Nanocapsules Market Report Scope & Overview:

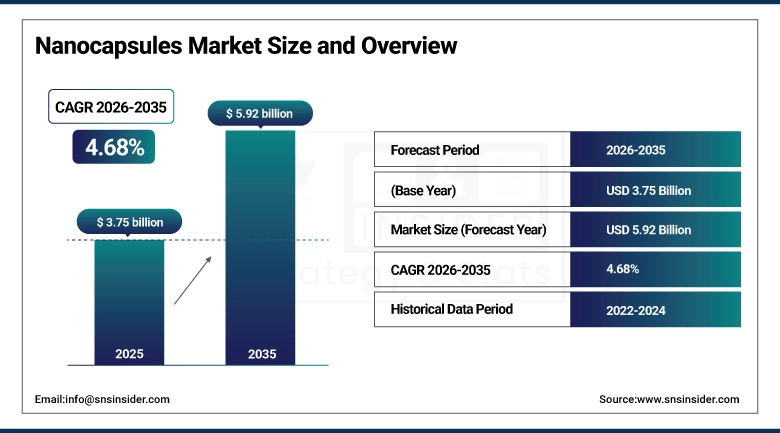

The Nanocapsules Market size was valued at USD 3.75 billion in 2025 and is expected to reach USD 5.92 billion by 2035, growing at a CAGR of 4.68% over the forecast period of 2026-2035.

The nanocapsules market is growing at a steady pace with high momentum; this is mainly because a growing number of industries are now realizing the potential benefits offered by nanotechnology for the delivery of products. In the case of the pharmaceutical industry, for example, the growing need for precision oncology and personalized medicine is now prompting a number of drug manufacturers to concentrate more on the formulation of polymer-based and lipid nanocapsule systems for the targeted delivery of drugs directly to the site of the disease without the occurrence of side effects. In the case of the food and nutraceutical industry, a growing number of manufacturers are now using nanocapsule technology for the formulation of products for longer shelf life, bitter taste masking, and heat protection of ingredients during food processing and gastrointestinal digestion. Similarly, the cosmetics industry is not far behind; a growing number of manufacturers are now using nanocapsule technology for the formulation of high-performance products. The growing investments in nanomedicine R&D, the availability of a favorable regulatory environment for nano-enabled drug delivery in the U.S. and European markets, and the growing manufacturing capabilities in the Asian market are also contributing to the growth of the nanocapsules market.

For instance, in April 2024, a global pharmaceutical industry survey found that nano-based drug delivery systems, including nanocapsules, accounted for approximately 18.4% of all new drug formulation development projects initiated in 2023, reflecting a measurable and growing industry pivot toward nanoscale delivery platforms.

Nanocapsules Market Size and Forecast:

-

Market Size in 2025: USD 3.75 billion

-

Market Size by 2035: USD 5.92 billion

-

CAGR: 4.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Nanocapsules Market - Request Free Sample Report

Nanocapsules Market Trends

-

Sustained adoption of polymeric and lipid-based nanocapsule platforms in oncology drug delivery, supported by growing clinical validation of nanoparticle-mediated tumor accumulation through enhanced permeability and retention (EPR) effects.

-

Increasing integration of stimuli-responsive nanocapsule systems, including pH-triggered, thermo-sensitive, and redox-activated formulations, enabling on-demand payload release within targeted biological microenvironments.

-

Growing commercial interest in nutraceutical encapsulation to improve oral bioavailability of omega-3 fatty acids, curcumin, coenzyme Q10, and fat-soluble vitamins, driven by rising global consumer health awareness.

-

Expanding application of nanocapsule coatings in crop protection and agricultural formulations, where controlled pesticide and herbicide release is reducing chemical runoff and improving field efficacy.

-

Rising adoption of naturally derived wall materials, including chitosan, zein, and cellulose nanocrystals, as manufacturers respond to consumer and regulatory pressure for biodegradable and clean-label encapsulation systems.

-

Growing convergence of nanocapsule technologies with mRNA delivery platforms, illustrated by the success of lipid nanoparticle systems in vaccine development and its spillover effect into broader nanomedicine investment.

-

Increasing collaboration between academic nanomedicine research centers and pharmaceutical companies to advance scale-up of laboratory-stage nanocapsule formulations into commercially viable GMP-compliant manufacturing processes.

