Migraine Drugs Market Report Scope & Overview:

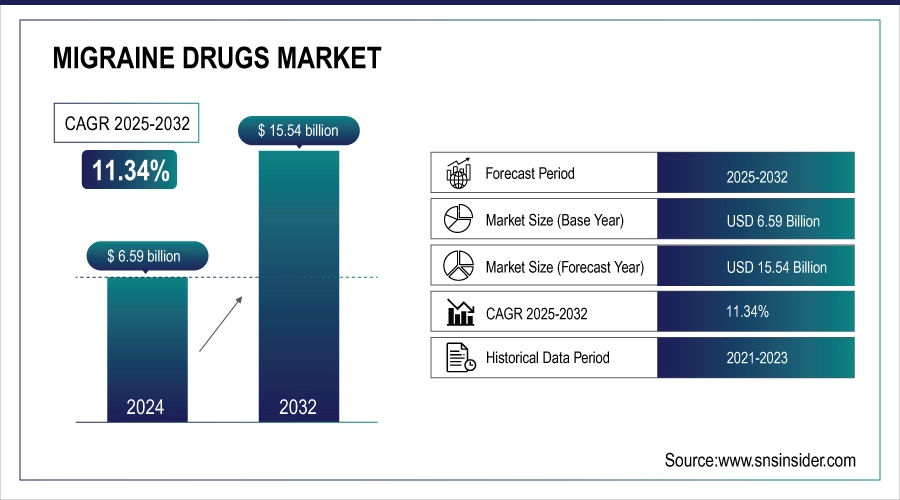

The migraine drugs market was valued at USD 6.59 billion in 2024 and is expected to reach USD 15.54 billion by 2032, growing at a CAGR of 11.34% over the forecast period of 2025-2032.

The global migraine drug markets are growing ever faster with the advent of alternatives that target CGRP monoclonal antibodies or gepants. The answer is that these therapies are more effective, better tolerated, and provide targeted relief, particularly for patients who don't respond to traditional medications, including triptans. This migraine drugs market trend underscores a pivot towards mechanism-based innovation, improved patient adherence, and an embracing of higher costs on a global scale. The trend, of course, perpetuates R&D investment, enriching its treatment diversity and boosting the market by advancing to unmet needs in migraine prevention and acute care.

For instance, in February 2025, Pfizer reported USD 835 million in 2024 global sales of Nurtec ODT, marking a 35% growth driven by CGRP therapy adoption.

Migraine Drugs Market Size and Forecast

-

Market Size in 2024: USD 6.59 Billion

-

Market Size by 2032: USD 15.54 Billion

-

CAGR: 11.34% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2020–2024

To Get more information On Migraine Drugs Market - Request Free Sample Report

Migraine Drugs Market Trends

-

Rising global prevalence of migraine disorders is driving drug demand, affecting over 1 billion people worldwide, with nearly 15% of the adult population impacted.

-

Increasing adoption of CGRP inhibitors is transforming treatment, accounting for over 35% of new migraine prescriptions in developed markets.

-

Growing use of preventive therapies is improving patient outcomes, with preventive treatment adoption rising by 20–25% in the last few years.

-

Expansion of oral and self-administered drugs is enhancing accessibility and compliance, contributing to over 50% of total migraine drug usage.

-

Rising healthcare spending and awareness is boosting market growth, with the migraine drugs market expected to grow at a CAGR of around 8–10% over the forecast period.

