Passive Electronic Components Market Report Scope & Overview:

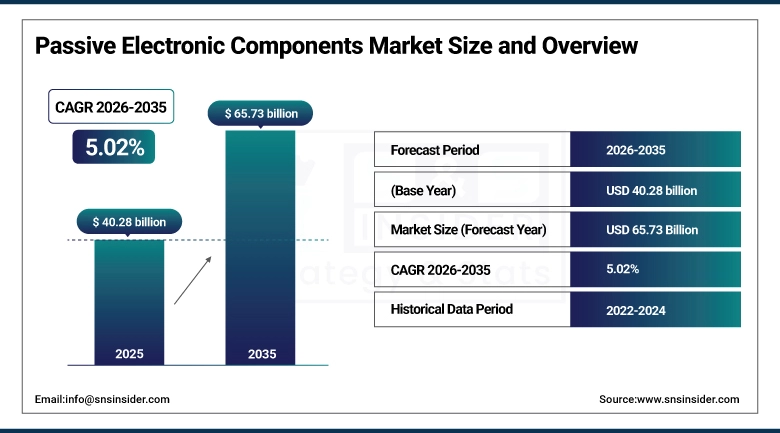

The Passive Electronic Components Market size was valued at USD 40.28 Billion in 2025 and is projected to reach USD 65.73 Billion by 2035, growing at a CAGR of 5.02% during 2026–2035.

The passive electronic components market is thriving in its growth driven by the increasingly demanded need for advanced protection and reliability solutions brought by the needs of the modern electronics systems. Growing implementation of resettable fuses, inductors, capacitors, and other passive components is propelling growth in telecommunication systems, industrial electronics, as well as in power distribution applications. Ris Increasing penetration of high-density circuits, up-scale 5G infrastructure and electric power systems have led to demand for smaller form factors, high performance with better safety and efficiency. This pushes system requirements toward miniaturization, higher voltage handling, and stability of thermal characteristics, which are the current focus of manufacturers. This trend is reinforcing passive components as system protections and operational continuity enablers.

In February , 2026 – Bourns introduced new Multifuse PPTC resettable fuse models under its MF2603 and MF-LSMF series, designed for higher power and voltage protection in compact surface-mount formats. The upgraded devices provide fast overcurrent response, automatic reset capability, and enhanced reliability for telecom, networking, and industrial electronics, improving system safety, reducing maintenance needs, and protecting sensitive components in high-density electronic applications.

Market Size and Growth Forecast:

-

Market Size in 2025: USD 40.28 Billion

-

Market Size by 2035: USD 65.73 Billion

-

CAGR: 5.02% (from 2026 to 2035)

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Passive Electronic Components Market - Request Free Sample Report

Passive Electronic Components Market Highlights:

-

Capacitors, resistors, and inductors remain the core product segments with rising demand for miniaturization.

-

Asia-Pacific dominates production, while North America and Europe show strong technological advancement.

-

Increasing adoption of EVs, renewable energy systems, and smart devices is boosting component usage.

-

Chip-scale and surface-mount technologies are gaining traction for high-density electronic designs.

-

Supply chain resilience and material innovation are key focus areas for manufacturers.

U.S. Passive Electronic Components Market Size Outlook:

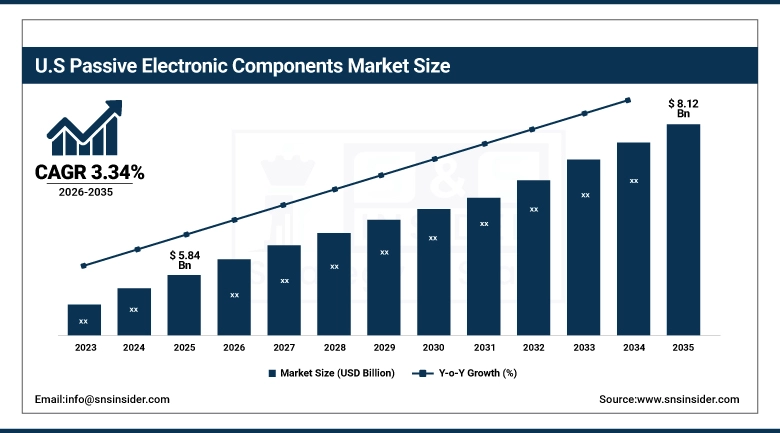

The U.S. Passive Electronic Components Market was valued at USD 5.84 Billion in 2025 and is projected to reach USD 8.12 Billion by 2035, growing at a CAGR of 3.34% during 2026–2035. U.S. backed by increasing demand from automotive electronics, telecommunication, industrial automation, and consumer appliances. Rising adoption of electric vehicles along with advanced driver-assistance systems is driving demand incremental for high-performance capacitors, resistors and inductors. Consumption of components is further aided by an expansion of 5G infrastructure and data centers. Furthermore, heavily investing in renewable energy systems as well as smart grid technologies are expanding the market prospects. On-going advances in miniaturization, reliability and thermal efficiency are fortifying domestic production capabilities Reshoring initiatives and government initiatives to promote manufacturing of advanced electronics and semiconductor ecosystem are also providing support to market.

