Medical Device Regulatory Affairs Market Report Scope & Overview:

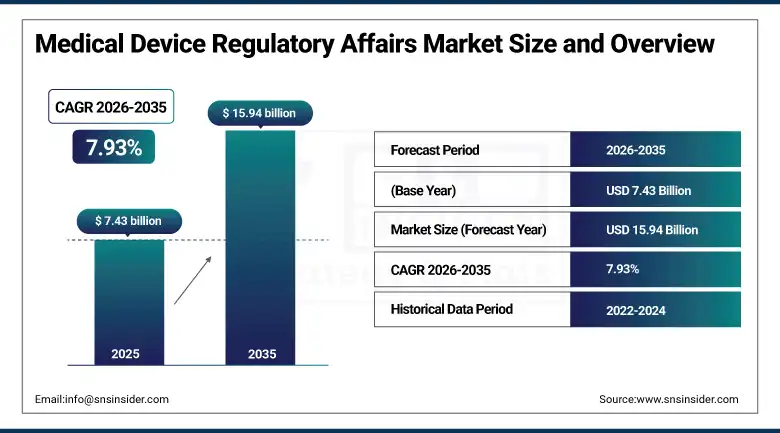

The Medical Device Regulatory Affairs Market was valued at USD 7.43 Billion in 2025 and is expected to reach USD 15.94 Billion by 2035, growing at a CAGR of 7.93% from 2026 to 2035.

Medical device regulatory affairs encompass the professional discipline and commercial service market through which medical device manufacturers navigate the complex, jurisdiction-specific, and continuously evolving regulatory approval. The commercial scale of the regulatory affairs market reflects the enormous and non-discretionary investment that medical device manufacturers make in regulatory compliance as a prerequisite for market access, rather than as a discretionary enhancement to product development.

Market growth is driven by expanding global medical device regulations. The EU Medical Device Regulation (MDR) has increased requirements for clinical evidence, certification, and post-market surveillance, creating strong demand for regulatory affairs services. In the United States, FDA compliance initiatives are supporting similar investment. Growing development of AI-enabled devices, combination products, and advanced diagnostics is further increasing the need for specialized regulatory expertise.

ICON PLC expanded its dedicated medical device regulatory affairs practice in 2025 through the acquisition of a specialist EU MDR strategy consulting firm, strengthening its capability to guide medical device manufacturers through the complex clinical evaluation and notified body submission requirements of the EU Medical Device Regulation. The acquisition reflected ICON's recognition that MDR transition assistance represents one of the most durable commercial service opportunities in medical device regulatory affairs.

Market Size and Forecast

-

Market Size in 2026E: USD 8.02 Billion

-

Market Size by 2035: USD 15.94 Billion

-

CAGR: 7.93% from 2026 to 2036

-

Fastest Growing Region: Asia Pacific

-

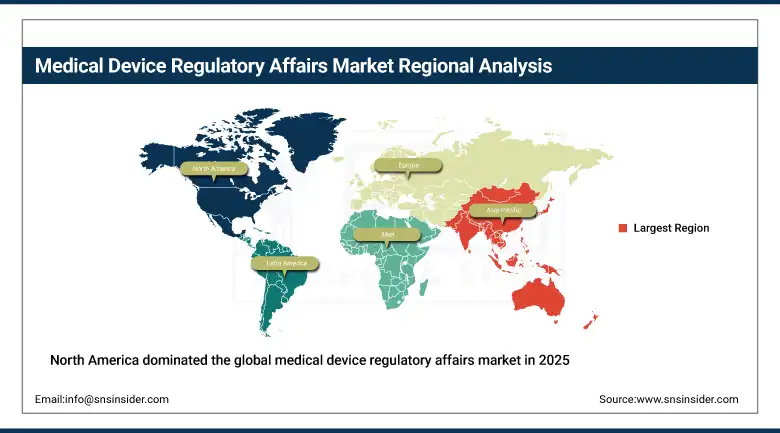

Largest Region: North America

To Get more information On Medical Device Regulatory Affairs Market - Request Free Sample Report

Medical Device Regulatory Affairs Market Trends

-

EU MDR and IVDR compliance requirements are driving strong demand for regulatory consulting and submission support services.

-

AI-enabled medical devices are creating new regulatory specialization needs as approval frameworks continue to evolve.

-

Post-market surveillance requirements are increasing demand for ongoing compliance monitoring and reporting services.

