Organ Care System Market Report Scope & Overview:

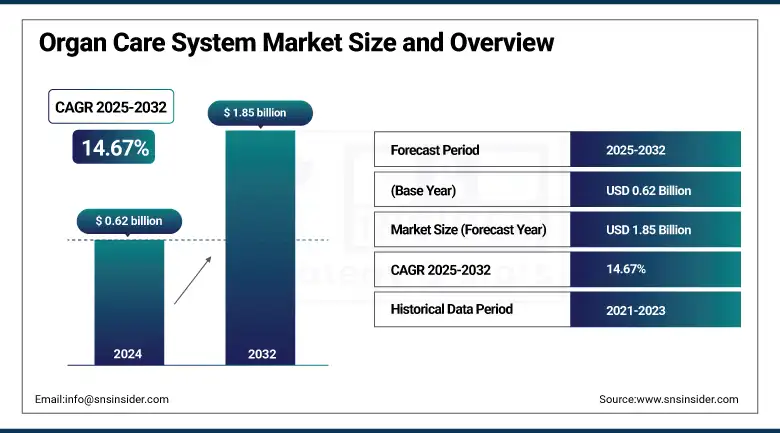

The organ care system market size was valued at USD 0.62 billion in 2024 and is expected to reach USD 1.85 billion by 2032, growing at a CAGR of 14.67% over 2025-2032.

The organ care system market is developing due to increasing numbers of transplants, increasing awareness of organ viability preservation, and technological advances leading to higher success rates post-transplant. Increased demand for advanced organ care systems is likely in the coming years, with global demand for organ transplants exceeding 150,000 in 2023 and close to 20% of viable organs becoming unusable due to preservation restrictions. Increasing demand for organ care systems in the developed regions, such as the US, which is equipped with a high-quality healthcare system, is driven by reimbursement models. Furthermore, the market growth is driven by rising R&D spending. TransMedics, for instance, made large investments in clinical trials and device refinement, and organ care system companies such as XVIVO Perfusion and Paragonix Technologies are continually releasing new portable and AI (artificial intelligence) devices.

To Get more information On Organ Care System Market - Request Free Sample Report

Regulatory agencies, including the FDA, have expedited the approval process for normothermic perfusion devices, allowing rapid dissemination across transplant centers. Heart and lung perfusion systems companies also have a major share in the organ care system market, owing to the high demand for these organs. Some of the factors driving the organ care system market growth are the shortage of donor organs, along with the long waiting lists, the rise in the acceptance of marginal donors, and the use of AI-incorporated preservation systems. Supply-side enhancements, such as smart transport systems and prolonged preservation time, also add to the organ care system market analysis. Public-private-based DoD-funded initiatives and growing acceptance in academic medical centers bring innovation and improved patient outcomes, which act as a major impact provider to the organ care systems market analysis.

In March 2024, XVIVO Perfusion reported that its transportable lung perfusion system has been successfully tested, improving logistics in transplants and gaining market share for its organ care system.

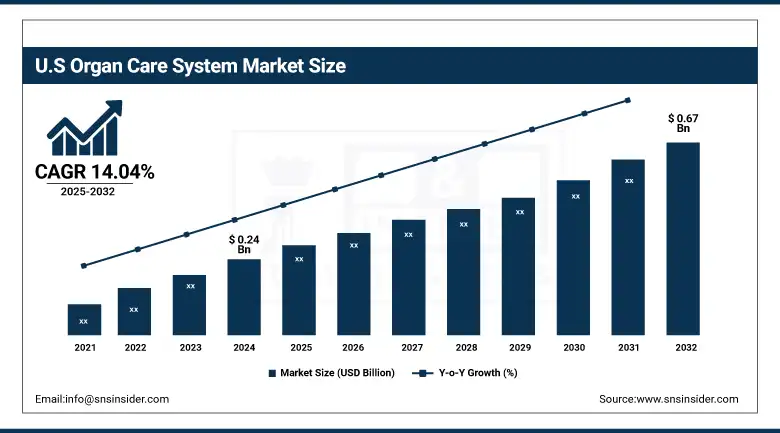

The U.S. organ care system market size was valued at USD 0.24 billion in 2024 and is expected to reach USD 0.67 billion by 2032, growing at a CAGR of 14.04% over 2025-2032. The U.S. dominated the market due to the existence of major organ care system players and a large number of transplants, because of the highest demand for organ transplantation, with statistics published by UNOS indicating more than 42,000 transplants in 2023. Market players' augmented investment in R&D and uptake of the leading-edge perfusion techniques, including normothermic machine perfusion, ensured market dominance. Canada also performed well, fuelled by strong governmental backing and an increasing donor registry rate. The U.S. is also the fastest-growing market in the region, driven by advancements in the field of organ monitoring devices and logistics systems with AI platforms.

