Cell and Gene Therapy CDMO Market Report Scope & Overview:

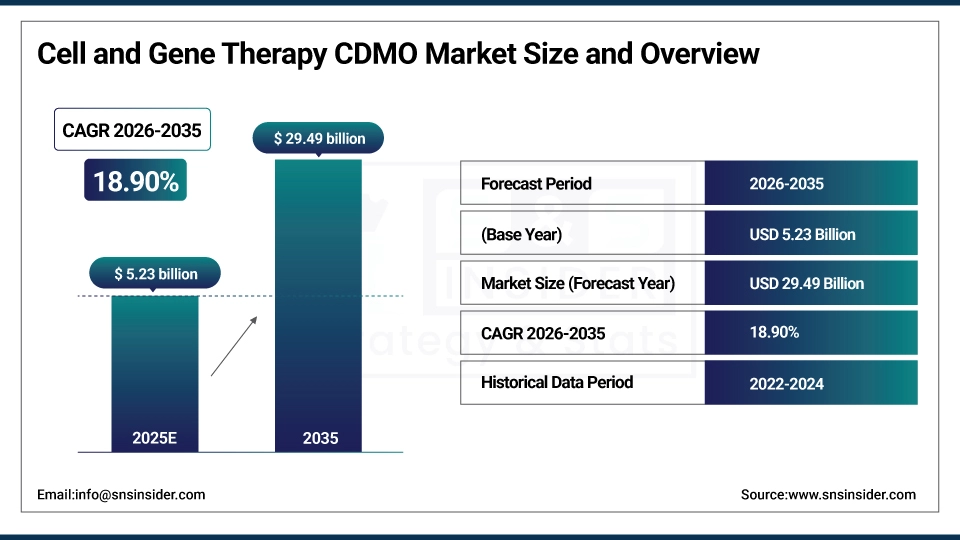

The Cell and Gene Therapy CDMO Market was estimated at USD 5.23 billion in 2025 and is expected to reach USD 29.49 billion by 2035 and grow at a CAGR of 18.90% over the forecast period of 2026-2035.

The Cell and Gene Therapy CDMO market is rapidly growing due to the increasing number of advanced therapies in the pipelines for oncology, rare diseases and genetic disorders. Rising manufacturing complexity, capital intensive nature and stringent regulatory requirements are prompting biopharm manufacturers to adopt development and production outsourcing. Companies include detailed profiles of leading and emerging Contract and Development Manufacturing Organisations (CDMOs) with capacity across process development, viral vectors, cells and commercial manufacture. Continuing to increase capacity, furthering technology, and the support from regulators are all continuing to reinforce the position of CDMOs in speeding products into clinical development and gaining commercial market share.

Market Size and Forecast

-

Market Size in 2025: USD 5.23 Billion

-

Market Size by 2035: USD 29.49 Billion

-

CAGR: 18.90%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Cell and Gene Therapy CDMO Market - Request Free Sample Report

Key Trends in the Cell and Gene Therapy CDMO Market

-

Viral vector manufacturing capacity is expanding rapidly to support the growing volume of clinical and commercial gene therapy programs.

-

Biopharmaceutical companies are increasingly opting for end-to-end CDMO partnerships to streamline development and reduce time to market.

-

Automation and scalable manufacturing platforms are being adopted to improve efficiency, consistency, and cost control in cell therapy production.

-

Significant investments are being made in global CGT manufacturing infrastructure, particularly across North America and Asia-Pacific.

-

Enhanced regulatory scrutiny is driving stronger emphasis on GMP compliance, advanced analytics, and quality-by-design approaches.

U.S. Cell and Gene Therapy CDMO Market Outlook:

