Managed Digital Workplace Services Market Report Scope & Overview:

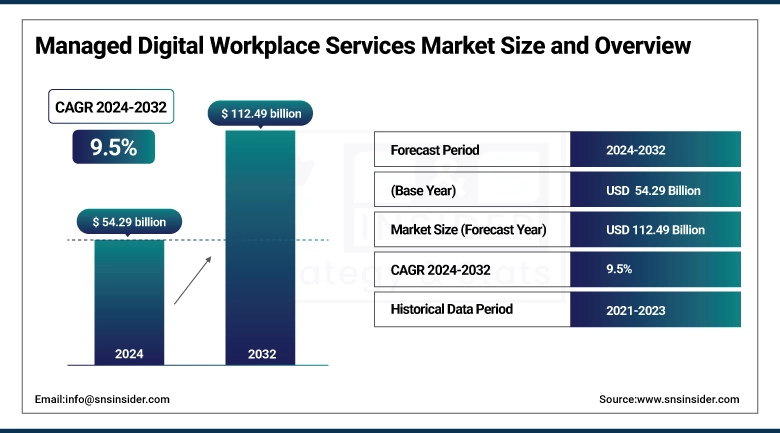

The Managed Digital Workplace Services Market size was valued at USD 54.29 billion in 2024 and is expected to reach USD 112.49 billion by 2032, expanding at a CAGR of 9.5% over the forecast period of 2025-2032.

The Digital Workplace Services Market is gaining rapidly as enterprises adapt to hybrid work models while harnessing digital transformation. Examples include service desk support, device management, and modern workplace solutions that improve productivity and minimize IT complexity. The market is dominated significantly by big businesses; SMEs, too, are embracing managed services for flexibility and cost-effectiveness. A few of the key drivers include AI automation, cloud-based solutions, and secure, seamless remote access. Market penetration is most significant in North America, with significant expansion occurring in the Asia Pacific and Europe.

According to research, over 68% of digital workplace services now leverage cloud-native platforms, with AI and automation reducing incident handling time by up to 43% in service desk and endpoint management.

To Get more information on Managed Digital Workplace Services Market - Request Free Sample Report

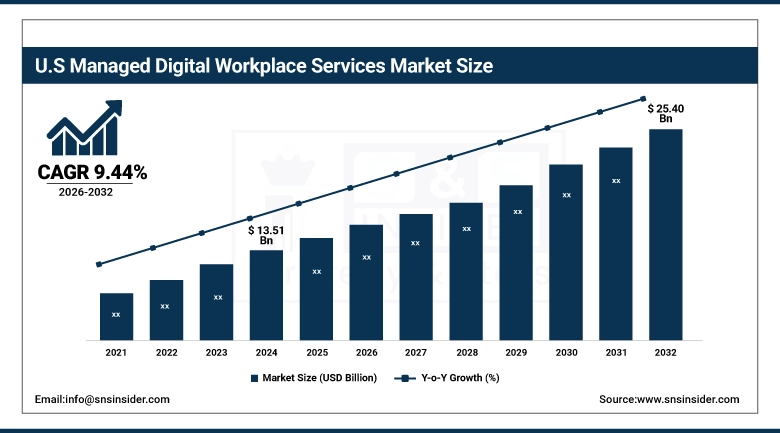

The U.S facility condition assessment market size reached USD 13.51 billion in 2024 and is expected to reach USD 25.40 billion in 2032 at a CAGR of 9.44% from 2025 to 2032.

The U.S. holds a dominant position in the global market due to its advanced IT infrastructure, high cloud adoption, and widespread implementation of hybrid work models. Organizations in managed digital workplace services industries like BFSI, healthcare, and technology are increasingly engaging in digital transformation of the workplace to drive employee productivity and satisfaction. Early adoption of AI-based tools, the need for smooth remote collaboration, and the availability of top-notch managed services providers are key drivers. Consistent innovation and focus on digital employee experience solidify the U.S. market's leadership position in this space even more.

Market Dynamics

Drivers:

-

Increasing Focus on Employee Experience and Remote Collaboration Tools Drives Market Expansion Across Industries.

Digital workplace services are slowly being adopted by organizations to promote the overall employee experience and productivity. Though the reason behind the adoption of managed workplace services is unclear. To facilitate distributed and hybrid workforces, businesses will implement intelligent collaboration platforms, unified communication tools, and AI-driven support systems. Emerging technologies such as Virtual Desktop Infrastructure, cloud-based productivity suites, and self-service portals only add fuel to this fire. Executive Summary: There has been a growing demand for employee experience platforms among organizations recently, with large vendors adding analytics and automation capabilities to help enhance remote collaboration and performance monitoring.

Restraints:

-

High Implementation and Transition Costs Hinder Widespread Adoption Among Cost-Sensitive Enterprises.

