Softgel Capsule Market Report Scope & Overview:

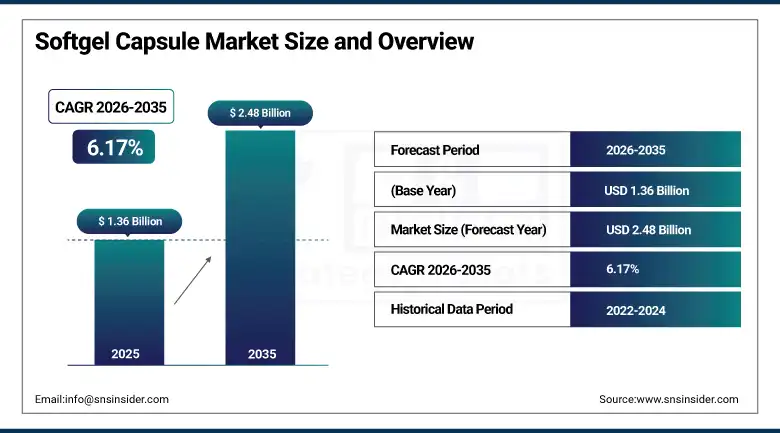

The Softgel Capsule Market was valued at USD 1.36 Billion in 2025 and is expected to reach USD 2.48 Billion by 2035, growing at a CAGR of 6.17% from 2026–2035.

The global softgel capsule market is experiencing steady growth driven by rising demand for easy-to-swallow pharmaceutical and nutraceutical dosage forms, increasing adoption for poorly water-soluble active ingredient encapsulation, and growing consumer preference for softgel’s superior bioavailability relative to tablet and hard capsule alternatives. Softgel capsules are one-piece sealed soft gelatin or plant-based shells containing liquid, semi-solid, or suspension fill materials that provide hermetic encapsulation protecting sensitive active ingredients from oxidation, moisture, and light degradation while enabling efficient gastrointestinal dissolution and active ingredient release. The technology’s particular commercial advantage in lipid-based drug delivery whose self-emulsifying drug delivery system formulation creates bioavailability improvement for BCS Class II and IV poorly water-soluble APIs creates structured pharmaceutical development investment in softgel dosage form specification.

In 2025, Lonza Capsugel introduced its Vegicaps Twist plant-based softgel capsule with enhanced seal integrity and improved fill compatibility for liquid omega-3 and botanical extract formulations, targeting the growing vegan and clean-label supplement market whose consumer base specifies plant-based capsule alternatives to conventional bovine gelatin softgel formulations. The product development reflects the commercial direction of the softgel capsule market toward plant-based alternatives whose halal, vegan, and clean-label credentials create premium pricing justification above commodity gelatin softgel alternatives in the growing premium supplement segment.

Softgel Capsule Market Size and Forecast

-

Market Size in 2026E: USD 1.44 Billion

-

Market Size by 2035: USD 2.48 Billion

-

CAGR: 6.17% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Softgel Capsule Market - Request Free Sample Report

Softgel Capsule Market Trends

-

Plant-based and vegan softgel capsules are growing rapidly using starch and pullulan alternatives, enabling clean-label, halal, and vegan supplement positioning globally.

-

Lipid-based drug delivery softgels are expanding due to improved bioavailability of poorly soluble drugs through SEDDS and SMEDDS formulations.

-

Enteric-coated softgels are increasing in demand for protecting acid-sensitive APIs and probiotics, improving stability and controlled release performance.

-

Targeted drug delivery softgels using pH-sensitive and enzyme-responsive polymers are enabling site-specific gastrointestinal drug release systems.

-

Omega-3 and vitamin D nutraceutical softgels are witnessing strong growth due to rising consumer focus on heart, immune, and bone health.

