Fitness Apps Market Report Scope & Overview:

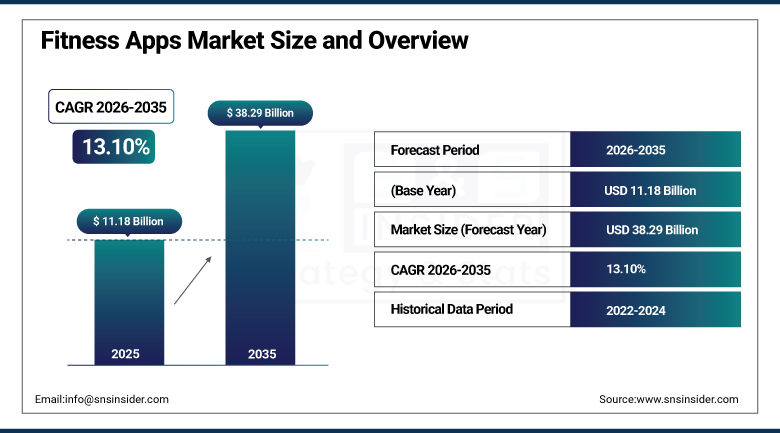

The Fitness Apps Market was valued at USD 11.18 Billion in 2025 and is expected to reach USD 38.29 Billion by 2035, growing at a CAGR of 13.10% from 2026 to 2035.

The Fitness Apps Market continues to expand as growing health consciousness, technological advancements, and favorable economic factors including rising disposable income converge with the widespread penetration of smartphones and tablets across all demographics. Prescription therapies built on semaglutide and tirzepatide are increasingly being stitched into leading fitness platforms, blending medication adherence tools with activity coaching in a way that is reshaping what a fitness app fundamentally does. As device processing shifts directly onto the wrist through native wearable operating systems, fitness apps continue evolving well beyond simple step counting toward comprehensive readiness and recovery scoring that aggregates sleep, activity, and heart-rate signals into single actionable metrics.

WeightWatchers began issuing GLP-1 prescriptions inside its app, funneling members to telehealth providers and streamlining home delivery, a strategic shift that blends medication adherence tools with the company's established activity coaching and weight management platform for members using prescription weight-loss therapies.

Market Size and Forecast

- Market Size in 2026E: USD 12.64 Billion

- Market Size by 2035: USD 38.29 Billion

- CAGR: 13.10% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information On Fitness Apps Market - Request Free Sample Report

Fitness Apps Market Trends

- Prescription therapies built on semaglutide and tirzepatide are increasingly integrated into leading fitness platforms.

- Native wearable operating systems are shifting processing directly onto the wrist, compounding smartwatch app engagement.

- Readiness and recovery scoring that aggregates sleep, activity, and heart-rate signals is becoming a standard app feature.

- AI-powered coaching continues improving user engagement and subscription retention across fitness app categories.

- Rising user concern about health data privacy is prompting demand for offline, on-device tracking alternatives.

The United States Fitness Apps Market Outlook

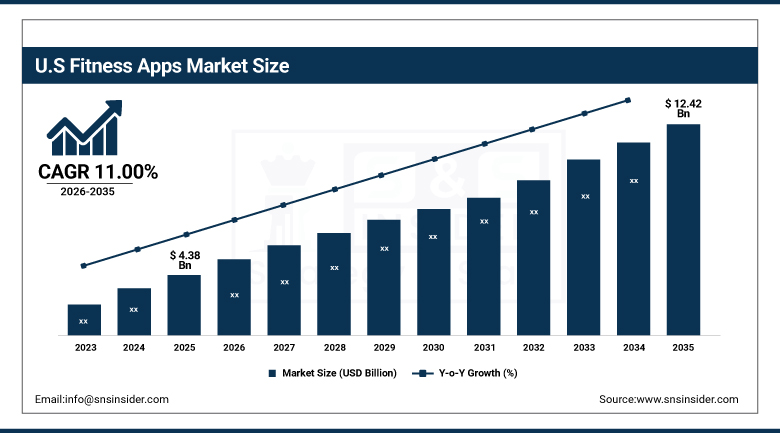

The United States Fitness Apps Market was valued at USD 4.38 Billion in 2025 and is expected to reach USD 12.42 Billion by 2035, growing at a CAGR of 11.00% from 2026 to 2035.

