Microcrystalline Cellulose Market Report Scope & Overview:

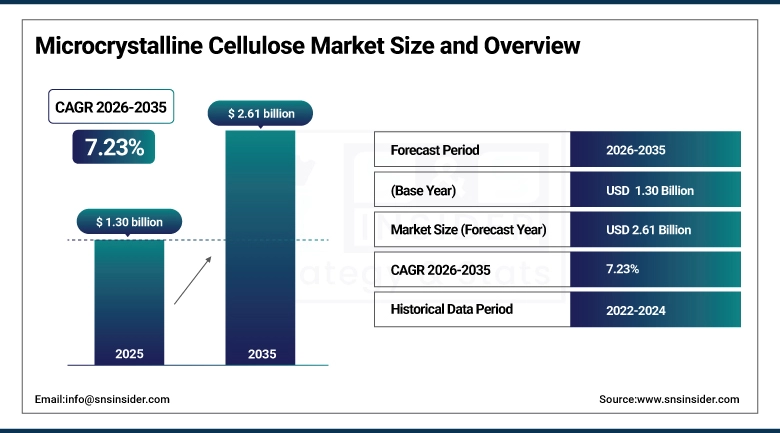

The Microcrystalline Cellulose Market size was valued at USD 1.30 billion in 2025 and is expected to reach USD 2.61 billion by 2035, growing at a CAGR of 7.23% over the forecast period of 2026-2035.

The global microcrystalline cellulose market trend is a growing demand for natural excipient materials such as pharmaceutical-grade binders and disintegrants, food-grade fat replacers and anti-caking agents, and personal care emulsion stabilizers as the growth of the market is driven by increasing pharmaceutical solid dosage form production, expanding clean-label food and beverage formulation requirements, and consumer preference for plant-derived functional ingredients. This trend is also driven by a growing adoption of wood pulp and non-wood cellulose processing technologies and the growing focus on sustainable raw material sourcing in specialty chemical manufacturing as formulators become more focused on replacing synthetic excipients with naturally derived alternatives and are more willing to invest in advanced cellulose hydrolysis and co-processing capabilities, resulting in growth in the domestic and international market for wood-based and non-wood-based microcrystalline cellulose solutions.

For instance, in April 2024, growing pharmaceutical manufacturer preference for natural-origin excipients drove a 19% increase in microcrystalline cellulose procurement contracts for tablet and capsule production facilities across North America and Europe, boosting wood-based cellulose supplier revenues and clean-label excipient adoption at scale.

Microcrystalline Cellulose Market Size and Forecast:

-

Market Size in 2025: USD 1.30 billion

-

Market Size by 2035: USD 2.61 billion

-

CAGR: 7.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Microcrystalline Cellulose Market - Request Free Sample Report

Microcrystalline Cellulose Market Trends

-

Microcrystalline cellulose is being adopted across pharmaceutical solid dosage manufacturing because formulators demand reliable binder, disintegrant, and filler performance in tablet compression and capsule filling operations.

-

Increasing use of co-processed microcrystalline cellulose grades combining cellulose with carboxymethylcellulose sodium, silicon dioxide, or calcium carbonate to improve flow properties and compressibility for high-speed tablet production lines.

-

The development of spray-dried and colloidal microcrystalline cellulose grades for suspension stabilization, emulsion structuring, and fat replacement applications in low-calorie food and personal care product formulations.

-

Growing demand for non-wood-based microcrystalline cellulose derived from agricultural residues including sugarcane bagasse, cotton linters, and rice husks as manufacturers seek cost-competitive and regionally available cellulose raw material alternatives.

-

Increased focus on pharmaceutical excipient regulatory compliance, including USP/NF, Ph. Eur., and JP monograph adherence, to support drug master file submissions and global market access for tablet and capsule product registrations.

-

Collaboration between cellulose raw material suppliers, pharmaceutical excipient manufacturers, and food ingredient companies to develop application-specific microcrystalline cellulose grades with optimized particle size, moisture content, and bulk density profiles.

