Third-Party Risk Management Market Report Scope and Overview:

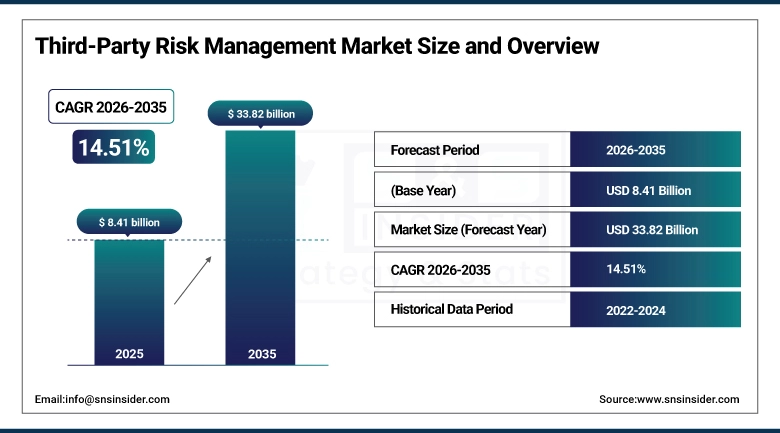

The Third-Party Risk Management Market was valued at USD 8.41 billion in 2025 and is expected to reach USD 33.82 billion by 2035, growing at a CAGR of 14.51% from 2026-2035.

The Third-Party Risk Management industry is changing quickly as more companies are relying on their vendors, cloud providers, software providers, logistics providers, and even outsourced business functions for conducting their activities. With the digital transformation in mind and connectivity within the company's IT system, third-party risks have been increased due to cybersecurity risks, regulatory risks, operational risks, and reputation risks.

Third-party risk management tools including AI-based risk intelligence software, automated vendor assessment, risk monitoring solutions, and predictive analytics software are being used by companies to manage third-party risks. Increased cases of cyber threats against an organization’s third-party vendors, ransomware attacks, data breaches, and regulatory sanctions have led businesses to implement third-party risk management systems. Furthermore, the requirement of adhering to strict regulations such as GDPR, DORA, HIPAA, and financial regulations has forced companies to implement continuous third-party risk management programs.

Third-Party Risk Management Market Size and Forecast

-

Market Size in 2025: USD 8.41 Billion

-

Market Size by 2035: USD 33.82 Billion

-

CAGR: 14.51% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Third-Party Risk Management Market - Request Free Sample Report

Third-Party Risk Management Market Trends

-

Quicker implementation of AI-powered vendor risk ratings and compliance management automation.

-

More reliance on continuous monitoring tools that can provide real-time assessments of vendor cybersecurity positions.

-

A greater number of cloud-based third-party risk management systems employed by small and medium enterprises thanks to the lower cost of maintenance.

-

The growing popularity of predictive analytics aimed at identifying risks linked to disruptions within the supply chain.

-

Advancements in terms of ESG sustainability risk management capabilities offered by vendor risk management solutions.

-

Much higher regulatory pressures in such verticals as BFSI, healthcare, and critical infrastructure leading to GRC-driven adoption.

-

Greater demand for GRC integration capabilities.

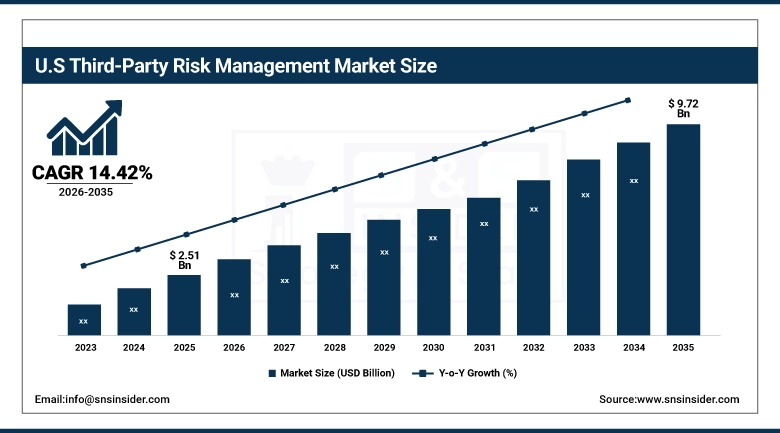

U.S. Third-Party Risk Management Market was valued at USD 2.51 billion in 2025 and is expected to reach USD 9.72 billion by 2035, growing at a CAGR of 14.42%.