The U.S. Softgel Capsule Market Outlook

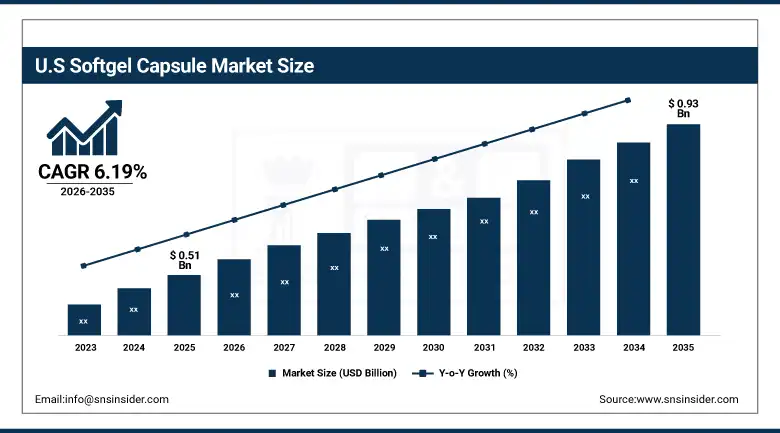

The U.S. Softgel Capsule Market was valued at approximately USD 0.51 Billion in 2025 and is expected to reach approximately USD 0.93 Billion by 2035, growing at a CAGR of approximately 6.19%.

The U.S. is the most commercially significant softgel capsule market within North America’s dominant revenue position. Lonza Capsugel, Catalent, Aenova Group, Procaps Group, and Soft Gel Technologies collectively define the domestic commercial landscape. The pharmaceutical industry’s increasing use of softgel for bioavailability enhancement creates structured prescription softgel procurement, while the extraordinary U.S. dietary supplement market’s omega-3, vitamin D, vitamin E, and multivitamin softgel consumption creates the most commercially concentrated consumer nutraceutical softgel demand environment globally.

In 2024, Catalent expanded its Somerset, New Jersey advanced softgel manufacturing facility with new high-speed encapsulation lines capable of processing above 500,000 softgel capsules per hour for commercial pharmaceutical manufacturing programmes, targeting the growing demand for outsourced pharmaceutical softgel production from specialty pharma companies whose poorly water-soluble pipeline creates above-average lipid formulation softgel specification.

Softgel Capsule Market Segment Analysis

-

By Type, the gelatin-based/animal-based segment dominated the softgel capsule market with approximately 72% share in 2025, while the non-animal-based/plant-based segment is the fastest growing.

-

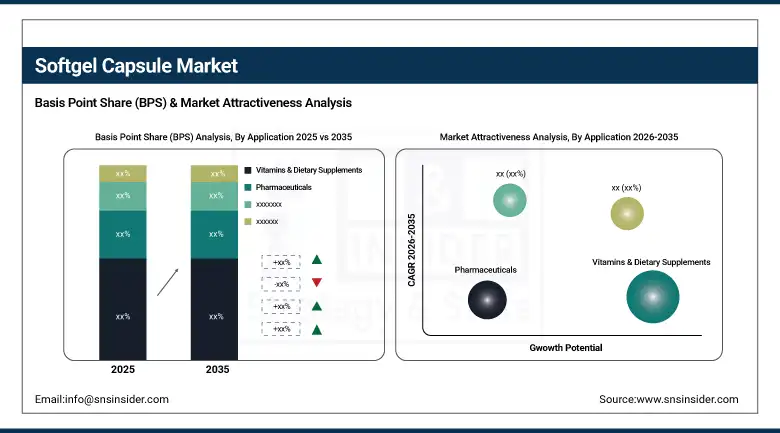

By Application, the vitamins & dietary supplements segment dominated the softgel capsule market with approximately 58% share in 2025, while the pharmaceuticals segment is the fastest growing.

-

By End-use, the nutraceuticals segment dominated the softgel capsule market with approximately 62% share in 2025, while the pharmaceutical industry segment is the fastest growing.