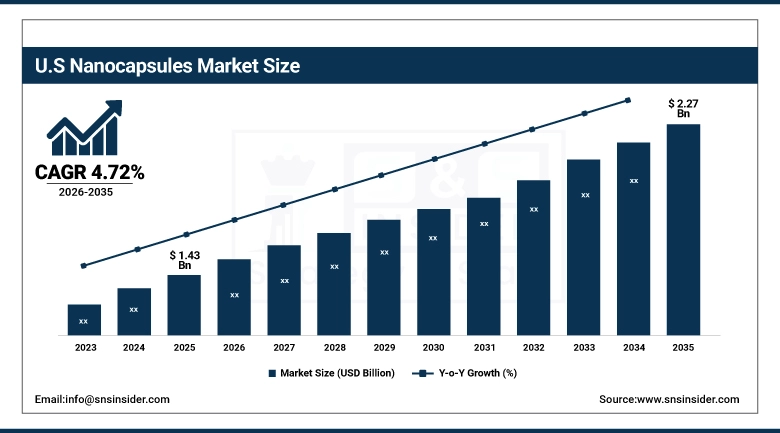

The U.S. Nanocapsules Market was valued at USD 1.43 billion in 2025 and is expected to reach USD 2.27 billion by 2035, growing at a CAGR of 4.72% from 2026-2035. Nanocapsules Market : Market Dynamics North America Region is the market leader for nanocapsules market owing to research & development activities for pharmaceutical products, quality of existing CMO infrastructure for nanoscale formulation work and regulatory framework improving for nanotechnology-enabled drug products by FDA. Financial support for nanotechnology research and design expenditures from the National Nanotechnology Initiative (NNI), as well as the funding of nanomedicine start-up enterprises by private risk capital investors, will continue to power the initial breakthroughs in new nanocapsule classes prior to the upscaling of supply to develop larger commercial market sizes. Nanocapsules are in strong demand for the oncology, pain relief and functional foods application.

Nanocapsules Market Growth Drivers:

-

Rising Demand for Targeted Drug Delivery in Oncology is Driving the Nanocapsules Market Growth

One of the most visible and tangible market drivers of an expanding nanocapsule market may be the need for an increasingly accurate and precise method of delivering cancer drugs. The current method of chemotherapy has been shown to be deficient in a number of areas. It has been shown to be systemically toxic and to cause dose-limiting side effects. The nanocapsule is able to encapsulate the chemotherapy agent and then deliver it to the target site. This is done by encapsulating the agent in a membrane. The need to address this burgeoning area of research is becoming increasingly evident due to the fact that there will be over 35 million cases of cancer by the year 2050, as estimated by the World Health Organization.

For instance, in August 2024, the FDA's Center for Drug Evaluation and Research reported that nanotechnology-based drug products, inclusive of polymer nanocapsule formulations, represented approximately 22% of all novel cancer drug applications reviewed under NDA and BLA pathways during fiscal year 2023, underscoring the growing role of nanocapsule technology in oncology drug pipelines.

Nanocapsules Market Restraints:

-

High Manufacturing Complexity and Scalability Challenges are Hampering Nanocapsules Market Growth

While the laboratory-scale results for nanocapsule formulations have been impressive, moving them towards commercial-scale GMP manufacture is arguably one of the tougher hurdles that has thus far prevented the market for such products from growing faster. This is particularly true for certain contract manufacturers that, despite having invested in state-of-the-art equipment, are not yet fully equipped to handle the highly specialized process conditions that are necessary for the manufacture of nanocapsule formulations on a commercial scale. Issues related to quality control, for example, regarding reproducibility, colloidal stability, and sterile fill finish compatibility, also contribute to the overall complexity and expense of the process. For smaller biotech companies and emerging market players, the overall capital costs that are necessary for accessing nanocapsule manufacturing capabilities may be a barrier, effectively limiting the overall competitive landscape for this exciting new class of drug delivery systems.

Nanocapsules Market Opportunities:

-

Expanding Application in Food, Nutraceuticals, and Functional Cosmetics Presents Significant Growth Opportunities for the Nanocapsules Market

Outside of the pharmaceutical arena, the food, nutraceutical, and personal care markets present a genuinely vast and growing business opportunity for nanocapsule technology suppliers that has not yet been fully tapped. For the production of functional foods, the capacity to encapsulate probiotics, polyphenols, and bioactive peptides in nanoscale delivery systems that are able to survive the gastrointestinal environment and deliver active ingredients in the target location is becoming increasingly important to food manufacturers seeking to support health benefit claims with bioavailability data. For the personal care industry, the performance advantage of encapsulated retinol, vitamin C, and peptide actives over their unencapsulated analogues is creating business investment opportunities for nanocapsule-based formulation platforms among premium personal care manufacturers as consumers in North America, Europe, and Asia Pacific are increasingly willing to pay a premium for science-based, functional personal care products, thereby increasing the business case for nanocapsule integration into the food and personal care value chain.

