NUT midline carcinoma treatment Market Report Scope & Overview:

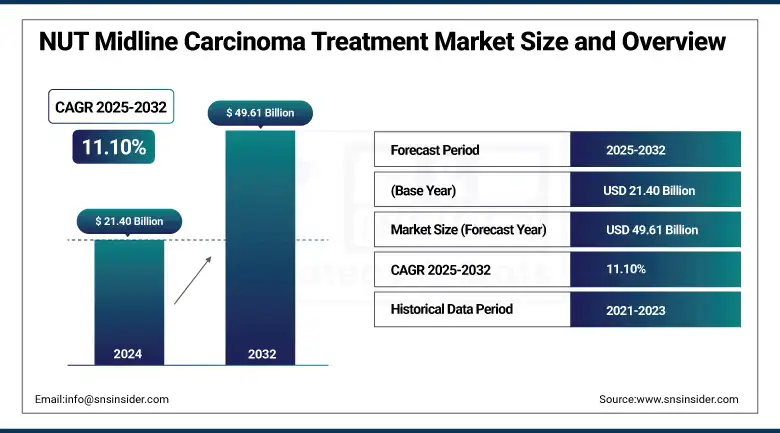

NUT midline carcinoma treatment market size was valued at USD 21.40 billion in 2024 and is expected to reach USD 49.61 billion by 2032, growing at a CAGR of 11.10% over the forecast period 2025-2032.

The NUT midline carcinoma treatment market is undergoing rapid transformation, driven by government-supported research, regulatory incentives, and precision oncology breakthroughs. The NUT midline carcinoma (NMC) treatment market is growing rapidly due to the poor prognosis of the disease.

To Get more information On NUT Midline Carcinoma Treatment Market - Request Free Sample Report

For instance, just 30% of patients with NUT-midline carcinoma survive for two years, according to the National Cancer Institute (NCI); their average survival is about 10 months.

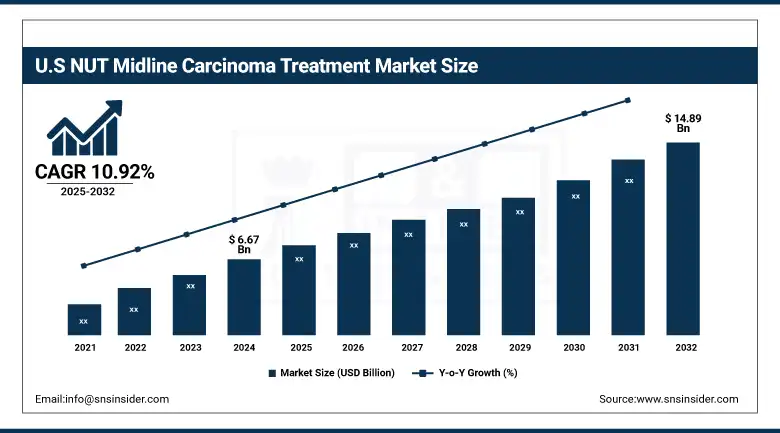

Due to its advanced diagnostics infrastructure, early adoption of next-generation sequencing, and strong clinical research ecosystem, the U.S. NUT midline carcinoma treatment market is expected to account for a major share and is valued at USD 6.67 billion in 2024 and expected to reach USD 14.89 billion by 2032 with a CAGR of 10.92% from 2025-2032.

Regulating authorities in the U.S. and Europe have assigned orphan disease status to NMC medicines, therefore rewarding NUT midline carcinoma treatment companies with tax benefits and market exclusiveness, and so promoting market expansion. These factors, taken combined with increasing investment in cancer research and collaboration efforts between biopharmaceutical companies and research institutions, constitute major drivers of NUT midline carcinoma treatment market expansion and innovation.