By Type, gelatin-based dominates, plant-based grows fastest

Gelatin-based softgel capsules retained the dominant type position with approximately 72% of the softgel capsule market in 2025. The commercial primacy of bovine and porcine gelatin softgel reflects its decades of established pharmaceutical and nutraceutical application whose seal integrity validation, regulatory acceptance across all major markets, and manufacturing process optimization collectively create a production infrastructure advantage that plant-based alternatives are progressively overcoming but have not yet fully closed. Gelatin’s thermoplastic properties at elevated manufacturing temperatures creating the rotary die encapsulation process’ seamless fill-seal operation create production efficiency at commercial softgel manufacturing speeds that current plant-based alternatives cannot consistently match.

Non-animal-based plant-based softgel is the fastest-growing type because the convergence of vegan diet adoption, halal pharmaceutical requirement in Muslim-majority markets, and clean-label supplement positioning creates above-average growth in plant-based softgel capsule specification. Each nutraceutical brand that reformulates from gelatin to plant-based softgel to achieve vegan certification creates procurement migration that compounds with the dietary supplement market’s clean-label trend. Lonza’s Vegicaps and ACG’s non-animal softgel product lines demonstrate the commercial investment in plant-based softgel manufacturing capability whose scale improvement progressively reduces the cost differential from gelatin alternatives.

By Application, vitamins & supplements dominate, pharma grows fastest

Vitamins and dietary supplements retained the dominant application position with approximately 58% of the softgel capsule market in 2025. The omega-3 fish oil softgel’s status as the world’s highest-selling dietary supplement by volume creates the most commercially significant single softgel product procurement whose aggregate across global omega-3 supplement consumption creates consistent high-volume soft encapsulation demand. Vitamin D softgel’s rapid adoption driven by pandemic-era immune health awareness and vitamin E and vitamin A’s established nutraceutical softgel formats collectively sustain vitamins and supplements’ dominant softgel application position. The supplement industry’s above-average new product introduction velocity creates consistent new softgel application development that compounds with established product volume growth.

Pharmaceuticals is the fastest-growing application because the pharmaceutical industry’s progressive adoption of lipid-based drug delivery systems for poorly water-soluble API bioavailability improvement creates structured prescription softgel procurement. Each new drug application for a BCS Class II compound whose oral bioavailability improvement through SEDDS or SMEDDS softgel formulation creates FDA approval creates long-duration commercial softgel procurement whose generic entry eventually multiplies the procurement volume across multiple manufacturers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Softgel Capsule Market Insights

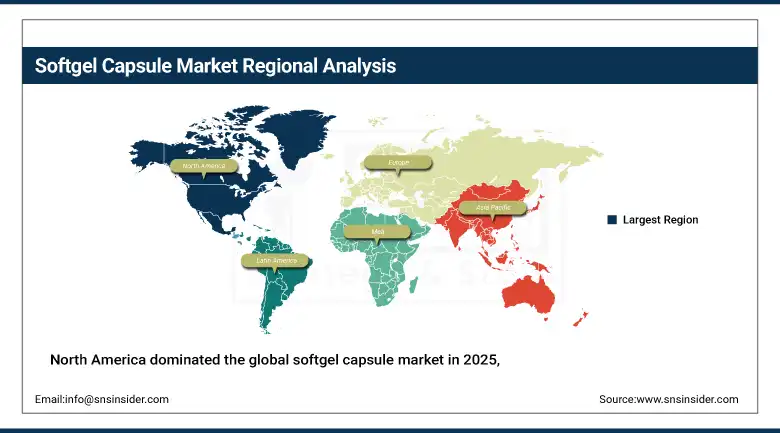

North America dominated the global softgel capsule market in 2025, driven by the most commercially sophisticated dietary supplement and pharmaceutical softgel sectors globally. The United States accounts for approximately 87.4% of North American revenues through Lonza Capsugel, Catalent, and Procaps Group’s commercial operations and the extraordinary domestic dietary supplement market’s omega-3 and vitamin softgel consumption.