The USA boasts considerable dominance in the North American market owing to the high rate of investments made by the organization into cybersecurity, effective regulatory measures, and the presence of risk management software vendors. The increasing cases of cyber-attacks against supply chain providers and software-as-a-service providers are motivating enterprises to invest in vendor management and compliance monitoring solutions. Several major industry segments such as BFSI, health care, IT & Telecom, and governments are embracing artificial intelligence risk intelligence solutions.

The growing use of cloud services and digital transformation trends among organizations will increase the complexities of the third party ecosystem and fuel market growth.

Third-Party Risk Management Market Segment Analysis

-

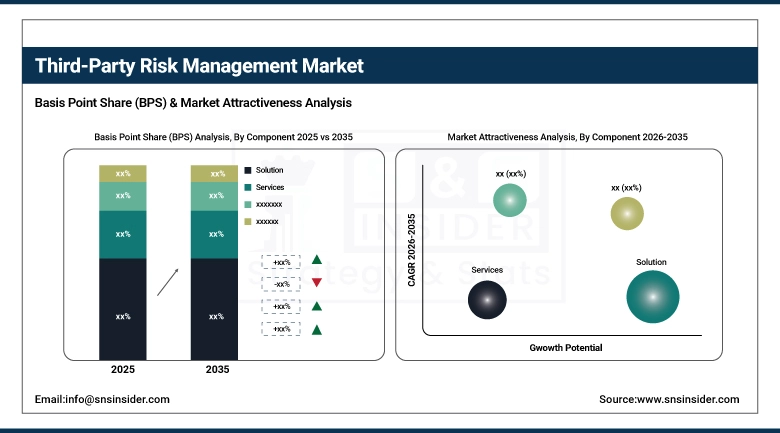

Based on Component, Solutions dominated the market in 2025 with approximately 64.2% revenue share, while Services are expected to witness the fastest growth during the forecast period.

-

Based on Deployment Mode, Cloud-based solutions accounted for nearly 63.2% market share in 2025, while on-premises are expected to witness the fastest growth during the forecast period.

-

Based on Organization Size, Large Enterprises dominated the market in 2025 with around 68.1% share due to high vendor exposure and regulatory requirements.

-

Based on Vertical, BFSI held the largest market share of approximately 26.4% in 2025, while Healthcare and Life Sciences is expected to register the fastest CAGR through 2035.

By Component, Solutions dominated while Services are expected to grow fastest

The Solutions segment held the majority market share in 2025 as there was growing demand among enterprises for risk assessment, continuous monitoring, regulatory compliance management, and workflow management platforms from vendors. There was an increase in the deployment of third-party risk management solutions, which included capabilities such as cyber security assessment, operational risks analysis, ESG (Environment, Social, and Governance), and regulatory compliance reporting features.

The Services segment is projected to witness the highest CAGR between 2026 and 2035 due to growing demand for consulting, managed services, and vendor continuous monitoring solutions. Several organizations were outsourcing their vendor risk assessment processes to vendors to address any skill gaps they might have.

By Deployment Mode, Cloud dominated the market, on-premises growing rapidly

The reason behind cloud deployment being a dominant segment was due to less initial capital investment, scalability, quick deployment ability, and easy compatibility with the organization’s ecosystem. Cloud-based solutions for third-party risk management are allowing enterprises to automate vendor assessments and monitor supplier risks consistently irrespective of geographic locations.

On the other hand, on-premise deployment still holds significance in highly regulated industries like governments and defense, where data sovereignty is the top priority for the enterprises.

By Organization Size, Large Enterprises dominated the market, SME’s growing fastest

The majority market share was attributed to large organizations, which had large third-party ecosystems, global supply chains, and were subject to strict compliance regulations. Such organizations have thousands of vendors that necessitated a sophisticated monitoring system with machine learning analytics and centralization features.

The increased interest in third-party risk management systems by small and medium-sized businesses has been attributed to the increased risk of cyber-attacks and lower costs.

By Vertical, BFSI dominated while Healthcare and Life Science expected to grow fastest

The BFSI sector was the leading player in the market due to strict financial regulatory compliance, susceptibility to cybersecurity risks, and increased use of outsourced digital banking services and fintech vendors. The BFSI sector is adopting continuous monitoring tools to enhance vendor management and operational resilience.