For instance, in November 2024, the global functional food ingredients market report by a leading industry intelligence firm noted that nanocapsule-based bioactive delivery systems were incorporated in approximately 14.7% of new functional food product launches globally in 2024, reflecting a year-on-year increase of 3.2 percentage points from 2023 and confirming the segment's growing commercial relevance.

Nanocapsules Market Segment Analysis

-

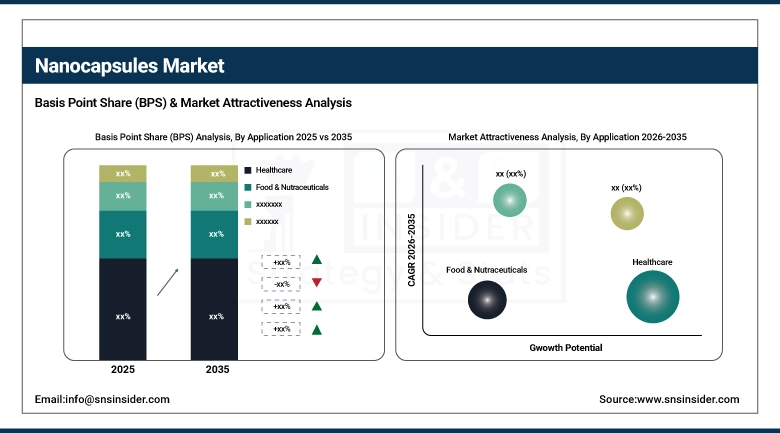

By application, healthcare held the largest share of approximately 52.40% in 2025, while the food and nutraceuticals segment is expected to register the highest CAGR of 6.12% over the forecast period.

-

By therapeutic area, oncology dominated with a share of approximately 44.27% in 2025, and the endocrinology segment is expected to register the highest CAGR of 5.87% through 2035.

By Application, Healthcare Leads the Market, While Food & Nutraceuticals Registers Fastest Growth

The healthcare segment held the largest revenue share of around 52.40% in 2025 due to the high degree of nanocapsule technology incorporation in pharmaceutical drug delivery systems, including injectable oncology agents, oral bioavailability enhancement systems, and topical dermatology agents. Strong regulatory backing and clinical development activity, along with an increasing degree of acceptance of nano-based therapeutics by healthcare providers, will ensure the continued dominance of the healthcare industry in the overall market. The food and nutraceuticals industry is projected to record the highest CAGR of around 6.12% during the forecast period of 2026-2035 due to an increase in consumer interest in high bioavailability ingredients for supplement formulation, clean label encapsulant resins and polymers, and functional food products with clinical evidence of health benefits. The cosmetics industry recorded a share of around 18.67% in 2025 and will continue to enjoy the premiumization trend in global skincare products due to an increased degree of differentiation of products by nanocapsule delivery system suppliers.

By Therapeutic Area, Oncology Leads, While Endocrinology Registers Fastest Growth

Therapeutic area share of oncology is also prominent accounting for 44.27% in 2025, supported by broad clinical adoption of nano-formulated cytotoxic agents; expanding pipeline of nanocapsule-encapsulated small molecule inhibitors and nucleic acid therapeutics targeting solid tumors and hematological malignancies; as well as strong FDA and EMA regulatory support for oncology nano-drug applications. In 2025, pain management captured the second largest share, at nearly 28.16%, propelled by the ability of various nanoparticles to enhance the delivery profiles of NSAIDs, opioids, and local anestheticals, via systemic and localized administration routes. During the period 2026 to 2035, the highest approximate CAGR of 5.87% is projected for the endocrinology segment, attributed to the increase in demand for nanocapsule-insulin delivery systems, stabilization platform for peptide hormones, and oral delivery of biologics which are typically limited to parenteral administration. This endocrinology opportunity is relevant to advances in mucus-penetrating nanoparticle coatings and gastrointestinal-targeted release systems.

