Orthodontics Market Report Scope & Overview:

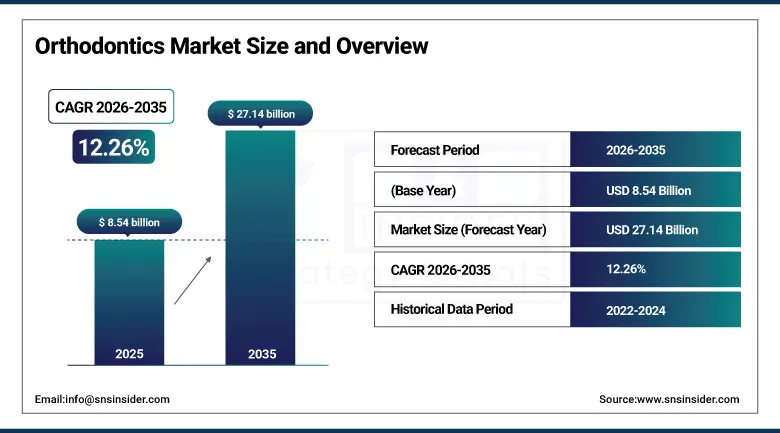

The Orthodontics Market was valued at USD 8.54 Billion in 2025 and is expected to reach USD 27.14 Billion by 2035, growing at a CAGR of 12.26% from 2026 to 2035.

One of the most commercially exciting developments ever to impact the orthodontics industry is the dramatic transformation of the industry through the intersection of cutting-edge clear aligner technology, the digitally based orthodontics planning process, and the fundamental change in the patient demographic for orthodontic treatment. Throughout the history of orthodontics in practice over its last hundred years, the key patient demographic group seeking treatment was teenagers undergoing traditionally funded braces at a biological stage in their lives where malocclusion correction can most efficiently occur. This paradigm has been thoroughly upended by recent trends. Adults constitute about 62% of the current patient population seeking orthodontic treatments due to increased understanding of the value of correcting malocclusion to ensure good long-term oral health, coupled with the availability of discreet and clear aligner technology, making orthodontic treatment possible without affecting professional or social standing.

The Align Technology expanded GP dentist training programme, which has certified over 240,000 general dentists globally to provide Invisalign treatment, represents a strategic market development investment that progressively shifts orthodontic case volume from specialist practices to the general dentistry setting where patient access frequency and the absence of a referral barrier dramatically expand the addressable treatment opportunity.

Market Size and Forecast

-

Market Size in 2026E: USD 9.52 Billion

-

Market Size by 2035: USD 27.14 Billion

-

CAGR: 12.26% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Orthodontics Market - Request Free Sample Report

Orthodontics Market Trends

-

Clear aligner adoption is expanding rapidly across both orthodontic specialists and general dentistry practices due to growing digital dentistry integration and aligner accessibility.

-

AI-powered treatment planning software is improving orthodontic workflow efficiency, treatment accuracy, and outcome predictability.

-

Self-ligating and customized bracket systems are gaining popularity for enhanced patient comfort and faster treatment efficiency.

-

Expansion of corporate dental groups and managed care networks is improving access to orthodontic treatments across wider patient populations.

-

Digital retention management and remote monitoring platforms are extending patient engagement beyond active orthodontic treatment periods.

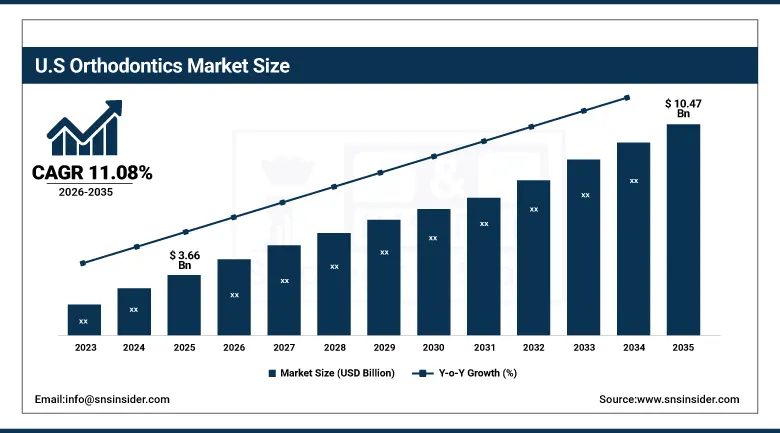

The U.S. Orthodontics Market Outlook

The U.S. Orthodontics Market was valued at approximately USD 3.66 Billion in 2025 and is expected to reach approximately USD 10.47 Billion by 2035, growing at a CAGR of approximately 11.08%.

