Digital PCR Market Report Scope & Overview:

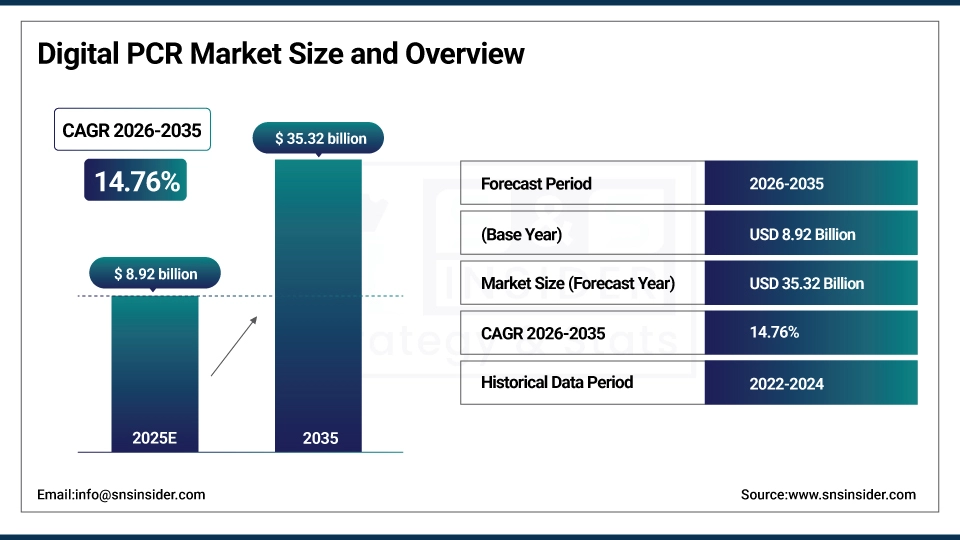

The Digital PCR Market size is estimated at USD 8.92 billion in 2025 and is expected to reach USD 35.32 billion by 2035, growing at a CAGR of 14.76% over the forecast period of 2026-2035.

The global digital PCR market trend is a growing demand for precision molecular diagnostics solutions such as droplet digital PCR systems, absolute quantification platforms, and next-generation sequencing validation tools. The growth of the market is driven by increasing cancer prevalence, rising infectious disease outbreaks, and pharmaceutical industry investment in companion diagnostics development. This trend is also driven by a growing adoption of liquid biopsy technologies and the growing focus on personalized medicine as research institutions become more focused on achieving single-molecule detection sensitivity and are more willing to invest in advanced nucleic acid amplification technologies, resulting in growth in the domestic and international market for chip-based and droplet-based digital PCR platforms.

For instance, in March 2024, growing awareness and improved molecular diagnostic infrastructure drove a 28% increase in digital PCR system installations for clinical laboratories globally, boosting rare mutation detection and copy number variation analysis capabilities.

Digital PCR Market Size and Forecast:

-

Market Size in 2025: USD 8.92 billion

-

Market Size by 2035: USD 35.32 billion

-

CAGR: 14.76% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Digital PCR Market - Request Free Sample Report

Digital PCR Market Trends

-

Digital PCR solutions are being adopted because researchers demand absolute quantification capabilities, rare mutation detection, and high-precision gene expression analysis.

-

Customized digital PCR assays based on cancer types, pathogen detection requirements, and genetic variation profiling to improve diagnostic accuracy outcomes.

-

The development of AI-powered data analysis software, multiplex assay capabilities, and automated partition generation to improve the workflow efficiency and reduce hands-on time burden.

-

Microfluidic chip technology, nanoliter droplet generation, and high-throughput screening platforms are all available to ensure precise nucleic acid quantification and single-cell analysis.

-

Increased demand for portable digital PCR systems, point-of-care diagnostic solutions and cloud-based data management to help field testing and remote analysis capabilities.

-

Collaboration between diagnostic companies, pharmaceutical manufacturers and academic institutions to develop validated digital PCR workflows and improve standardization protocols.

-

FDA, EMA and ISO promoting standards for assay validation, quality control requirements, clinical laboratory improvement amendments, and companion diagnostic approval pathways.

