Liquid Biopsy Market Report Scope & Overview:

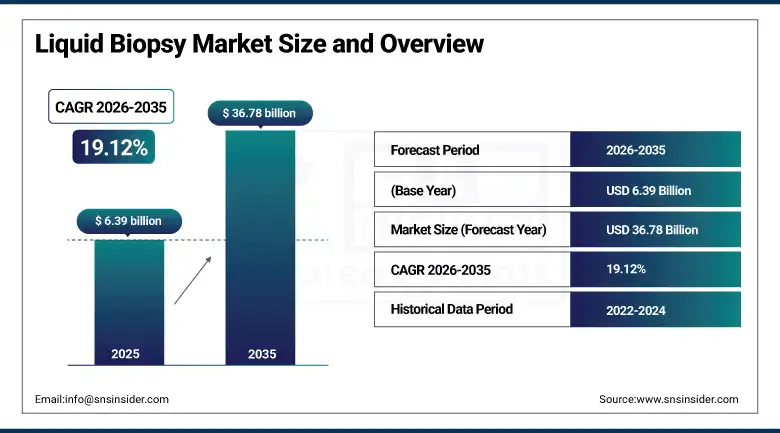

The Liquid Biopsy Market was valued at USD 6.39 Billion in 2025 and is expected to reach USD 36.78 Billion by 2035, growing at a CAGR of 19.12% from 2026–2035.

The global liquid biopsy market is growing at an exceptional pace. Liquid biopsy detects cancer and other diseases through analysis of circulating biomarkers in blood or urine. It eliminates the need for invasive surgical tissue biopsy. The technology analyses circulating tumour DNA, circulating tumour cells, and exosomes to detect cancer presence, guide treatment selection, monitor therapy response, and identify acquired resistance mutations. Over 2 million new cancer cases will be reported in the U.S. in 2025 alone. Traditional tissue biopsy cannot be repeated frequently due to patient safety and cost constraints. Liquid biopsy enables serial sampling at diagnosis, during treatment, and at recurrence. FDA approvals for ctDNA-based companion diagnostics from Guardant Health and Foundation Medicine have validated the technology’s clinical utility and created reimbursement pathways that sustain commercial market expansion. Emerging applications in reproductive health, organ transplant monitoring, and early multi-cancer detection are creating new commercial categories.

In January 2025, Mayo Clinic Laboratories partnered with Lucence to broaden global access to Lucence’s LiquidHallmark liquid biopsy technology. This collaboration enables Mayo Clinic Laboratories to offer Lucence’s solutions to international markets. The partnership reflects the commercial strategy of distributing validated liquid biopsy tests through established laboratory network infrastructure rather than building independent commercial distribution, accelerating global patient access and revenue generation simultaneously.

Liquid Biopsy Market Size and Forecast

-

Market Size in 2026E: USD 7.61 Billion

-

Market Size by 2035: USD 36.78 Billion

-

CAGR: 19.12% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Liquid Biopsy Market - Request Free Sample Report

Liquid Biopsy Market Trends

-

Multi-cancer early detection assays are emerging as the most commercially transformative liquid biopsy application, with GRAIL’s Galleri test demonstrating the ability to screen for 50+ cancer types from a single blood draw.

-

AI-driven bioinformatics platforms are improving ctDNA signal detection sensitivity below 0.1% variant allele frequency, enabling earlier cancer detection before clinical symptoms develop.

-

FDA companion diagnostic approvals for ctDNA-guided targeted therapy selection are creating clinically validated and reimbursed liquid biopsy applications that drive routine adoption in oncology practice.

-

Minimal residual disease monitoring through ctDNA is replacing imaging-based surveillance in certain cancer types, providing more sensitive detection of molecular relapse weeks before radiological evidence appears.

-

Reproductive health applications including non-invasive prenatal testing and preimplantation genetic testing are expanding the liquid biopsy addressable market beyond oncology into obstetrics and fertility medicine.