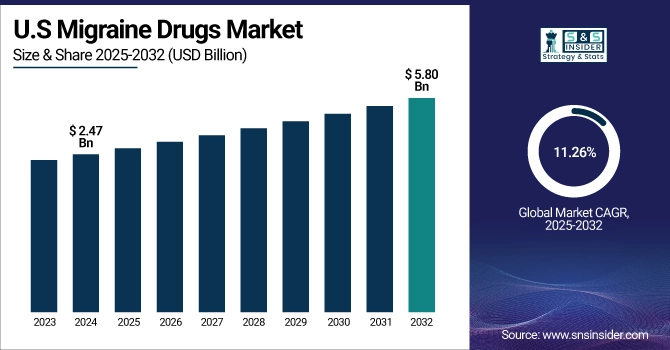

The U.S. migraine drugs market was valued at USD 2.47 billion in 2024 and is expected to reach USD 5.80 billion by 2032, growing at a CAGR of 11.26% over 2025-2032. The U.S. leads migraine drugs market due to its strong base for the pharmaceutical industry with high R&D, FDA approvals with efficiency, and high health care penetration. The high level of healthcare expenditure, targeted investment, and an innovation culture drive the pace of development and access to CGRP-targeted treatments. This champion analysis demonstrates how the US ecosystem fosters fast commercialization, rendering the country the most attractive pathway to launch innovative migraine drugs and expand the market over time.

For instance, in December 2024, IQVIA reported that the U.S. contributed over 63% of global CGRP migraine drug sales, led by AbbVie, Pfizer, and Eli Lilly.

Market Dynamics:

Drivers:

-

Rise of Fast-Acting Migraine Medications is Driving the Migraine Drugs Market Growth

Growing fast-acting migraine medications are the major drivers as they increase patient adherence, satisfaction & clinical outcomes for migraine drugs market. Such therapies address immediate symptom alleviation needs, driving adoption and growing the patient population. The effectiveness and convenience justify high pricing and innovation. This dynamic has a substantial impact on the migraine drugs market share. When the market leaders have drugs that work fast, such drug companies can win a competitive edge and drive the market further with R&D.

For instance, in November 2024, the Migraine Research Foundation reported that 64% of patients preferred fast-acting migraine therapies, citing quicker relief and improved post-dose functionality.

Restraints:

-

Side Effects and Dependency Risks Are a Significant Restraint on the Migraine Drugs Market Growth

Side effects and dependency risks remain significant barriers to the migraine drugs market growth by lowering patient compliance, constraining physician prescribing, and resulting in regulatory and reimbursement issues. Nothing is widely adopted over concerns about safety, particularly with opioids or drugs that don’t sit well with patients. Such risks impede public perception and market entry, which is hampering the growth of the migraine drugs market despite market innovation. Safety and tolerability are clearly still critical to tapping into the greater market.

For instance, in September 2024, the CDC reported that 14% of migraine patients discontinued their medication due to side effects, especially over triptans and older antidepressant-based treatments.

Segmentation Analysis:

By Treatment

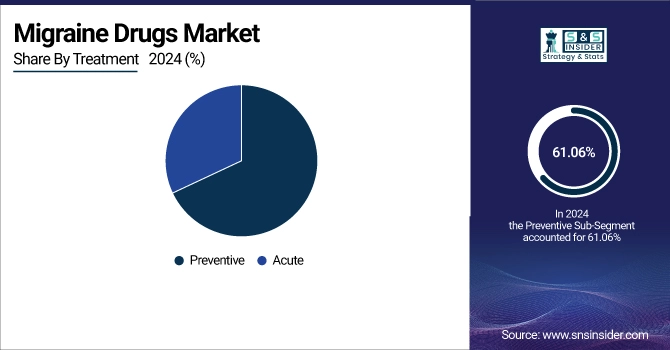

Preventive is the dominant segment in the global migraine drugs market, with a 61.06% market share in 2024, owing to increasing use of CGRP monoclonal antibodies and gepants that reduce attack frequency and severity. Increasing awareness, improved patient compliance, and the necessity of handling chronic migraine in the long term are factors. Preventive treatments are increasingly favoured by doctors to enhance treatment outcomes and diminish reliance on emergency care.

The acute segment is emerging as the fastest growing, with a CAGR of 11.05% in the migraine drugs market, fueled by more people with episodic migraines being diagnosed. Developments including gepants and nasal sprays provide fast symptom relief with fewer side effects than triptans. Patients' desire for rapid relief and better tolerance of the drugs were major factors that have been driving growth in this segment.

