Middle Office Outsourcing Market Report Scope & Overview:

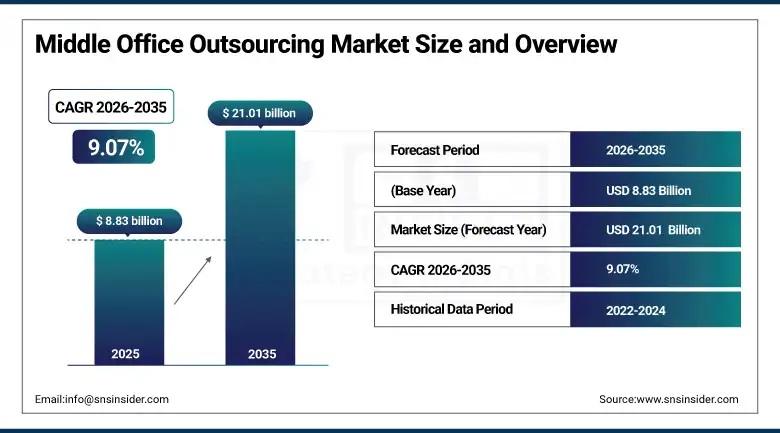

The Middle Office Outsourcing Market was valued at USD 8.83 Billion in 2025 and is expected to reach USD 21.01 Billion by 2035, growing at a CAGR of 9.07% from 2026–2035.

The global middle office outsourcing market occupies a strategically critical position in the evolution of financial services operations, as the world’s asset management, hedge fund, insurance, and pension fund industries progressively recognise that the post-trade processing, risk analytics, compliance reporting, and portfolio accounting functions that comprise the middle office represent both one of their largest operational cost centres and one of the areas where specialist third-party service providers with dedicated technology platforms, regulatory expertise, and economies of scale can deliver equivalent or superior capability at lower total cost than internal function management. Middle office outsourcing contracts reached 1,420 globally in 2025, a market milestone that reflects the structural shift in financial institution operating model philosophy from the vertical integration of all operational functions as a control preference to the selective outsourcing of non-differentiating operational functions as an efficiency and capability improvement strategy. The market’s growth is being driven by the extraordinary complexity growth of financial regulatory requirements, where firms operating across multiple asset classes and jurisdictions must simultaneously comply with EMIR, MiFID II, Dodd-Frank, Basel III, AIFMD, and SFDR reporting requirements whose combined compliance burden has exceeded the management capacity of in-house teams without the scale, technology platform investment, and regulatory intelligence infrastructure that specialist outsourcing providers maintain as a core service proposition. The rapid adoption of AI and automation tools across middle office operations, including machine learning-powered trade matching anomaly detection, automated reconciliation exception management, and natural language processing-based regulatory report generation, is simultaneously improving outsourcing service quality and reducing per-unit transaction processing costs in ways that make the value proposition of specialist outsourcing providers increasingly compelling relative to internal function management.

State Street’s 2025 integration of an end-to-end digital platform with expanded middle office capabilities for Charles River Investment Management Solution clients, providing cloud-based portfolio analytics, automated compliance monitoring, and real-time performance attribution for institutional asset management clients, represents the direction in which the market’s largest service providers are evolving their propositions: from process execution outsourcing toward technology-enabled insight generation that creates genuine analytical value beyond the cost arbitrage of operational function transfer.

Middle Office Outsourcing Market Size and Forecast

-

Market Size in 2026E: USD 9.63 Billion

-

Market Size by 2035: USD 21.01 Billion

-

CAGR: 9.07% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Middle Office Outsourcing Market - Request Free Sample Report

Middle Office Outsourcing Market Trends

-

Accelerating adoption of cloud-based middle office platforms by financial institutions whose legacy on-premise infrastructure is creating data management bottlenecks, system integration complexity, and scalability limitations that prevent the real-time analytics, regulatory reporting automation, and operational efficiency improvements that cloud-native outsourcing platforms can deliver through elastic compute resources, pre-built regulatory reporting engines, and API-based integration with front and back office systems.

-

Growing demand for integrated outsourcing solutions that combine middle office function delivery with technology platform licensing in a managed service wrapper, enabling financial firms to access the capabilities of sophisticated portfolio accounting, risk analytics, and compliance reporting platforms through a subscription service relationship rather than incurring the capital investment and ongoing maintenance costs of licensing and operating equivalent technology internally.

