Medical Suction Devices Market Report Scope & Overview:

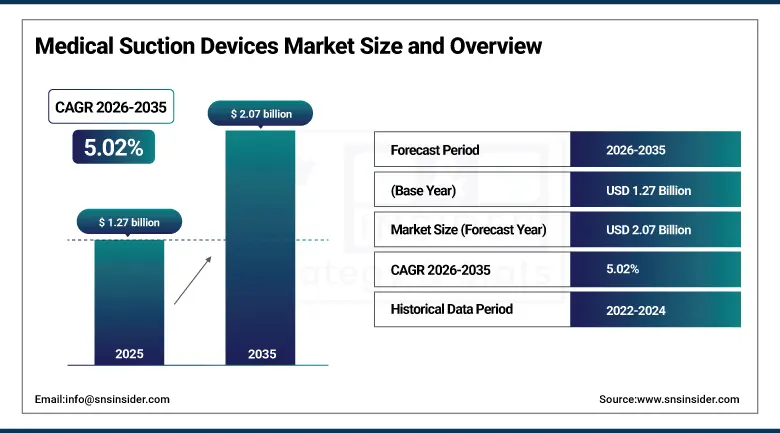

The Medical Suction Devices Market was valued at USD 1.27 billion in 2025 and is expected to reach USD 2.07 billion by 2035, growing at a CAGR of 5.02% from 2026-2035.

The medical suction devices market is experiencing growth because of the increase in the number of surgeries being conducted, increased cases of respiratory diseases, and greater demand for emergency care. The increase in aged patients and higher hospital admission rates are also playing a role in boosting the uptake of these devices. Improvements in the technology used in portable and battery-powered suction systems have resulted in greater effectiveness and mobility in the health care facilities. Increased investments in healthcare facilities and modern medical instruments are driving the market forward. Improved quality of home health care is another factor behind the growth of this market.

According to the World Health Organization, chronic respiratory diseases affected approximately 454.6 million people worldwide in 2025, significantly increasing the need for airway clearance and suction systems in hospitals and emergency care units.

Market Size and Forecast

-

Market Size 2026E: USD 1.33 Billion

-

Market Size 2035: USD 2.07 Billion

-

CAGR (2026-2035): 5.02%

-

Fastest Growing Market: Asia Pacific

-

Largest Market: North America

To Get more information on Medical Suction Devices Market - Request Free Sample Report

Medical Suction Devices Market Trends

-

Rising number of surgical procedures and emergency care cases is driving the medical suction devices market.

-

Growing adoption across hospitals, clinics, ambulatory surgical centers, and homecare settings is boosting market growth.

-

Expansion of respiratory care and critical care services is fueling demand for suction equipment.

-

Increasing focus on infection control, patient safety, and efficient fluid removal is shaping adoption trends.

-

Advancements in portable suction systems, battery-powered devices, and noise-reduction technologies are enhancing usability and performance.

U.S. Medical Suction Devices Market Size Outlook

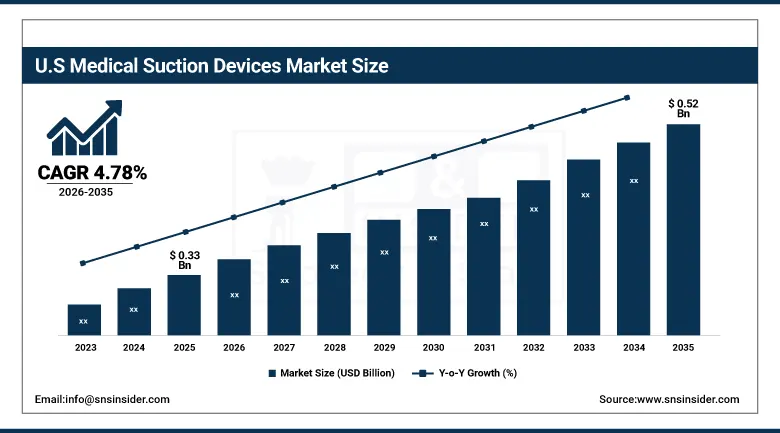

The U.S. medical suction devices market was valued at USD 0.33 Billion in 2025 and is expected to reach USD 0.52 Billion by 2035, growing at a CAGR of 4.78% over 2026–2035.

The U.S. medical suction devices market is witnessing significant growth owing to an increase in surgical procedures, the prevalence of respiratory ailments, and the high demand for critical care equipment. The growth of the elderly population and home healthcare services are also driving the growth of the market. The developments in technology such as portable and electrical devices are enhancing the effectiveness of treatment provided to patients. Besides, the well-developed health care system and constant investments in technological advancements are fueling the market growth.

According to the United Nations, the global population aged 65 years and above is projected to reach nearly 1.6 billion by 2050, increasing demand for surgical, respiratory, and long-term care treatments requiring suction devices.