-

Digital regulatory submission platforms are improving filing efficiency and accelerating multi-country approval processes.

-

Outsourcing of regulatory affairs functions is growing as manufacturers seek specialized expertise and cost efficiency.

The U.S. Medical Device Regulatory Affairs Market Outlook

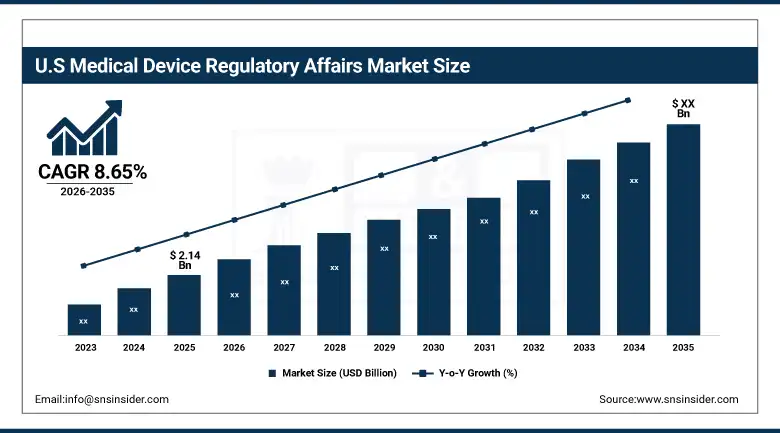

The U.S. Medical Device Regulatory Affairs Market was valued at approximately USD 2.14 Billion in 2025 and is expected to grow at a CAGR of approximately 8.65% through 2035.

Demand from the U.S. market for medical devices for regulatory affairs services stems from thousands of FDA submissions annually. 510(k), De Novo, PMA, and Breakthrough Device Designation are some examples of the many pathways to approval that require specialist knowledge and regulatory compliance planning. Most companies prefer outsourcing their FDA application processes through a regulatory consultant. In addition, the rising number of software-based medical devices and artificial intelligence (AI) applications within the field creates a need for FDA submission and regulatory services.

In 2025, Freyr Solutions upgraded their RegAI platform with features like AI-enabled regulatory intelligence, impact assessment automation, and document creation automation. This platform made the task of preparing documents for regulatory submission much faster, by about 40%. It also allowed fast analysis of any changes in the regulatory landscape. In addition to that, their automatic monitoring feature made it easy for manufacturers to find out which products or technical files were impacted.

Medical Device Regulatory Affairs Market Segmentation Analysis

-

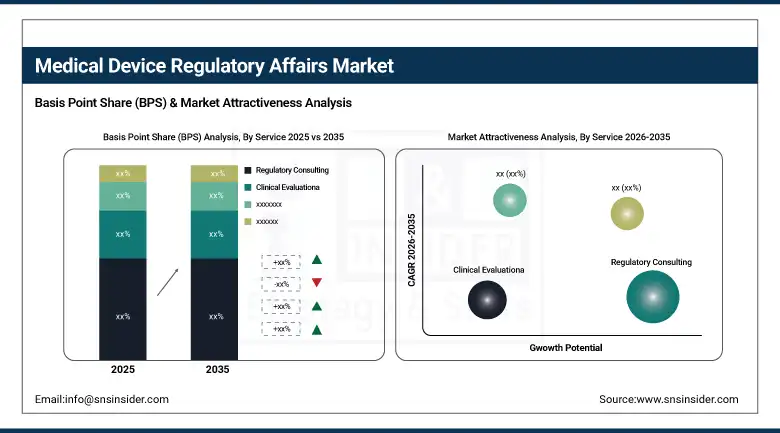

By Service, the regulatory consulting segment dominated the market in 2025, while regulatory submissions & approvals is the fastest growing service with strong above-average CAGR.

-

By Device Class, the Class II devices segment dominated the market in 2025 due to the volume of moderate-risk device filings, while Class III devices generate the highest per-device regulatory service value.

-

By Service Provider, the outsourced segment dominated the market in 2025, while in-house is the fastest growing segment.

-

By End User, the medical device manufacturers segment dominated the market with the largest share in 2025, while contract research organizations are growing as integrated regulatory and clinical service providers.

By Service, regulatory consulting dominates, regulatory submissions grow fastest

Regulatory consulting generated the dominant service revenue in 2025. The consulting segment's commercial leadership reflects the high value of expert regulatory strategy advice whose impact on development programme timelines, approval probability, and market access speed has direct financial consequence for device manufacturers whose product revenue generation depends on efficient regulatory navigation. Each successful major device approval typically involves regulatory consulting fees across the clinical strategy, submission preparation, and agency interaction phases whose cumulative value substantially exceeds the direct submission filing costs.

Regulatory submissions and approvals services are growing fastest as the volume of global regulatory filings increases with expanding international market access ambitions, new device development activity, and regulatory renewal requirements that create ongoing submission demand beyond the initial market access event.

By Service Provider, outsourced dominates; in-house grows fastest

Outsourced regulatory affairs services dominate the market as medical device manufacturers increasingly rely on specialized consulting firms for regulatory submissions, compliance management, clinical evaluation, and post-market surveillance activities. External providers offer broad expertise across multiple jurisdictions, including FDA, EU MDR, and other international frameworks. Their cost efficiency, scalability, and ability to manage complex regulatory requirements make outsourcing the preferred model for many manufacturers.

The most rapidly growing category is that of internal regulatory affairs departments due to the fact that larger companies manufacturing medical devices are enhancing their compliance capacity internally. The complexity of regulations, the increasing demands on post-market activities, as well as the requirement for constant control of products being offered internationally are among the factors that have encouraged companies to invest in regulation.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Medical Device Regulatory Affairs Market Insights

North America dominated the global medical device regulatory affairs market in 2025, holding the largest regional share. The United States accounts for approximately 82.47% of regional revenue through the scale of its medical device industry's FDA submission activity, the commercial presence of leading regulatory affairs service firms, and the premium pricing that FDA regulatory strategy expertise commands relative to equivalent services in other jurisdictions. Canada contributes supplementary demand through its Health Canada medical device regulatory framework whose requirements create parallel compliance investment for manufacturers seeking Canadian market access alongside U.S. FDA approval.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Medical Device Regulatory Affairs Market Insights

Europe held a significant share of global medical device regulatory affairs revenues in 2025. The EU MDR transition, whose full implementation deadline passed in December 2024 for legacy devices requiring MDR certification, created several years of concentrated regulatory affairs service demand whose backlog continues to generate consulting and submission service revenue as manufacturers work through technical file updates, clinical evaluation reports, and notified body certification processes. Germany, France, the United Kingdom, Switzerland, and the Netherlands are the leading national markets, each hosting significant medical device manufacturing sectors and established regulatory affairs consultancy firms whose EU regulatory expertise serves both domestic and international client manufacturers seeking European market access.

Asia Pacific Medical Device Regulatory Affairs Market Insights

Asia Pacific is the fastest-growing regional medical device regulatory affairs market, driven by the rapid expansion of medical device markets across China, India, Japan, South Korea, and Southeast Asia, the progressive development of local regulatory frameworks, and the growing ambitions of Asian device manufacturers to access international regulated markets requiring sophisticated regulatory affairs capability. China accounts for approximately 38.47% of Asia Pacific revenues through its large domestic device manufacturing sector's NMPA regulatory submissions and its international market access aspirations. India's expanding medical device regulatory framework under the CDSCO and its growing device manufacturing sector are creating growing domestic regulatory affairs market demand.

MEA & Latin America Medical Device Regulatory Affairs Market Insights

Middle East and Latin America are growing medical device regulatory affairs markets where increasing local device manufacturing activity, regulatory framework development, and the extension of international manufacturers' market access programmes into emerging markets are creating expanding commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its MOHAP regulatory framework for medical devices and its position as a regional distribution hub whose market access requirements create regulatory filing demand for international manufacturers.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through ANVISA's comprehensive medical device regulatory framework, whose CE mark recognition provisions and local technical file requirements create substantial regulatory affairs service demand from both domestic and international manufacturers.

Growth Drivers: Escalating global regulatory framework complexity are creating sustained structural demand growth for specialist regulatory affairs services.

The medical device regulatory affairs market is driven by the combination of regulatory framework intensification and device innovation acceleration. The EU MDR's elevated clinical evidence requirements, post-market obligations, and UDI implementation have more than doubled compliance investment for EU market access, a structural market expansion event independent of new product development because it applies to the entire installed base. Novel device categories including AI-enabled medical software, implantable digital health devices, and advanced combination products simultaneously create regulatory challenges requiring specialist expertise that established frameworks have not yet fully codified.