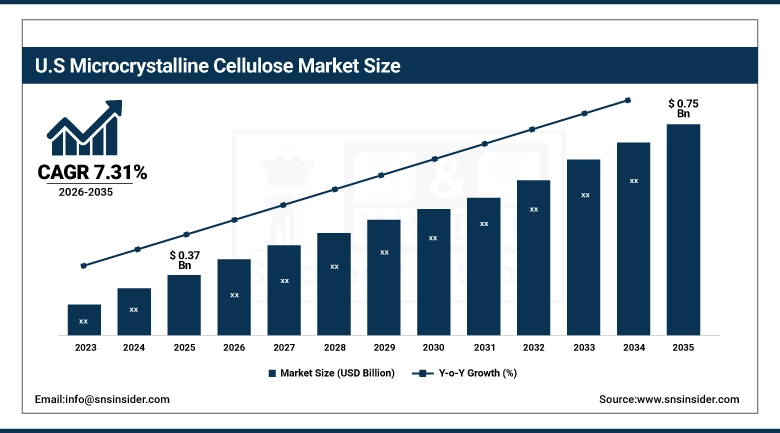

The U.S. Microcrystalline Cellulose Market was valued at USD 0.37 billion in 2025 and is expected to reach USD 0.75 billion by 2035, growing at a CAGR of 7.31% from 2026-2035.

The United States represents the largest market for microcrystalline cellulose, primarily driven by the well-established pharmaceutical solid dosage manufacturing base, high per-capita dietary supplement consumption, and well-developed food ingredient processing infrastructure. Strong FDA excipient compliance frameworks, moderately high levels of generic drug production activity, and increased formulator spending on natural and plant-derived ingredient sourcing help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of wood-based and co-processed microcrystalline cellulose grades across pharmaceutical, food, and personal care end-use applications.

Microcrystalline Cellulose Market Growth Drivers:

-

Expanding Pharmaceutical Solid Dosage Form Production and Generic Drug Manufacturing is Driving the Microcrystalline Cellulose Market Growth

Expanding pharmaceutical solid dosage form production and generic drug manufacturing take the center stage as a growth driver for the microcrystalline cellulose market share, and are driven by the rising global volume of tablet and capsule production, patent expiry-driven generic drug launch pipelines, and pharmaceutical manufacturer preference for USP/NF-grade excipients with well-established regulatory acceptance across major drug approval jurisdictions. These solutions for tablet compression performance and drug product stability are driving the base of the market, the penetration of pharmaceutical-grade and food-grade cellulose excipient demand, and adding to the overall market share globally.

Microcrystalline Cellulose Market Restraints:

-

Raw Material Price Volatility and Wood Pulp Supply Chain Disruptions are Hampering the Microcrystalline Cellulose Market Growth

Raw material price volatility and wood pulp supply chain disruptions also restrict the microcrystalline cellulose market growth, as a large number of cellulose manufacturers who depend on dissolving-grade wood pulp sourcing remain exposed to forest resource availability constraints or face difficulties maintaining consistent raw material pricing and quality specifications across production batches. This might lead to margin compression for cellulose processors, formulation cost increases for pharmaceutical and food manufacturers, and reduced competitive pricing for finished microcrystalline cellulose grades. As a result, end-user switching behavior toward synthetic excipient alternatives may increase, and market growth is stunted in regions where domestic wood pulp processing infrastructure and non-wood cellulose sourcing networks remain underdeveloped.

Microcrystalline Cellulose Market Opportunities:

-

Growing Clean-Label Food Formulation and Non-Wood Cellulose Sourcing Drive Future Growth Opportunities for the Microcrystalline Cellulose Market

The opportunity in the growing clean-label food formulation and non-wood cellulose sourcing in the microcrystalline cellulose market is in the form of agricultural residue-derived cellulose grades, plant-based fat replacer ingredient systems, and natural anti-caking and texturizing solutions for processed food applications. These solutions provide for clean-label ingredient transparency for food manufacturers, reduced reliance on wood pulp raw material supply chains, and improved cost competitiveness for cellulose producers operating in agricultural residue-rich developing regions. Through enhanced food ingredient functionality, sustainable raw material utilization, and formulation compatibility, particularly in areas with growing demand for low-fat and fiber-enriched food products, these developments may improve product label appeal, decrease synthetic additive dependency, and expand the market.

Microcrystalline Cellulose Market Segment Analysis

-

By Source, wood-based held the largest share of around 72.34% in 2025, and the non-wood-based segment is expected to register the highest growth with a CAGR of 8.46%.

