Operating Room Management Market Size & Overview:

Get more information on Operating Room Management Market - Request Sample Report

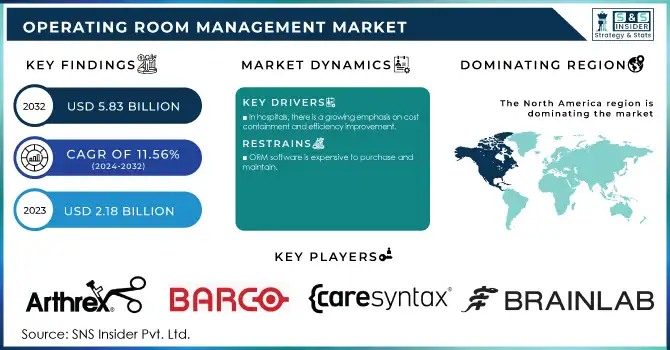

The Operating Room Management Market Size was valued at USD 2.18 billion in 2023, and is expected to reach USD 5.83 billion by 2032 and grow at a CAGR of 11.56% over the forecast period 2024-2032.

Operating room administration entails the use of software-based solutions to ensure that operating rooms run smoothly and efficiently. Multiple problems have become more prevalent as the world's senior population has grown. To combat this, operating rooms around the world are focusing on increasing cost-effectiveness and efficiency. The concentrate on the overall working room the board market gives a thorough investigation of the business. The exploration incorporates an intensive assessment of key market sections, patterns, drivers, limitations, cutthroat scene, and other significant factors.

The science of operating room administration focuses on the efficient management of operating room suites. Operating Rooms (ORs) are a critical hub in a hospital, and their resources must be managed effectively to maintain high-performance output and patient safety.

Operating Room Management Market Dynamics:

DRIVERS

-

In hospitals, there is a growing emphasis on cost containment and efficiency improvement.

-

EHRs and other HCIT solutions are becoming increasingly popular.

-

Supportive government policies and initiatives in the healthcare field

-

Projects for redevelopment and investment to promote OR infrastructure

RESTRAINTS

-

ORM software is expensive to purchase and maintain.

-

Issues concerning interoperability

OPPORTUNITIES

-

Emerging markets and growing medical tourism

-

Technological advances in hospitals

CHALLENGES

-

Incorporated operating rooms have a scarcity of experienced surgeons.

-

Healthcare providers are being merged.

IMPACT OF COVID-19

The COVID-19 pandemic has unleashed ruin on many individuals' lives and organizations for a monstrous scope. However, if there is one area that has benefited from this catastrophe, it is the healthcare IT sector. While many businesses are struggling to stay afloat, those who have chosen operating room management solutions are doing just well. The pandemic has resulted in a temporary restriction on elective surgeries all over the world, resulting in elective surgery cancellations all over the world. According to a paper issued by CovidSurg Collaborative experts, roughly 28 million procedures were cancelled around the world during the COVID-19 pandemic's peak interruption period of 12 weeks.

Hospitals are extending OR hours and concentrating on greater OR utilisation to deal with the rising surgery loads. The ORM programming business sector will profit from the COVID-19. It will boost ORM software usage because most hospitals would now focus on improving capacity by leveraging technology to boost efficiency.

Operating Room Management Market Segmentation Analysis

By Component Type

Software and services make up the operating room management market. The software category is likely to dominate the market. Moreover, during the projection period, this category is expected to increase at the highest CAGR. The expanding installation of ORM software is responsible for the big share and rapid expansion.

By Solutions Type

Data and communication management solutions, anesthesia management systems, workplace management solutions, operating room planning solutions, performance management solutions, and other solutions are all part of the solution phase. Because of the advantages such as easy sharing of patient status in patient care sections, schedule compliance, and sharing of media and information related to cases within separate operating rooms or outpatient departments, data management and communication solutions account for the largest component of the operating room management market.

By Delivery Mode

On-premise solutions, cloud-based solutions, and web-based solutions are the three categories in which the market is divided. During the projection period, the market for cloud-based solutions is predicted to grow at the fastest rate. This segment's rapid expansion is due to benefits such as scalable data storage, scalable processing power, machine-learning capabilities, and speedier data movement between cloud platforms' enterprises.

By End User

Hospitals and surgical centers are two types of services on the market. Due to the growing need for effective disease management, the increasing number of surgical procedures in hospitals, and the growing number of hospitals established in developing countries, hospitals are a major part of the global market for operating room operating systems.

KEY MARKET SEGMENTATION:

By Component Type

-

Software

-

Services

By Solutions Type

-

Data management and communication solutions

-

Anesthesia information management systems

-

Operating room supply management solutions

-

Operating room scheduling solutions

-

Performance management solutions

By Delivery Mode

-

On-premise solutions

-

Cloud-based solutions

By End User

-

Hospitals

-

Ambulatory surgery centers

Operating Room Management Market Regional Outlook

Because of the speedier adoption of new technologies, the presence of well-developed hospital infrastructure in the United States and Canada, the highest number of multi-specialty hospitals, and other factors, North America, led by the United States, commands the largest market share. Europe is the second largest market, with Germany, France, and the United Kingdom leading the way.

Japan, China, and India are expected to expand at the quickest CAGR in the Asia Pacific area. Due to weak social and economic conditions, particularly in Africa, the Middle East and African region is predicted to grow at a slow pace. The Gulf economy, on the other hand, are predicted to grow rapidly due to the region's faster expansion of healthcare and the creation of big hospital complexes like the King Fahd hospitals in Riyadh.

Need any customization research on Operating Room Management Market - Enquiry Now

REGIONAL COVERAGE:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS:

Some of the major key players of Operating Room Management Market are as follows: Arthrex, Inc., Barco, Care Syntax, Braiblab AG, Dragerwerk AG & Co. KGaA, Getinge AB, Olympus, Stryker, KARL STORZ SE & CO. KG, Steris and Other Players.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 2.18 Billion |

| Market Size by 2032 | USD 5.83 Billion |

| CAGR | CAGR of 11.56% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Software, Services) • By Solutions Type (Data management and communication solutions, Anesthesia information management systems, Operating room supply management solutions, Operating room scheduling solutions, Performance management solutions) • By Delivery Mode (On-premise solutions, Cloud-based solutions) • By End User (Hospitals, Ambulatory surgery centers) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Arthrex, Inc., Barco, Care Syntax, Braiblab AG, Dragerwerk AG & Co. KGaA, Getinge AB, Olympus, Stryker, KARL STORZ SE & CO. KG, and Steris. |

| Drivers | • In hospitals, there is a growing emphasis on cost containment and efficiency improvement. • EHRs and other HCIT solutions are becoming increasingly popular. • Supportive government policies and initiatives in the healthcare field • Projects for redevelopment and investment to promote OR infrastructure |

| Restraints | • ORM software is expensive to purchase and maintain. • Issues concerning interoperability |

Frequently Asked Questions

Top-down, bottom-up, Quantitative, Qualitative Research, Descriptive, Analytical, Applied, Fundamental Research.

The challenges faced by Particle Counter market is Incorporated operating rooms have a scarcity of experienced surgeons.

The by Delivery Mode is divided into two sub segments is On-premise solutions, Cloud-based solution.

Ans: The Operating Room Management Market is to grow at a CAGR of 11.56% over the forecast period 2024-2032.

Ans: The Operating Room Management Market size is expected to reach USD 5.83 Bn by 2032.

Get in Touch