Minimal Residual Disease Testing Market Report Scope & Overview:

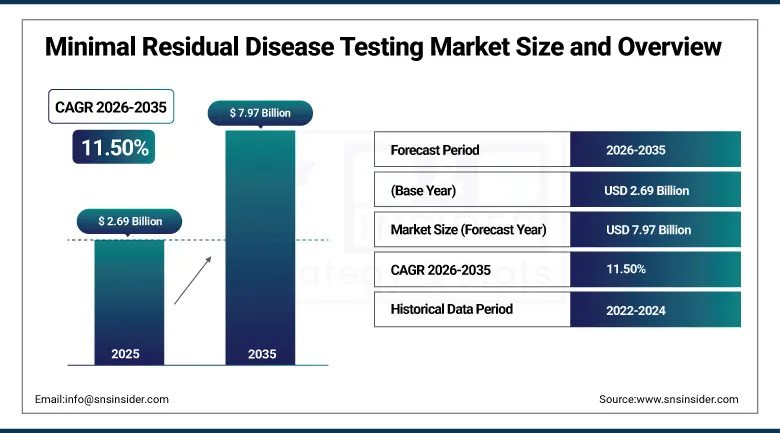

The Minimal Residual Disease Testing Market was valued at USD 2.69 Billion in 2025 and is expected to reach USD 7.97 Billion by 2035, growing at a CAGR of 11.50% from 2026 to 2035.

There is a noticeable trend of robust growth in the global market for minimal residual disease testing. Minimal residual disease testing is used for identifying microscopic quantities of residual cancer cells present in the body post-treatment for oncologists and hematologists to have an understanding of prognosis of the patient. MRD is now being identified as a surrogate endpoint for clinical trials of multiple myeloma, acute lymphoblastic leukemia, and chronic lymphocytic leukemia, making for integration of regulation and clinical guidelines that foster structured procurement within the institutions. The growth of is driven by rising incidence of cancer, MRD assay clearances by FDA, and rising use of circulating tumor DNA detection via liquid biopsy for MRD testing.

In June 2024, Adaptive Biotechnologies received an FDA Breakthrough Device Designation for their clonoSEQ MRD test to monitor patients with multiple myeloma in blood, representing a significant regulatory milestone that validates non-invasive blood-based MRD monitoring as an alternative to serial bone marrow biopsy for myeloma surveillance. This designation accelerates the commercial pathway for blood-based clonoSEQ deployment, creating above-average adoption momentum in multiple myeloma treatment centers whose current reliance on bone marrow aspirates creates procedural burden that blood-based monitoring eliminates.

Market Size and Forecast

-

Market Size in 2026E: USD 3.00 Billion

-

Market Size by 2035: USD 7.97 Billion

-

CAGR: 11.50% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Minimal Residual Disease Testing Market - Request Free Sample Report

Minimal Residual Disease Testing Market Trends

-

Liquid biopsy-based MRD testing is expanding as circulating tumor DNA analysis enables non-invasive disease monitoring and reduces dependence on bone marrow biopsies.

-

Next-generation sequencing is improving MRD detection sensitivity, enabling earlier identification of disease recurrence and deeper remission assessment.

-

MRD is increasingly being adopted as a regulatory and clinical trial endpoint, accelerating its use in oncology drug development.

-

Standardized multi-parameter flow cytometry protocols are improving MRD testing consistency and comparability across clinical laboratories.

-

MRD testing is expanding beyond hematological cancers into solid tumors through advanced circulating tumor DNA–based assays.

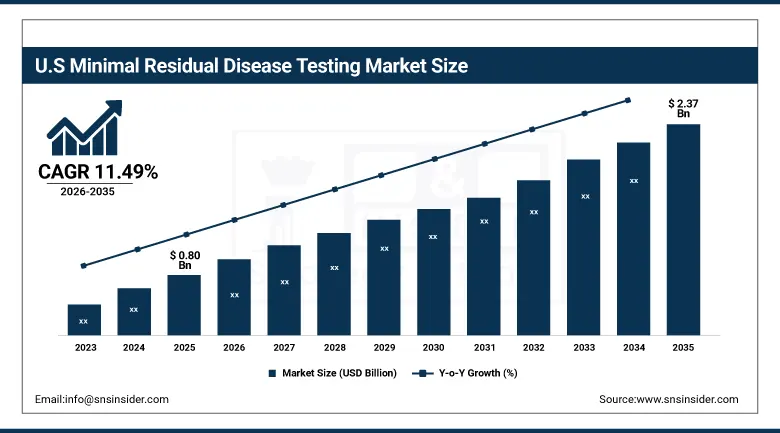

The U.S. Minimal Residual Disease Testing Market Outlook

The U.S. Minimal Residual Disease Testing Market was valued at approximately USD 0.80 Billion in 2025 and is expected to reach approximately USD 2.37 Billion by 2035, growing at a CAGR of approximately 11.49%.