-

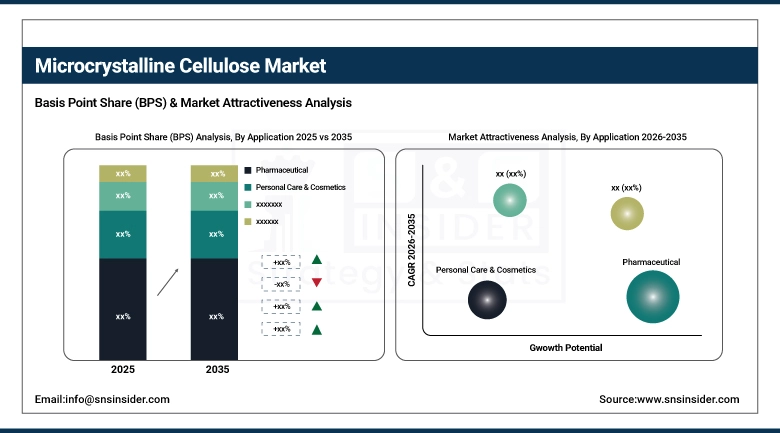

By Application, pharmaceutical accounted for the leading share of nearly 54.67% in 2025, and is expected to register the highest growth with a CAGR of 7.58%.

By Application, Pharmaceutical Leads, and Registers Fastest Growth

The pharmaceutical segment accounted for the largest share of the microcrystalline cellulose market with about 54.67%, owing to the near-universal use of microcrystalline cellulose as a binder, disintegrant, and filler in solid oral dosage form manufacturing, established USP/NF and Ph. Eur. compendial monograph acceptance, and strong global generic drug production volume growth driving excipient demand across tablet compression and direct compression formulation workflows. Reasons driving the pharmaceutical segment include increasing oral solid dosage form production activity in India, China, and the U.S., and growing dietary supplement tablet and capsule manufacturing volumes. In addition, it is slated to grow at the fastest rate with a CAGR of around 7.58% throughout the forecast period of 2026–2035, as pharmaceutical manufacturers, contract development and manufacturing organizations (CDMOs), and nutraceutical producers seek consistent-grade microcrystalline cellulose excipient supply, value-based excipient sourcing models, and co-processing capabilities for improved tablet flow and compressibility performance. Increased focus on high-speed tablet press compatibility and moisture-sensitive drug formulation protection contribute to adoption, while expanding generic drug approvals and biosimilar solid dosage development drive continued excipient investment.

By Source, Wood-Based Leads the Market, While Non-Wood-Based Registers Fastest Growth

The wood-based segment accounted for the highest revenue share of approximately 72.34% in 2025, owing to the well-established dissolving-grade wood pulp supply chains, consistent cellulose purity levels meeting USP/NF and Ph. Eur. pharmaceutical monograph specifications, and strong global manufacturer preference for wood-derived cellulose grades with proven regulatory acceptance across drug and food product registration frameworks. Emerging trends, including increasing investment in kraft pulp processing upgrades and expansion of wood cellulose production capacity in Scandinavia, North America, and Southeast Asia, are reinforcing wood-based segment dominance across near-term forecast periods. The non-wood-based segment is anticipated to achieve the highest CAGR of nearly 8.46% during the 2026–2035 period, driven by the increasing availability of agricultural residue feedstocks including cotton linters, sugarcane bagasse, and rice straw for cellulose extraction, growing manufacturer interest in supply chain diversification, and cost competitiveness of non-wood cellulose production in agricultural residue-abundant developing economies. Drivers include rising environmental pressure on wood pulp sourcing and the preference for regionally available raw material alternatives among Asian and Latin American cellulose producers.

Microcrystalline Cellulose Market Regional Highlights:

Asia Pacific Microcrystalline Cellulose Market Insights:

Asia Pacific is the fastest-growing region in the microcrystalline cellulose market with a CAGR of 8.62%, as the awareness about pharmaceutical-grade excipient quality standards, generic drug manufacturing volume growth, and food ingredient processing infrastructure modernization in India, China, and Southeast Asian economies is growing. Factors including India’s dominant generic pharmaceutical export production base, China’s large-scale food processing industry, and Japan’s advanced pharmaceutical formulation technology ecosystem are stimulating the market growth. Government-supported pharmaceutical manufacturing incentive programs and domestic cellulose production capacity expansion initiatives have been instrumental in improving microcrystalline cellulose supply availability, especially in high-volume solid dosage and processed food manufacturing corridors. Public investment in agricultural residue cellulose processing and chemical manufacturing park development also help in advancing regional cellulose production and market competitiveness.