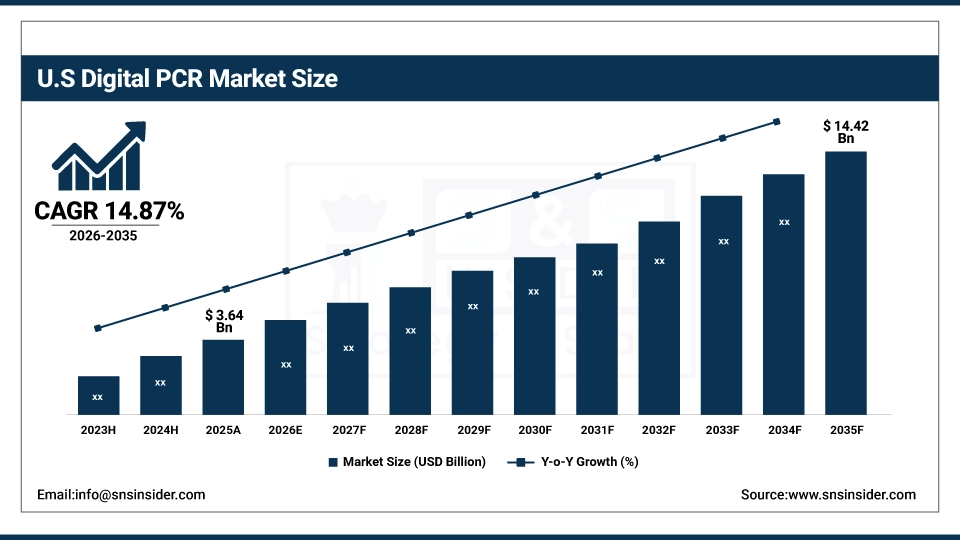

The U.S. Digital PCR Market is estimated at USD 3.64 billion in 2025 and is expected to reach USD 14.42 billion by 2035, growing at a CAGR of 14.87% from 2026-2035. The United States represents the largest market for digital PCR, primarily driven by the extensive cancer research funding, advanced molecular diagnostic infrastructure, and well-developed precision medicine initiatives. Government grants, high levels of biotechnology investment, and increased spending on genomics research from academic institutions and pharmaceutical companies help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of droplet-based and chip-based digital PCR platforms.

Digital PCR Market Growth Drivers:

-

Rising Cancer Prevalence and Precision Oncology Demand is Driving the Digital PCR Market Growth

Rising cancer prevalence and precision oncology demand take the center stage as a growth driver for the digital PCR market share, and are driven by the implementation of liquid biopsy testing, circulating tumor DNA monitoring, and minimal residual disease detection for enhanced treatment response assessment and early relapse identification. These solutions for personalized cancer management and targeted therapy selection are driving the base of the market, the penetration of clinical & research markets, and adding to the overall market share globally.

For instance, in June 2024, oncology-focused and liquid biopsy applications accounted for ~58% of the total global digital PCR market revenue, reflecting growing clinical adoption and expanding market share.

Digital PCR Market Restraints:

-

High Equipment Costs and Technical Complexity are Hampering the Digital PCR Market Growth

High equipment costs & technical complexity of digital PCR systems also restrict the digital PCR market growth, as a large number of small research laboratories and diagnostic centers face difficulties affording capital-intensive instrumentation and maintaining specialized technical expertise. This might lead to limited market penetration, restricted adoption in resource-constrained settings, and reduced accessibility for emerging research institutions. As a result, diagnostic innovation suffers, and market growth is stunted in regions where laboratory budgets are limited and trained molecular biology professionals are scarce.

Digital PCR Market Opportunities:

-

Emerging Infectious Disease Surveillance and Environmental Monitoring Drive Future Growth Opportunities for the Digital PCR Market

The opportunity in the emerging infectious disease surveillance and environmental monitoring in digital PCR market is in the form of rapid pathogen detection, water quality testing, and food safety verification applications. These solutions provide for early outbreak identification, antimicrobial resistance tracking, and microbial contamination assessment. Through enhanced public health protection, agricultural biosecurity, and ecosystem monitoring, particularly in areas with emerging zoonotic disease threats, these technologies may improve response times, decrease disease transmission, and expand the market.