-

Rising complexity of cross-asset class and multi-jurisdictional portfolio management creating outsourcing demand from asset managers whose geographic expansion and product range diversification has outpaced the capability of internal operational teams and technology systems built for narrower mandate management, with specialist outsourcing providers whose multi-asset class processing infrastructure and global regulatory compliance expertise are specifically designed for the operational complexity that increasingly diversified investment portfolios generate.

-

Increasing focus on operational resilience and business continuity planning following the market volatility events and operational disruptions of recent years, driving financial institutions to reassess the concentration risk of internally managed critical operational functions and to value the redundancy, disaster recovery capability, and operational expertise depth that specialist outsourcing providers can deliver as inherent features of their multi-client service infrastructure rather than bespoke investments required for each individual client.

-

Growing regulatory scrutiny of outsourcing arrangements under frameworks including the EU’s Digital Operational Resilience Act and the UK FCA’s operational resilience standards, which require financial firms to demonstrate that outsourced critical functions maintain operational continuity standards equivalent to internal management, creating a compliance driver that simultaneously raises the bar for outsourcing provider capability and creates commercial opportunity for the most operationally robust and transparently governed service providers.

U.S. Middle Office Outsourcing Market Outlook

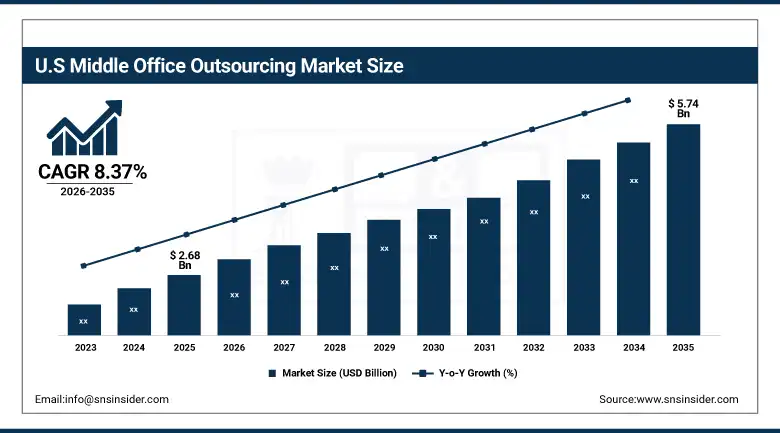

The U.S. Middle Office Outsourcing Market was valued at approximately USD 2.68 Billion in 2025 and is expected to reach approximately USD 5.74 Billion by 2035, growing at a CAGR of approximately 8.37%.

The United States middle office outsourcing market is driven by the world’s deepest and most commercially sophisticated asset management industry whose combined assets under management exceed USD 37 trillion and whose operational complexity, regulatory burden, and cost efficiency imperatives collectively create the strongest commercial motivation for middle office outsourcing adoption of any national market globally. The U.S. market’s distinctive characteristics include the concentration of the world’s largest and most technically demanding hedge fund community in the New York and Connecticut metropolitan area, whose operational model of running lean core investment teams supported by outsourced infrastructure services has established middle office outsourcing as a standard operating model assumption rather than an exceptional arrangement. State Street Global Services, BNY Mellon’s Asset Servicing division, Northern Trust, and Citco Group collectively serve the majority of the institutional asset management and hedge fund outsourcing market through comprehensive service offerings that combine portfolio accounting, performance attribution, risk analytics, and regulatory reporting in integrated platform propositions whose scale enables technology investment levels and regulatory expertise depth that individual asset management firms cannot efficiently replicate internally. The SEC’s ongoing enhancement of investment adviser reporting requirements, including expanded Form PF obligations for private fund advisers and the proposed amendments to rule 2a-5 for fund valuation, is creating incremental compliance burden that reinforces asset manager outsourcing decisions by adding to the regulatory complexity that specialist providers manage more efficiently than in-house teams.

Northern Trust’s 2025 launch of a partnership with Hazeltree for integrated treasury management within its middle office outsourcing service for asset management clients demonstrates the commercial direction of leading providers toward supplementary service capability expansion that deepens the value delivered to existing clients while creating new differentiation that attracts new client relationships seeking comprehensive operational partnership rather than selective function outsourcing.