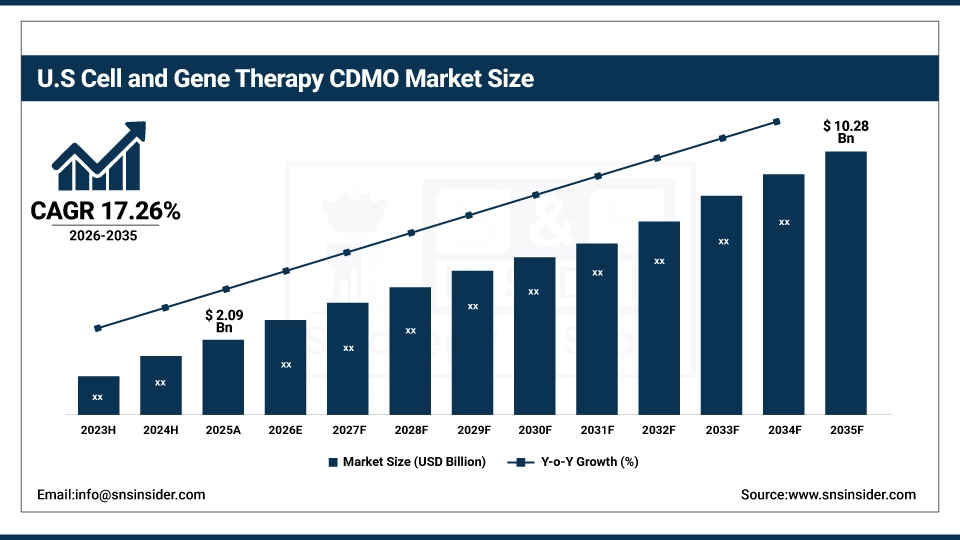

The U.S. Cell and Gene Therapy CDMO Market is projected to grow from USD 2.09 Billion in 2025 to USD 10.28 Billion by 2035, at a CAGR of 17.26%. Growth is driven by expanding cell and gene therapy pipelines, strong FDA regulatory support, increasing outsourcing by biopharma companies, rising viral vector demand, and continuous investments in advanced manufacturing infrastructure.

Cell and Gene Therapy CDMO Market Growth Drivers:

-

Increased Cell & Gene Therapy Pipeline / Outsourced Demand

Growing number of clinical and commercial cell and gene therapy programs for oncology, rare diseases & genetic disorders drive the market. It’s all too clear to biopharma manufacturers where they need a CDMO, however: high manufacturing complexity, investment in capital-intensive facilities and strict regulatory requirements are driving companies to outsource both development and production to specialty CDMOs. Regulatory motivations such as the FDA RMAT, and accelerated approval pathways also facilitate market growth for faster clinical translation and commercialization.

Cell and Gene Therapy CDMO Market Restraints:

-

High cost of production, limited capacity and technical hurdles

Car and gene therapy manufacturing are expensive with respect to GMP facilities, labor, viral vector production, and quality control. A lack of global capacity in manufacturing large scale viral vectors, long lead times and issues with the scalability and reproducibility of this manufacturing process are constraining rapid market growth. Furthermore, ever-changing regulations and complicated process of technology transfer may extend project schedules.

Cell and Gene Therapy CDMO Market Opportunities:

-

Progress in Manufacturing Methods and Capacity Expansion at the Worldwide Level

Advancements in technology such as automation, closed-systems manufacturing, single-use bioreactors and smart analytics is contributing to tremendous opportunities for growth. Growing investments in the construction of full-scale CGT production facilities, mainly in North America and Asia-Pacific is overcoming capacity constraints. Strategic alliances between CDMOs, biotech companies and academic organizations as well as increasing demand for commercial-scale manufacturing will help to drive growth prospects in the long run.

Cell and Gene Therapy CDMO Market Segment Analysis:

-

By Therapy Type: In 2025, Cell Therapy dominated with 49% share; Gene Therapy fastest growing segment during 2026-2035

-

By Service Type: In 2025, Manufacturing dominated with 57% share; Process & Analytical Development fastest growing segment during 2026-2035

-

By Vector Type: In 2025, Viral Vectors dominated with 69% share; Non-Viral Vectors fastest growing segment during 2026-2035

-

By End User: In 2025, Biopharmaceutical Companies dominated with 61% share; Startups fastest growing segment during 2026-2035

By Therapy Type: Cell Therapy Dominates, Gene Therapy Fastest-Growing

Cell therapy dominates the therapy type segment due to the high volume of clinical-stage and commercial programs, particularly CAR-T, TCR, and stem-cell-based therapies. The multistep, complex manufacturing processes of these therapies have led to heavy dependence on CDMO support, as is reflected by the requirement for state-of-the-art facilities as well as GMP compliance and rigorous quality systems. The requirement for scalable autologous and allogeneic manufacturing adds to the dominance of cell therapy in outsourced development and production.

Gene therapy is the fastest growing modality propelled by a vast growing pipeline for AAV and lentiviral products for rare genetic, neurological, and inherited metabolic disorders. Expanding number of regulatory approvals, better vector design and access to investment for large-scale viral vector manufacturing are driving the demand for outsourcing of gene therapy CDMO services.

By Service Type: Manufacturing Dominates, Process & Analytical Development Fastest-Growing

Manufacturing, including cell processing and vector production, dominates the service type segment due to its capital-intensive nature, high technical complexity, and strict regulatory requirements. Biopharma companies are moving towards outsourcing of GMP manufacturing to CDMOs from in-house due to the following reasons - avoid significant initial capital investments, optimize capacity utilization and consistently high product quality at clinical and commercial scales.

Process and analytical development is the largest and fastest growing service segment owing to a growing early-stage CGT pipeline as well as requirement of process that are scalable, optimized and reproducible. The need for thorough robust methods, comparison studies and quality by design is also growing as sponsors look to de-risk clinical development and speed up regulatory approvals.

