Medical Cyclotron Market Report Scope & Overview:

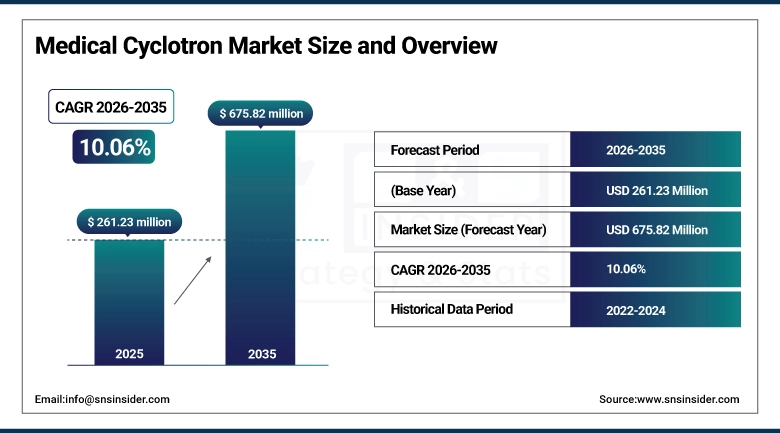

The Medical Cyclotron Market size is valued at USD 261.23 Million in 2025 and is projected to reach USD 675.82 Million by 2035, growing at a CAGR of 10.06% during the forecast period 2026–2035.

This Medical Cyclotron Market analysis report delivers comprehensive insights on market dynamics, advancements in technology, and medical applications. The factors such as rising demand for PET scans, high cancer cases, adoption of small and superconducting cyclotrons, and installation in hospitals have been boosting the market significantly over 2026-2035.

The number of medical cyclotron installations surpassed 1,000 in 2025 due to increasing cancer diagnoses, investments in the isotope production in hospitals, and usage of low-energy cyclotrons for Fluorine 18 production.

Medical Cyclotron Market Size and Forecast:

-

Market Size in 2025: USD 261.23 Million

-

Market Size by 2035: USD 675.82 Million

-

CAGR: 10.06% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Medical Cyclotron Market - Request Free Sample Report

Medical Cyclotron Market Trends:

-

The increasing number of installations of cyclotrons in hospitals to minimize dependency on centralized radiopharmaceutical supplies for hospitals.

-

The use of cyclotrons in the diagnostic process for oncology treatments due to increased cancer cases.

-

Implementation of cyclotron systems along with imaging devices and AI workflows in the diagnosis process.

-

Increase in investment in multi-isotope cyclotrons in order to serve multiple applications such as neurology and cardiology.

-

Increased demand for cyclotrons across the Asia-Pacific countries with development in healthcare infrastructure.

-

Growing concentration on making the equipment more economical to minimize operating costs.

-

Collaborations of research institutions and hospitals for developing new innovations related to isotope production.

-

Concentration of regulatory authorities on safety and quality standards in producing isotopes for cyclotrons.

U.S. Medical Cyclotron Market Insights:

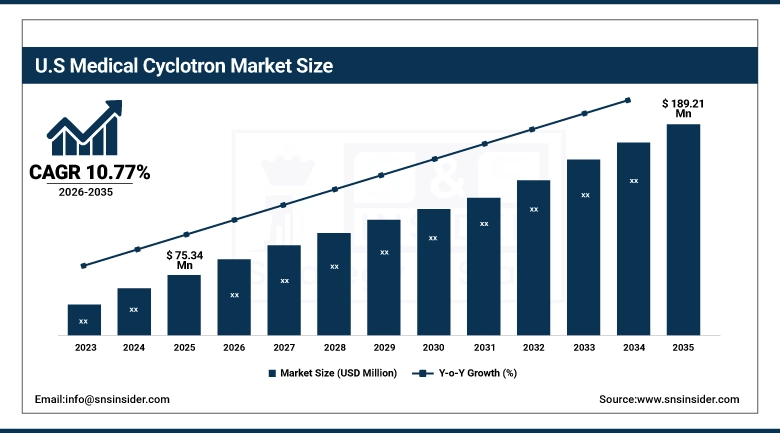

The U.S. Medical Cyclotrons Market will reach USD 75.34 Million in 2025 and is expected to grow to USD 189.21 Million by 2035 at a CAGR of 10.77%, driven by oncology imaging applications, decentralized production of isotopes, and growth in the number of hospital-based cyclotrons. The market is additionally boosted by developments in the efficiency of isotope production, integration into diagnostic imaging systems, and expansion of healthcare infrastructure in key states.