Middle Office Outsourcing Market Segment Analysis

-

By Service Type, portfolio accounting & reporting led the middle office outsourcing market in 2025 as the foundational function whose accuracy, timeliness, and auditability are prerequisites for all other investment management activities; risk management is the fastest-growing service type driven by the growing complexity of multi-asset class and derivatives-inclusive portfolios whose risk analytics requirements exceed the capability of standard accounting systems.

-

By Deployment Type, on-premise deployment dominated with approximately 46.78% share in 2025 as large financial firms prioritise control, data security, and customisation for their existing infrastructure; cloud-based deployment is projected to expand at the fastest CAGR of approximately 11.34% as financial firms become more comfortable with cloud security, regulators provide clearer cloud adoption guidance, and cloud platform economics increasingly favour outsourced cloud delivery over internal data centre investment.

-

By Enterprise Size, large enterprises accounted for the highest market share of approximately 62.41% in 2025, reflecting their higher operational complexity and greater financial resources supporting comprehensive outsourcing engagement; small and medium enterprises are anticipated to record the fastest CAGR of approximately 10.86% as cloud-based outsourcing platforms make sophisticated middle office capability accessible at price points and engagement structures that fit SME operational budget constraints.

-

By End User, asset managers held the largest share of approximately 29.84% in 2025 driven by the diversity and complexity of their portfolio management, reporting, and compliance requirements across multiple asset classes and investor types; hedge funds are expected to grow at the fastest CAGR of approximately 10.43% during 2026–2035 as they leverage outsourcing to scale operations quickly while maintaining lean internal teams focused on investment strategy rather than operational infrastructure.

By Deployment Type, on-premise dominates, cloud-based grows fastest

On-premise deployment retained the dominant position with approximately 46.78% of the middle office outsourcing market in 2025, reflecting the large financial institutions’ historically entrenched preference for maintaining critical operational functions within their own data centre infrastructure where they retain direct control over data residency, system configuration, access management, and integration with proprietary front-office and back-office systems whose bespoke integration requirements have historically been more practically served by on-premise deployment than by standardised cloud platform alternatives. The on-premise deployment model’s commercial persistence reflects both the genuine operational advantages it provides in terms of data sovereignty assurance, customisation flexibility, and integration depth with legacy system infrastructure and the institutional risk aversion that makes technology architecture change in mission-critical financial operations subject to extended review cycles, regulatory pre-approval in some jurisdictions, and conservative implementation timelines that extend the existing model’s commercial life well beyond the point at which technology economics alone would favour transition to cloud alternatives.

Cloud-based deployment is the fastest-growing segment at a CAGR of approximately 11.34% through 2035, driven by the convergence of improving cloud security standards that address the regulatory concerns that previously slowed cloud adoption in financial services, regulators’ publication of clearer cloud adoption guidance including the European Banking Authority’s cloud outsourcing guidelines and the U.S.’ OCC’s cloud computing guidance that provide compliance frameworks enabling cloud adoption without regulatory uncertainty, and the compelling economics of cloud-based outsourcing platforms whose multi-tenant infrastructure sharing enables investment in technology capability that no individual financial institution’s IT budget could justify for a dedicated internal system. SS&C Technologies’ Dimension platform, SimCorp’s cloud-native Dimension offering, and FIS’s asset management cloud suite collectively represent the commercial maturity of cloud-delivered middle office platform capability that is progressively matching the customisation depth of on-premise alternatives while delivering the scalability, update frequency, and total cost of ownership advantages that are driving financial institution migration decisions.

By End User, asset managers dominate, hedge funds grow fastest

Asset managers retained the dominant end user position with approximately 29.84% of the middle office outsourcing market in 2025, reflecting the investment management industry’s progressive recognition that the portfolio accounting, performance attribution, regulatory compliance, and investor reporting functions that constitute the asset management middle office are operationally complex, resource-intensive, and strategically non-differentiating in ways that make specialist outsourcing a commercially rational response to the cost, capability, and complexity challenges they present. The asset management outsourcing market’s growth is driven by the industry’s dual pressure of fee compression from passive investment competition and regulatory compliance cost growth, whose combined impact on operating margins is creating financial motivation to outsource operational functions at the costs that specialist providers can deliver through economies of scale and technology automation that in-house operations cannot match. Global asset management outsourcing engagements increasingly encompass the full middle office suite of portfolio accounting, performance measurement, risk analytics, compliance monitoring, and investor reporting delivered through a single integrated platform proposition from providers including State Street, BNY Mellon, Northern Trust, Caceis, and JP Morgan that compete for mandate relationships through technology platform differentiation, service level commitment, and strategic advisory value added beyond operational execution.