The healthcare and life science sector is expected to have the highest CAGR over the forecast period because of the growing digitization of healthcare systems, increasing concern about patient data privacy, and growing connectivity of healthcare facilities.

Third-Party Risk Management Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~76% |

|

Europe |

United Kingdom |

~24% |

|

Asia Pacific |

China |

~38% |

|

Middle East and Africa |

UAE |

~29% |

|

Latin America |

Brazil |

~47% |

North America Third-Party Risk Management Market Insights

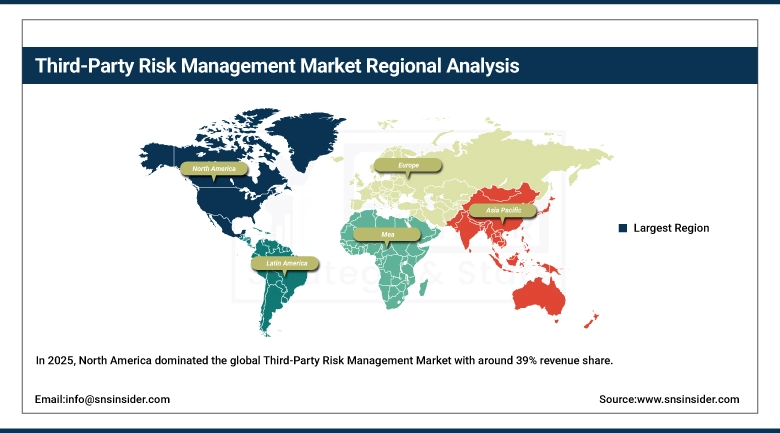

In 2025, North America held its dominance in the Third-Party Risk Management Market worldwide, contributing around 39% to the total global revenue. High expenditure on cybersecurity, digitalization of enterprises, and stringent regulations for compliance in the United States and Canada have been driving the growth of the Third-Party Risk Management Market in North America. The wide prevalence of cloud technology and use of AI-based risk analysis tools and cybersecurity governance platforms among larger enterprises and financial organizations in the region are fueling demand for third-party risk management solutions. The growing incidents of ransomware attacks, software supply chain attacks, and third-party data breaches continue to drive the adoption of vendor compliance and monitoring systems. Compliance with regulations such as the Health Insurance Portability and Accountability Act (HIPAA), Sarbanes-Oxley Act (SOX), and Securities and Exchange Commission (SEC) guidelines for cybersecurity disclosures have been fueling the adoption of third-party risk management solutions among enterprises.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Third-Party Risk Management Market Insights

Asia-Pacific is expected to witness the fastest CAGR in the worldwide Third-Party Risk Management Market over the forecast period of 2026-2035 owing to the high rate of digital transformation among enterprises in this region, widespread use of cloud infrastructure and rising Fintech Ecosystems in China, India, Japan, South Korea, and South-East Asia. The rising trend towards the outsourcing of Information Technology services and third-party ecosystems coupled with the digitization of banking platforms is driving organizations towards improved risk management and cybersecurity resilience in relation to their third-party service providers. Governments in Asia-Pacific are introducing stricter data protection rules and frameworks for compliance in order to enhance the security of digital infrastructure. The countries of China and India have been experiencing rising demand owing to the expansion of cloud infrastructures as well as cybersecurity consciousness among enterprises.

Europe Third-Party Risk Management Market Insights

Europe plays an important role in the global third-party risk management market due to the presence of strict data protection laws, mature enterprise cybersecurity ecosystems, and growing demand for comprehensive compliance management tools in Germany, the UK, France, and Nordic nations. Regulations such as GDPR, DORA, NIS2, and supply chain cybersecurity requirements have led to greater enterprise pressure on improving third-party risk management and monitoring systems. Banks, hospitals, manufacturers, and other enterprises have started leveraging AI-powered third-party risk management solutions to handle third-party vendors’ risks related to cybersecurity, operations, and regulatory non-compliance. The UK and Germany continue to be the biggest regional markets on account of robust enterprise cybersecurity spending and advanced digital ecosystem. Increasing focus on operational resilience, ESG requirements, and improved supply chain transparency keeps driving third-party risk management market opportunities.