The global NUT midline carcinoma treatment market is characterized by increasing attention on early identification, precision medicine, and the development of new targeted drugs. Governments such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have encouraged uncommon cancer research by giving orphan drug designations and supporting accelerated approval processes for NMC treatments. Although insufficient testing and clinical awareness make the occurrence of NMC essentially unknown, the Dana-Farber Cancer Institute (October 2023) claims that around 500 cases are identified annually in the United States. Key NUT midline carcinoma treatment market trends show that more effective, customized treatment options are being enabled by improved early diagnosis made possible by advanced diagnostics, including molecular profiling and next-generation sequencing (NGS).

Market Dynamics:

Drivers

-

Expansion of Advanced Diagnostic Technologies and Early Detection Efforts by Government and Academic Institutions To Propel Market Growth

Due to government and academic programs, early detection and diagnosis rates for rare and severe malignancy NUT midline carcinoma (NMC) have especially improved. Although inadequate testing and clinical awareness mean that the true frequency is yet unclear, the National Cancer Institute (NCI) estimates that 500 persons in the United States are diagnosed with NUT midline carcinoma (NMC) annually.

Supported by government-funded research and public health campaigns, the combination of contemporary diagnostic methods, including next-generation sequencing (NGS) and genetic profiling, has increased the capacity to diagnose NMC at earlier periods.

For instance, in a 2024 National Library of Medicine study of 362 head and neck carcinoma patients, NUT carcinoma accounted for 2.9% of poorly differentiated and 12.5% of undifferentiated cases, therefore highlighting the need for better diagnosis tools.

Starting proper treatment in a disease known for fast advancement and poor prognosis depends on more precise and quick diagnosis arising from government-supported innovations. The European Medicines Agency (EMA) has encouraged the development of new therapies for NMC utilizing orphan drug designations and accelerated approval processes, hence further promoting inventiveness and access to new medicines. These combined efforts by regulatory bodies and research centers are directly enhancing patient identification, early intervention, and a more stable treatment environment for NUT midline cancer.

Restraints

-

Limited Clinical Awareness and Testing Infrastructure Compromises Accuracy in Diagnosis and Timely Treatment

Despite progress in diagnostic technologies, limited clinical awareness and inadequate testing infrastructure continue to significantly restrict the effective management of NUT midline carcinoma. The Dana-Farber Cancer Institute noted in an October 2023 report that the real frequency of NMC is still largely unknown, mostly because of insufficient diagnostic tools and a lack of clinical awareness among healthcare professionals. NUTM1 fusion testing is only performed regularly by a small percentage of American community oncology facilities; this discrepancy is even more clear in poor areas where access to next-generation sequencing and specialized immunohistochemistry panels is restricted. Misdiagnosis rates remain high; many instances fall under either other poorly differentiated or undifferentiated carcinomas.

The National Cancer Institute (NCI) emphasizes even more the vital need for early detection and treatment since the average survival for NMC patients is roughly 10 months and with a two-year survival rate of roughly 30%. Moreover, a 2024 study by University Hospital Tuebingen, which was published by the National Library of Medicine, evaluated 35 adult NMC patients from five European countries and found that most cases included thoracic tumors; diagnosis was often delayed due to limited awareness and testing capability. These continuous challenges highlight the vital need to extend clinical education, standardize diagnostic techniques, and fund testing infrastructure to ensure that patients have the right and timely treatment.

Segmentation Analysis:

By Treatment

Chemotherapy remains the cornerstone of NUT midline carcinoma treatment, accounting for the largest revenue share of 33% in 2024. Its established use as a first-line treatment for aggressive tumors, as NMC, particularly in cases of fast intervention needed, helps explain its predominance. Governmental and academic studies, including the National Library of Medicine publications (December 2023) and the Indian Council of Medical Research (ICMR) corroborate that, including five recently recorded cases in India, chemotherapy is the first treatment used in most diagnosed cases. The endorsement of the U.S. FDA and EMA for chemotherapy regimens as standard-of-care confirms their significance in the global NUT midline carcinoma treatment market analysis.