Although managed digital workplace services offer long-term benefits, their adoption has been limited by the need for a high upfront investment in time and money to implement and transition to them. They are usually quite costly for Enterprises as they need to overhaul their existing IT infrastructure, software licensing, integration with their legacy systems, and a huge workforce that needs to be trained. These services, especially when their cost-benefit and outright cost are hard to justify, are not attractive to small and medium-sized businesses that often don't have the budgets to spend on them.

Opportunities:

-

Rising Adoption of Cloud-Native and AI-Driven Solutions Presents Significant Growth Prospects for Service Providers.

Service providers can capitalise on the increasing adoption of cloud-native platforms and AI-enabled technologies to offer digital workplace solutions that are innovative, scalable, and cost-effective. More and more enterprises are migrating to the cloud as a means to improve flexibility, reduce infrastructure costs, and support a remote workforce. So here are a few of the recent managed digital workplace services market trends showcasing the integration of AI for predictive support or intelligent automation, and personalized user experiences. The hybrid-enabled solutions, like hybrid cloud enabling solutions, as well as digital experience monitoring tools, are being adopted by many organizations across industries, including finance and healthcare, which is bringing more opportunities in the global digital experience monitoring market.

Challenges:

-

Lack of Standardization and Integration Challenges Across Diverse IT Ecosystems Impede Service Efficiency and User Satisfaction.

The lack of standardization and the complexities involved in integrating divergent IT ecosystems are one of the leading obstacles in delivering managed digital workplace services. Enterprises have to work across many platforms, devices, and applications, resulting in poor seamless interoperability and service delivery. Integration problems when apps do not connect effectively can create data silos, lower automation speed slashes, and a broken user experience. Additionally, varying enterprise requirements often necessitate personalized solutions from service providers, adding further complexity and cost to a project.

Segment Analysis

By Services

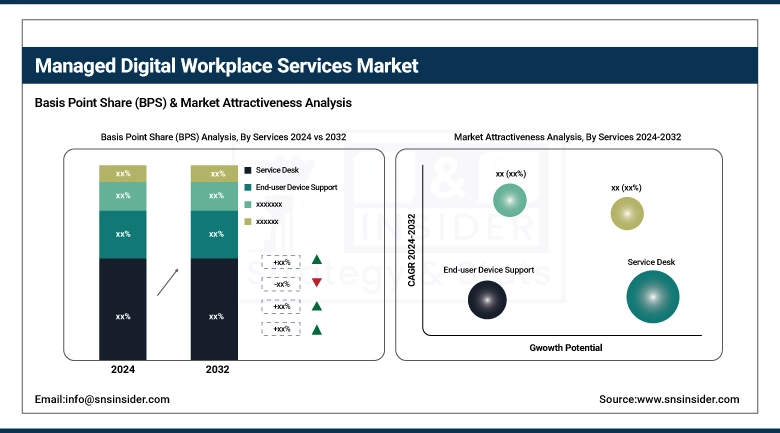

In 2024, the Service Desk segment held the largest market share, at 36.27%, due to the growing need for 24/7 IT support, remote troubleshooting, and improved employee experience. Enterprises have the expectation that their ticketing systems are efficient, fast at resolving issues, and can seamlessly handle multiple issues. Important developments include the upgrades of its service desk with AI by IBM and the introduction of intelligent IT support opportunity platforms by HCL Technologies for productivity integration. This segment also continues to gain more momentum due to increasing reliance on automation and self-service capabilities.

The Digital Workplace segment is expected to grow at the fastest CAGR of 10.99%, owing to the growing adoption of cloud-based collaboration tools, virtual desktops, and artificial intelligence-driven productivity solutions. As organizations are moving towards unified digital workspaces to run their operations and to accommodate remote, as well as hybrid, workforces, other things include Citrix becoming digital workspace delivery and Workspace ONE developments at VMware. This is a response to ever-increasing expectations of personalized user experiences along with centralized control for IT.

By End-user Vertical

In 2024, the BFSI sector emerged on top with a revenue share of 25.27%, driven by its reliance on secure, compliant, and optimized digital and remote workplaces. Financial institutions focus on secured data storage, access from remote locations as well as compliance with regulatory standards, exactly the areas managed digital workplace caters to. The BFSI sector drives growth as digital transformation becomes essential for customer engagement and ensuring operational resilience.

Examples are Accenture, which integrated managed services against global banks, and Infosys, which deployed a digital workplace for financial Institutions.

The Healthcare segment will grow at 12.87% CAGR due to more digitized patient care, a broader telehealth market, and secure access to EHRs. From the clinical space to administrative arenas, hospitals and health systems want compliant and dependable digital environments for their clinical staff and administration teams. Fujitsu has released smart hospital solutions, while Dell has announced healthcare-optimized workplace platforms. This growth is supported by the HIPAA-compliant focus, real-time collaboration tools, and mobile health app.

According to research, in the healthcare sector, the integration of telehealth and remote diagnostics has fueled a 14.5% yearly growth in demand for managed digital workplace platforms.