Hedge funds are the fastest-growing end user segment at a CAGR of approximately 10.43% through 2035, propelled by the structural alignment between the hedge fund operating model’s emphasis on lean core investment teams and the middle office outsourcing proposition’s ability to deliver institutional-grade operational infrastructure without the headcount, technology capital expenditure, and management attention that internal operation would require. The hedge fund sector’s outsourcing adoption rate has accelerated following several high-profile operational failures at funds that maintained extensive in-house operational infrastructure without achieving the resilience or accuracy standards that their institutional investors’ due diligence requirements impose, creating both a best practice argument for outsourcing and a competitive differentiation argument for funds whose outsourced infrastructure passes institutional investor operational due diligence more reliably than equivalent in-house arrangements.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Middle Office Outsourcing Market Insights

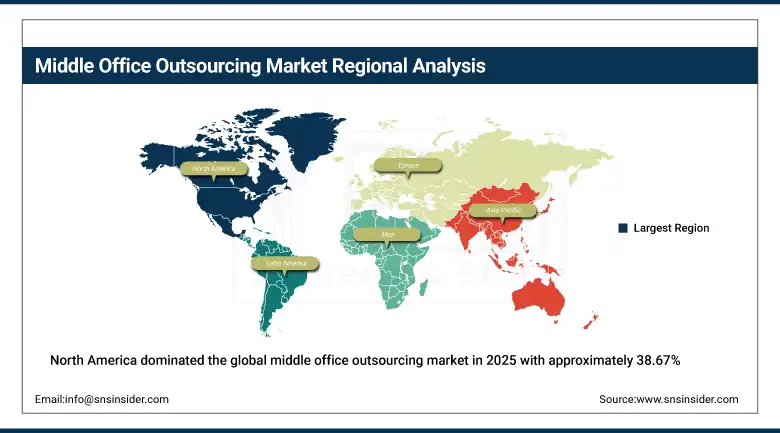

North America dominated the global middle office outsourcing market in 2025 with approximately 38.67% of global revenues, driven by the region’s concentration of the world’s largest asset management firms, hedge funds, and institutional investors whose combined operational complexity and regulatory burden create the strongest commercial motivation for middle office outsourcing adoption. The United States accounts for approximately 87.4% of North American revenues through the extraordinary depth of its financial services industry whose competitive fee pressure, regulatory complexity, and technology investment requirements are collectively driving outsourcing adoption across a broadening range of firm sizes and asset management strategies. Canada contributes approximately 12.6% of North American revenues through a sophisticated institutional investment management industry whose pension fund sector, including CPPIB, Ontario Teachers’ Pension Plan, and Caisse de dépôt et placement du Québec, generates significant middle office outsourcing demand through their complex multi-asset class and global market investment mandates.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Middle Office Outsourcing Market Insights

Europe is the world’s second-largest middle office outsourcing market where the EU’s comprehensive and evolving financial regulatory framework, whose AIFMD, UCITS, EMIR, MiFID II, and SFDR reporting requirements collectively impose a regulatory compliance burden that creates structural demand for outsourcing providers with dedicated regulatory technology platforms and compliance expertise across all major EU financial market regulatory frameworks. Germany accounts for approximately 22.3% of European revenues through its concentration of both institutional asset managers including DWS, Union Investment, and Allianz Global Investors and the specialised outsourcing infrastructure of German Landesbanks and major custodians including Clearstream that serve the European institutional investment industry’s middle office requirements. The EU’s Digital Operational Resilience Act implementation requirements, which mandate comprehensive operational resilience testing and third-party ICT service provider oversight for financial institutions, are reshaping the middle office outsourcing procurement standards that European financial firms apply to their service provider relationships.