Targeted therapy is the fastest-growing segment driven by the expanding attention on tailored medicine and the creation of novel drugs such as BET (bromodomain and extra-terminal) inhibitors. These treatments especially target NMC's BRD4-NUT fusion protein, a feature of clinical trials and market release of these agents are hastening under the direction of regulatory incentives such as orphan drug status and accelerated approval from the FDA and EMA.

For instance, a BET inhibitor, Bristol-Myers Squibb's Trotabresib (CC-90010), entered Phase I studies in June 2024, therefore significantly changing the trends in NUT midline carcinoma treatment markets.

A multi-country European study released in March 2024, assessing 35 adult NMC patients and underlining the rising importance of targeted therapy, shows how the EMA's orphan medicine status and fast-track approvals have resulted in higher investment and research in this market.

By Route of Administration

Intravenous (IV) administration accounted for the largest NUT midline carcinoma treatment market share of 67% in 2024, reflecting its position as the usual delivery mode for both chemotherapy and many targeted therapies. The main places of treatment for NMC are hospitals and oncology centers ready for sophisticated IV regimens.

For instance, A study conducted at University Hospital Tuebingen (2016–2023), published by the National Library of Medicine in March 2024, found that 54% of 35 European NMC patients had thoracic tumors and received IV-administered treatments, underscoring the real-world dominance of this route.

Driven by the development of oral targeted treatments and patient inclination for less invasive treatment choices, the oral segment is expected to achieve the highest CAGR. Greater convenience, outpatient management, and better adherence are made possible by oral administration in particular. Companies such as Bristol-Myers Squibb are moving oral BET inhibitors through clinical studies; regulatory authorities including the EMA have accelerated the registration of oral medications. With oral treatments gaining traction as novel agents prove safe and effective, these trends are projected to change the global NUT midline carcinoma therapy market.

By End Use

Hospitals held the largest NUT midline carcinoma treatment market share of around 65% in 2024, reflecting their major importance in providing sophisticated cancer treatment, diagnostics, and interdisciplinary treatment for NMC. The hospitals are the primary site for NUT midline carcinoma treatment since they have sophisticated IV regimens, advanced molecular profiling, and management of aggressive disease presentations ready for them.

Specialty clinics are expected to have the greatest CAGR, driven by the move toward outpatient care and the growing availability of oral targeted treatments. These offices provide targeted knowledge, individualized treatment programs, and simplified access to new treatments. This development is being driven by government regulations endorsing outpatient oncology services and insurance reimbursement for specialized clinic treatment. Specialty clinics are a major point for NUT midline carcinoma treatment market expansion since they are positioned to provide individualized, effective therapy.

Regional Analysis

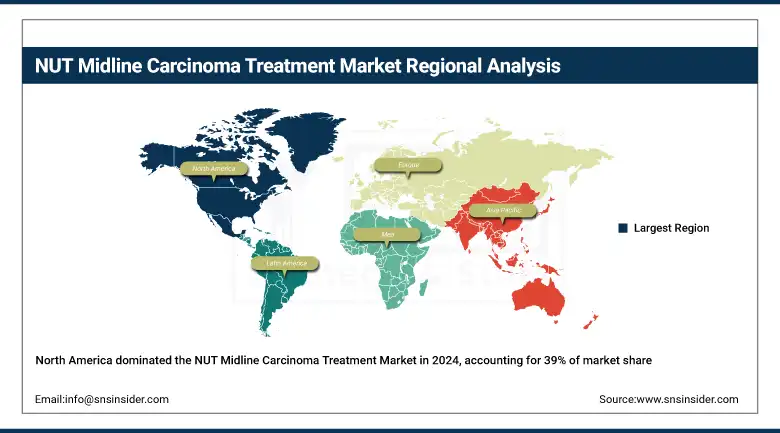

The North America region dominated and held the global NUT midline carcinoma treatment market share of 39% in 2024. Advanced healthcare infrastructure, large investments in rare cancer research, and a great degree of clinical knowledge fuel this leadership. Strong government and corporate financing for oncology research help the United States; early adoption of sophisticated diagnostics, including molecular profiling and next-generation sequencing (NGS), also advantages it. Given the aggressive character of NUT midline carcinoma (NMC), these elements enable early and more accurate detection of the illness.