USA remained one of the front-running countries in the North American demand for fitness apps due to the change in consumers' health priorities and the growth in technology within the nation’s biggest pool of fitness apps developers. Awareness and interest in preventive medicine made people search for tools to maintain their fitness and health, a trend driven by increased smartphone ownership and internet availability that made the country remain the biggest national market for such technology.

Samsung introduced its Energy Score feature within its Galaxy ecosystem, aggregating sleep, activity, and heart-rate signals into a single readiness index designed to translate complex biometric data into one actionable metric for users managing their daily fitness and recovery routines.

Fitness Apps Market Segmentation Analysis

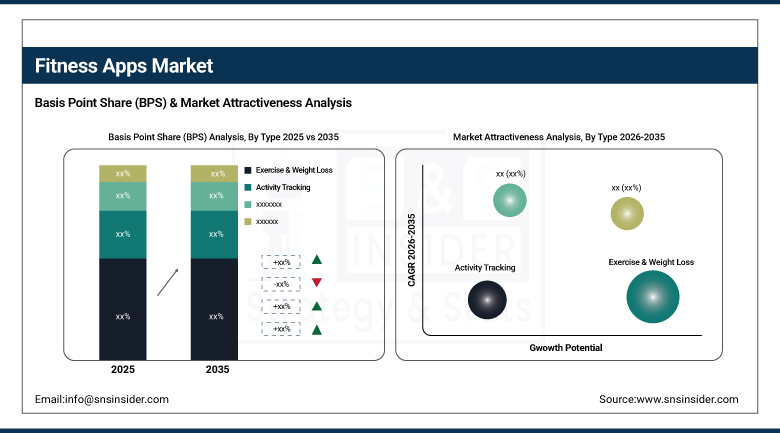

- By Type, the exercise weight loss segment held approximately 53.69% share in 2025, while the activity tracking segment is the fastest growing.

- By Platform, the iOS segment held approximately 51.99% share in 2025, while the android segment is the fastest growing.

- By Device, the smartphones segment held approximately 66.70% share in 2025, while the wearables segment is the fastest growing.

- By Payment Model, the freemium segment held approximately 41.10% share in 2025, while the subscription segment is the fastest growing.

By Type, exercise weight loss led the market, activity tracking grew fastest

The exercise weight loss segment dominated the type category in 2025, holding approximately 53.69% of total revenue, attributable to the increasing number of people seeking a health-conscious lifestyle and structured workout guidance. That sustained consumer demand for weight management and structured exercise programming keeps this type category firmly at the top of the broader type segmentation across nearly every major fitness app category worldwide.

The activity tracking segment is projected to grow at the fastest CAGR during the forecast period, as native wearable operating systems increasingly shift processing directly onto the wrist, compounding engagement for passive, continuous monitoring features. Rising consumer interest in comprehensive readiness and recovery metrics that aggregate sleep, activity, and heart-rate signals continues pushing this type category's growth rate ahead of the broader type segmentation.

By Platform, iOS led the market, android grew fastest

The iOS segment held the largest platform share in 2025, at approximately 51.99%, favored by a consumer base with historically higher fitness app spending and deeper integration with Apple's broader health and wellness ecosystem. That established ecosystem advantage continues keeping iOS the dominant platform choice across the majority of premium fitness app subscriptions worldwide.

The android segment, including native wearable operating system variants, is projected to grow at the fastest CAGR during the forecast period, as improved battery life thresholds continue turning multi-day wearable tracking into a practical reality for Android device owners. Rising smartphone and wearable penetration across price-sensitive emerging markets continues pushing Android platform adoption ahead of the broader platform segmentation.

By Device, smartphones led the market, wearables grew fastest

The smartphones segment held the largest device share in 2025, at approximately 66.70%, anchored by the universal ownership and constant accessibility that smartphones offer relative to any dedicated wearable device. That ubiquity keeps smartphones firmly at the top of the broader device segmentation across the majority of fitness app installations and daily usage sessions worldwide.

The wearables segment is projected to grow at the fastest CAGR during the forecast period, as smartwatches and fitness bands increasingly deliver passive, continuous monitoring capability that smartphone-only tracking cannot match. Rising integration of on-device processing and extended battery life continues pushing wearable device adoption ahead of the broader device segmentation.