Medical Suction Devices Market Segment Analysis

-

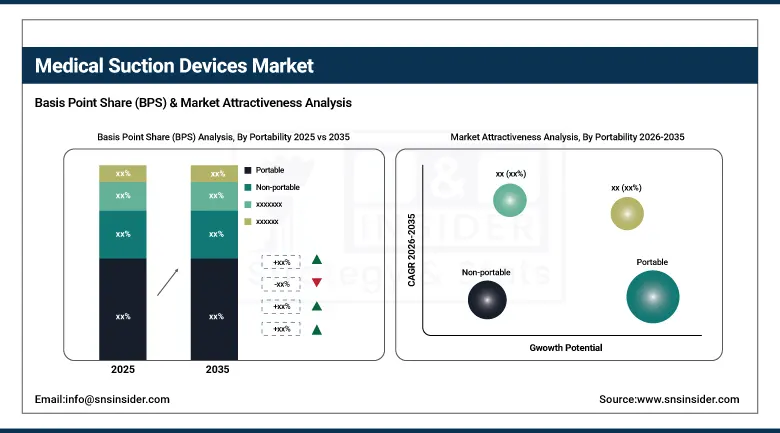

By Portability, Portable segment dominated the medical suction devices market in 2025 with 61% share; Non-portable segment is the fastest growing (CAGR).

-

By Application, Surgical Procedures segment dominated the medical suction devices market in 2025 with 39% share; Airway Clearing segment is the fastest growing (CAGR).

-

By Systems, Electrically Powered segment dominated the medical suction devices market in 2025 with 52% share; Venturi segment is the fastest growing (CAGR).

-

By End User, Respiratory segment dominated the medical suction devices market in 2025 with 33% share; Wound Suction segment is the fastest growing (CAGR).

By Portability, portable medical suction devices dominate the medical suction devices market, non-portable medical suction devices are the fastest growing

Portable medical suction devices dominate the medical suction devices market owing to their easy mobility, portability feature, and suitability for emergency cases, ambulances, and home healthcare purposes. The ability to offer instantaneous suction services during critical medical emergencies is one reason that contributes to the higher use of these products by patients in hospitals and outpatient centers. Increasing preference towards point-of-care therapy and demand for portable respiratory support devices help drive growth in this segment. Efficiency in battery operations also contributes significantly to their popularity.

Non-portable medical suction devices are the fastest growing segment owing to their increasing adoption in hospitals, surgical centers, and ICU due to increased suctioning power, effectiveness, and longer hours of operation. Higher hospital admission rates, increased surgical numbers, and the expansion in the healthcare industry are boosting demand. Recent developments in technology have been offering more safety features in addition to durability, helping boost adoption rates of this product category around the globe.

By Application, surgical procedures dominate the medical suction devices market, airway clearing is the fastest growing

Surgical procedures dominate the medical suction devices market owing to the crucial importance of suction equipment in facilitating removal of blood, body fluids, and debris during surgery. The demand for these devices is on the rise owing to high incidences of surgeries in the fields of cardiovascular, orthopedic, neurosurgery, and general surgeries. Efficient suction devices ensure clear operating fields and safe operations. Advances in precision suction devices and high incidence rates of surgeries around the world are key reasons for dominance of the application segment in 2025.

Airway clearing is the fastest growing segment in the Market owing to higher incidence of respiratory ailments, chronic obstructive pulmonary disease, asthma, and breathing difficulties in emergencies. The need to quickly eliminate mucus from the lungs and facilitate breathing is leading to increased demand for suction equipment. Increased aging population and availability of home health services are key factors supporting market growth. Advancements in portable suction devices and awareness about respiratory health care have been key factors contributing to growth in the past few years.

By Systems, electrically powered systems dominate the medical suction devices market, venturi systems are the fastest growing

Electrically powered systems dominate the medical suction devices market because of their high suction power, continuous operation, and high efficiency. They are considered an important choice for any operation that requires reliable performance. The rising number of applications in ICU wards, operating theaters, and other medical facilities is also driving its dominance. Technical developments related to better energy management, automatic control, and higher levels of safety continue to raise the demand for electrical systems, thus positioning them as the major market segment in 2025.

Venturi systems are the fastest growing segment in the Market because of their portability, reduced maintenance needs, and effective working without reliance on electrical power. They are widely applied in emergency departments and ambulances, making them suitable for emergencies. Demand for the system is rapidly growing due to the need for portable devices. Growth in the emergency medical services sector and the need for alternative sources of suction power during disruptions of electrical supply have contributed significantly to growth.