Get Customized Report as per Your Business Requirement - Enquiry Now

Furthermore, NMC medicines have been given orphan illness designation by the U.S. Food and Drug Administration (FDA), which provides incentives meant to boost pharmaceutical research and hasten the approval of new treatments. With about 500 new NMC cases reported annually in the U.S., the Dana-Farber Cancer Institute estimates that joint efforts between research facilities and biopharmaceutical businesses strengthen the leadership in the area even more.

Europe held a significant share of the global NUT midline carcinoma treatment market, with nations including Germany, the UK, France, Italy, and Spain leading the way. Strong regulatory frameworks, especially the European Medicines Agency's (EMA) orphan drug designations and accelerated approval paths for rare cancer treatments, help to boost the region's NUT midline carcinoma treatment market growth. The NUT midline carcinoma treatment market analysis notes leading nation in this region is Germany, which reflects its commitment to rare cancer research as well as its sophisticated healthcare system. Cooperative research projects, including a multi-country review released in March 2024, show Europe's emphasis on early detection and cross-border clinical trials, qualities vital for a rare disease with small patient pools.

The Asia-Pacific region is emerging as the fastest-growing market for NUT midline carcinoma treatment, with China and India leading the expansion. Reflecting fast improvements in healthcare infrastructure, more investment in cancer research, and rising involvement in international clinical trials, China is expected to attain a stunning CAGR. Driven by government-supported research projects and greater clinical awareness, India's market is likewise fast-growing. Early detection and more efficient treatment of NMC in the region are made possible by the increasing acceptance of sophisticated diagnostic technologies and the increased attention on individualized care. Despite these advances, Asia-Pacific faces challenges related to limited awareness, access disparities, and the need for more specialized expertise in rare cancers.

While holding a smaller share, LAMEA (Latin America, Middle East, and Africa) is progressing with government-led awareness efforts and upgraded cancer treatment facilities. These initiatives are progressively improving diagnosis capacity and access to innovative therapies.

Key Players

The key NUT midline carcinoma treatment companies are Pfizer Inc., C4 Therapeutics, Inc., Novartis International AG, Merck & Co. Inc, F. Hoffmann-La Roche Ltd, Incyte Corporation, Johnson & Johnson, Bristol-Myers Squibb Company, Ipsen Biopharmaceuticals, Inc, GSK plc, Takeda Pharmaceutical Company Limited, Zenas BioPharma, and others.

Recent Developments

-

Targeting NMC and other uncommon malignancies, Bristol-Myers Squibb launched Phase I clinical trials for Trotabresib (CC-90010), an oral BET inhibitor, in June 2024. Government publications and formal clinical trial registries brought this to underlined attention.

-

Emphasizing the need for early detection and cooperative research in rare tumors, the National Library of Medicine released a European study of 35 adult NMC patients in March 2024.

-

The Dana-Farber Cancer Institute revised U.S. NMC prevalence figures in October 2023, verifying over 500 new cases yearly and underlining the necessity of better diagnosis and treatment plans.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 21.40 Billion |

| Market Size by 2032 | USD 49.61 Billion |

| CAGR | CAGR of 11.10% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment (Chemotherapy, Radiation Therapy, Targeted Therapy, Immunotherapy, and Others) • By Route Of Administration (Oral, Intravenous (IV), and Other) • By End Use (Hospitals, Specialty Clinics, and Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Pfizer Inc., C4 Therapeutics, Inc., Novartis International AG, Merck & Co. Inc, F. Hoffmann-La Roche Ltd, Incyte Corporation, Johnson & Johnson, Bristol-Myers Squibb Company, Ipsen Biopharmaceuticals, Inc, GSK plc, Takeda Pharmaceutical Company Limited, Zenas BioPharma, and others |

Get in Touch