By Payment Model, Freemium led the market, Subscription grew fastest

The freemium segment held the largest payment model share in 2025, at approximately 41.10%, favored for lowering the barrier to initial app adoption by letting users access basic functionality before committing to any payment. That low-friction onboarding continues keeping freemium the dominant payment model across the broader payment model segmentation for new user acquisition.

The subscription segment is projected to grow at the fastest CAGR during the forecast period, as fitness app developers increasingly convert free users into recurring subscribers through premium coaching, personalized programming, and integrated health data features. Rising subscription fatigue notwithstanding, well-differentiated premium tiers continue pushing this payment model's growth rate ahead of the broader payment model segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.90% |

|

Europe |

Germany |

27.40% |

|

Asia Pacific |

China |

36.30% |

|

Middle East & Africa |

UAE |

26.60% |

|

Latin America |

Brazil |

37.70% |

North America Fitness Apps Market Insights

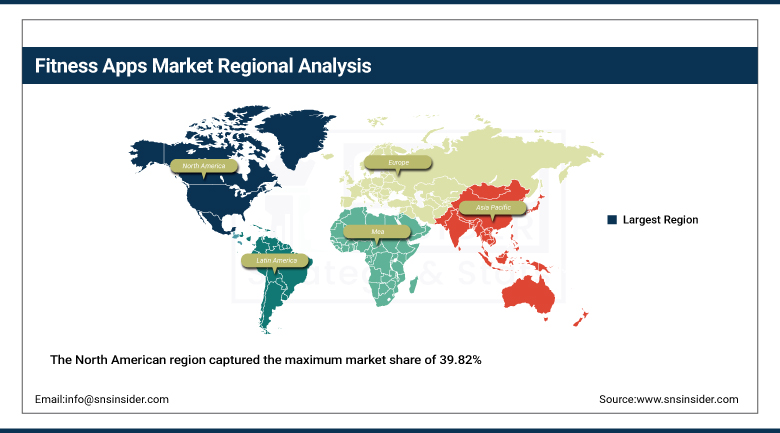

The North American region captured the maximum market share of 39.82% in the worldwide fitness applications market in 2025 due to its high number of smartphone users as well as the health awareness of the region. High disposable income and seamless integration with the premium ecosystem of wearables further strengthened this dominance.

The United States accounted for roughly 84.90% of regional revenue, reflecting its concentration of leading fitness app developers and high per-capita fitness technology spending. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding digital health and wellness adoption, keeping North America firmly ahead of every other region in this market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Fitness Apps Market Insights

In 2025, Europe represented a significant portion of the global market for fitness apps, owing to high awareness levels regarding fitness and health in addition to the adoption of fitness-connected technology among consumers in the region. Germany contributed about 27.40% to the region’s market revenue, driven by the presence of health-conscious consumers and high wearable technology penetration rates in the country.

Following the same trend were France, the United Kingdom, and the Nordic countries, owing to the adoption of digital wellness. Continued growth in employer wellness program adoption is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Fitness Apps Market Insights

Asia Pacific was the fastest-growing region in the global fitness apps market, driven by rapid urbanization and an increase in disposable income across the region's largest and most populous economies. India in particular continued driving regional fitness app growth as urbanization trends expanded the addressable consumer base for digital fitness technology.

The China region contributed approximately 36.30% of revenues to the region due to the rapid adoption of smartphones along with growing capabilities to develop fitness applications in that region. Japan and South Korea also played an important role by contributing to the regional demand via their advanced consumer electronic and wearable devices.

MEA & Latin America Fitness Apps Market Insights

The Middle East and Africa region recorded steady growth in fitness app adoption in 2025, driven by rising smartphone penetration and growing health consciousness across the Gulf states in particular. The UAE accounted for roughly 26.60% of regional revenue, supported by rising consumer demand for premium fitness and wellness technology.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.70% of regional revenue, where growing smartphone adoption and health awareness continued to support category growth. Mexico and Argentina followed a similar trajectory as regional digital fitness adoption expanded further through the remainder of the forecast period.

Growth Drivers: Health consciousness and wearable ecosystem integration

Increasing health awareness, technological advancements, and favorable economic factors including rising disposable income and lower healthcare costs continue to be the central force behind fitness apps market growth. The growing penetration of smartphones and tablets across all demographics has resulted in high adoption of fitness apps, with some apps offering customized services based on body physiology and individual requirements.