Asia Pacific Middle Office Outsourcing Market Insights

Asia Pacific is the fastest-growing regional middle office outsourcing market at a CAGR of approximately 10.72% through 2035, driven by the rapid growth of the region’s asset management industry as rising middle-class wealth across China, India, Japan, South Korea, and Singapore creates institutional and retail investment demand that is growing the assets under management of regional investment managers at rates that create proportional middle office operational complexity growth whose outsourcing solutions are increasingly sought from both global service providers and regional specialists. China accounts for approximately 61.7% of Asia Pacific revenues through the extraordinary growth of its fund management industry, with China’s publicly offered fund assets exceeding RMB 30 trillion by 2025, creating a large and growing middle office service demand that domestic providers including ChinaAMC and CIFM are addressing alongside international entrants including State Street and Caceis who are building their China middle office service capabilities.

MEA & Latin America Middle Office Outsourcing Market Insights

The Middle East and Africa and Latin America are emerging middle office outsourcing markets where the rapid growth of sovereign wealth fund assets, the development of local capital markets requiring institutional-grade operational infrastructure, and the entry of global asset management firms into regional markets are creating growing demand for outsourced middle office capabilities that domestic providers are beginning to serve alongside established global firms. Saudi Arabia leads Middle East and Africa revenues at approximately 38.4% of the regional total through the Public Investment Fund’s extraordinary growth, whose expanding assets under management and increasingly sophisticated investment programme across diverse asset classes and geographies are creating middle office operational requirements whose scale and complexity justify institutional-grade outsourcing partnerships with global service providers. Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large and sophisticated asset management industry, with Brazilian fund managers including Itau Asset Management, Bradesco BBI, and BTG Pactual generating substantial middle office outsourcing demand as their product range sophistication and regulatory reporting burden grow proportionally with assets under management.

Market Dynamics

Growth Drivers: Rising regulatory compliance complexity creating institutional demand for specialist outsourcing expertise, AI and automation technology improving outsourcing service quality and cost efficiency, and fee compression across asset management industry driving operational efficiency imperatives

The primary structural growth drivers for the middle office outsourcing market are the compounding regulatory compliance burden whose complexity growth across multiple simultaneous international frameworks creates operational demands that exceed the expertise and technology capacity of in-house compliance teams at all but the world’s largest financial institutions, combined with the asset management industry’s fee pressure dynamic that requires institutions to reduce their total expense ratios by delivering operational functions at lower cost without compromising the quality and accuracy standards that institutional investors’ due diligence frameworks require. The AI and automation technology wave is simultaneously improving the commercial proposition of outsourced middle office services by enabling providers to deliver higher-quality, more timely, and more error-free operational outputs through automation of the reconciliation, exception management, and report generation workflows that previously required large teams of operations staff whose cost structures made outsourcing economics less compelling relative to well-managed internal operations.

Restraints: Data security and regulatory sovereignty concerns limiting cloud adoption, transition complexity and cost from internal to outsourced operational model, and service provider concentration risk concerns from financial institution oversight frameworks

A significant restraint on the middle office outsourcing market is the data security and regulatory sovereignty concern that financial institutions face when considering the transfer of sensitive portfolio, risk, and client data to third-party service providers whose data handling standards, geographic data residency practices, and cybersecurity infrastructure must be independently verified and continuously monitored to satisfy both internal risk management standards and regulatory outsourcing oversight requirements. The operational transition cost and complexity of moving from established internal middle office operations to an outsourced service model represents a procurement barrier that delays outsourcing decision implementation even when the economics and capability improvement rationale are clearly favourable, as the data migration, system integration, process documentation, and parallel running requirements of outsourcing transitions impose substantial one-time investment and management attention that competes with other IT and operational transformation priorities.

Opportunities: Hedge fund operational due diligence requirements creating outsourcing adoption pressure, private credit and alternatives growth creating new complex asset class outsourcing demand, and ESG reporting requirements creating new compliance outsourcing service category

ESG and sustainability reporting represents one of the most commercially significant new service category opportunities in the middle office outsourcing market, as the proliferation of mandatory and voluntary ESG disclosure requirements including SFDR PAI reporting, TCFD climate risk disclosure, and the SEC’s climate disclosure rule creates complex data collection, portfolio-level aggregation, and regulatory report generation requirements whose operational burden is creating demand for specialist outsourcing solutions that combine ESG data provider relationships, reporting template libraries, and regulatory compliance expertise in integrated service propositions.