Restraints: Notified body capacity shortages create compliance programme bottlenecks that constrain medical device manufacturers' market access timelines.

The EU MDR transition created a severe and well-documented notified body capacity crisis as the increased clinical evidence and technical documentation requirements of the new regulation substantially increased the workload per certification audit while the number of designated notified bodies declined from over 50 under MDD to approximately 20 designated under MDR by early 2025. This capacity constraint created certification queue waiting times of 18 to 36 months for many device categories, forcing manufacturers to extend regulatory compliance programme timelines and creating revenue delays whose cost is borne by both the affected manufacturers and the healthcare systems whose patients await access to improved device technologies.

FDA 510(k) review times have similarly extended as the volume of AI-enabled device submissions requiring novel review approaches has increased faster than CDRH's reviewer specialization capacity has grown.

Opportunities: Digital regulatory submission platforms and AI-powered regulatory intelligence represent improvements for the medical device regulatory affairs service market.

AI-powered regulatory affairs platforms whose capabilities include automated regulatory guidance monitoring, intelligent technical document drafting, and cross-jurisdiction regulatory requirement mapping are beginning to transform the productivity economics of regulatory affairs service delivery. Each hour of regulatory specialist time that AI-assisted platforms save in document preparation, regulatory change monitoring, and submission compilation translates directly into either cost reduction for device manufacturers or enhanced margin for regulatory affairs service firms.

The competitive differentiation advantage of AI-enhanced regulatory affairs services whose faster, more comprehensive, and more accurate deliverables command premium pricing relative to purely manual equivalents is motivating substantial technology investment by leading regulatory affairs firms whose AI adoption creates platform advantages that sustain quality differentiation against lower-cost competitors.

Recent Developments:

-

2025: ICON PLC expanded its medical device regulatory affairs practice through acquisition of an EU MDR specialist consultancy, strengthening its clinical evaluation and notified body submission capability.

-

2025: Freyr Solutions launched its RegAI platform enhancement with AI-powered regulatory change impact assessment and intelligent document drafting assistance.

-

2024: Emergo by UL expanded its Asia Pacific medical device regulatory affairs services through new office openings in India and Southeast Asia, positioning to serve the growing regional demand for multi-jurisdiction regulatory strategy and submission services.

Medical Device Regulatory Affairs Market Key Players are:

-

Parexel International Corporation

-

Emergo by UL

-

Medpace Holdings Inc.

-

Intertek Group PLC

-

SGS SA

-

BSI Group

-

TUV SUD AG

-

Halloran Consulting Group

-

Proxima Clinical Research

-

Phlexglobal Ltd. (Crisp)

-

Regulatory Compliance Associates

-

GMED

-

NAMSA

-

WuXi AppTec Co. Ltd.

-

ProPharma Group

-

Cato Research Ltd.

-

DDReg Pharma

Medical Device Regulatory Affairs Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.43 Billion |

| Market Size by 2035 | USD 15.94 Billion |

| CAGR | CAGR of 7.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service (Regulatory Consulting, Regulatory Submissions & Approvals, Clinical Evaluation, Post-Market Surveillance, Quality Management, Others) • By Device Class (Class I, Class II, Class III) • By Service Provider (In-house, Outsourced) • By End User (Medical Device Manufacturers, Contract Research Organizations, Government & Regulatory Bodies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ICON PLC, IQVIA Holdings Inc., Parexel International Corporation, Freyr Solutions, Emergo by UL, Medpace Holdings Inc., Intertek Group PLC, SGS SA, BSI Group, TUV SUD AG, Halloran Consulting Group, Proxima Clinical Research, Phlexglobal Ltd. (Crisp), Regulatory Compliance Associates, GMED, NAMSA, WuXi AppTec Co. Ltd., ProPharma Group, Cato Research Ltd., DDReg Pharma |

Frequently Asked Questions

The Medical Device Regulatory Affairs Market is expected to grow at a CAGR of 7.93% from 2026 to 2035.

The Medical Device Regulatory Affairs Market was valued at USD 7.43 Billion in 2025.

The primary growth factors are the global tightening of medical device regulatory frameworks requiring greater clinical evidence and post-market surveillance investment.

The regulatory consulting segment dominated the Medical Device Regulatory Affairs Market with the largest share in 2025.

North America dominated the Medical Device Regulatory Affairs Market in 2025.

Get in Touch