By End User, respiratory applications dominate the medical suction devices market, wound suction is the fastest growing

Respiratory segment dominated the medical suction devices market owing to increasing cases of chronic respiratory diseases, asthma, pneumonia, and chronic obstructive pulmonary diseases across the world. The suction device finds wide application in clearing airways and providing breathing assistance in hospitals, intensive care units, and emergency departments. Increasing geriatric population and incidences of respiratory infections act as fuel to the segment. Further, technological innovations in respiratory care devices and increasing applications of suction devices in home care are contributing towards market leadership till 2025.

Wound suction segment is the fastest growing segment in the Market due to growing usage of negative pressure wound therapy for speedy healing and infection management. Increasing incidences of diabetic ulcers, traumatic wounds, burn cases, and post-operative wounds are the major reasons for growth. Healthcare professionals' preference for innovative and technologically advanced wound management system that helps in improving recovery and minimizing hospitalization periods fuels market growth. Innovations in portable wound suction devices and awareness regarding wound treatment also contribute to rapid growth in the market.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

92.3% |

|

Europe |

United Kingdom |

24.7% |

|

Asia Pacific |

China |

45.1% |

|

Middle East & Africa |

UAE |

13.9% |

|

Latin America |

Brazil |

50.2% |

North America Medical Suction Devices Market Insights

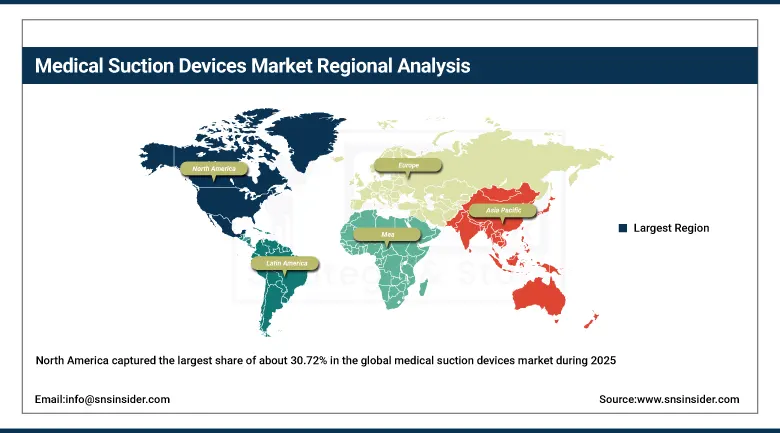

North America captured the largest share of about 30.72% in the global medical suction devices market during 2025 because of its advanced healthcare facilities, higher number of surgeries performed, and increased use of medical equipment with advanced technology. There is a good hospital network in North America along with advanced emergency facilities in addition to the increased use of respiratory care equipment. Increased incidence of chronic respiratory diseases and a growing geriatric population will boost the demand for these products. Other factors contributing to the growth include the presence of key players and continuous development in the healthcare sector.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Medical Suction Devices Market Insights

Europe holds a significant position in the medical suction devices market owing to the presence of well-established healthcare facilities, presence of established medical device companies, and rising use of advanced medical devices. Increasing numbers of surgical operations, along with the rising incidence rate of breathing diseases, are fueling the demand for such products. Europe also enjoys good healthcare spending and favorable reimbursement policies. The focus on hygiene control and patient safety has led to the adoption of advanced suction systems. The growing number of elderly people and increasing demand for home healthcare services have helped in boosting the market.

Asia Pacific Medical Suction Devices Market Insights

The Asia Pacific segment is projected to witness the fastest CAGR of 5.70% during the forecast period of 2026–2035 owing to factors such as improved healthcare infrastructure, increased healthcare spending, and increased demand for sophisticated medical devices in the emerging nations. The increase in the prevalence of respiratory diseases and the increase in surgical procedures have led to an increase in demand for medical suction devices. Furthermore, factors like rapid population growth and increasing numbers of the geriatric population have also contributed significantly to market growth. Besides, growing awareness about emergency care services and home healthcare services has fueled the demand for advanced medical suction devices.

Middle East & Africa and Latin America Medical Suction Devices Market Insights

Middle East & Africa and Latin America regions are experiencing steady growth in the medical suction devices market due to the presence of developed healthcare infrastructure and investments made by the governments towards healthcare sector in these regions. Increasing incidences of respiratory disorders coupled with rising requirement for emergency care and surgeries is driving the usage of products. Expansion in healthcare facilities and establishment of hospitals in emerging economies is driving market growth. Increasing investments in healthcare equipment for improved standards of care and increasing awareness about respiratory disorders along with rising need for portable healthcare products is contributing to sustained growth.