Recent Developments:

-

2025: State Street launched an integrated end-to-end digital platform with expanded middle office capabilities for its Charles River Investment Management Solution clients, providing cloud-based portfolio analytics, automated compliance monitoring, and real-time performance attribution through a unified technology platform that consolidates front-to-middle office workflows for institutional asset management clients.

-

2025: Northern Trust partnered with Hazeltree in 2025 to integrate treasury management capabilities within its middle office outsourcing service for asset management clients, expanding the scope of outsourced functions beyond traditional portfolio accounting and compliance to include cash management, financing, and counterparty risk capabilities that institutional clients increasingly seek from comprehensive operational partnerships.

-

2025: SS&C Technologies expanded its Dimension cloud platform with new ESG data integration and sustainability reporting automation capabilities, enabling asset management clients to automate the data collection, aggregation, and regulatory report generation for SFDR, TCFD, and institutional investor ESG mandate compliance requirements through the outsourced platform rather than internal process development.

-

2025: BNY Mellon Asset Servicing launched an AI-powered reconciliation automation service that applies machine learning to reduce reconciliation exception volumes by over 40% for outsourcing clients, improving settlement efficiency and reducing the manual exception resolution effort that represents a significant operational cost component in traditional middle office service delivery.

-

2025: Citco Group expanded its alternative investment fund middle office services with new private credit portfolio monitoring and reporting capabilities targeting the growing private credit fund manager segment whose complex loan portfolio management, covenant tracking, and investor reporting requirements create specific middle office operational demands that general asset management platforms do not natively serve.

Middle Office Outsourcing Market Key Players

-

State Street Corporation

-

BNY Mellon (Bank of New York Mellon)

-

Northern Trust Corporation

-

J.P. Morgan Securities Services

-

Citco Group

-

SS&C Technologies Inc.

-

SimCorp A/S (Deutsche Boerse)

-

Caceis (Crédit Agricole)

-

FIS (Fidelity National Information Services)

-

Broadridge Financial Solutions Inc.

-

HSBC Securities Services

-

Apex Group Ltd.

-

NAV Consulting Inc.

-

Maitland Group

-

IQ-EQ Group

-

Alter Domus

-

Amundi Asset Management

-

Kroll (formerly Duff & Phelps)

-

SGSS (Societe Generale Securities Services)

-

Hazeltree LLC

Middle Office Outsourcing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.83 Billion |

| Market Size by 2035 | USD 21.01 Billion |

| CAGR | CAGR of 9.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Portfolio Accounting & Reporting, Risk Management, Compliance & Regulatory Reporting, Trade Processing & Settlement, Performance Measurement, Others) • By Deployment Type (On-Premise, Cloud-Based, Hybrid) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By End User (Asset Managers, Hedge Funds, Insurance Companies, Pension Funds, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | State Street Corporation, BNY Mellon (Bank of New York Mellon), Northern Trust Corporation, J.P. Morgan Securities Services, Citco Group, SS&C Technologies Inc., SimCorp A/S (Deutsche Boerse), Caceis (Crédit Agricole), FIS (Fidelity National Information Services), Broadridge Financial Solutions Inc., HSBC Securities Services, Apex Group Ltd., NAV Consulting Inc., Maitland Group, IQ-EQ Group, Alter Domus, Amundi Asset Management, Kroll (formerly Duff & Phelps), SGSS (Societe Generale Securities Services), Hazeltree LLC |

Frequently Asked Questions

North America dominated the Middle Office Outsourcing Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

On-Premise deployment dominated with approximately 46.78% of revenues in 2025.

Rising regulatory compliance complexity across multiple international financial regulatory frameworks creating institutional demand for specialist outsourcing expertise and technology platform capability, combined with fee compression across the asset management industry creating cost efficiency imperatives that make specialist outsourcing providers’ scale economics and automation capability increasingly compelling relative to internal operational function management.

The Middle Office Outsourcing Market was valued at USD 8.83 Billion in 2025.

The Middle Office Outsourcing Market is expected to grow at a CAGR of 9.07% from 2026 to 2035.

Get in Touch