By Route of Administration

In 2024, the injectables dominated the ophthalmic lasers industry with a 68.76% market share, owing to the increasing use of CGRP monoclonal antibodies including Aimovig, Ajovy, and Emgality for preventive therapy. These long-acting injectables deliver a dose once a month or once per quarter, and their use has been shown to increase compliance while cutting the frequency of migraines. Proven effectiveness, ease of use, and expanding physician acceptance are likely to support wide adoption and the continued dominance of these drugs in the marketplace.

The Oral segment is the fastest growing aspect of the Migraine Drugs Market analysis, as the use of CGRP receptor antagonists including Nurtec ODT and Qulipta grows. These well-tolerated, non-invasive interventions may be used both acutely and prophylactically. Increased patient convenience, quicker onset of action, and lower adverse effects vs. older oral therapies are among the factors driving rapid expansion of this segment.

By Age

Pediatric held a dominant migraine drugs market share of 60.40% of the migraine drugs industry in 2024, driven by migraines are increasingly common in children and teenagers. The demand is driven by early diagnosis, parental awareness, and progress in formulation required for different age groups. Child neurologists are more and more involved in preventive and urgent treatments according to the recent approval for the use of moAbs in children with migraine, consolidating the pivotal role of these specialists in migraine management.

Geriatrics is emerging as the fastest-growing segment in the migraine drugs industry with the highest CAGR of 12.43%, owing to the rising prevalence of migraine in older adults and better recognition of late-onset migraine. Progress in such safer and better-tolerated treatments as CGRP inhibitors lowers the increased cardiovascular risk seen with drugs we currently have. Ageing populations and broader treatment recommendations are key drivers for the growth of this underserved population.

By Availability

Prescription Drugs are the largest segment of the migraine drugs industry and register for the highest CAGR of 11.58% over the forecast period, owing to the use of clinically available therapies, including triptans, gepants, and the novel drugs related to CGRP. They do need to be used under the guidance of a physician, as they are used most effectively in long-term or severe cases. Demand is high, powered by strong physician preference plus regulatory and insurance traction behind Rxist products. The expanding range of targeted therapy also reflects the dominance of this category in migraine treatment.

Regional Analysis:

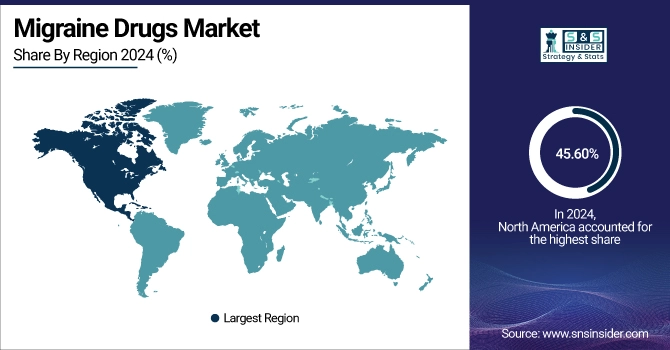

In 2024, the North American region holds the largest market share of the migraine drugs industry and dominates the market with a 45.60% market share, owing to a high disease burden, strong medical structure, and prevalent knowledge of migraine treatment. The adoption of advanced treatments at an early stage, the emergence of major pharmaceutical companies, and favorable reimbursement policies are some of the factors that contribute to the growth of the local market. A combination of high healthcare spending, clinical trials, and regulatory support of the FDA takes the market penetration of these CTC tests at full speed. Furthermore, the rise in the demand for new CGRP-based drugs and preventive treatments plays a key role in the dominance of the region in the global market for migraine medication.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe has a second large market for drugs due to the prevalence of migraine cases and government support for healthcare, and more awareness of early prevention of treatments. Factories producing potent pharmaceutical products, easy availability of advanced treatment, and public healthcare coverage have increased the availability of drugs in the area. Favorable reimbursement and increasing use of CGRP inhibitors are also fueling growth. Furthermore, research partnerships and multinational research programmes support Europe’s continued market presence.