North America Microcrystalline Cellulose Market Insights:

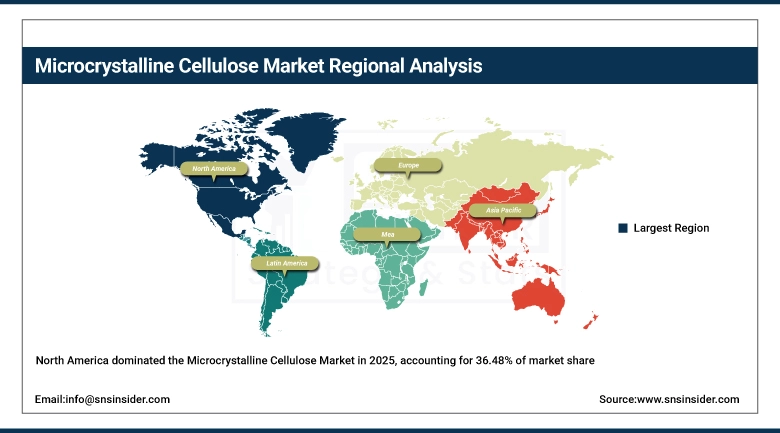

North America held the largest revenue share of over 36.48% in 2025 of the microcrystalline cellulose market due to an established pharmaceutical manufacturing base, stringent FDA excipient GMP compliance requirements, and increased formulator awareness regarding the functional performance advantages of pharmaceutical- and food-grade microcrystalline cellulose. Drivers include widespread solid oral dosage form production activity, an established dietary supplement manufacturing sector, growing clean-label food formulation demand, and greater acceptance of natural excipient and food ingredient alternatives stemming from consumer preference for plant-derived product compositions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Microcrystalline Cellulose Market Insights:

The microcrystalline cellulose market in Europe is the second-dominating region after North America on account of a well-developed pharmaceutical excipient manufacturing sector, stringent Ph. Eur. compendial standards for cellulose excipient quality, and increasing clean-label and natural food ingredient adoption initiatives across European food and beverage product development programs. Rising implementation of European Pharmacopoeia monograph compliance requirements, advanced pharmaceutical excipient GMP certification practices, favorable EU funding for sustainable biomass processing research, and cross-border food ingredient regulatory harmonization are also contributing to the sustained growth of the market in leading European pharmaceutical and food ingredient economies.

Latin America (LATAM) and Middle East & Africa (MEA) Microcrystalline Cellulose Market Insights:

In Latin America, and Middle East & Africa, the growing pharmaceutical manufacturing localization efforts and increase in food processing industry investment with expanding consumer goods production capacity support the microcrystalline cellulose market growth. The rising adoption of imported pharmaceutical-grade cellulose excipients and the growing availability of agricultural residue-derived non-wood cellulose feedstocks, along with regulatory modernization programs aligned with international pharmacopoeia standards, will aid excipient quality improvement and market accessibility. The increasing domestic pharmaceutical production activity and improving food ingredient processing infrastructure in these regions are continuing to encourage market growth.

Microcrystalline Cellulose Market Competitive Landscape:

DuPont de Nemours, Inc. (est. 1802) is a leading specialty materials and food ingredient company that focuses on cellulose-based excipient and functional ingredient solutions for pharmaceutical, food, and personal care manufacturing applications. It uses its Avicel® microcrystalline cellulose product portfolio and global distribution partnerships to produce application-specific cellulose grades, with a strong commitment to pharmaceutical regulatory compliance and continuous excipient innovation.

-

In October 2024, expanded its Avicel® co-processed microcrystalline cellulose product line with two new grades optimized for direct compression tablet manufacturing at high-speed production rates, aiming to improve tablet hardness uniformity and reduce capping defect rates across pharmaceutical and nutraceutical customer formulations.

Asahi Kasei Corporation (est. 1931) is a well-known global cellulose excipient manufacturer focused on pharmaceutical-grade microcrystalline cellulose, hydroxypropyl cellulose, and co-processed excipient systems for solid dosage form applications. It invests in cellulose processing technology upgrades and pharmaceutical regulatory documentation support with the hopes of revolutionizing excipient sourcing for formulators seeking consistent quality microcrystalline cellulose supply across Asia Pacific, European, and North American drug manufacturing markets.