Medical Cyclotron Market Growth Drivers:

-

Rising cancer incidence and expanding use of PET/CT imaging are driving demand for cyclotron‑produced isotopes in oncology diagnostics.

The U.S. Medical Cyclotron Market is experiencing growth due to the rising demand for compact and superconducting cyclotrons in hospitals and cancer facilities. Improved efficiency in production, the association with advanced imaging systems, and more decentralized production channels have boosted the market. The use of medium energy cyclotrons for multiple isotope production along with better sustainability and lower costs has driven the adoption rate.

More than 62% of hospitals and cancer treatment facilities in the United States used cyclotron produced isotopes for PET imaging and diagnostics in 2025.

Medical Cyclotron Market Restraints:

-

High installation and maintenance costs are limiting broader adoption of advanced cyclotron systems.

The US Medical Cyclotron Market is likely to face challenges in terms of high costs incurred in procuring cyclotrons, setting up facilities, and other operational costs. Besides, the high regulatory framework required to produce isotopes and the requirement for technical know-how pose a challenge to adoption rates. In addition, inadequate reimbursement policies for nuclear medicine treatments, alongside a shortage of skilled personnel to handle radiopharmaceuticals, limits growth in small hospitals and regional facilities.

By 2025, more than 41% of hospitals and cancer care centers were faced with challenges in terms of costs and regulations to adopt medical cyclotrons.

Medical Cyclotron Market Opportunities:

-

Expanding applications of PET imaging beyond oncology are opening new opportunities for cyclotron‑based isotope production.

It is expected that the future of the market will get a boost from rising demand from neurology, cardiology, and infections diagnostics due to the increasing use of positron emission tomography. In addition, improvements in multi-isotope cyclotrons and their incorporation in hybrid imaging systems are contributing towards their application in clinical settings. Moreover, increased government/private funding for nuclear medicine studies and decentralization of isotope production are providing impetus to the market.

In the year 2025, more than 36% of US-based research centers and specialty clinics are seen using cyclotrons beyond oncological uses.

Medical Cyclotron Market Segmentation Analysis:

-

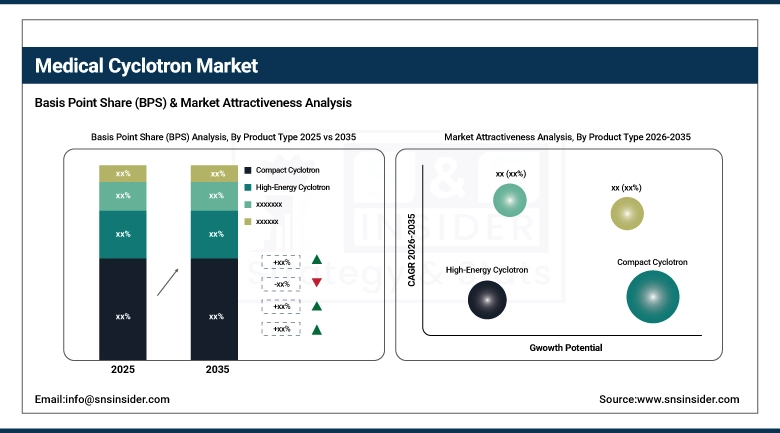

By Product Type, Compact Cyclotron held the largest market share of 55.46% in 2025, while Superconducting Cyclotron are expected to grow at the fastest CAGR of 13.48% during 2026–2035.

-

By Component, Target System dominated with 29.54% market share in 2025, whereas they are also projected to record the fastest CAGR of 9.24% through 2026–2035.

-

By Installation Type, Hospital-based accounted for the highest market share of 48.62% in 2025, while Centralized production facilities are expected to grow at the fastest CAGR of 11.21% during the forecast period.