U.S. Liquid Biopsy Market Outlook

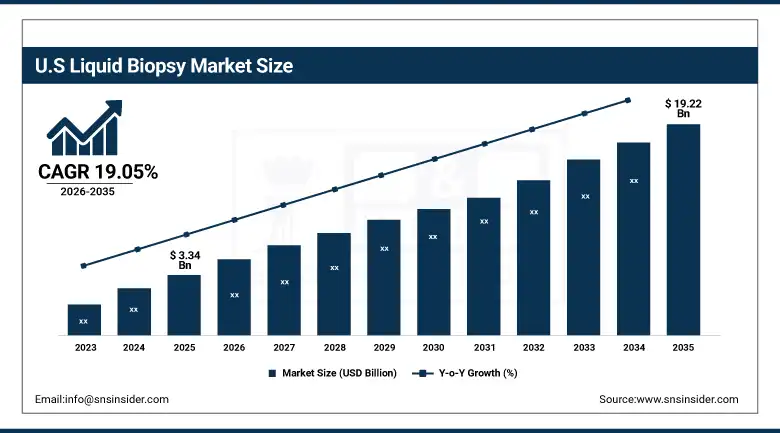

The U.S. Liquid Biopsy Market was valued at approximately USD 3.34 Billion in 2025 and is expected to reach approximately USD 19.22 Billion by 2035, growing at a CAGR of approximately 19.05%.

The U.S. is the world’s largest and most commercially advanced liquid biopsy market. More than 2 million new cancer cases are diagnosed annually. FDA approval of Guardant360 CDx and FoundationOne Liquid CDx as companion diagnostics created the reimbursement foundation for routine oncology use. CMS coverage decisions for liquid biopsy are expanding the covered patient population. Research funding from NCI and NIH is advancing early detection and MRD monitoring applications. The commercial ecosystem includes established diagnostics companies, pure-play liquid biopsy companies, and major laboratory networks including Quest Diagnostics and Labcorp whose testing volumes sustain market scale.

In January 2025, Oxford Cancer Analytics secured USD 11 million in Series A funding to advance early lung cancer detection using liquid biopsy proteomics. Dr. Heinrich Roder, a lung cancer proteomics specialist, was appointed SVP of Research and Development at OXcan. The investment reflects the growing commercial interest in expanding liquid biopsy beyond ctDNA toward multi-analyte approaches that improve sensitivity and specificity for the most prevalent cancer types.

Liquid Biopsy Market Segment Analysis

-

By Biomarker, the Circulating Tumour DNA segment dominated the Liquid Biopsy Market in 2025 as the most clinically validated, commercially deployed, and FDA-approved biomarker for cancer detection, treatment selection, and residual disease monitoring across multiple tumour types, while the Exosomes/Microvesicles segment is the fastest growing as their rich protein and RNA cargo provides complementary biological information beyond ctDNA mutation analysis.

-

By Technology, the PCR-Based segment dominated the Liquid Biopsy Market in 2025 as the most widely deployed clinical laboratory technology for ctDNA analysis through droplet digital PCR and quantitative PCR platforms, while Next-Generation Sequencing is the fastest growing as decreasing sequencing costs and multi-gene panel capability make NGS-based comprehensive genomic profiling increasingly routine in oncology practice.

-

By Application, the Cancer segment dominated the Liquid Biopsy Market with 86.46% share in 2025 as the foundational and most commercially validated application spanning diagnosis, treatment selection, response monitoring, and recurrence surveillance, while the Reproductive Health segment is the fastest growing with a CAGR of 12.82% as NIPT adoption expands and preimplantation genetic testing grows with ART procedure volumes globally.

-

By End User, the Hospitals & Laboratories segment dominated the Liquid Biopsy Market with 42.38% share in 2025 as the primary setting for clinical liquid biopsy testing where patient access, insurance reimbursement, and clinical workflow integration converge, while Research Institutes are growing fastest as academic oncology and genomics research programmes drive technology development and clinical validation studies.

By Biomarker, ctDNA dominates, exosomes grow fastest

Circulating tumour DNA retained the dominant biomarker position in the liquid biopsy market in 2025. ctDNA’s clinical validation spans a decade of research demonstrating its correlation with tumour burden, genetic heterogeneity, and treatment response. FDA-approved companion diagnostics from Guardant Health and Foundation Medicine validate ctDNA’s clinical utility for companion diagnostic applications in NSCLC, colorectal cancer, and solid tumours. Insurance reimbursement for approved ctDNA tests creates the commercial infrastructure that sustains routine clinical adoption. ctDNA’s shedding characteristics directly reflect active tumour DNA release, making it the most directly actionable biomarker for clinical decision-making.