The U.S. is the world's most commercially significant MRD testing market within North America's dominant regional position. Adaptive Biotechnologies, Natera, Guardant Health, NeoGenomics, Invivoscribe, Labcorp, and Foundation Medicine collectively define the domestic MRD testing commercial landscape across flow cytometry, PCR, and NGS technology platforms. FDA-cleared assays including Adaptive Biotechnologies’ clonoSEQ for multiple myeloma, ALL, and CLL have established reimbursement frameworks that sustain structured institutional procurement. The U.S. healthcare system's growing emphasis on precision oncology, increasing clinical trial activity incorporating MRD endpoints, and the extraordinary scale of hematology practice creating above-average per-capita MRD testing volumes collectively sustain U.S. market leadership.

In September 2023, Guardant Health announced that Geisinger Health Plan began offering coverage for the Guardant Reveal MRD test, a blood test detecting circulating tumor DNA after treatment including surgery, helping oncologists identify cancer patients with residual disease who may benefit from additional treatment. This coverage decision represents a landmark reimbursement milestone for ctDNA-based MRD testing in solid tumors, demonstrating the commercial pathway for private payer coverage of liquid biopsy MRD tests that sustains physician ordering adoption beyond the clinical trial setting.

Minimal Residual Disease Testing Market Segment Analysis

-

By Product, the assay kits & reagents segment dominated the minimal residual disease testing market with approximately 68% share in 2025, while the assay kits & reagents segment is also the fastest growing.

-

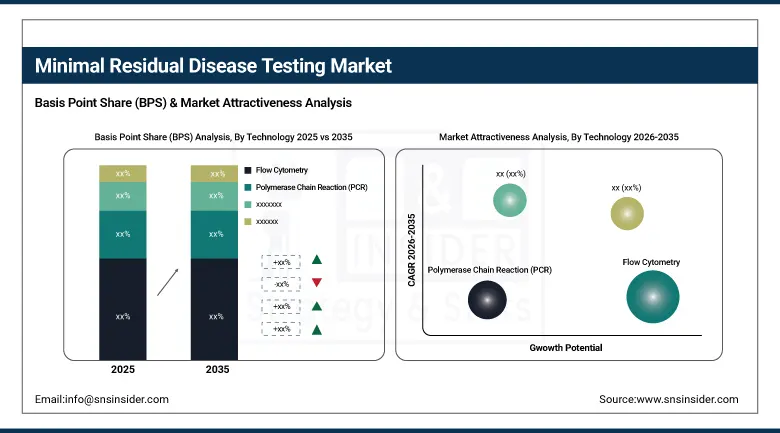

By Technology, the flow cytometry segment dominated the minimal residual disease testing market with approximately 40% share in 2025, while the next-generation sequencing segment is the fastest growing.

-

By Cancer Type, the hematological malignancies segment dominated the minimal residual disease testing market with approximately 68% share in 2025, while the solid tumors segment is the fastest growing.

-

By End Use, the hospitals and specialty clinics segment dominated the minimal residual disease testing market with approximately 45% share in 2025, while the diagnostic laboratories segment is the fastest growing.

By Technology, flow cytometry dominates, NGS grows fastest

Flow cytometry retained the dominant technology position with approximately 40% of the MRD testing market in 2025. The technology's commercial primacy reflects its decades of validated clinical application in haematological malignancy MRD detection, whose standardized multiparameter protocols enable identification of leukemia and lymphoma residual cells among 100,000 bone marrow or peripheral blood cells with results available within 24 hours. Flow cytometry's broad availability in hospital and reference laboratory settings, its lower cost relative to NGS alternatives, and its ability to deliver actionable clinical results without bioinformatics infrastructure requirements that complex molecular methods necessitate collectively sustain its dominant procurement position across clinical oncology settings globally.