For instance, in April 2024, global health organizations reported that 71% of molecular diagnostic laboratories adopted digital PCR for infectious disease quantification, highlighting rising platform utilization and increasing demand for sensitive pathogen detection tools.

Digital PCR Market Segment Analysis

-

By product, consumables & reagents held the largest share of around 62.47% in 2025E, and the instruments segment is expected to register the highest growth with a CAGR of 15.34%.

-

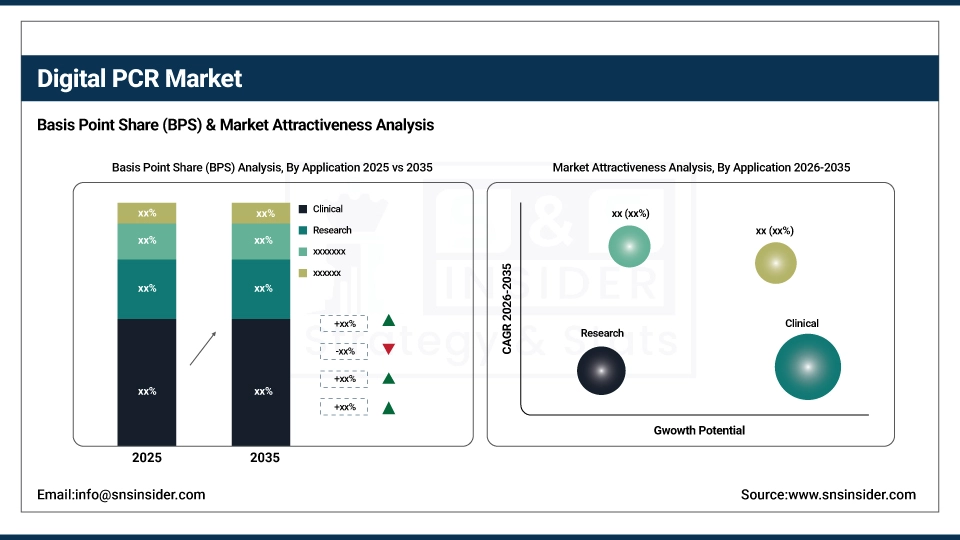

By application, the clinical segment dominated the market with approximately 56.82% share in 2025E, while the research is expected to register the highest growth with a CAGR of 15.12%.

-

By indication, oncology accounted for the leading share of nearly 48.96% in 2025E, and is expected to register the highest growth with a CAGR of 15.23%.

By Application, the Clinical Segment dominates, while the Research Segment Shows Rapid Growth

By 2025, the clinical segment contributed the largest revenue share of 56.82% due to increasing cancer diagnostic testing, infectious disease monitoring requirements and companion diagnostic development activities. Growing adoption of precision medicine protocols coupled with reimbursement policy expansion, healthcare providers are increasingly implementing digital PCR for patient stratification. The research segment is projected to grow at the highest CAGR of about 15.12% between 2026 and 2035 due to the growing need for single-cell genomics studies and gene editing validation applications. Some of the reasons include better funding for basic research programs, better accessibility to digital PCR technology in academic institutions, and biotechnology companies' preference for absolute quantification methods in drug discovery.

By Product, Consumables & Reagents Lead the Market, While Instruments Registers Fastest Growth

The consumables & reagents segment accounted for the highest revenue share of approximately 62.47% in 2025, owing to recurring purchase requirements, continuous assay optimization needs, and expanding test volumes across clinical and research laboratories. Emerging trends, including increasing adoption of pre-validated assay kits and growing demand for multiplex reagent systems. In comparison, the instruments segment is anticipated to achieve the highest CAGR of nearly 15.34% during the 2026–2035 period, driven by the technological advancements in droplet generation systems, laboratory automation integration, and declining instrument pricing strategies. Drivers include rising establishment of molecular diagnostic centers, the preference for high-throughput platforms in pharmaceutical development.