Exosomes and extracellular vesicles are the fastest-growing biomarker because their molecular cargo encompasses proteins, RNA, and lipids that provide complementary cancer biology information beyond ctDNA point mutations. Exosome analysis can identify cancer types where ctDNA shedding is low, such as brain tumours and certain breast cancer subtypes, expanding liquid biopsy clinical utility to tumour types poorly served by ctDNA approaches. Commercial exosome isolation and analysis platform development is accelerating as companies including Exosome Diagnostics and Veracyte invest in standardised clinical-grade exosome processing workflows.

By Application, cancer dominates, reproductive health grows fastest

Cancer retained the dominant application position with 86.46% of the liquid biopsy market in 2025. Oncology is where liquid biopsy’s non-invasive advantage is most clinically compelling. Tissue biopsy in solid tumours requires surgical procedures with complication risk, sampling limitations, and impossibility of repeat access to track tumour evolution. Liquid biopsy provides real-time, repeatable molecular profiling that enables treatment decision-making at diagnosis, resistance monitoring during therapy, and early relapse detection after treatment completion. Each of these clinical use cases represents a separately reimbursable test with distinct commercial value, creating a multi-touchpoint revenue model across the oncology patient journey.

Reproductive health is the fastest-growing application at a CAGR of 12.82% because non-invasive prenatal testing has become standard of care in many markets and preimplantation genetic testing adoption is growing with IVF procedure volumes. NIPT analyses cell-free foetal DNA in maternal blood to detect chromosomal abnormalities. The technology is clinically superior to invasive amniocentesis for screening purposes and is progressively expanding its application from trisomy detection toward broader genetic screening panels. Each new clinical indication added to NIPT panels creates incremental test volume per pregnancy.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Liquid Biopsy Market Insights

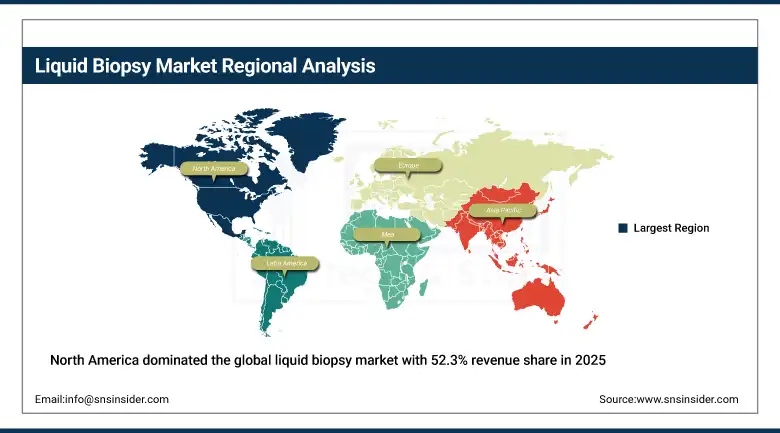

North America dominated the global liquid biopsy market with 52.3% revenue share in 2025. The U.S. accounts for approximately 87.4% of North American revenues. FDA approval infrastructure, Medicare reimbursement frameworks, and the world’s most intensive cancer research ecosystem create the commercial conditions for liquid biopsy market leadership. Guardant Health, GRAIL, Foundation Medicine, and Natera are all headquartered in the U.S. and collectively define the commercial frontier of liquid biopsy technology and clinical applications.

Canada contributes approximately 12.6% of North American revenues through publicly funded cancer programmes that are progressively incorporating liquid biopsy into standard oncology practice, provincial health technology assessment processes that evaluate new liquid biopsy tests, and research funding through CIHR that supports clinical validation studies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Liquid Biopsy Market Insights

Europe is a significant liquid biopsy market where the EU’s In Vitro Diagnostic Regulation creates a rigorous performance evaluation pathway for commercial liquid biopsy tests, national health system reimbursement decisions determine clinical adoption scale, and active academic oncology research programmes generate clinical evidence that supports market development. Germany accounts for approximately 22.3% of European revenues through its oncology clinical research infrastructure, private laboratory market, and G-BA health technology assessment process.