NGS is the fastest growing technology because its exceptional sensitivity at one in a million cells, ability to track personalized patient-specific clonal sequences through clonoSEQ-style immune repertoire profiling, and expanding FDA approval and clinical guideline recognition create above-average adoption growth in the most clinically demanding MRD monitoring contexts. Each pharmaceutical clinical trial that specifies NGS-based MRD endpoint assessment creates laboratory procurement that sustains NGS platform installation at academic medical centers whose trial participation motivates technology investment beyond what routine clinical volume alone would justify.

By Cancer Type, hematological malignancies dominate, solid tumors grow fastest

Hematological malignancies retained the dominant cancer type position with approximately 68% of the MRD testing market in 2025. Blood cancers’ commercial dominance reflects the historically earlier and more comprehensive clinical validation of MRD testing in leukemia, lymphoma, and multiple myeloma, where clear molecular targets, established MRD detection methodologies, and clinical trial evidence supporting MRD-guided treatment adaptation have created integrated clinical guideline recommendations. The International Myeloma Working Group's consensus on MRD as a primary treatment endpoint in multiple myeloma, NCCN guidelines incorporating MRD assessment in ALL management, and EMA and FDA's recognition of MRD as a surrogate endpoint in drug approvals collectively create regulatory-driven clinical adoption that sustains haematological malignancy’s market dominance.

Solid tumors are the fastest growing cancer type because the convergence of liquid biopsy technology maturation, FDA clearance for ctDNA-based solid tumor MRD assays, and growing private payer reimbursement creates structured commercial adoption in colorectal, breast, lung, and bladder cancer oncology practice. The solid tumor addressable patient population substantially exceeds haematological malignancy volumes, creating a market expansion opportunity whose full commercial realization requires continued clinical validation and reimbursement coverage expansion. NeoGenomics’ RaDaR assay tracking 48 tumor-specific genetic variants for ctDNA-based MRD detection and Natera’s Signatera test's growing adoption across multiple solid tumor types demonstrate the commercial momentum sustaining solid tumor MRD testing growth.

By End Use, hospitals dominate, diagnostic labs grow fastest

Hospitals and specialty clinics retained the dominant business model position with approximately 45% of the MRD testing market in 2025. Hospital hematology and oncology departments’ direct patient access, integration with treatment workflows that connect MRD results to chemotherapy administration decisions, and availability of specialized hematology laboratory infrastructure create the most commercially concentrated and clinically integrated MRD testing procurement. Each comprehensive cancer centers whose MRD testing laboratory maintains flow cytometry, PCR, and NGS capabilities for serial patient monitoring creates high-volume institutional procurement relationships with test kit and reagent suppliers. Academic medical centers’ simultaneous roles as MRD technology developers, clinical trial sites, and patient treatment facilities create procurement that compounds across research and clinical channels.

Diagnostic laboratories are the fastest growing business model because the centralized scale economies of NGS-based MRD testing, whose high capital cost for sequencing equipment and bioinformatics infrastructure creates per-test cost structures that individual hospital laboratories cannot match at lower volume, creates procurement from hospitals outsourcing complex molecular MRD testing to specialist reference laboratories. Quest Diagnostics’ and Labcorp’s national reference laboratory networks, whose combined sequencing capacity creates NGS per-test economics below individual hospital programme costs, create structured send-out MRD testing relationships whose commercial aggregate grows with clinical adoption.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

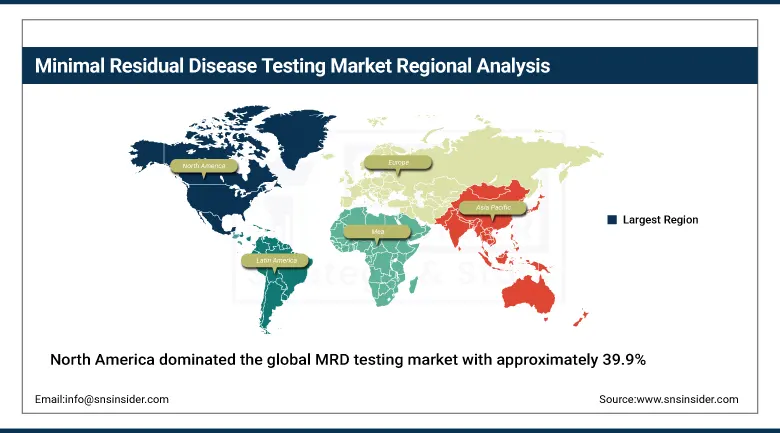

North America Minimal Residual Disease Testing Market Insights

North America dominated the global MRD testing market with approximately 39.9% of revenues in 2025, fueled by the prevalence of hematologic malignancies, robust reimbursement structures, and the presence of major market players including Adaptive Biotechnologies, Natera, and Invitae. The United States accounts for approximately 87.4% of North American revenues through these commercial operations combined with Guardant Health, NeoGenomics, and Labcorp’s clinical MRD testing services.