Market Dynamics:

Drivers:

-

Rising Transplant Demand & Technological Advancements Fueling Adoption Fuel the Market Growth

The increasing number of transplants needs both locally and abroad, preservation technology advancement, and growing investment in R&D will continue to propel the organ care system market. More than 1.5 million patients globally are awaiting organ transplants, and only a small percentage of available donor organs meet the criteria for transplantation, making it necessary to develop new technologies that can extend organ viability. Advanced perfusion technologies, particularly hypothermic and normothermic machine perfusion, are emerging as a vital tool for increasing the number of available organs. Next-generation liver and kidney perfusion devices have been developed by companies including OrganOx and Bridge to Life that can extend preservation times and increase post-transplant recovery rates by as much as 30 per cent. In addition, interest in investing in climate tech has picked up, and several climate tech startups have raised a combined more than USD 300 million since 2021.

Regulatory backing is also playing an important role in accelerating the organ care system market share. For instance, OrganOx’s Metra device received the FDA Priority Review Designation, allowing manufacturers to streamline the trials and review processes. In addition, the increasing acceptance of marginal donors (MD) and ECD is driving demand for real-time monitoring and ex vivo perfusion solutions, adding to the supply-side momentum. These concerted trends are influencing the organ care system market trends towards increased clinical efficacy, less wastage, and better patient outcomes.

Restraints:

-

High Capital Costs & Operational Complexities Limiting Adoption

High capital and operational expenditure linked with these sophisticated systems is one of the major factors that limit the growth of the market. The majority of perfusion systems are priced at USD 200,000-350,000 per unit, and disposable and maintenance costs are not included, which places these systems out of reach of small transplant centers and low-income hospitals. Moreover, the requirement of skilled personnel to manage and control perfusion systems also during transportation or pre-operative periods, restrains the use in decentralized environments. Supply chain inconsistencies, including the availability of perfusate solutions and sterile consumables, add further barriers to seamless application, especially in remote or underdeveloped areas.

There are also still regulatory hurdles, as manufacturers have to go through multi-stage clinical validation and conform to changing standards such as the EU MDR and FDA’s 21 CFR Part 820, which postpone time-to-market. Assessing barriers to the utilization of portable perfusion systems during a February 2023 industry survey, 41% of transplant hospitals identified reimbursement uncertainty and complexity associated with portable perfusion as significant barriers to adoption. Furthermore, in-hospital connectivity to EHR and transplant workflow systems is suboptimal and currently does not allow for real-time syncing of data. These challenges that are related to cost, training, and infrastructure are hindering the full-scale adoption and restricting the organ care system market growth in many potential use settings.

Segmentation Analysis:

By Organ Type

In 2024, the heart segment led the market for organ care systems, with more than 36.5% of the market share. This has been due to the high prevalence of cardiovascular diseases at the global level and the essential role of maintaining cardiac viability of real-time perfusion to be integrated during transport. Devices such as the TransMedics OCS Heart are increasingly used because of the possibility to extend preservation time and functionally assess the heart before transplantation.

Lung segment is the fastest growing segment, owing to increased acceptance of marginal donors and a surge in demand for ex vivo lung perfusion (EVLP). Technologies like XVIVO’s lung perfusion system and the larger success rates in transplanting organs are continuing to drive hospitals to utilise lung-specific organ care technologies.

By Technology

Machine perfusion was the dominant segment in 2024 and accounted for more than 42.3% of the total revenue. Having the potential to preserve organ function, decrease ischemia-reperfusion injury, and evaluate viability in situ, compared to static storage, SSS is advantageous, especially for marginal organs.

Normothermic regional perfusion (NRP) is a rapidly expanding field in EVLP, which facilitates in situ organ recovery in almost physiological circumstances. The rise in usage in DCD cases and support by regulators in Europe and North America is driving its use.

By Product Type

Perfusion systems accounted for 39.8% in terms of revenue in the year 2024, as they were utilized significantly for the evaluation of organ viability and long-distance transportation. The availability of FDA-approved devices for heart and liver perfusion and the growth of hospital-based transplant programs are additional factors promoting their acceptance.

Monitoring systems are rapidly expanding, as the transplant teams require constant information on temperature, flow, pressure, and oxygenation during transport. The rise in the segment is driven by the changeover from dumb to smart, artificial intelligence-integrated tracking platforms.

By Application

In 2024, organ transplantation continued to dominate the market, accounting for more than 61.2% owing to increasing multi-organ transplantation globally and an increase in the use of perfusion systems in donor-recipient logistics.

Remote monitoring and transport tracking are becoming among the fastest-growing applications, with increasing pressure for data-driven logistics and transparency in organ transfer. They are being driven by startups that provide integrated GPS and IoT-enabled tracking solutions.

By End User

The transplant centers segment dominated the market in 2024, as these can receive organs, evaluate, and use advanced techniques of perfusion systems and have a direct impact on the success rate of transplants.