-

In March 2025, launched the Ceolus™ KG series of high-functionality microcrystalline cellulose grades targeting moisture-sensitive drug formulations and high-dose tablet production, announcing expanded technical support services for pharmaceutical CDMO customers across India and Southeast Asia.

Mingtai Chemical Co., Ltd. (est. 1970) is a leading Taiwanese microcrystalline cellulose manufacturer in the fields of pharmaceutical excipient production, food-grade cellulose ingredient supply, and co-processed excipient system development. The company’s microcrystalline cellulose product portfolio focuses on USP/NF- and Ph. Eur.-compliant grades across a broad particle size and bulk density range, and features a strong commitment to pharmaceutical GMP manufacturing standards and continuous product line expansion to complement its growing export customer base across pharmaceutical and food processing markets in Asia, Europe, and North America.

-

In June 2024, introduced three new microcrystalline cellulose grades with enhanced flow and compressibility profiles for use in nutraceutical tablet and hard capsule filling applications, aiming to strengthen product competitiveness in the dietary supplement excipient segment and expand market presence in the U.S. and European natural health product manufacturing sectors.

Microcrystalline Cellulose Market Key Players:

-

DuPont de Nemours, Inc. (Nutrition & Biosciences)

-

Mingtai Chemical Co., Ltd.

-

JRS Pharma GmbH & Co. KG

-

Roquette Frères S.A.

-

Sigachi Industries Limited

-

Anhui Sunhere Pharmaceutical Excipients Co., Ltd.

-

Wei Ming Pharmaceutical Mfg. Co., Ltd.

-

Blanver Farmoquimica e Farmaceutica Ltda.

-

Avantor, Inc.

-

Merck KGaA (MilliporeSigma)

-

Biogrund GmbH

-

Accent Microcell Pvt. Ltd.

-

Prachin Chemical Pvt. Ltd.

-

Huzhou Zhanwang Pharmaceutical Co., Ltd.

-

Juku Orchem Private Limited

-

Dfe Pharma GmbH & Co. KG

-

Thorlakson Holdings Ltd. (Tembec)

-

Sappi Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.30 Billion |

| Market Size by 2035 | USD 2.61 Billion |

| CAGR | CAGR of 7.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Wood-based, and Non-wood-based) • By Application (Pharmaceutical, Personal Care & Cosmetics, Food & Beverages, Paints & Coatings, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | DuPont de Nemours, Inc. (Nutrition & Biosciences), Asahi Kasei Corporation, Mingtai Chemical Co., Ltd., JRS Pharma GmbH & Co. KG, Roquette Frères S.A., Sigachi Industries Limited, Anhui Sunhere Pharmaceutical Excipients Co., Ltd., Wei Ming Pharmaceutical Mfg. Co., Ltd., Blanver Farmoquimica e Farmaceutica Ltda., Avantor, Inc., Merck KGaA (MilliporeSigma), Celanese Corporation, Biogrund GmbH, Accent Microcell Pvt. Ltd., Prachin Chemical Pvt. Ltd., Huzhou Zhanwang Pharmaceutical Co., Ltd., Juku Orchem Private Limited, DFE Pharma GmbH & Co. KG, Thorlakson Holdings Ltd. (Tembec), and Sappi Limited. |

Frequently Asked Questions

Innovations like moisture-resistant, low-nitrite, and high-compressibility MCC grades are expanding its use in pharmaceuticals and clean-label food products.

Biodegradable and functional MCC variants are also enabling growth in eco-friendly cosmetics and nutraceutical applications.

DuPont, FMC Corporation, JRS Pharma, Roquette, DFE Pharma, Asahi Kasei Corporation, Avantor Inc., Mingtai Chemical Co., Ltd., Sigachi Industries, and Libraw Pharma.

North America currently dominates the Microcrystalline Cellulose market, while Asia Pacific is the fastest-growing region.

Growing adoption in processed and functional foods drives the market growth.

The Microcrystalline Cellulose Market was valued at USD 1.30 billion in 2025 and is expected to reach USD 2.61 billion by 2035, growing at a CAGR of 7.23%.

Get in Touch