Asia-Pacific emerges as the fastest-growing region with the highest CAGR of 8.28%, driven by an increase in the number of cases of migraine disorders, a rise in awareness regarding healthcare, the introduction of new products, and demand for innovative therapies in highly populated countries, including China and India. Urbanization, changing lifestyle, and stress-related diseases are imposing a greater burden of migraine. Governments are stepping up the development of healthcare infrastructure and specialty access, and big pharma is increasing funds into regional clinical development and manufacturing. The portion of novel therapies, including CGRP inhibitors and personalized medicine, is becoming more rapid. Moreover, better reimbursement policies, increased disposable income, and increasing penetration of telehealth further increase access to migraine treatment for patients. All these factors combined to make Asia Pacific one of the major growth-promoters of the market ahead.

The Middle East & Africa have the least share in the global migraine drugs market, as the region has poor healthcare infrastructure, less knowledge regarding migraine as a chronic disease, and limited availability of advanced treatment options. High cost of out-of-pocket treatments, low numbers of neurologists, and underdiagnosis are additional bottlenecks in the growth of the market. And given the regulatory obstacles and economic instability in some areas, the pharmaceutical investment is slow, leading to delayed adoption of more recent and effective migraine therapies.

The Latin American region accounts for a moderate share in the global migraine drugs market, with growing awareness, enhanced healthcare infrastructure, and growing prevalence of migraines. However, restricted access to novel treatments, high out-of-pocket expenses, and uneven health care coverage in some countries will continue to hamper more widespread market expansion. Government efforts to upgrade neurological care and increase urbanization are driving demand, however, pricing pressure and regulatory barriers are limiting the use of the latest migraine treatments in the region.

Key Players:

Migraine drugs Companies, including AbbVie Inc., Pfizer Inc., Eli Lilly and Company, Teva Pharmaceuticals, Amgen Inc., Novartis AG, Lundbeck A/S, H. Lundbeck A/S, Biohaven Ltd., Satsuma Pharmaceuticals, Zosano Pharma, Impel Pharmaceuticals, Axsome Therapeutics, Tonix Pharmaceuticals, Dr. Reddy’s Laboratories, Sun Pharma, Mylan, GSK plc, Boehringer Ingelheim, Aurobindo Pharma., and other players.

Recent Developments:

-

In March 2025, AbbVie announced the expanded global rollout of Qulipta (atogepant) for preventive migraine treatment, following positive Phase 3 results in Europe and Asia-Pacific.

-

In May 2025, Teva launched a biosimilar to fremanezumab (Ajovy) in selected Latin American markets to improve affordability and access to migraine preventive therapies.

-

In June 2024, Biohaven launched a Troriluzole Phase 2 trial for migraine prophylaxis, signaling its strategy to diversify its pipeline beyond CGRP-targeting drugs.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 6.59 billion |

| Market Size by 2032 | USD 15.54 billion |

| CAGR | CAGR of 11.34% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment (Acute, Preventive) • By Route of Administration (Oral, Injectable, Others) • By Age (Pediatric, Adult, Geriatric) •By Availability (Prescription Drugs, Over-the-Counter (OTC) Drugs) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | AbbVie Inc., Pfizer Inc., Eli Lilly and Company, Teva Pharmaceuticals, Amgen Inc., Novartis AG, Lundbeck A/S, H. Lundbeck A/S, Biohaven Ltd., Satsuma Pharmaceuticals, Zosano Pharma, Impel Pharmaceuticals, Axsome Therapeutics, Tonix Pharmaceuticals, Dr. Reddy’s Laboratories, Sun Pharma, Mylan, GSK plc, Boehringer Ingelheim, Aurobindo Pharma and other players. |

Get in Touch