The U.S. market is the biggest in the world in terms of sales and the benchmark for orthodontics markets globally. There are about 11,000 specialists practicing orthodontics in the U.S., and they cater to teenage and adult patients on the back of insurance plans for eligible teenagers and self-payments for adults. The provision of the orthodontic benefit within the U.S. market of dental insurance usually caps the lifetime coverage of orthodontic services at USD 1,000-USD 2,500. This minimum reimbursement helps to eliminate any potential financial obstacles for treatment initiation and to maintain consistent treatment volumes throughout business cycles.

3M's Oral Care Solutions division launched its Clarity Ultra Self-Ligating Bracket System with an updated bracket design incorporating ceramic tooth-colored bracket bodies and a low-friction self-ligating mechanism in the United States in 2025.

Orthodontics Market Segment Analysis

-

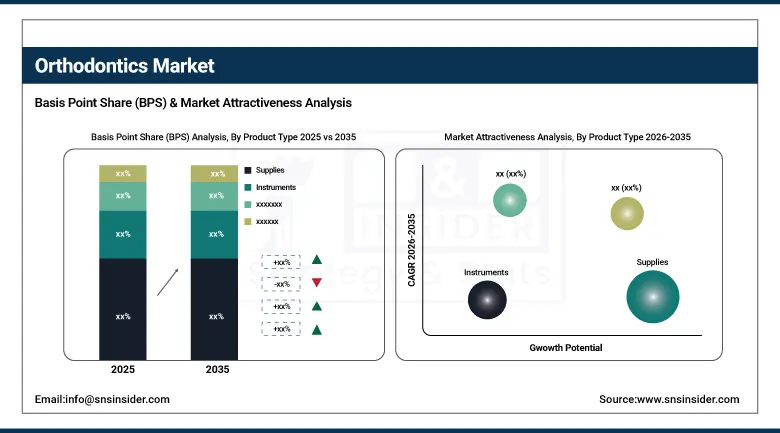

By Product Type, the supplies segment dominated the orthodontics market with 72.84% share in 2025, while the instruments segment is the fastest growing product type during 2026 to 2035.

-

By Age Group, the adults segment dominated the orthodontics market with 62.00% share in 2025, while the teens segment is the fastest growing age group during 2026 to 2035.

-

By End User, the dentist & orthodontist owned practices segment dominated the orthodontics market with 64.73% share in 2025, while the hospitals & dental clinics segment is the fastest growing end user during 2026 to 2035.

-

By Distribution Channel, the direct sales segment dominated the orthodontics market in 2025, while online channels are the fastest growing distribution channel during 2026 to 2035.

By Product Type, supplies dominate, instruments grow fastest

The supplies segment generated 72.84% of orthodontics market revenue in 2025. Within this dominant category, clear aligner systems are the most commercially significant and fastest-growing sub-segment whose market share within total orthodontic supplies revenue has expanded dramatically since Invisalign's commercial launch and continues growing as new aligner platforms and indications expand the treatable case portfolio. Fixed appliance supplies including brackets, bands, archwires, and bonding adhesives serve a large and stable volume base representing the conventional orthodontic treatment modality that retains clinical preference for complex malocclusion cases, interdisciplinary treatment combining orthodontics with orthognathic surgery, and patient populations including young adolescents for whom fixed appliance compliance management advantages are clinically relevant.

Orthodontic instruments including pliers, band seaters, debonders, and measuring tools represent the fastest-growing product type as instrument replacement cycles, new product introductions incorporating ergonomic and material improvements, and the growing orthodontic specialist workforce in emerging markets sustain instrument procurement growth above the broader market rate.

By Age Group, adults dominate, teens grow fastest

Adults accounted for 62% of orthodontics market revenue in 2025, a structural market share that would have seemed implausible two decades ago when the orthodontic category was predominantly a paediatric and adolescent clinical service. The commercial transformation has been driven primarily by the clear aligner format whose patient experience advantages over conventional bracket systems removed the most significant psychosocial barriers to adult treatment initiation.

Teens are projected to grow at the fastest CAGR during 2026 to 2035 as the expanding global teen population, rising parental investment in dental health outcomes for children, and growing availability of teen-specific clear aligner products including Invisalign Teen with compliance indicators collectively increase the proportion of the global adolescent malocclusion burden that receives active orthodontic treatment.

By End User, specialist practices dominate, hospitals & dental clinics grow fastest

Dentist and orthodontist owned specialist and general practices accounted for 64.73% of orthodontics market revenue in 2025. Private specialist practices remain the primary treatment environment for complex orthodontic cases, interdisciplinary treatment planning, and patients seeking the highest level of specialist expertise and customized care whose premium positioning supports practice economics that sustain investment in advanced digital workflow technology including intraoral scanners, AI treatment planning software, and in-house clear aligner manufacturing capability.