-

By Energy Level, Medium-energy (12–20 MeV) dominated with a 39.36% share in 2025, while Low-energy (<12 MeV) are anticipated to expand at the fastest CAGR of 11.00% through 2026–2035.

-

By End-User, Hospitals held the largest share of 41.63% in 2025, while Research Institutes are expected to grow at the fastest CAGR of 10.99% during the forecast period.

By Product Type, Compact Cyclotron dominates while Superconducting Cyclotron grows rapidly:

The Compact Cyclotron market segment dominated the industry owing to the wide usage of these systems in hospitals and oncology centers for producing stable isotopes in a smaller setup and at reduced costs. Their ability to efficiently help in positron emission tomography (PET) makes them the most preferred option for decentralized institutions.

Superconducting Cyclotron is emerging as the fastest-growing segment, mainly due to their technical advancement, high energy, and versatility in advanced research and multiple isotope production. They also offer significant operational efficiency and reduced footprint, making them increasingly attractive for hospitals and research institutes seeking sustainable, high‑performance solutions.

By Component, Target System dominates while also growing fastest:

The Target System component had a dominant market share due to its crucial function in the production of isotopes and extensive usage in hospitals and laboratories for various applications. The high efficiency, reliability, and significance of the target system in the production of radiopharmaceuticals make it the ideal selection for health care organizations.

Target System is expected to grow at the fastest rate due to the continuous advancements in technology. It will emerge as the leading and most dynamic component of the market in the upcoming decade. Additionally, its critical role in enhancing isotope yield and improving operational efficiency makes it indispensable for hospitals and research facilities.

By Installation Type, Hospital‑based dominates while Centralized facilities grow fastest:

The hospital-based system installations held a leading position in the industry due to its significant contribution to the prompt availability of isotopes used in PET scans and oncology diagnostic procedures. Convenience, efficiency, and decentralization capabilities make it the first choice among health care institutions.

The centralized production systems are gaining momentum and proving themselves to be the most dynamic part of the market, thanks to high-volume production, efficient distribution processes, and growing collaboration with regional cancer facilities and research centers.

By Energy Level, Medium‑energy dominates while Low‑energy grows fastest:

Medium Energy Cyclotrons were the leading products in the market in 2025 owing to their flexibility in creating a variety of isotopes for use in both diagnosis and therapy purposes. The capability of generating multiple isotopes makes medium energy cyclotrons the most popular among large hospitals and research centers.

Low Energy Cyclotrons are becoming the fastest growing category due to the increasing usage of PET isotopes, including Fluorine 18, small size, and adoption in hospitals for cancer diagnosis. They also provide cost‑effective solutions with easier installation and maintenance, making them highly attractive for decentralized healthcare facilities.

By End‑User, Hospitals dominate while Research Institutes grow fastest:

The Hospital sector accounted for the dominant market share during the forecast period, mainly due to the fact that these centers provide direct access to the use of isotopes for PET scanning and diagnostics in oncology. The infrastructure developed at hospitals makes them leading consumers.

Research Institutions will prove to be the most rapidly growing sector of the industry due to the increase in clinical research, the development of isotopes, and collaboration with academic and healthcare facilities. They also play a pivotal role in advancing innovation, fostering new diagnostic and therapeutic applications.

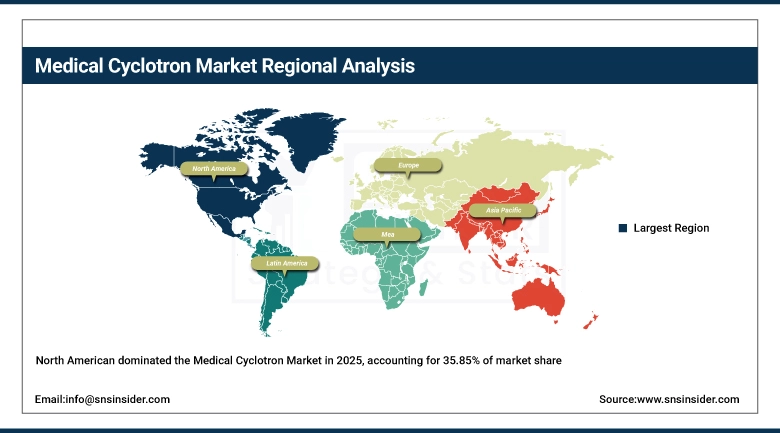

Medical Cyclotron Market Regional Analysis:

North America Medical Cyclotron Market Insights:

The North American region leads in the market with market share of 35.85%, with the help of its developed health care system, high prevalence of cancer cases, and extensive use of PET technology. Hospitals and clinics are making increasing investments in smaller-sized cyclotrons for decentralized production of isotopes. The growing number of autoimmune and inflammatory diseases, along with sophisticated biological drugs and targeted therapies, further aid market growth. Favorable reimbursement systems, expert clinicians, and innovative developments in oral, injectable, and intravenous drugs will make North America a stable market until 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Medical Cyclotron Market Insights:

The United States is the leading country in the North American market, thanks to a high incidence of organ transplantations, a good healthcare infrastructure, and widespread use of cyclotron produced isotopes in oncology diagnosis. High incidences of auto-immune and inflammatory conditions, establishment of new specialized hospitals, and growing demand for biologicals and mAbs are contributing factors towards growth in this market.

Asia‑Pacific Medical Cyclotron Market Insights:

The fastest-growing market region is that of Asia-Pacific with CAGR of 11.78%, which is experiencing increased incidences of cancers and improved health care infrastructures coupled with government spending on nuclear medicine. Medical institutions have been adopting smaller and superconducting cyclotrons to enhance access to PET imaging. Increased demand for innovative treatments and supportive regulatory frameworks are some of the factors behind the rapid adoption. In regions such as India, Japan, and South Korea, the market region is showing tremendous growth in the coming years up to 2035.

China Medical Cyclotron Market Insights:

China represents an important growth driver in Asia Pacific, bolstered by rapid development of healthcare infrastructure, high cancer incidence rates, and the government’s strong emphasis on nuclear medicine. The installation of small cyclotrons in hospitals to localize isotope generation and cater to the increasing demands for PET scans is becoming more common. Investments in research facilities, partnerships with international technology companies, and favorable policies have driven rapid uptake.

Europe Medical Cyclotron Market Insights:

Europe is a developed market characterized by highly advanced healthcare systems, regulatory environments, and the use of PET scanning equipment. Hospitals and research centers have been increasingly acquiring medium-energy cyclotrons that will help in manufacturing various isotopes for the application in oncology, cardiology, and neurology. Increased cases of cancer, favorable payment schemes, and university-hospital partnerships have driven growth further. Innovation within the cyclotron market and development of imaging devices has ensured that Europe remains a consistent and growing market throughout the forecast period.

Germany Medical Cyclotron Market Insights:

Germany is at the forefront of the European market, thanks to its advanced healthcare facilities, research potential, and extensive use of PET scanning technology. Hospitals and cancer centers have been employing small to medium-energy cyclotrons to produce various types of isotopes. This is made possible by government funding, research, and partnerships with universities.

Latin America Medical Cyclotron Market Insights:

Latin America represents an emerging market, based on increasing rates of cancer, the development of healthcare facilities, and the increased use of PET imaging systems. Institutions are increasingly acquiring small-size cyclotrons in order to move isotope production from centralized locations. The efforts of governments to enhance nuclear medicine access, together with partnerships with foreign firms, are driving the market.

Middle East & Africa Medical Cyclotron Market Insights:

Middle East & Africa is emerging as an emerging market for cyclotron-based PET scans due to increasing rates of cancer, improved healthcare facilities, and the need for diagnostic tools such as diagnostic imaging. Hospitals and specialty centers are adopting small-scale cyclotrons as the trend in PET imaging advances. The government's efforts towards improving the healthcare sector, in conjunction with the partnership between the government and international technology companies, have contributed towards its development.

Medical Cyclotron Market Competitive Landscape:

GE Healthcare is one of the top medical technologies’ companies in the United States with a significant footprint in the market of medical cyclotrons, especially through innovative PET imaging solutions and radiopharmaceutical manufacturing equipment. The company places considerable emphasis on innovations in cyclotrons with high energy and small size, thus ensuring consistent supply of isotopes to hospitals and cancer treatment centers around the world.

-

In February 2025, GE Healthcare announced enhancements to its PET/CT portfolio, integrating cyclotron‑based isotope production with AI‑driven imaging workflows to improve diagnostic accuracy and efficiency.

Siemens Healthineers is a Germany-based multinational firm which occupies a very prominent position in the medical cyclotron industry and provides integrated solutions in nuclear medicine and imaging. Siemens specializes in small-sized cyclotrons suitable for hospitals, thanks to an established service network of the company. The core of Siemens' business approach includes accurate imaging, isotopic production efficiency, and cooperation with cancer facilities.

-

In June 2025, Siemens Healthineers expanded its collaboration with European oncology institutes to deploy hospital‑based cyclotrons, strengthening localized radiopharmaceutical supply chains.

Philips Healthcare (The Netherlands) is one of the top players in healthcare technology that is making headway in the field of medical cyclotrons by virtue of its specialty of compact and superconducting cyclotrons. Philips has made a name for itself through its innovative imaging equipment, which it couples with its technology of cyclotrons to ensure smooth diagnostic practices for PET scanning and oncological procedures.

-

In October 2025, Philips Healthcare introduced a new compact cyclotron solution designed for hospital‑based isotope production, reducing operational costs while expanding access to PET imaging in emerging markets.

Medical Cyclotron Market Key Players:

Some of the Medical Cyclotron Market Companies are:

-

GE Healthcare

-

Siemens Healthineers

-

Philips Healthcare

-

IBA Group

-

Elekta

-

Sumitomo Heavy Industries

-

Advanced Cyclotron Systems Inc.

-

Best Cyclotron Systems Inc.

-

Ion Beam Applications SA

-

Varian Medical Systems

-

Hitachi Ltd.

-

ACSI (Advanced Cyclotron Systems)

-

ProNova Solutions

-

Mevion Medical Systems

-

Nordion Inc.

-

TRIUMF

-

Ebco Industries Ltd.

-

Scanditronix

-

ACCSys Technology Inc.

-

KIRAMS (Korea Institute of Radiological & Medical Sciences)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 261.23 Million |

| Market Size by 2035 | USD 675.82 Million |

| CAGR | CAGR of 10.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Compact Cyclotron, High-Energy Cyclotron, Superconducting Cyclotron, Variable-Energy Cyclotron, Others), • By Component (Target System, Beam Transport System, Control System, Radioactive Source, Others), • By Installation Type (Hospital-based, Centralized Production Facilities, Research Laboratories, Others), • By Energy Level (Medium-energy [12–20 MeV], Low-energy [<12 MeV], High-energy [>20 MeV], Others), • By End-User (Hospitals, Research Institutes, Cancer Treatment Centers, Diagnostic Imaging Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GE Healthcare, Siemens Healthineers, Philips Healthcare, IBA Group, Elekta, Sumitomo Heavy Industries, Advanced Cyclotron Systems Inc., Best Cyclotron Systems Inc., Ion Beam Applications SA, Varian Medical Systems, Hitachi Ltd., ACSI (Advanced Cyclotron Systems), ProNova Solutions, Mevion Medical Systems, Nordion Inc., TRIUMF, Ebco Industries Ltd., Scanditronix, ACCSys Technology Inc., KIRAMS (Korea Institute of Radiological & Medical Sciences). |

Frequently Asked Questions

Research Institutes are projected to grow at the highest CAGR of 10.99%, fueled by rising cancer incidence and increasing adoption of PET/CT imaging in oncology care.

Radiopharmaceutical production for PET imaging in cancer diagnosis and treatment is the dominant application, accounting for the majority of cyclotron usage.

Hospital-based installations are growing fastest with market share of 48.62%, as healthcare providers seek in-house isotope production to reduce reliance on centralized facilities.

Centralized production facilities are the fastest-growing with CAGR of 11.21%, driven by demand for PET isotopes including Fluorine-18 in oncology diagnostics.

Compact cyclotrons hold the largest share of 55.46% due to their suitability for hospital-based isotope production, smaller footprint, and cost efficiency.

Get in Touch