The United Kingdom’s NHS Genomics Medicine Service and Cancer Research UK’s translational research investment are creating structured clinical adoption pathways for liquid biopsy. France’s national cancer strategy includes liquid biopsy within precision oncology infrastructure investment. These institutional programmes create predictable commercial market development that sustains European market growth independently of private payer dynamics.

Asia Pacific Liquid Biopsy Market Insights

Asia Pacific is the fastest-growing regional liquid biopsy market. China accounts for approximately 44.8% of Asia Pacific revenues through its high cancer incidence, growing private oncology sector, and active domestic liquid biopsy company development. Chinese companies including Berry Genomics and Burning Rock Genomics are developing ctDNA platforms for the domestic market. Japan’s precision medicine initiative and South Korea’s advanced molecular diagnostics sector represent sophisticated secondary markets with above-average adoption.

India represents a commercially significant emerging market where rising cancer incidence, growing awareness of early detection’s survival benefit, and expanding private hospital oncology investment are creating first-time liquid biopsy demand. Mayo Clinic Laboratories’ partnership with Lucence specifically targets Asia Pacific market access through established laboratory network distribution infrastructure.

MEA & Latin America Liquid Biopsy Market Insights

The Middle East and Africa and Latin America are growing liquid biopsy markets where high cancer incidence, improving healthcare infrastructure, and growing awareness of non-invasive diagnostics are creating commercial demand. UAE leads MEA revenues at approximately 38.4% through its advanced private oncology sector in Dubai and Abu Dhabi, international patient medical tourism, and above-average consumer health investment that sustains premium diagnostic test adoption.

Brazil leads Latin American revenues at approximately 44.2% through its large oncology patient population, active cancer research institutions, and growing private health insurance sector whose oncology benefit coverage is progressively including molecular diagnostics as standard.

Growth Drivers: Rising cancer incidence creating clinical demand, FDA approvals creating reimbursement pathways, and multi-cancer early detection commercially validating the technology’s screening potential

Rising global cancer incidence is the liquid biopsy market’s most structurally reliable growth driver. Over 20 million new cancer cases are diagnosed globally each year. This burden is growing with ageing populations and lifestyle factors in developing economies. Every new cancer patient represents a potential liquid biopsy test recipient across multiple clinical decision points in their treatment journey. The compounding of cancer incidence growth with the progressive expansion of reimbursed indications creates a multiplicative revenue growth dynamic.

FDA companion diagnostic approvals and Medicare reimbursement decisions have fundamentally changed liquid biopsy’s commercial standing. Before FDA approval, liquid biopsy was an experimental test with limited payer coverage. FDA-approved companion diagnostic status converts liquid biopsy from an elective test into a medically necessary diagnostic whose reimbursement is contractually required by insurance plans that cover approved molecular oncology treatments. Each new FDA companion diagnostic approval creates a new reimbursed clinical use case whose patient volume scales with the paired therapy’s prescription volume.

Restraints: Limited standardisation across platforms reducing clinical interchangeability, high test cost limiting developing market adoption, and analytical sensitivity challenges for early-stage cancer detection

Analytical and pre-analytical standardisation gaps limit liquid biopsy’s clinical interchangeability. Different ctDNA platforms use different variant calling algorithms, sensitivity thresholds, and quality metrics that produce non-comparable results. A result from Guardant360 cannot be directly compared to one from Foundation One Liquid CDx. This lack of interoperability limits the efficiency of multi-site clinical trials, impedes reference range standardisation, and creates quality assurance complexity for clinical laboratories implementing multiple platforms.

Analytical sensitivity remains challenging for early-stage cancer detection where ctDNA shedding rates are extremely low. Stage I solid tumours shed ctDNA at variant allele frequencies below 0.01% in many cases. Current sequencing error rates make reliable detection at these levels technically demanding and expensive. The multi-cancer early detection commercial opportunity depends on solving this sensitivity challenge at a cost that health systems and patients can afford.