Hospitals and dental clinics are the fastest-growing end user setting as corporate dental group expansion, managed care network orthodontic programme development, and hospital-integrated dental services bring organised orthodontic treatment access to patient populations that geography or income have historically excluded from specialist private practice settings.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.72% |

|

Europe |

Germany |

26.84% |

|

Asia Pacific |

China |

34.82% |

|

Middle East & Africa |

UAE |

24.47% |

|

Latin America |

Brazil |

43.84% |

North America Orthodontics Market Insights

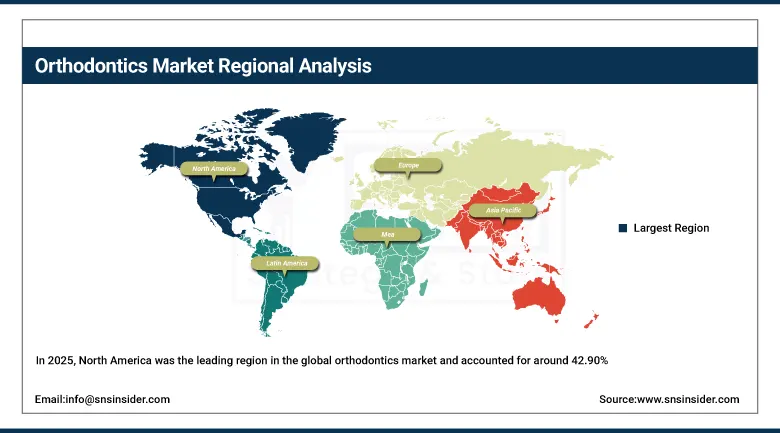

In 2025, North America was the leading region in the global orthodontics market and accounted for around 42.90% of worldwide market revenues. The US makes up approximately 84.72% of the revenue generated in the region because it has the most commercially advanced clear aligner market in the world along with an ample number of well-paid orthodontist dentists and a culture that values dental aesthetics, thereby making consumers very willing to pay for their orthodontic treatment at any age. Canada accounts for approximately 15.28% of the revenue generated by the region as it provides subsidized dental services for kids and has recently started including orthodontic treatment under the public dental coverage plan of qualifying kids.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Orthodontics Market Insights

Orthodontics revenues in Europe accounted for 24.73% of world revenues in the year 2025. The commercial environment of the region is impacted by significant differences between reimbursements for orthodontic treatment offered in different EU members countries. High penetrations levels of adolescents who require orthodontic treatment are facilitated by public coverage of children's orthodontics services in Germany, the Netherlands, and Scandinavian countries. Meanwhile, treatments of adults require private financing in all European regions. Major national markets are represented by Germany, France, the UK, Italy, and Spain. Revenue growth at above-average levels in adult orthodontics in Europe is driven by increasing penetration of clear aligner treatment, which is fueled by investments of clear aligners providers into consumer marketing activities. Additionally, the increase is facilitated by the rising share of clear aligner treatments offered by GP dentists.

Asia Pacific Orthodontics Market Insights

The Asia-Pacific region has the highest growth potential within the global orthodontics market with an expected Compound Annual Growth Rate (CAGR) of around 15.84% over the period till 2035. China is the biggest revenue contributor in the Asia-Pacific region accounting for 34.82%, which is attributed to a highly active middle-class demographic, growing consumer awareness about dental aesthetics, coupled with rising incomes leading to increased orthodontic treatment rates using both clear aligners and traditional brackets. Domestic manufacturing companies such as AngelAlign and EasySmile are offering clear aligners at competitive prices vis-à-vis premium products manufactured by international players. This is resulting in increased orthodontic procedures amongst patients from all economic backgrounds who cannot afford premium products available from global players. Other markets such as Japan, South Korea, India, and Australia also have strong demand dynamics.

MEA & Latin America Orthodontics Market Insights

The Middle East and Latin America represent regions where growth in Orthodontics is driven by increased awareness of aesthetic dental treatments, the development of an extensive infrastructure of private dental clinics, and a growing ability to pay amongst middle-class individuals for discretionary medical services. The United Arab Emirates is the top revenue earner within MEA, with revenues accounting for around 24.47% of the region's overall figure because of its wealthy population of international patients, the presence of high-caliber private dental clinic infrastructures, and a growing social acceptance of aesthetic dental procedures amongst Gulf nation populations with an increasingly visible awareness of smile aesthetics from their social media platforms. In terms of Latin America, Brazil is the leader of revenues, representing around 43.84% of the overall market revenues due to its large population of dentists and strong consumer culture valuing smile aesthetics.