By Organization Size

In 2024, the large enterprise segment has the largest managed digital workplace services market share of 60.42%, owing to the complex IT infrastructures comprising large enterprises with multiple offices across the world, with a larger budget for digital transformations. Such organizations require scaling, integrated, and safe digital workplace solutions. They also include enterprise-wide deployments from Atos, as well as integrated collaboration platforms from Cisco designed for large corporations.

The SME market is anticipated to register the fastest CAGR of 11.68%, as small managed digital workplace services market companies are opting for managed digital workplace solutions to transform their IT at an economical pace. With fewer in-house IT resources, SMEs are searching for outsourced solutions to manage devices, remote support, and secure collaboration. Recent developments on these lines have come from the likes of TCS with their SME focused cloud workplace offerings and VMware simplifying the workspace for small businesses. This is being driven, in part, by the growing adoption of SaaS platforms, flexible pricing models, and digital agility.

Regional Analysis

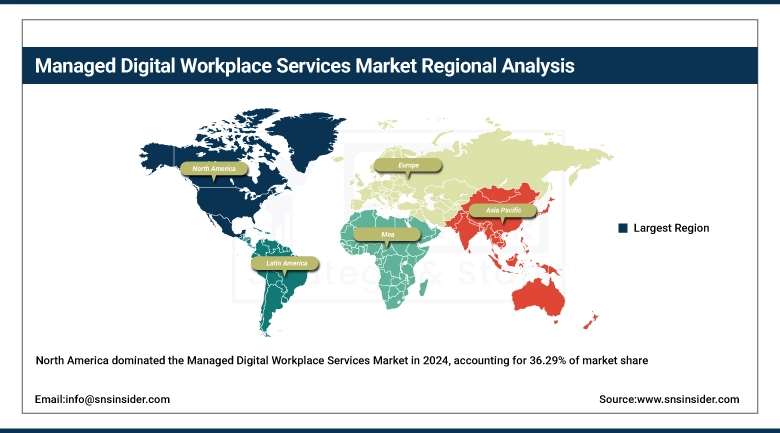

North America held the largest market share with 36.29% of the market. The high managed digital workplace services market growth is due to the early adoption of hybrid work models by businesses in the region, advanced IT infrastructure, and the presence of notable players such as IBM, Dell Technologies, and Cisco. Companies across different industries have embraced new service paradigms, AI-based platforms, and virtual devices to contribute to the productivity of their labor force as well as business continuity.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States dominates the region with its established digital ecosystem, extensive cloud adoption, and enterprise demand for large-scale, secure workplace solutions.

The European region accounts for a considerable portion of the market, owing to the presence of various data privacy regulations, the growing emphasis on digital sustainability in public and private IT system upgrades. Germany, the UK, and France are investing heavily in secure remote work infrastructure across the BFSI and government sectors.

Germany continues to lead Europe, driven by industrial digitalization, manufacturing base, and demand for unified endpoint & service desk solutions.

Asia Pacific is the region with the fastest growth at an estimated CAGR of 11.84%, Digital transformation projects across emerging economies, growth in mobile workforce adoption, and investments in cloud infrastructure continue to push revenue growth in the region. As the acceleration to managed IT services to support scalability and reduce complexity continues, countries like India, China and Japan are going through transformation at a breakneck speed.

India dominates due to its growing IT services sector, growing digitalization of the SME sector, and also support from the government for cloud-first and digital workplace strategies.

In the MEA & Latin America regions, continue to see strong growth in managed digital workplace services (MDWS) fuelled by digital transformation along with the intelligent information technology (IT) infrastructure development and cloud adoption, while the UAE and Brazil lead with strategic investments and enterprise modernization.

Key Players

The major key players of the managed digital workplace services market are Accenture, IBM, HCL Technologies, Tata Consultancy Services (TCS), DXC Technology, NTT Data, Infosys, Fujitsu, Atos, Dell Technologies, and others.

Key Development

-

In March 2024, DXC Technology was recognized as a Leader in the Gartner Magic Quadrant for ODWS based on DXC Uptime, an AI-powered Modern Workplace platform that applies generative AI to enrich digital employee experiences.

-

In February 2024, Accenture joined hands with NVIDIA to initiate its AI refinery initiative to upskill 30000 employees to continue to scale enterprise AI adoption faster with drill-down capabilities for specific solutions for specific industries.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 54.29 Billion |

| Market Size by 2032 | USD 112.49 Billion |

| CAGR | CAGR of 9.5% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Services (Service Desk, End-user Device Support, Digital Workplace) •By End-user Vertical (BFSI, Healthcare, Manufacturing, Energy and Utility, Government and Public Sector, Other End-user Verticals) •By Organization Size (Small and Medium-Sized Enterprises (SMEs), Large Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Accenture, IBM, HCL Technologies, Tata Consultancy Services (TCS), DXC Technology, NTT Data, Infosys, Fujitsu, Atos, Dell Technologies. |

Get in Touch