Opportunities: Multi-cancer early detection screening market, MRD monitoring expanding post-treatment surveillance, and transplant rejection monitoring creating new clinical applications

Multi-cancer early detection represents liquid biopsy’s most commercially transformative emerging application. GRAIL’s Galleri test has demonstrated the ability to detect over 50 cancer types from a single blood draw before clinical symptoms appear. If proven to reduce cancer mortality at population scale, multi-cancer early detection could become a routine annual screening test for adults over 50. The addressable market would encompass hundreds of millions of annual tests globally, creating a commercial opportunity that substantially exceeds the current oncology monitoring market.

Organ transplant monitoring is an emerging application whose clinical validation is progressing rapidly. Donor-derived cell-free DNA in recipient blood provides an early, sensitive indicator of graft rejection that precedes biopsy-detectable pathology. Earlier rejection detection enables preventive intervention that improves transplant survival rates. Each solid organ transplant recipient represents a potential recurring liquid biopsy customer across the life of the transplant. CareDx and Natera are leading commercial development in this high-value recurring application category.

Recent Developments:

-

2025: Mayo Clinic Laboratories partnered with Lucence in January 2025 to broaden global access to LiquidHallmark liquid biopsy technology, enabling international market distribution through Mayo’s established laboratory network and demonstrating the commercial strategy of partnering validated liquid biopsy technology with global laboratory distribution infrastructure.

-

2025: Oxford Cancer Analytics secured USD 11 million in Series A funding in January 2025 to advance early lung cancer detection using proteomics-based liquid biopsy, appointing Dr. Heinrich Roder as SVP of R&D and representing investor confidence in multi-analyte approaches that expand beyond ctDNA to improve sensitivity and specificity.

-

2024: GRAIL continued commercial expansion of its Galleri multi-cancer early detection test in 2024, expanding employer benefit programme partnerships and direct-to-consumer access, validating the commercial model for population-level cancer screening through liquid biopsy at pricing accessible to self-pay and employer-funded health benefit channels.

Liquid Biopsy Market Key Players

-

Illumina

-

Thermo Fisher Scientific

-

GRAIL

-

QIAGEN

-

Bio-Rad Laboratories

-

Myriad Genetics

-

Foundation Medicine

-

Lucence Health

-

Oxford Cancer Analytics

-

Burning Rock Genomics

-

Berry Genomics

-

Veracyte

-

Labcorp Holdings

-

Quest Diagnostics

-

Exact Sciences

-

Personalis

-

Freenome

Liquid Biopsy Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.39 Billion |

| Market Size by 2035 | USD 36.78 Billion |

| CAGR | CAGR of 19.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Biomarker (Circulating Tumour DNA, Circulating Tumour Cells, Exosomes/Extracellular Vesicles, Others) • By Technology (PCR-Based, NGS, Digital PCR, Others) • By Application (Cancer, Reproductive Health, Transplantation, Others) • By End User (Hospitals & Laboratories, Research Institutes, Pharmaceutical & Biotech Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Guardant Health, Inc., F. Hoffmann-La Roche Ltd., Illumina, Inc., QIAGEN N.V., Exact Sciences Corporation, Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., Natera, Inc., NeoGenomics, Inc., Myriad Genetics, Inc., PERSONALS, Inc., Freenome Holdings, Inc., GRAIL, LLC, Angle plc, Menarini Silicon Biosystems S.p.A., Biocept, Inc., Burning Rock Biotech Limited, Adaptive Biotechnologies Corporation, Sysmex Corporation, and MDxHealth SA |

Frequently Asked Questions

The Liquid Biopsy Market is expected to grow at a CAGR of 19.12% from 2026 to 2035.

The Liquid Biopsy Market was valued at USD 6.39 Billion in 2025.

Rising global cancer incidence creating clinical demand across diagnosis, treatment selection, monitoring, and recurrence surveillance, FDA companion diagnostic approvals creating insurance reimbursement pathways that sustain routine clinical adoption, and multi-cancer early detection technology commercially validating liquid biopsy’s population screening potential.

Cancer dominated the Liquid Biopsy Market with 86.46% share in 2025.

North America dominated the Liquid Biopsy Market in 2025 with 52.3% revenue share, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch