Irritable Bowel Syndrome Treatment Market Report Scope & Overview:

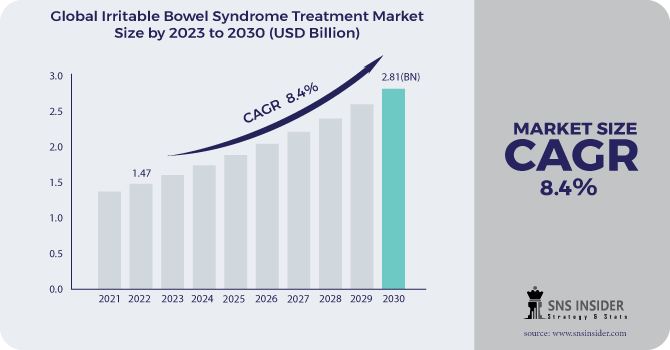

The Irritable Bowel Syndrome Treatment Market Size was valued at USD 3.05 Billion in 2023 and is expected to reach USD 6.46 Billion by 2032 and grow at a CAGR of 8.7% over the forecast period 2024-2032. This report puts emphasis on the rising incidence and prevalence of IBS, fueled by changing lifestyles, stress levels, and food habits, besides reviewing regional IBS drug prescription trends, including regional differences in treatment preferences and access. The report also reviews healthcare expenditure on the treatment of IBS in government, commercial, private, and out-of-pocket segments, delineating the economic burden of the disease. The report also examines developing therapeutic trends, including the growth in gut microbiome-targeted treatments and targeted therapeutics, as well as increasing impact of lifestyle and dietary trends on market demand, highlighting the move towards holistic and non-pharmacological management of IBS.

Get more information on Irritable Bowel Syndrome Treatment Market - Request Sample Report

Market Dynamics

Drivers

-

The IBS treatment market is driven by rising prevalence of irritable bowel syndrome (IBS) globally.

IBS treatment is driven by escalating prevalence of irritable bowel syndrome (IBS) worldwide, with research supporting that 10-15% of the worldwide population has IBS, while only 40% receive medical treatment. More awareness and rate of diagnosis increased the demand for specialized treatments such as Linzess (Linaclotide), Xifaxan (Rifaximin), and Viberzi (Eluxadoline). Furthermore, improvements in drug discovery, such as microbiome-specific therapies and gut-targeted neuromodulators, are increasing treatment effectiveness and patient outcomes. The transition towards personalized medicine and non-invasive diagnostics is also fueling market growth. Furthermore, growing incorporation of dietary and probiotic-based strategies, including the low FODMAP diet and therapy with gut microbiota, is complementing conventional pharmacological therapy. Pharmaceutical firms are aggressively investing in R&D, with Ironwood Pharmaceuticals, Takeda, and Ardelyx driving innovation. In addition, positive reimbursement policies in established markets have enhanced access to new therapies. Increasing demand for over-the-counter (OTC) medications and self-care products, especially in retail pharmacies, is also driving the market. The development of digital healthcare solutions and symptom monitoring using AI is another major driver, enhancing the management of diseases and patient compliance with treatment protocols.

Restraints

-

The high cost of advanced IBS medications and limited insurance coverage in certain regions.

Several new drugs, including Linzess and Viberzi, are costly, which impairs access, particularly in low- and middle-income nations. Moreover, side effects that arise from drugs used in the treatment of IBS, including diarrhea, bloating, and abdominal pain, result in patient nonadherence and drug discontinuation. Linzess (Linaclotide), for instance, can effectively manage IBS-C but tends to induce diarrhea, making patients reluctant to continue treatment. Another major challenge is the absence of a clear diagnostic test for IBS, with consequent underdiagnosis and misdiagnosis. IBS symptoms are confusingly similar to other gastrointestinal illnesses such as Inflammatory Bowel Disease (IBD) and Celiac Disease, making them difficult to accurately diagnose. Finally, social stigma associated with IBS discourages many patients from visiting doctors. Regulatory hurdles are also a hindrance, in that strict approval procedures for novel IBS therapies can slow the entry of drugs into the marketplace. For example, Synthetic Biologics' SYN-010, a treatment for IBS-C that is still in the investigative stage, has been delayed because of prolonged clinical trial phases. Lastly, the absence of curative drugs implies that existing drugs are only aimed at alleviating symptoms and not at treating the root cause, thus constraining long-term treatment efficacy.

Opportunities

-

The rising adoption of microbiome-based therapies and personalized medicine.

Growth in gut microbiota- targeted treatments, including probiotics, prebiotics, and fecal microbiota transplantation (FMT), provides viable alternatives to conventional drug treatments. Biologic and small-molecule drugs are growing investments for companies, with Ardelyx's Ibsrela (Tenapanor) emerging as a new treatment option for IBS-C. Digital health solutions also represent a huge opportunity, such as AI-based symptom tracking applications and telemedicine platforms, improving patient engagement and treatment compliance. Retail pharmacy development also holds promise, with more and more patients seeking OTC therapy, dietary supplements, and lifestyle-based treatments to control symptoms. Further, widening clinical research into the genetic and neurobiologic underpinnings of IBS may bring about paradigm-breaking therapies aimed at the gut-brain axis. Furthermore, government programs and investments in gastrointestinal research are fueling the creation of new therapies. Strategic acquisitions and collaborations among leading pharmaceutical firms, like Ironwood and AbbVie's collaboration for Linzess, further provide channels for innovation and market expansion.

Challenges

-

The IBS treatment market faces several challenges, primarily due to the complex nature of IBS diagnosis and treatment.

One of the biggest challenges is the high level of patient variability in response to current treatments, which complicates standardization of therapy. For instance, while Linzess (Linaclotide) is effective in some IBS-C patients, others have profound diarrhea and discomfort, causing them to discontinue. Another major challenge is the lengthy development period for new IBS medications since clinical trials demand large amounts of patient data and regulatory approvals, which slows market entry. For example, Synthetic Biologics' SYN-010 has encountered prolonged trial durations as a result of difficulties in demonstrating its effectiveness. Moreover, the psychological aspect of IBS, which is commonly associated with stress and anxiety, makes treatment challenging, necessitating a multidisciplinary strategy involving pharmacological and psychological interventions. Low awareness and misdiagnosis rates are still a significant issue, as a large number of IBS cases remain undiagnosed as a result of symptom overlap with other gastrointestinal diseases. In addition, herbal and alternative therapies like peppermint oil and curcumin supplements are becoming increasingly popular, competing with conventional pharmaceuticals. Finally, concerns over data privacy in digital health solutions for IBS management, including AI-based symptom tracking and telemedicine platforms, can hinder adoption through regulatory limitations and patient reluctance.

Segmentation Analysis

By Type

The IBS-D (Diarrhea-Predominant IBS) segment led the market in 2023 with the highest revenue share of 43.8%. The widespread prevalence of IBS-D, combined with the presence of targeted therapies like rifaximin (Xifaxan) and eluxadoline (Viberzi), has fueled its market leadership. Growing awareness, diagnosis rates, and strong physician preference for prescription drugs have fueled this dominance.

The IBS-C (Constipation-Predominant IBS) segment is expected to have the highest growth rate during the forecast period. The increasing uptake of Linzess (Linaclotide) and Amitiza (Lubiprostone), combined with rising patient awareness of available management options for IBS-C, is driving the growth of this segment. Further, the increase in patients visiting healthcare providers for chronic constipation symptoms has created a greater demand for prescription drugs.

By Drug Class

Linzess/Constella (Linaclotide) was the market leader in IBS treatment in 2023, with the highest revenue share of 32.3%. Its leadership is supported by its excellent efficacy in IBS-C treatment, extensive physician preference, and supportive reimbursement policies in major markets such as the U.S. and Europe. Its established status as a first-line treatment for IBS-C further reinforced its leadership in the market.

Viberzi (Eluxadoline) is expected to have the fastest growth in the coming years. Its rising usage for the treatment of IBS-D, driven by its two-mechanism approach acting on opioid receptors in the intestine, has boosted demand. The rising demand for targeted therapies compared to conventional anti-diarrheal drugs is also likely to propel its market growth.

By Distribution Channel

Hospital pharmacies dominated the IBS treatment market in 2023, accounting for the largest revenue share of 45.2%. Hospital sales were higher due to growing hospital visits for IBS conditions, a preference for specialist prescriptions, and the instantaneous availability of recommended medications for chronic IBS cases.

Retail pharmacies should see the strongest growth among treatment of IBS. Increased patient demand for over-the-counter (OTC) products and simplicity of accessing prescription drugs have grown sales via the retail route. The move toward direct purchases by consumers and wider pharmacist consulting services is driving segment growth even more.

Regional Analysis

North America led the IBS treatment market in 2023, with 34.2% revenue share owing to the widespread prevalence of IBS, robust healthcare infrastructure, and growing awareness regarding available treatments. The presence of major pharmaceutical firms, high prescription drug use such as Linzess and Xifaxan, and supportive reimbursement policies have also driven the market. The U.S. is at the forefront of the region with the highest diagnosis rates and growing demand for new therapies.

Europe has a strong market share, fueled by growing IBS incidence, growing healthcare spending, and government backing for IBS research. Germany, the UK, and France are among the countries that make a strong contribution to market growth because of improved access to sophisticated treatment methods. The use of microbiome-based treatments and dietary management strategies is also picking up in the region.

Asia-Pacific is predicted to observe the fastest growth, led by rising awareness, enhanced accessibility of healthcare, and investments in treatment of digestive health. China, Japan, and India are seeing heightened cases of IBS because of lifestyle changes, urbanization, and eating habits. Market growth is being driven by heightened availability of over-the-counter and prescription drugs as well as retail pharmacy network expansion.

Key Players and Their Products in the IBS Treatment Market

-

Ironwood Pharmaceuticals, Inc. – Linzess (Linaclotide)

-

Allergan – Viberzi (Eluxadoline), Linzess (Co-marketed with Ironwood)

-

Astellas Pharma, Inc.

-

Takeda Pharmaceutical Company Limited – Amitiza (Lubiprostone)

-

AstraZeneca

-

Sanofi S.A.

-

Sebela Pharmaceuticals Inc. – Motofen (Difenoxin/Atropine)

-

Bausch Health – Xifaxan (Rifaximin)

-

Synthetic Biologics, Inc. – SYN-010 (Investigational therapy for IBS-C)

-

Ardelyx – Ibsrela (Tenapanor)

Recent Developments

In Feb 2025, Michigan Medicine and Cleveland Clinic researchers developed a new IBS treatment approach using a personalized diet based on blood test panels to eliminate trigger foods. Conducted across eight research centers, the study aims to alleviate IBS symptoms and improve patient quality of life.

In Feb 2025, Sanofi and Teva Pharmaceuticals unveiled new detailed data from the RELIEVE UCCD Phase 2b study on duvakitug (TEV’574/SAR447189), demonstrating its efficacy in treating moderate-to-severe ulcerative colitis (UC) and Crohn’s disease (CD). The findings reinforce its potential as a novel therapy for inflammatory bowel disease (IBD).

In Dec 2024, Takeda Canada Inc. launched the MILESTONE Canada Advanced IBD Fellowship Initiative, aiming to standardize training, build professional networks, and implement Entrustable Professional Activities (EPAs) for advanced Inflammatory Bowel Disease (IBD) fellows in Canada. This initiative reflects Takeda’s commitment to advancing IBD education and specialized care.

| Report Attributes | Details |

| Market Size in 2023 | USD 3.05 billion |

| Market Size by 2032 | USD 6.46 billion |

| CAGR | CAGR of 8.7% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type [IBS-Cs, IBS-D] • By Drug Class [Xifaxan, Linzess/Constella, Viberzi, Amitiza, Others] • By Distribution Channel [Hospital Pharmacy, Retail Pharmacy, Others] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Ironwood Pharmaceuticals, Inc., Allergan, Astellas Pharma, Inc., Takeda Pharmaceutical Company Limited, AstraZeneca, Sanofi S.A., Sebela Pharmaceuticals Inc., Bausch Health, Synthetic Biologics, Inc., Ardelyx. |

Frequently Asked Questions

The IBS-D (Diarrhea-Predominant IBS) segment led the market in 2023 with the highest revenue share of 43.8%.

North America led the IBS treatment market in 2023, with 34.2% revenue share owing to the widespread prevalence of IBS, robust healthcare infrastructure, and growing awareness regarding available treatments.

Irritable Bowel Syndrome Treatment Market is divided into three segments and they are By Type, By Drug class, By distribution channel

Government regulations that are extremely strict, and Patients are dissatisfied with the IBS treatment they are receiving are the restraints of the Irritable Bowel Syndrome Treatment.

Irritable Bowel Syndrome Treatment market is expected to grow at a CAGR of 8.7% over the forecast period 2024-2032.

Get in Touch