By Indication, Oncology Lead, and Registers Fastest Growth

The oncology segment accounted for the largest share of the digital PCR market with about 48.96%, owing to extensive liquid biopsy applications, circulating tumor DNA analysis requirements, and investment capacity for molecular profiling infrastructure. Reasons driving the oncology segment include increasing personalized cancer therapy adoption and tumor mutation burden assessment needs. In addition, it is slated to grow at the fastest rate with a CAGR of around 15.23% throughout the forecast period of 2026–2035, as oncology research centers, pharmaceutical companies, and diagnostic laboratories seek comprehensive mutation detection platforms, minimal residual disease monitoring capabilities, and treatment response prediction tools. Increased focus on early cancer detection and targeted therapy optimization contribute to their adoption, while improved patient survival rates and reduced healthcare costs drive continued investment.

Digital PCR Market Regional Highlights:

North America Digital PCR Market Insights:

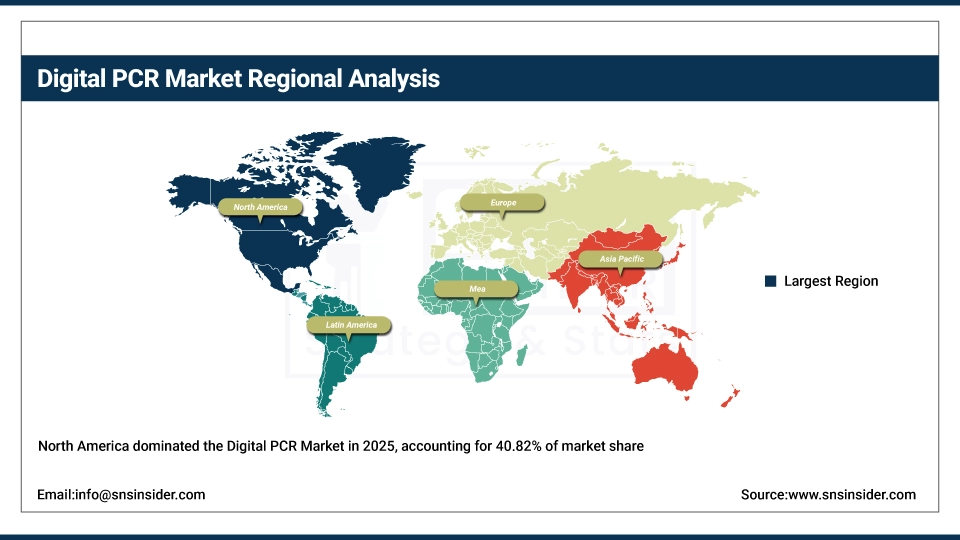

North America held the largest revenue share of over 40.82% in 2025 of the digital PCR market due to an established molecular diagnostics industry, extensive cancer research funding, and increased biotechnology sector awareness regarding the advantages of absolute quantification. Drivers include ubiquitous use of liquid biopsy testing, an advanced laboratory automation environment, growing precision medicine adoption and greater acceptance of companion diagnostics stemming from personalized therapy needs. At the same time, various government research grants, National Cancer Institute initiatives and enormous investments in genomics technology from pharmaceutical manufacturers and academic institutions are anchoring digital PCR platforms and services in the market, and ensuring multibillion dollar revenues around the world.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Digital PCR Market Insights:

Asia Pacific is the fastest-growing segment in the digital PCR market with a CAGR of 16.84%, as the awareness about precision diagnostics, government biotechnology investment initiatives, and research infrastructure modernization in developing nations is growing. Factors including rapid pharmaceutical industry expansion, rising contract research organization establishment with molecular testing capabilities, and growing adoption of international quality standards are stimulating the market growth. Academic institution strengthening and genomics program implementation have been instrumental in improving molecular diagnostic capabilities, especially in countries with emerging biotechnology sectors. Public health surveillance programs and infectious disease monitoring also help in advancing nucleic acid testing and pathogen detection systems. Increase in demand in Asia Pacific region owing to rising healthcare research expenditure against historical spending levels and growing affordability and accessibility of digital PCR instrumentation.

Europe Digital PCR Market Insights:

The digital PCR market in Europe is the second-dominating region after North America on account of an increase in the adoption of molecular diagnostic technologies, robust healthcare quality standards including CE-IVD regulations, and increasing research excellence initiatives across academic systems. Rising implementation of national genomics programs, advanced translational medicine infrastructure, favorable European Union funding for biotechnology projects, and cross-border research collaboration frameworks are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Digital PCR Market Insights:

In Latin America, and Middle East & Africa, the growing molecular diagnostics infrastructure development and increase in infectious disease surveillance priorities with clinical laboratory modernization support the digital PCR market growth. The rising popularity of accessible digital PCR training programs and regional technology transfer initiatives, along with international diagnostic company presence, will aid research capacity building and diagnostic accessibility. The increasing healthcare investment and improving regulatory framework capabilities in these regions are continuing to encourage market growth.