Latin America Third-Party Risk Management Market Insights

The Third-Party Risk Management market is experiencing growth in the Latin America region, owing to factors such as enterprise digitization, cyber security breaches, and increased use of cloud computing by organizations located in Brazil, Mexico, Argentina, and Colombia. Organizations belonging to sectors including banking, telecommunications, and government bodies are increasingly adopting third-party risk management software in order to enhance vendor management, mitigate risks, and manage their compliance. Brazil represents the largest market among Latin American countries owing to growing investments in cyber security infrastructure and the implementation of LGPD laws. Increased awareness regarding the threats posed by third party cyber-attacks and outsourcing services risk management have fueled the demand for risk management solutions in the region.

Middle East & Africa Third-Party Risk Management Market Insights

The Middle East & Africa (MEA) region is witnessing an increase in demand in the Third-Party Risk Management Market owing to the growing investment in digital infrastructure, growing focus on cybersecurity, and increasing deployment of cloud computing among enterprises in the UAE, Saudi Arabia, and South Africa. The MEA region has started realizing the importance of cybersecurity and vendor risk management as they move towards digital transformation in their banks, energy sector, telecommunications industry, and public administration organizations. Saudi Arabia and UAE have emerged as major adopters in the region owing to their smart city initiatives, financial services modernization efforts, and development of national-level cybersecurity strategies. Growing worries around cyber threats in supply chains, regulatory compliance, and third-party operations are contributing towards the demand for third-party risk management solutions in the region.Top of Form

Bottom of Form

Market Growth Drivers:

-

Rising cybersecurity threats and supply chain attacks driving enterprise investment in vendor risk monitoring

With an increasing number of ransomware attacks, data breaches, and cyber-attacks in the supply chain, the management of third-party risks has become essential. The businesses have come to realize the importance of vulnerabilities that can pose a threat to their functioning and reputation as well as regulatory concerns. The prominent cyber incidents related to software vendors and cloud service providers have made businesses take steps toward effective monitoring and vendor assessments.

Market Restraints:

-

High implementation complexity and lack of standardized risk assessment frameworks

While more and more demands are being placed on organizations, however, they face challenges stemming from complicated implementations, integrations, and lack of standard methodologies when it comes to the assessment of vendors. Organizations struggle with collecting information regarding vendors due to their scattered nature across various departments.

Market Opportunities:

-

AI-powered predictive analytics and automation creating next-generation growth opportunities

The increased application of AI is providing many promising avenues for developing intelligent third-party risk management platforms. Predictive analytics based on artificial intelligence technologies can automatically score vendors, identify any anomalies immediately, and predict potential threats to operations and cyber safety.

Recent Developments:

-

2026: The AI-based third-party risk intelligence capabilities by IBM were bolstered via increased automation and predictive analytics integration in their governance software platform offerings.

-

2025: Advanced vendor lifecycle management capabilities by ServiceNow allowed for real-time risk monitoring and automated compliance processes.

Third-Party Risk Management Market Key Players

Some of the Third-Party Risk Management Market Companies

• IBM Corporation

• Deloitte

• ServiceNow

• OneTrust

• RSA Security

• MetricStream

• ProcessUnity

• LogicGate

• NAVEX

• Archer Technologies

• SAP SE

• PwC

• BitSight Technologies

• RapidRatings

• Genpact

• KPMG

• EY

• Prevalent Inc.

• Venminder

• Resolver Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.41 Billion |

| Market Size by 2035 | USD 33.82 Billion |

| CAGR | CAGR of 14.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Services) • By Deployment Mode (Cloud, On-premises), By Organization Size (SMEs, Large Enterprises) • By Vertical (BFSI, IT and Telecom, Healthcare and Life Sciences, Government, Defense, and Aerospace, Retail and Consumer Goods, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Deloitte, ServiceNow, OneTrust, RSA Security, MetricStream, ProcessUnity, LogicGate, NAVEX, Archer Technologies, SAP SE, PwC, BitSight Technologies, RapidRatings, Genpact, KPMG, EY, Prevalent Inc., Venminder, and Resolver Inc. |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 16.5% in the Third-Party Risk Management Market.

BFSI dominated with approximately 26% share in 2025.

Solution held approximately 62% share in 2025.

The Third-Party Risk Management Market was valued at USD 8.41 Billion in 2025.

The Third-Party Risk Management Market is expected to grow at a CAGR of 14.51% from 2026 to 2035.

Get in Touch