Nanocapsules Market Regional Highlights:

North America Nanocapsules Market Insights:

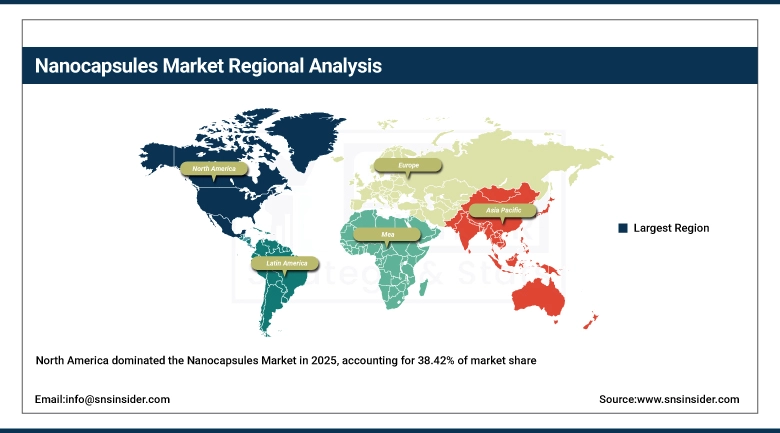

In 2025, North America contributed maximum share of 38.42% in terms of market revenue owing to dominance of the US in pharmaceutical innovation, the existence of the most developed contract manufacturing infrastructure for nanotechnology, and a readily funded community of investors interested in funding nanomedicine start-up and scale-up platforms. In addition, it also enjoys the benefits of coordinated support from the federal government via the National Nanotechnology Initiative, ongoing FDA regulatory guidance initiatives for nanotechnology, and a high yield pharmaceutical R&D landscape consistently spinning out best-in-class nanocapsule drug candidates for oncology, immunology, and CNS diseases. Canada is also a rising player in the sector, particularly in nutraceutical encapsulation, where novel encapsulant materials and process technologies with commercial implication are being developed through university industry partnerships.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Nanocapsules Market Insights:

Asia Pacific is the market leader in the growth of nanocapsules, recording a CAGR of 6.84%, driven by the rapidly expanding pharmaceutical manufacturing base, the expanding government research base in nanotechnology, and the huge and expanding population base of affluent consumers eager to adopt premium healthcare and food products. The two major contributors of growth in this market are China and India, as API and formulation companies within both countries are rapidly expanding their investment base in nanotechnology-based drug delivery systems to capture premium export markets and address the expanding demand for pharmaceuticals within their own countries. Japan and South Korea are major contributors of innovation within this market through well-funded academic-industry consortia focused on nanomedicine and the expanding base of biotechnology companies focused on nanotechnology. The regional authorities, such as NMPA and CDSCO, are gradually clarifying their guidelines on nanotechnology-based products, helping to reduce the uncertainty previously associated with this market.

Europe Nanocapsules Market Insights:

Europe secured the second position in revenue share, which was approximately 29.17% as of 2025. This was due to a well-established pharmaceutical and specialty chemical manufacturing industry, a high academic research output in nanoscience, and the European Commission's Horizon Europe funding program, which has invested considerable funds into nanotechnology and nanomedicine research and development. The countries contributing most to this market are Germany, France, and the UK, where a combination of large pharmaceutical companies and specialty encapsulation ingredient companies, as well as a CDMO industry segment increasingly focused on nano-enabled drug product services, is seen. The REACH legislation and EMA nanomedicine guidelines are establishing best practices in responsible nanocapsule development, and environmental biodegradability and nanotoxicology characterization are increasingly being emphasized as part of the approval requirements.

Latin America (LATAM) and Middle East & Africa (MEA) Nanocapsules Market Insights:

In Latin America, rising pharmaceutical generic production investments in Brazil and Mexico, as well as a growing nutraceuticals and cosmetics market, are contributing to a rising, though still small, demand for nanocapsule encapsulation services and technologies in these countries. In particular, research programs within the region's public university systems in Brazil and Argentina have been highly active in the development of natural polymer nanocapsule technologies, contributing to a still small, though rising, body of intellectual property in the region. In the Middle East and Africa, healthcare infrastructure upgrades in the Gulf Cooperation Council countries, as well as rising pharmaceutical import sophistication, represent the key near-term market driver for nanocapsule technologies, with South Africa and the UAE representing the most receptive markets for advanced nano-enabled formulation technologies in the region.