Digital PCR Market Competitive Landscape:

Bio-Rad Laboratories, Inc. (est. 1952) is a leading life science research and clinical diagnostics company that focuses on innovative molecular biology solutions for precision measurement applications. It uses its pioneering droplet digital PCR technology and extensive assay development expertise to produce cutting-edge quantification platforms with seamless laboratory workflow integration.

-

In February 2025, it expanded its QX600 Droplet Digital PCR System capabilities with enhanced automation features and increased throughput capacity, aiming to improve clinical laboratory efficiency and research productivity across its global user network.

Thermo Fisher Scientific Inc. (est. 1956) is a well-known global biotechnology company focused on analytical instruments, laboratory equipment, and life sciences solutions. It invests in advanced digital PCR platforms and comprehensive reagent portfolios with the hopes of revolutionizing molecular diagnostics with accurate, reproducible, and scalable nucleic acid quantification tools.

-

In May 2024, launched an enhanced QuantStudio Absolute Q Digital PCR System featuring real-time partition monitoring and integrated sample preparation modules across global research markets, enhancing workflow simplicity, data quality, and experimental reproducibility.

QIAGEN N.V. (est. 1984) is a leading molecular diagnostics and sample preparation technology provider in the fields of nucleic acid purification, PCR assays, and companion diagnostic development. The company's digital PCR product portfolio focuses on user-friendly nanoplate technology and validated assay solutions, and features a strong commitment to quality standards and continuous innovation to complement the strong market presence in both clinical and research settings.

-

In September 2024, introduced advanced QIAcuity digital PCR analytics software and expanded oncology assay portfolio for its nanoplate platform, strengthening liquid biopsy capabilities and expanding adoption among precision medicine laboratories.

Digital PCR Market Key Players:

-

Bio-Rad Laboratories, Inc.

-

Thermo Fisher Scientific Inc.

-

QIAGEN N.V.

-

F. Hoffmann-La Roche Ltd.

-

Agilent Technologies, Inc.

-

Illumina, Inc.

-

Standard BioTools Inc.

-

Stilla Technologies

-

JN Medsys

-

Combinati

-

Formulatrix

-

Qiagen Manchester Ltd.

-

PerkinElmer, Inc.

-

Sysmex Corporation

-

Biomérieux SA

-

RainDance Technologies

-

Eppendorf AG

-

Danaher Corporation

-

Takara Bio Inc.

-

Biomerieux Inc.

| Report Attributes | Details |

|---|---|

|

Market Size in 2025 |

USD 8.92 Billion |

|

Market Size by 2035 |

USD 35.32 Billion |

|

CAGR |

CAGR of 14.76% from 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2035 |

|

Historical Data |

2022–2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

•By Product (Consumables & Reagents, Instruments, Software & Services) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Bio-Rad Laboratories Inc., Thermo Fisher Scientific Inc., QIAGEN N.V., F. Hoffmann-La Roche Ltd., Agilent Technologies Inc., Illumina Inc., Standard BioTools Inc., Stilla Technologies, JN Medsys, Combinati, Formulatrix, Qiagen Manchester Ltd., PerkinElmer Inc., Sysmex Corporation, Biomérieux SA, RainDance Technologies, Eppendorf AG, Danaher Corporation, Takara Bio Inc., Biomerieux Inc. |

Frequently Asked Questions

Ans: The Digital PCR Market is expected to grow at a CAGR of 14.76% over the forecast period.

Ans: The Digital PCR Market size was USD 8.92 billion in 2025 and is expected to reach USD 35.32 billion by 2035.

Ans: Rising Cancer Prevalence and Precision Oncology Demand is Driving the Digital PCR Market Growth.

Ans: By product, the Consumables & Reagents segment dominated the Digital PCR Market in 2025.

Ans: North America dominated the Digital PCR Market in 2025.

Get in Touch