By Vector Type: Viral Vectors Dominate, Non-Viral Vectors Fastest-Growing

Viral vectors dominate the vector type segment due to their high transduction efficiency, established clinical performance, and broad regulatory acceptance. AAV and lentiviral vectors are common to both in vivo gene therapies and ex vivo gene-modified cell therapies, so the need for specialized CDMO expertise and extensive vector production capacity continues unabated.

Non-viral vectors are the fastest growing sector, driven by developments in lipid nanoparticles, plasmid DNA and gene-editing delivery technologies. Reduced immunogenicity, better safety profiles and simpler manufacturing are driving uptake, especially in next-generation gene therapies and in the repeat dosing space.

By End User: Biopharmaceutical Companies Dominate, Startups Fastest-Growing

The end user segment of the global CGT CDMO market is dominated by biopharmaceutical companies who have large number of CGT pipeline, huge financial resources and dependence on CDMOs for multi-program development and commercial manufacturing. Strategic outsourcing provides these businesses the opportunity to concentrate on clinical development, relying on CDMOs for regulatory strategy, scale-up and quality oversight.

Startups represent the fastest-growing end-user segment as virtual biotech models, increased venture funding, and academic spin-outs continue to expand the CGT ecosystem. Limited in-house manufacturing capabilities and the need for rapid clinical progression are driving strong outsourcing demand among early-stage and emerging companies.

Regional Insights

North America Cell and Gene Therapy CDMO Market Insights:

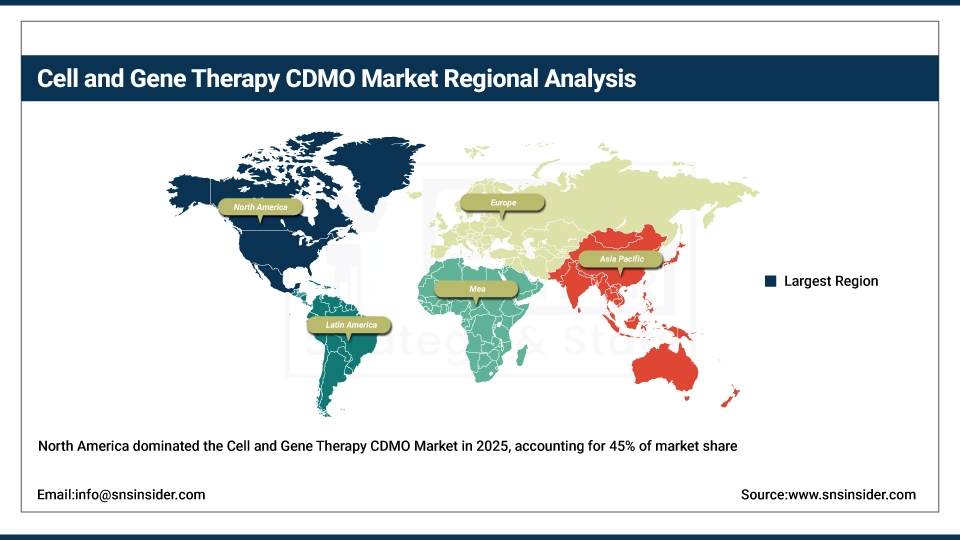

North America dominates the global Cell and Gene Therapy CDMO market, accounting for approximately 45% of total market revenue. This leadership is supported by a high density of biotech and pharmaceutical companies and a large, advanced cell and gene therapy clinical development pipeline, along with strong regulatory support including from the FDA. Long-standing CDMO manufacturing capabilities, large investments in viral vector capacity and early adoption of cutting-edge manufacturing technologies further support the region’s leadership position and continued expansion.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cell and Gene Therapy CDMO Market Insights:

Europe is a mature and growing Cell and Gene Therapy CDMO market with a strong foundation in academic research, increasing number of biotech spin-outs. The harmonisation of regulations across the region, growing cross-border cooperation, and investment in advanced therapy manufacturing are all positive for the sector. Growth in virial vector manufacturing capacity and stronger alliances between CDMOs and pharma are strengthening Europe’s role as a source of support for cell- and gene therapy clinical development and commercialisation.

Asia-Pacific Cell and Gene Therapy CDMO Market Insights:

Asia-Pacific is the fastest-growing region in the Cell and Gene Therapy CDMO market, registering a CAGR of 23.05% during 2026-2035. Rapid developments are spurred on by increasing biomanufacturing capacity, the cost-effectiveness of production and growing government support for advanced therapeutics. Mounting number of clinical trials, surging biotech ecosystems in China, Japan and South Korea, and partnerships with global pharmaceutical companies are fueling regional demand for outsourced cell and gene therapy development and manufacturing services.