Prescription therapies built on semaglutide and tirzepatide being stitched into leading platforms continue blending medication adherence tools with activity coaching, opening genuinely new revenue and engagement models for fitness app developers. Native wearable operating systems shifting processing directly onto the wrist continue reinforcing structural demand growth across nearly every major fitness app category worldwide.

Restraints: Subscription fatigue and health data privacy concerns

Increasing user concern regarding privacy issues related to health and fitness information remains a significant barrier for wider fitness app usage, as a 2025 survey showed that most fitness app users were concerned about the use of their personal information, a significant increase from just a few years ago. This privacy issue keeps the popularity of offline tracking apps growing.

Subscription fatigue among consumers facing an increasingly crowded landscape of overlapping wellness app subscriptions continues creating genuine retention challenges for fitness app developers. That competitive saturation continues requiring app developers to demonstrate clear, differentiated value to justify recurring subscription costs against free or lower-cost alternatives.

Opportunities: GLP-1 integration and employer wellness program expansion

Growing integration of GLP-1 medication adherence tools into fitness app platforms presents substantial opportunity for developers positioned to serve the rapidly expanding population of prescription weight-loss therapy users. App developers capable of delivering genuinely useful medication tracking alongside traditional activity coaching stand to capture a growing share of demand from this expanding user base.

Expanding employer wellness program adoption presents a further significant growth avenue, as companies increasingly view fitness app subscriptions as a genuine employee benefit and healthcare cost-management tool. App developers capable of delivering enterprise-ready wellness platforms stand to capture meaningful new institutional revenue streams through 2035.

Recent Developments:

- 2025: Apple's watchOS 11 Vitals app began surfacing overnight heart rate variability and respiratory-rate deviations, nudging users toward preventive health behaviors without requiring phone intervention.

- 2025: Google's Wear OS 5 improved battery life by twenty percent, a threshold that turns multi-day activity and fitness tracking into a practical reality for Android smartwatch owners.

- 2025: Omada Health expanded its reimbursed diabetes-prevention pathway to include GLP-1 support, shifting payment liability for weight-loss medication adherence tools from individual users to insurers.

- 2025: Anytime Fitness integrated Apple Fitness+ content into its gym membership app starting December 1, giving gym members complimentary access to Apple's premium workout content alongside free trials for prospective members.

Fitness Apps Market key players are:

- MyFitnessPal, Inc.

- Under Armour, Inc.

- Azumio, Inc.

- Strava, Inc.

- Peloton Interactive, Inc.

- Fitbit LLC

- Apple Inc.

- Nike, Inc.

- Adidas AG

- WeightWatchers International, Inc.

- Freeletics GmbH

- Nexercise Inc.

- Aaptiv Inc.

- Sweat Media Pty Ltd

- Fitplan Inc.

- JEFIT Inc.

- Noom, Inc.

- Headspace Health

- FitOn, Inc.

- Garmin Ltd.

Fitness Apps Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.18 Billion |

| Market Size by 2035 | USD 38.29 Billion |

| CAGR | CAGR of 13.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Exercise Weight Loss, Activity Tracking, Diet Nutrition, Others) • By Platform (iOS, Android) • By Device (Smartphones, Wearables) • By Payment Model (Freemium, Subscription) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | MyFitnessPal, Inc., Under Armour, Inc., Azumio, Inc., Strava, Inc., Peloton Interactive, Inc., Fitbit LLC, Apple Inc., Nike, Inc., Adidas AG, WeightWatchers International, Inc., Freeletics GmbH, Nexercise Inc., Aaptiv Inc., Sweat Media Pty Ltd, Fitplan Inc., JEFIT Inc., Noom, Inc., Headspace Health, FitOn, Inc., Garmin Ltd. |

Frequently Asked Questions

The Exercise Weight Loss segment held approximately 53.69% share in 2025.

The Fitness Apps Market is expected to grow at a CAGR of 13.10% from 2026 to 2035.

The Fitness Apps Market was valued at USD 11.18 Billion in 2025.

Increasing health awareness combined with technological advancements and GLP-1 medication integration is the major growth factor.

Get in Touch