Growth Drivers: Increasing surgical procedures and emergency admissions driving demand for efficient suction systems across hospitals and critical care settings

A significant rise in the number of surgeries, trauma, and emergency medical cases has resulted in high demand for medical suction machines in hospitals and healthcare centers all over the world. Such suction devices are essential in evacuating fluids, blood, and secretion from surgical as well as emergency procedures. They ensure that the airway is clear in such situations, improving the safety of patients. The increasing incidences of chronic respiratory conditions and admissions into intensive care units have also contributed to the increasing use of these products. Improved healthcare infrastructure as well as healthcare spending has led to an increased preference for technologically advanced suction systems. Portable and battery-powered suction machines are highly desirable in ambulatory and emergency transportation situations.

Restraints: Risk of infections and operational complications creating patient safety concerns during prolonged suction procedures globally

Failure to clean, sterilize, and handle medical suction equipment effectively may result in healthcare-related infections and spread of infections from one patient to another. Long procedures performed using medical suction devices may result in respiratory irritation and tissue damage to the affected individuals. Malfunctions and poor suction pressure may impact the efficiency of the medical processes. Hygiene policies and monitoring of the equipment by healthcare facilities have added more operational complexities and workloads to the medical personnel. Safety concerns about product recalls of medical suction equipment that causes malfunctions may lower levels of confidence among the medical providers and purchasers.

Opportunities: Expanding home healthcare services and rising portable equipment demand creating growth opportunities for compact suction device manufacturers

The fast-growing trend of providing home healthcare solutions is leading to significant growth prospects for portable and handy medical suction machines across the globe. The increasing acceptance among older and chronically ill patients for home treatment is leading to an upsurge in the demand for handheld respiratory devices. The portability of the device along with its ease of use makes it convenient and cost-effective in non-clinical settings. With improvements in battery life and compact design of the device, its efficacy is being improved in the ambulatory environment. Rising awareness about telehealth and outpatient treatments is contributing to the growing demand for portable medical devices.

Recent Developments:

-

2026: SSCOR, Inc. enhanced portable suction systems for EMS, military, and hospital emergency applications. The upgraded systems improved durability, battery runtime, and high-performance airway suction capability in critical care situations.

-

2026: Laerdal Medical upgraded emergency care simulation platforms incorporating realistic suction and airway obstruction management training for healthcare professionals. The systems improve training quality for emergency respiratory and trauma response procedures.

-

2025: Smiths Medical introduced improvements to portable suction systems designed for emergency transport, ambulatory care, and hospital respiratory treatment applications. The upgrades emphasized compact design, battery performance, and reliable secretion removal.

-

2024: ATMOS MedizinTechnik GmbH & Co. KG introduced upgraded ENT and surgical suction systems with enhanced precision control, quieter operation, and improved hygiene standards. The systems were developed for operating rooms and specialized medical suction applications.

-

2024: Drive DeVilbiss Healthcare increased production and distribution of portable suction units designed for homecare and clinical respiratory management. The devices support mucus and secretion removal for patients with chronic respiratory conditions and post-operative care requirements.

Medical Suction Devices Market Key Players are:

-

Allied Healthcare Products, Inc.

-

Medtronic plc

-

Drive DeVilbiss Healthcare

-

ATMOS MedizinTechnik GmbH & Co. KG

-

Laerdal Medical

-

Welch Allyn

-

HERSILL S.L.

-

Laubscher Präzision AG

-

Olympus Corporation

-

Stryker Corporation

-

Smiths Medical

-

Intersurgical Ltd.

-

SSCOR, Inc.

-

MediSafe International

-

Penn Care, Inc.

-

Allied Medical Limited

-

Flexicare Medical Ltd.

Medical Suction Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.27 Billion |

| Market Size by 2035 | USD 2.07 Billion |

| CAGR | CAGR of 5.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Portability (Portable, Non-portable) • By Application (Surgical Procedures, Airway Clearing, Research & Diagnostics, Dental Applications) • By Systems (Manual, Electrically Powered, Venturi) • By End User (Respiratory, Gastric, Wound Suction, Delivery Rooms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Allied Healthcare Products, Inc., Precision Medical, Inc., Medtronic plc, Drive DeVilbiss Healthcare, ZOLL Medical Corporation, ATMOS MedizinTechnik GmbH & Co. KG, Laerdal Medical, Welch Allyn, HERSILL S.L., Laubscher Präzision AG, Olympus Corporation, Stryker Corporation, Smiths Medical, Intersurgical Ltd., SSCOR, Inc., MediSafe International, Penn Care, Inc., Medela AG, Allied Medical Limited, Flexicare Medical Ltd. and other players. |

Frequently Asked Questions

The Portable segment dominated the Medical Suction Devices Market in 2025.

Adoption of Portable & Homecare Devices is Driving the Medical Suction Devices Market Growth.

The Medical Suction Devices Market size was USD 1.27 billion in 2025 and is expected to reach USD 2.07 billion by 2035.

The Medical Suction Devices Market is expected to grow at a CAGR of 5.02% over the forecast period.

Get in Touch