Latin America Cell and Gene Therapy CDMO Market Insights:

Latin America represents an expanding cell and gene therapy CDMO services marketplace due to increasing medical infrastructure and trial research. Growing partnership with international drug manufacturers and slow-paced regulatory development allow for early-stage development and manufacturing. Although adoption is less than that in developed regions, growing investments in biotechnology and greater availability of advanced therapies are projected to drive consistent regional growth.

Middle East & Africa Cell and Gene Therapy CDMO Market Insights:

Middle East & Africa is an emerging market for cell and gene therapy CDMO services owing to growing healthcare investments in the region over time, and a slow buildup of biotechnology infrastructure. Momentum is being driven by increasing advanced therapeutic interest, expanding clinical research and global CDMO collaborations that help establish its initial market presence. But constrained by low local manufacturing capacity and changing regulations, the pace of adoption remains slower in most countries.

Competitive Landscape:

Lonza Group, headquartered in Basel, Switzerland, is a global leader in the cell and gene therapy CDMO market, providing end-to-end solutions across process development, viral vector manufacturing, cell therapy production, and commercial-scale supply. The company supports a broad range of advanced modalities, including autologous and allogeneic cell therapies, AAV and lentiviral vectors, and gene-modified cell therapies. Lonza leverages advanced manufacturing platforms, integrated analytical capabilities, and extensive regulatory expertise to help biopharmaceutical companies accelerate clinical development and commercialization. Its strong focus on scalable manufacturing, quality assurance, and long-term partnerships positions Lonza as a key enabler of next-generation cell and gene therapies.

-

In February 2025: Lonza expanded its cell and gene therapy manufacturing capacity in the United States to support increasing demand for late-stage and commercial CGT programs, strengthening its global CDMO footprint.

Catalent, Inc., headquartered in Somerset, New Jersey, USA, is a prominent cell and gene therapy CDMO, offering comprehensive services spanning viral vector development, cell therapy manufacturing, formulation, fill-finish, and clinical-to-commercial scale support. The company specializes in AAV, lentiviral, and retroviral vector platforms and provides integrated development and manufacturing solutions tailored to emerging biotech and large pharmaceutical clients. Catalent’s emphasis on flexible manufacturing infrastructure, regulatory compliance, and advanced delivery technologies enables efficient scale-up and accelerated time-to-market for complex CGT products, positioning it as a strategic partner in the advanced therapeutics ecosystem.

-

In January 2025: Catalent strengthened its viral vector manufacturing capabilities through facility upgrades and technology investments aimed at supporting high-volume gene therapy programs.

Cell and Gene Therapy CDMO Market Key Players

-

Lonza Group

-

Catalent, Inc.

-

Thermo Fisher Scientific

-

WuXi Advanced Therapies

-

Samsung Biologics

-

Charles River Laboratories

-

AGC Biologics

-

Oxford Biomedica

-

Fujifilm Diosynth Biotechnologies

-

Viralgen Vector Core

-

Kite Pharma Manufacturing

-

Resilience

-

Bayer Cell Therapy Manufacturing

-

Yposkesi

-

KBI Biopharma

-

Brammer Bio

-

Cobra Biologics

-

Cell and Gene Therapy Catapult Manufacturing Innovation Centre

-

Porton Advanced Solutions

-

Novasep

Cell and Gene Therapy CDMO Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.23 Billion |

| Market Size by 2035 | USD 29.49 Billion |

| CAGR | CAGR of 18.90% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Therapy Type: (Cell Therapy, Gene Therapy, Gene-Modified Cell Therapy) • By Service Type: (Process & Analytical Development, Manufacturing, Fill & Finish Services) • By Vector Type: (Viral Vectors, Non-Viral Vectors, Cell-Based Delivery Systems) • By End User: (Biopharmaceutical Companies, Biotechnology Startups, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Lonza Group, Catalent, Thermo Fisher Scientific, WuXi Advanced Therapies, Samsung Biologics, Charles River Laboratories, AGC Biologics, Oxford Biomedica, Fujifilm Diosynth Biotechnologies, Viralgen Vector Core, Kite Pharma Manufacturing, National Resilience, Bayer Cell Therapy Manufacturing, Yposkesi (SK pharmteco), KBI Biopharma, Brammer Bio, Cobra Biologics, Cell and Gene Therapy Catapult Manufacturing Innovation Centre, Porton Advanced Solutions, Novasep |

Frequently Asked Questions

The Cell and Gene Therapy CDMO Market is expected to grow at a CAGR of 18.90% during 2026–2035.

The market was valued at USD 5.23 Billion in 2025 and is projected to reach USD 29.49 Billion by 2035.

The key drivers of the Cell and Gene Therapy CDMO Market include expanding cell and gene therapy pipelines, rising outsourcing due to manufacturing complexity, regulatory support, growing viral vector demand, and increasing investments in advanced biomanufacturing infrastructure.

The Viral Vectors segment dominated during the projected period.

North America dominated the Cell and Gene Therapy CDMO Market in 2025.

Get in Touch