Nanocapsules Market Competitive Landscape:

BASF SE (founded in 1865) is one of the world's largest chemical companies and has a notable position in encapsulation ingredients used in the pharmaceutical, agrochemical, and food industries. The company contributes its expertise in polymer chemistry and its large-scale production capacity, along with its wide range of ingredients, to the supply chain of nanocapsules and is a partner of choice for those formulators requiring large quantities of reliable and pure encapsulant ingredients.

-

In February 2025, BASF expanded its pharmaceutical excipients portfolio with the commercial launch of a new grade of Kollicoat polymer specifically optimized for lipid-polymer hybrid nanocapsule formulations, targeting improved drug loading efficiency and gastrointestinal stability for oral oncology and endocrinology drug applications.

Evonik Industries AG (founded 1847; current legal form 2007) is a specialty chemicals company with a dedicated healthcare business segment providing polymeric biomaterials, lipid excipients, and drug delivery system components to the global pharmaceutical industry. Evonik's RESOMER and LIPOID brands are well established for the formulation of biodegradable polymeric nanocapsules and lipid nanoparticle-based drug delivery systems for injectables and oral applications.

-

In June 2024, Evonik announced the expansion of its Health Care business unit's nanotechnology capabilities through the inauguration of a dedicated lipid nanoparticle and nanocapsule process development laboratory in Darmstadt, Germany, designed to accelerate CDMO services for pharmaceutical clients advancing nano-formulated drug candidates through clinical development.

Croda International Plc (est. 1925) is a British specialty chemical company with a strong focus on high-performance ingredients for pharmaceuticals, personal care, and nutrition. Through its Croda Pharma division and the integration of Avanti Polar Lipids, Croda has established a leading position in lipid-based nanocapsule excipients, supplying ionizable lipid components and phospholipid materials used in lipid nanoparticle and nanocapsule formulations for both small molecule and nucleic acid drug delivery applications.

-

In October 2024, Croda International launched a new range of ionizable lipid excipients under its Excipients portfolio, specifically designed to improve mRNA and siRNA encapsulation efficiency and endosomal escape in nanocapsule-based nucleic acid delivery systems, addressing a key performance gap in next-generation nanomedicine formulation development.

Nanocapsules Market Key Players:

-

BASF SE

-

Evonik Industries AG

-

Croda International Plc

-

Givaudan SA

-

International Flavors & Fragrances Inc. (IFF)

-

Lonza Group AG

-

Syngenta AG

-

Encapsys LLC

-

Microtek Laboratories Inc.

-

Cabot Corporation

-

NanoViricides Inc.

-

Nanobiotix SA

-

Nanoform Finland Plc

-

Lubrizol Corporation (Particle Sciences)

-

Roquette Freres SA

-

Ashland Inc.

-

Adare Pharmaceuticals Inc.

-

Solvay SA

-

Thermo Fisher Scientific Inc.

-

Southwest Research Institute (SwRI)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.58 Billion |

| Market Size by 2035 | USD 5.92 Billion |

| CAGR | CAGR of 4.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application [Healthcare, Food & Nutraceuticals, Cosmetics, Others] • By Therapeutic Area [Oncology, Pain Management, Endocrinology, Others] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Evonik Industries AG, Croda International Plc, Givaudan SA, International Flavors & Fragrances Inc., Lonza Group AG, Syngenta AG, Encapsys LLC, Microtek Laboratories Inc., Cabot Corporation, NanoViricides Inc., Nanobiotix SA, Nanoform Finland Plc, Lubrizol Corporation (Particle Sciences), Roquette Freres SA, Ashland Inc., Adare Pharmaceuticals Inc., Solvay SA, Thermo Fisher Scientific Inc., Southwest Research Institute (SwRI). |

Frequently Asked Questions

The Nanocapsules Market is primarily driven by increasing demand for targeted drug delivery in oncology, rising adoption in nutraceuticals and cosmetics, and growing investment in nanotechnology-based R&D across pharmaceutical and food industries.

The Nanocapsules Market was valued at USD 3.75 billion in 2025 and is projected to reach USD 5.92 billion by 2035, growing at a CAGR of 4.68%.

The Nanocapsules Market is expanding across healthcare, food & nutraceuticals, and cosmetics, with healthcare leading due to strong adoption in drug delivery systems, while nutraceuticals show the fastest growth.

The Nanocapsules Market faces challenges such as high manufacturing complexity, scalability issues, and the need for advanced GMP-compliant production infrastructure, which can limit widespread commercialization.

The Nanocapsules Market is dominated by North America, holding approximately 38.42% market share in 2025, driven by strong pharmaceutical R&D and regulatory support.

Get in Touch