Canada contributes approximately 12.6% of North American revenues through its natural health products market’s softgel specification, the growing pharmaceutical sector’s lipid formulation softgel demand, and the supplement manufacturing sector’s contract encapsulation investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Softgel Capsule Market Insights

Europe is a technically sophisticated softgel capsule market where EU pharmaceutical regulations, the supplement sector’s above-average quality specification, and Aenova Group’s European manufacturing leadership create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its pharmaceutical industry’s lipid formulation softgel development, the supplement sector’s omega-3 and vitamin procurement, and the contract manufacturing sector’s commercial softgel production.

The United Kingdom and the Netherlands are significant secondary markets where the NHS supplement reimbursement, the pharmaceutical industry’s softgel programme, and the supplement retail market’s omega-3 consumer demand create consistent commercial procurement.

Asia Pacific Softgel Capsule Market Insights

Asia Pacific is the fastest-growing regional softgel capsule market, driven by China’s extraordinary pharmaceutical and nutraceutical sector growth, India’s generic pharmaceutical softgel manufacturing scale, Japan’s premium supplement market, and South Korea’s beauty-from-within nutraceutical softgel adoption. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic supplement market growth, the pharmaceutical industry’s softgel production, and the growing export-oriented CMO sector’s encapsulation capacity.

India represents the most commercially dynamic secondary market where the generic pharmaceutical industry’s softgel programme development, the growing domestic nutraceutical market’s supplement demand, and the contract manufacturing sector’s cost-competitive encapsulation service create above-average market growth.

MEA & Latin America Softgel Capsule Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its halal supplement market’s non-porcine gelatin specification driving non-animal softgel adoption, the growing pharmaceutical sector’s lipid formulation procurement, and Vision 2030’s healthcare supplement investment creating new consumer channels. UAE’s premium supplement consumer and the Gulf healthcare sector’s pharmaceutical softgel demand add complementary MEA revenues. Brazil leads Latin American revenues at approximately 44.2% through its large dietary supplement market, Procaps Group’s regional manufacturing leadership, and the pharmaceutical industry’s softgel procurement. South Africa’s growing pharmacy channel collectively sustains regional market development through 2035.

Market Dynamics

Growth Drivers: Nutraceutical omega-3 demand and pharmaceutical lipid formulation adoption creating structured softgel procurement

The extraordinary global omega-3 dietary supplement market’s growth creates the most commercially concentrated softgel capsule demand from a single product category whose fish oil, krill oil, and algal omega-3 fill compatibility with gelatin and plant-based softgel creates consistent high-volume procurement. Each consumer health awareness campaign demonstrating cardiovascular, cognitive, and inflammatory benefit from omega-3 supplementation creates new supplement adoption whose aggregate across global consumer markets sustains above-average softgel capsule demand growth.

Pharmaceutical lipid-based drug delivery system adoption creates above-average prescription pharmaceutical softgel specification investment from drug developers targeting bioavailability improvement. The pharmaceutical pipeline’s high proportion of BCS Class II and IV poorly water-soluble compounds whose oral bioavailability challenge creates structured SEDDS and SMEDDS softgel formulation investment sustaining pharmaceutical grade softgel procurement growth.

Restraints: High manufacturing complexity and gelatin supply variability

Softgel encapsulation’s rotary die manufacturing process complexity requires specialized capital equipment, environmental control, and process expertise that creates adoption barriers for smaller pharmaceutical manufacturers whose internal manufacturing capability cannot efficiently produce softgel at commercial quality. Each pharmaceutical company that lacks internal softgel manufacturing creates contract encapsulation dependence whose supply security risk moderates softgel specification in time-sensitive commercial launch programmes.

Bovine gelatin supply variability from animal processing industry cycles creates raw material availability sensitivity that moderates production planning certainty for gelatin softgel manufacturers whose supply chain dependence on rendering by-product availability creates price and availability cyclicality.

