2024, achieving 1.6 TB/sec bandwidth to enhance AI accelerator performance while reducing power consumption.

-

2024: Johanson Technology unveiled its 0898CP14C0035001T 900MHz Mini-Coupler in July 2024, designed for ISM, IoT, cellular, and LoRa applications in a compact EIA 0603 design.

-

2024: Murata Manufacturing announced new IPD solutions for 5G and Wi-Fi 7 applications, combining EMI filters and RF components in an ultra-compact package to support next-generation wireless devices.

Integrated Passive Devices Market Key Players are:

These vendors span global semiconductor leaders, RF component specialists, and passive component manufacturers serving automotive, telecom, and consumer electronics markets.

-

Broadcom

-

CTS Corporation

-

Global Communication Semiconductors, LLC.

-

Infineon Technologies AG

-

Johanson Technology, Inc.

-

MACOM

-

Murata Manufacturing Co., Ltd.

-

NXP Semiconductors

-

ON Semiconductor

-

Qorvo, Inc.

-

STMicroelectronics

-

Texas Instruments Incorporated

-

Skyworks Solutions, Inc.

-

pSemi Corporation

-

Kyocera Corporation

-

TDK Corporation

-

Vishay Intertechnology, Inc.

-

Alps Alpine Co., Ltd.

-

X-Fab Silicon Foundries SE

-

TE Connectivity Ltd.

Integrated Passive Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.48 Billion |

| Market Size by 2035 | USD 3.03 Billion |

| CAGR | CAGR of 7.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (EMS and EMI Protection, Radio Frequency Protection, LED Lighting, Digital and Mixed Signal) • By End Use (Automotive, Consumer Electronics, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Broadcom, CTS Corporation, Global Communication Semiconductors, LLC., Infineon Technologies AG, Johanson Technology, Inc., MACOM, Murata Manufacturing Co., Ltd., NXP Semiconductors, ON Semiconductor, Qorvo, Inc., STMicroelectronics, Texas Instruments Incorporated, Skyworks Solutions, Inc., pSemi Corporation, Kyocera Corporation, TDK Corporation, Vishay Intertechnology, Inc., Alps Alpine Co., Ltd., X-Fab Silicon Foundries SE, and TE Connectivity Ltd. |

Frequently Asked Questions

The Integrated Passive Devices Market is expected to grow at a CAGR of 7.43% from 2026 to 2035.

The Integrated Passive Devices Market was valued at USD 1.48 Billion in 2025, with Europe accounting for the largest regional share at approximately 40%.

Rising demand for energy-efficient miniaturized components across 5G, EV, and IoT applications is the primary growth factor.

The EMS and EMI Protection segment dominated with approximately 40% share in 2025. The LED Lighting segment is expected to grow fastest.

Europe dominated the Integrated Passive Devices Market with approximately 40% revenue share in 2025, driven by strong automotive innovation and stringent energy efficiency regulations. Asia Pacific is the fastest-growing region.

Get in Touch