Canada contributes approximately 12.6% of North American revenues through its national hematology programme's MRD testing adoption, academic medical center laboratory networks, and growing clinical trial participation that incorporates MRD endpoint assessment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Minimal Residual Disease Testing Market Insights

Europe is a technically sophisticated MRD testing market where the EuroFlow consortium's standardized multiparameter flow cytometry protocols, European Medicines Agency’s MRD endpoint recognition in hematology drug approvals, and the established academic hematology research network create consistent institutional demand. Germany accounts for approximately 22.3% of European revenues through its academic hospital laboratory network, pharmaceutical industry's MRD clinical trial investment, and the comprehensive hematology center programme.

The United Kingdom, France, and the Netherlands are significant secondary markets where NHS hematology programme MRD monitoring, Institut Gustave Roussy's oncology research, and Erasmus MC’s EuroFlow network participation create consistent procurement. Roche Diagnostics’ European operations and Sysmex's regional distribution sustain market supply.

Asia Pacific Minimal Residual Disease Testing Market Insights

Asia Pacific minimal residual disease testing market is projected to grow at a CAGR of approximately 14.2% during 2026–2035, making it the fastest-growing regional market, driven by China's oncology precision medicine investment, India's growing reference laboratory infrastructure, Japan's advanced hematology diagnostic adoption, and South Korea's genomics innovation. China accounts for approximately 44.8% of Asia Pacific revenues through strategic alliances between Western diagnostic companies and domestic oncology research centers, and the rapid buildout of clinical genomics laboratory capacity.

India represents the most commercially dynamic emerging market within Asia Pacific where growing reference laboratory networks including Metropolis Healthcare and Dr Lal PathLabs, expanding hematology oncology practice, and government investment in cancer diagnostics create above-average MRD testing market growth.

MEA & Latin America Minimal Residual Disease Testing Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through King Faisal Specialist Hospital's hematology programme, Vision 2030's oncology diagnostics investment, and the growing adoption of NGS-based molecular testing. The UAE's specialist cancer center network adds complementary Gulf demand.

Brazil leads Latin American revenues at approximately 44.2% through Fleury and DASA's molecular laboratory networks, the growing haemato-oncology practice, and the expanding clinical trial ecosystem. Argentina's hematology research institutes and Mexico's cancer center infrastructure collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Precision oncology adoption and MRD assay commercialization

The precision oncology paradigm's systematic integration of MRD testing into treatment response assessment protocols is the MRD testing market's most commercially impactful structural growth driver. Each haematological malignancy treatment guideline update that incorporates MRD status as a treatment decision parameter creates physician ordering behavior change whose clinical adoption compounds across the global hematology and oncology practice base. The FDA's recognition of MRD as a reasonably likely surrogate endpoint in multiple myeloma and ALL drug approvals creates an extraordinary commercial multiplier effect, where each new drug approved with MRD-based efficacy evidence creates both direct clinical trial testing procurement and sustained post-approval real-world MRD monitoring adoption in the drug's commercial indication.

FDA-cleared MRD assay commercialization, particularly Adaptive Biotechnologies’ clonoSEQ’s clearance across multiple myeloma, ALL, and CLL indications, creates reimbursement pathway establishment that sustains commercial adoption beyond early adopter academic medical centers into community hematology and oncology practices whose Medicare reimbursement coverage creates procurement motivation for previously uncompensated MRD testing.

Restraints: High test cost and reimbursement uncertainty limiting routine clinical adoption

High MRD test cost, particularly for NGS-based deep sequencing approaches whose laboratory processing cost of USD 1,000 to over USD 3,000 per test creates patient co-pay and payer coverage barriers, moderates routine serial monitoring adoption in community practice settings whose reimbursement coverage remains incomplete. Each insurance denial for non-emergency MRD monitoring creates clinical friction that moderates the frequency of serial MRD assessment in the community oncology practice setting where patient volume substantially exceeds academic medical center equivalents.