Opportunities: Plant-based softgel innovation and lipid SEDDS formulation services

Plant-based softgel development represents the most commercially premium innovation opportunity whose vegan certification, halal compliance, and clean-label positioning create above-gelatin-commodity pricing in premium supplement markets. Each nutraceutical brand that successfully launches a plant-based softgel product creates market education that sustains the commercial momentum of non-animal softgel adoption.

Lipid-based formulation development services for pharmaceutical companies seeking bioavailability enhancement creates a service category adjacent to softgel manufacturing whose SEDDS characterization, excipient screening, and regulatory dossier support creates above-encapsulation-fee commercial relationships with pharmaceutical clients.

Recent Developments:

-

2026: Lonza (Capsugel) advanced next-generation softgel platforms with increased emphasis on plant-based and carrageenan-free capsule shells, supporting clean-label and vegan nutraceutical demand across global supplement markets.

-

2025: Aenova Group expanded softgel manufacturing capabilities in Europe and North America, enhancing lipid-based and temperature-sensitive API encapsulation technologies to support advanced pharmaceutical and nutraceutical formulations with improved bioavailability performance.

-

2025: Catalent Inc. strengthened global softgel CDMO capacity through continued investment in liquid fill and encapsulation technologies, focusing on high-potency drug handling and scalable clinical-to-commercial manufacturing transition programs.

-

2025: Procaps Group expanded its Latin America and US manufacturing footprint, increasing production capacity for pharmaceutical and nutraceutical softgel products while integrating automation to improve batch consistency and yield efficiency.

Softgel Capsule Market Key Players are:

-

Lonza Group AG (Capsugel)

-

Catalent Inc. (Novo Holdings)

-

Aenova Group GmbH

-

Procaps Group SA

-

Soft Gel Technologies Inc.

-

Patheon NV (Thermo Fisher Scientific)

-

Sirio Pharma Co. Ltd.

-

Strides Pharma Science Ltd.

-

Qualicaps Co., Ltd.

-

Robinson Pharma Inc.

-

Captek Softgel International

-

Nutraceutix Inc.

-

CapsCanada Corporation

-

Vitaquest International LLC

-

ACG Capsules Ltd.

-

Divi’s Laboratories Ltd.

-

Elan Drug Delivery Ltd.

-

EuroCaps Ltd.

-

Fuji Capsule Co., Ltd.

-

Elmwood Park NJ Manufacturing

Softgel Capsule Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.36 Billion |

| Market Size by 2035 | USD 2.48 Billion |

| CAGR | CAGR of 6.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Gelatin-Based/Animal-Based, Non-Animal-Based/Plant-Based) • By Application (Vitamins & Dietary Supplements, Pharmaceuticals, Cosmetics & Personal Care, Others) • By End-use (Nutraceuticals, Pharmaceutical Industry, Cosmetics & Personal Care Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lonza Group AG (Capsugel), Catalent Inc. (Novo Holdings), Aenova Group GmbH, Procaps Group SA, Soft Gel Technologies Inc., Thermo Fisher Scientific (Patheon), Sirio Pharma Co. Ltd., Strides Pharma Science Ltd., Qualicaps Co., Ltd., Vitaquest International LLC, Captek Softgel International, Nutraceutix Inc., CapsCanada Corporation, ACG Capsules Ltd., Divi’s Laboratories Ltd., Elan Drug Delivery Ltd., EuroCaps Ltd., Fuji Capsule Co., Ltd. |

Frequently Asked Questions

The Softgel Capsule Market is expected to grow at a CAGR of 6.17% from 2026 to 2035.

The Softgel Capsule Market was valued at USD 1.36 Billion in 2025.

Rising nutraceutical omega-3 and vitamin supplement softgel demand and pharmaceutical industry adoption of lipid-based drug delivery systems.

Gelatin-Based/Animal-Based dominated the Softgel Capsule Market with approximately 72% share in 2025.

North America dominated the Softgel Capsule Market in 2025.

Get in Touch