OPOs will be the most rapidly growing end users, with the expanding use of mobile perfusion systems and cloud-based platforms to improve coordination, cut cold ischemia time, and increase the rate of organ acceptance across larger geographies.

Regional Analysis:

North America was the leading revenue-generating region in 2024, driven by its well-developed healthcare infrastructure and high organ transplant rates, along with stringent government regulations.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe was the second organ care system market share holder in 2024 on account of established transplant networks, growing awareness, and EU-funded programs for organ donation. Germany was the leading country in the region in terms of transplant procedures, due to rising investment in healthcare development and the presence of well-developed transplant centers. France and the United Kingdom are also among the biggest donors, diversified by legal changes to mandate organ donation. The UK largest growing country in the region, and more than 4,600 organ transplants were performed in 2023, supported by the “opt-out” organ donation legislation and the increasing usage of machine perfusion technology.

Asia Pacific is growing at the highest CAGR in the global organ care system market, driven by growing government steps, escalating development in the healthcare infrastructure, and the growing incidence of organ failure resulting from the growing dialysis population. China leads because of its growing transplant system based on investments made by the National Health Commission in organ-sharing networks and in logistic enhancements. India is observing the highest growth in the region for increasing deceased donor awareness, the success of the public-private partnership programs, and the introduction of cloud-based transport tracking solutions. Japan and South Korea are also spending heavily on R&D, lifting regional growth too.

Key Players:

Leading organ care system companies in the market include TransMedics Inc., XVIVO Perfusion AB, OrganOx Limited, Paragonix Technologies Inc., Bridge to Life Ltd, Organ Recovery Systems Inc., Organ Assist B.V., Water Medical System LLC, Preservation Solutions Inc., Organ Transport System Inc., Perfusion Solutions Inc., Stealth BioTherapeutics, Medical Solutions Inc., AlloSource, Cellerate, Organogenesis Inc., Tissue Regenix Group, Vital Therapies Inc., LifeShare Transplant Donor Services, and Tandem Diabetes Care Inc.

Recent Developments:

In May 2024, TransMedics announced the expansion of its OCS Lung platform trials to include broader donor and recipient profiles in the U.S., aiming to enhance utilization rates and reduce waiting times for lung transplants.

In January 2024, XVIVO Perfusion AB received CE Mark approval for its new portable organ perfusion system designed for heart and liver preservation, enabling real-time monitoring and transport across longer distances in Europe.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 0.62 billion |

| Market Size by 2032 | USD 1.85 billion |

| CAGR | CAGR of 14.67% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Organ Type (Heart, Liver, Kidney, Lung, Pancreas, and Others (intestines, composite tissues like face/limbs, multi-organ systems for research)) • By Technology (Machine Perfusion (normothermic, hypothermic), Static Cold Storage (basic, enhancers), Normothermic Regional Perfusion, and Cold Storage Technology) • By Product Type (Perfusion Systems, Organ Preservation Solutions, Transportation Systems, Monitoring Devices, and Others (logistics software, hybrid organ care kits)) • By Application (Organ Transplantation, Research & Development, In-Hospital Organ Preservation, Remote Monitoring & Transport Tracking) • By End User (Hospitals, Transplant Centers, Organ Procurement Organizations, Research Institutes & Clinical Laboratories, and Others (ambulatory surgical centers, academic transplant units, mobile transplant programs)) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | TransMedics Inc., XVIVO Perfusion AB, OrganOx Limited, Paragonix Technologies Inc., Bridge to Life Ltd, Organ Recovery Systems Inc., Organ Assist B.V., Water Medical System LLC, Preservation Solutions Inc., Organ Transport System Inc., Perfusion Solutions Inc., Stealth BioTherapeutics, Medical Solutions Inc., AlloSource, Cellerate, Organogenesis Inc., Tissue Regenix Group, Vital Therapies Inc., LifeShare Transplant Donor Services, and Tandem Diabetes Care Inc. |

Frequently Asked Questions

Recent advancements include normothermic machine perfusion, portable organ care devices, and smart monitoring for real-time organ function assessment during transport.

North America dominates the market due to strong transplant infrastructure and reimbursement support. Europe is the second-largest, with rapid growth in Germany and the U.K.

Rising organ transplant volumes, improved patient outcomes, and adoption of normothermic perfusion systems are key drivers. Supportive regulatory approvals and R&D funding also fuel growth.

Key players include TransMedics Inc., XVIVO Perfusion AB, Paragonix Technologies, OrganOx Ltd, and Bridge to Life Ltd, among others. These companies lead in perfusion and transport technologies.

The Organ Care System market is projected to reach USD 0.71 billion by 2025, driven by increased transplant demand. It is expected to grow at a CAGR of 14.67% through 2032.

Get in Touch