Standardization challenges between flow cytometry, PCR, and NGS platforms across different laboratories create interlaboratory comparability limitations that complicate serial monitoring when patients transfer between healthcare systems using different MRD testing methodologies. Each patient whose treatment monitoring requires platform-consistent serial MRD assessment across multiple testing laboratories creates a result interpretation challenge that moderates clinical confidence in monitoring programme design.

Opportunities: Solid tumor ctDNA MRD expansion and MRD-guided adaptive therapy trials

Solid tumor circulating tumor DNA-based MRD testing expansion represents the most commercially significant near-term market opportunity whose addressable patient population in colorectal, breast, lung, and bladder cancer substantially exceeds the haematological malignancy market whose MRD testing is already well-established. Each solid tumor indication that achieves FDA clearance for a ctDNA MRD test and private payer coverage creates a structured procurement channel whose patient population scale creates above-average revenue growth.

MRD-guided adaptive therapy trials represent the most commercially innovative near-term clinical development opportunity whose MRD-positive patient escalation and MRD-negative patient de-escalation trial designs create above-average per-trial MRD testing volume that sustains above-average revenue per enrolled patient. Each MRD-guided de-escalation trial that validates treatment reduction based on MRD negativity creates a clinical precedent that could substantially increase MRD testing frequency if adopted in standard clinical practice.

Recent Developments:

-

2026: Natera, Inc. expanded the clinical applications of its Signatera MRD assay with new evidence supporting personalized cancer monitoring across multiple solid tumors.

-

2025: Guardant Health, Inc. enhanced its Guardant Reveal MRD platform with expanded colorectal and breast cancer monitoring capabilities based on circulating tumor DNA analysis.

-

2025: Adaptive Biotechnologies Corporation introduced additional clonoSEQ MRD assay capabilities to support broader hematologic malignancy monitoring and clinical research applications.

-

2026: F. Hoffmann-La Roche Ltd. advanced its sequencing-based oncology diagnostics portfolio through expanded MRD testing solutions integrated with precision oncology workflows.

Minimal Residual Disease Testing Market key players are:

-

Adaptive Biotechnologies Corporation

-

Natera, Inc.

-

Guardant Health, Inc.

-

F. Hoffmann-La Roche Ltd.

-

Bio-Rad Laboratories, Inc.

-

Labcorp

-

NeoGenomics Laboratories, Inc.

-

Invivoscribe, Inc.

-

Foundation Medicine, Inc.

-

Sysmex Inostics GmbH

-

Veracyte, Inc.

-

Sebia SA

-

Illumina, Inc.

-

Becton, Dickinson and Company

-

Personalis, Inc.

-

Exact Sciences Corporation

-

Quest Diagnostics Incorporated

-

QIAGEN N.V.

-

ArcherDX, Inc. (Invitae)

-

Thermo Fisher Scientific Inc.

Minimal Residual Disease Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.69 Billion |

| Market Size by 2035 | USD 7.97 Billion |

| CAGR | CAGR of 11.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Assay Kits & Reagents, Instruments) • By Technology (Flow Cytometry, Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Others) • By Cancer Type (Hematological Malignancies, Solid Tumors, Multiple Myeloma, Others) • By End Use (Hospitals and Specialty Clinics, Diagnostic Laboratories, Academic and Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Adaptive Biotechnologies Corporation, Natera, Inc., Guardant Health, Inc., F. Hoffmann-La Roche Ltd., Bio-Rad Laboratories, Inc., Labcorp, NeoGenomics Laboratories, Inc., Invivoscribe, Inc., Foundation Medicine, Inc., Sysmex Inostics GmbH, Veracyte, Inc., Sebia SA, Illumina, Inc., Becton, Dickinson and Company, Personalis, Inc., Exact Sciences Corporation, Quest Diagnostics Incorporated, QIAGEN N.V., ArcherDX, Inc. (Invitae), Thermo Fisher Scientific Inc. |

Frequently Asked Questions

Flow Cytometry dominated with approximately 40% share in 2025.

North America dominated with approximately 39.9% of revenues in 2025.

Precision oncology integration of MRD status into haematological malignancy treatment guidelines creating structured clinical adoption.

The market was valued at USD 2.69 Billion in 2025.

The market is expected to grow at a CAGR of 11.50% from 2026 to 2035.

Get in Touch