Market Dynamics

Growth Drivers: Rising adult orthodontic treatment demand and increasing adoption of digital orthodontic workflows are driving orthodontics market growth.

Growth in the orthodontics market is greater than the rest of the dentistry industry due to the fact that it is fueled not only by population increase but also by the recruitment of a new patient base comprised of adults who do not seek treatment. It is estimated that between 70 and 80 percent of adults suffer from some type of misaligned teeth. However, traditional treatment had been limited by appearance concerns, lack of time and the misconception that orthodontics only treated children. Through clear aligner technology, all of these obstacles have been overcome.

Restraints: High clear aligner treatment costs and patient compliance challenges with removable appliances are restraining orthodontics market growth, particularly in cost-sensitive and complex treatment cases.

The more advanced clear aligner systems come with treatment costs at 30 to 70% higher than those of fixed appliances with similar features, thereby making it difficult for them to reach sensitive market segments where cost is a key consideration. There is a proven risk of poor patient compliance to wearing times of between 20 and 22 hours daily as recommended for proper tooth movement, a risk that is completely eliminated by fixed appliances.

Opportunities: AI-based treatment planning and direct-to-consumer orthodontic monitoring solutions are creating major growth opportunities by improving efficiency and expanding access to orthodontic care.

Treatment-planning software systems powered by artificial intelligence and capable of simulating the treatment, staging the aligner sequences, and identifying any potential biomechanical risks have been found to lower clinician time for each patient and increase the total number of patients an individual orthodontist can handle. Platforms utilizing images from smartphones for remote tracking of tooth movement without necessitating personal meetings are also enhancing the reach of orthodontic care services.

Recent Developments:

-

2025: Align Technology reported Invisalign cumulative treated patients exceeding 15 million globally, with the company's expanded GP dentist training programme certifying over 240,000 general dentists for Invisalign case provision, progressively shifting clear aligner treatment volume from specialist referral to the higher-frequency general dentistry patient access point.

-

2025: 3M Oral Care launched its Clarity Ultra Self-Ligating Bracket System in the United States, featuring tooth-colored ceramic bracket bodies with an integrated low-friction self-ligating clip design targeting aesthetically conscious adult fixed appliance patients who require biomechanical treatment capabilities beyond clear aligner clinical limits.

Orthodontics Market Key Players are:

-

Align Technology Inc.

-

Dentsply Sirona Inc.

-

Envista Holdings Corporation (Ormco)

-

3M Company (Oral Care)

-

Henry Schein Inc.

-

American Orthodontics Corp.

-

DENTAURUM GmbH & Co. KG

-

TP Orthodontics Inc.

-

G&H Orthodontics Inc.

-

Straumann Holding AG

-

Planmeca Oy

-

RMO Inc.

-

AngelAlign (Angelalign Technology Inc.)

-

EasySmile (Zhengzhou Zhenghai Biotech)

-

Spark (Ormco, Envista)

-

SmileStyler (Australian Dental Specialists Group)

-

ClearPath Healthcare Services

-

Invisalign (Align Technology sub-brand)

-

Klear Aligner by Ormco

-

Scheu Dental GmbH

Orthodontics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.54 Billion |

| Market Size by 2035 | USD 27.14 Billion |

| CAGR | CAGR of 12.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Instruments, Supplies, Removable Appliances) • By Age Group (Teens, Adults) • By End User (Dentist & Orthodontist Owned Practices, Hospitals & Dental Clinics, Others) • By Distribution Channel (Direct Sales, Retail Distributors, Online Channels) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Align Technology Inc., Dentsply Sirona Inc., Envista Holdings Corporation (Ormco), 3M Company (Oral Care), Henry Schein Inc., American Orthodontics Corp., DENTAURUM GmbH & Co. KG, TP Orthodontics Inc., G&H Orthodontics Inc., Straumann Holding AG, Planmeca Oy, RMO Inc., AngelAlign (Angelalign Technology Inc.), EasySmile (Zhengzhou Zhenghai Biotech), Spark (Ormco, Envista), SmileStyler (Australian Dental Specialists Group), ClearPath Healthcare Services, Invisalign (Align Technology sub-brand), Klear Aligner by Ormco, Scheu Dental GmbH |

Frequently Asked Questions

North America dominated the Orthodontics Market in 2025, holding approximately 42.90% of global revenues.

The primary growth factors are the structural expansion of adult orthodontic treatment adoption driven by clear aligner technology's patient experience advantages, rising global consumer awareness of orthodontic aesthetics and oral health benefits.

The adults segment dominated the Orthodontics Market with 62.00% share in 2025.

The Orthodontics Market was valued at USD 8.54 Billion in 2025.

The Orthodontics Market is expected to grow at a CAGR of 12.26% from 2026 to 2035.

Get in Touch