Passive Electronic Components Market Drivers:

-

Rising Aerospace and Defense Electronics Demand Driving High-Reliability MLCC Growth

The passive electronic components market has been driven by high-reliability multilayer ceramic capacitors (MLCCs) particularly in aerospace and defense applications. An increasing adoption of next-generation military systems, satellite communications, and mission-critical electronics is accelerating demand for these compact, robust, and higher-capacitance components. To meet stringent operational requirements, manufacturers are targeting miniaturization, improved thermal stability, and enhanced mechanical strength. Another growth driver that boosts demand for MIL-grade components is the expansion of global defense modernization programs combined with a host of space exploration missions. Also, the ongoing evolution towards lightweight, high process electronic systems is generating tremendous opportunities for advance capacitor technologies onboard varying environment applications.

In April , 2026 – KYOCERA AVX ELectronic Components (DLA)invests in new case size! KYOCERA AVX Adds New Case Sizes, Increased Capacitance Values to MIL-PRF-32535 BME NP0 MLCC Portfolio Approved by Defense Logistics Agency for Aerospace, Defense Applications Nigatsu's new user-friendly capacitors maximize miniaturization, reliability, and PCB performance to use for satellite, military, and advanced communication equipment applications requiring higher reliability (e.g., filtering, decoupling, and timing) solutions.

Passive Electronic Components Market Restraints:

-

Supply Chain Constraints and Material Volatility Limiting Market Expansion

The key factors restraining the growth of the passive electronic components industry are instability in the prices of raw materials such as ceramic, copper, and rare earth elements used in passive components like capacitors and inductors. Problems with the supply chain, geopolitical tensions are still affecting the global manufacturing and the timely delivery of components. Production.The more reliant you are on Asia-based production hubs, the more you put yourself in a vulnerable position due to macro-regional risks. Moreover, with increased miniature complexity, the research and production costs increases, making it a challenge for less-funded manufacturers to scale up. Moreover, having fierce price competition between major players squeezes profit margins and high-quality and automotive reliability standards raise development timelines and compliance obligations typically.

Passive Electronic Components Market Opportunities:

-

AI-Driven Miniaturization Unlocking Next-Gen Passive Component Growth

Huge opportunity creation driven by rapidly Growing AI chips, Electric Vehicles and Dense Computing systems is driving growth seen in Passive Electronic Components Market. Today, the rapidly growing demand for compact, high-capacitance multilayer ceramic capacitors (MLCCs) and advanced embedded substrate solutions empowers OEMs and ODMs to achieve the high levels of performance and differentiation required for competitive global market placement. Complex circuit architectures are now demanding miniaturization with high integration and better thermal efficiency, which manufacturers are catering. The demand for advanced passive components is further fueled by, and contributing to, the global growth of 5G infrastructure, automotive electrification and AI-based hardware systems. Accordingly, this transition is raising demand for higher-reliability, small footprint components throughout the semiconductor and electronics industries around the world.

In April, 2026 – As demand for advanced AI chips continues to rise, Samsung Electro-Mechanics is said to be in the process of strengthening its AI packaging capabilities by building a new MLCC embedded substrate production line in Vietnam → April,2026 The pact bolsters its demand for semiconductor packaging and increases sharing of dense, high performance parts to drive next-gen AI and computing.

Passive Electronic Components Market Segment Highlights:

-

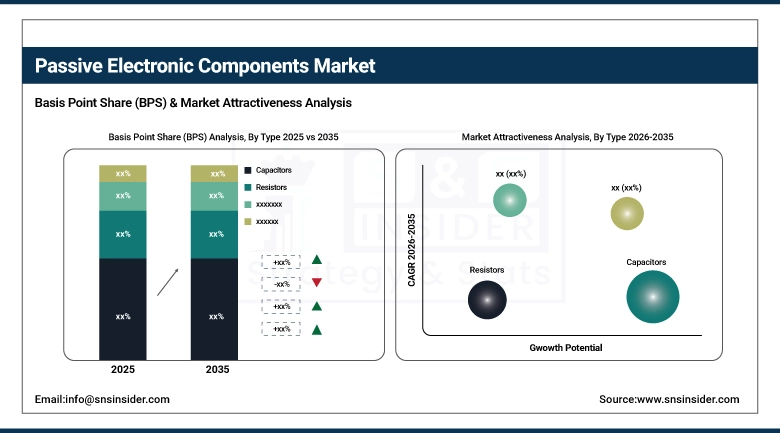

By Type: Dominant – Capacitors (50.37% in 2025 → 53.21% in 2035); Fastest Growing – Inductors (19.49% in 2025 → 18.73% in 2035)

-

By End User: Dominant – Consumer Electronics (39.20% in 2025 → 32.90% in 2035); Fastest Growing – Automotive (23.10% in 2025 → 28.50% in 2035)

-

By Technology: Dominant – Surface Mount Device (SMD) Components (52.37% in 2025 → 51.00% in 2035); Fastest Growing – Chip Scale / Miniaturized Components (21.15% in 2025 → 24.00% in 2035)

-

By Material Type: Dominant – Ceramic-based Components (28.37% in 2025 → 34.37% in 2035); Fastest Growing – Ferrite / Magnetic Core Inductors (10.08% in 2025 → 16.08% in 2035)

Capacitors (Dominant) and Inductors (Fastest-Growing) – By Type

Capacitors segment is estimated to hold the largest share of the passive electronic components market, in terms of value, throughout the forecast period as they are used in numerous applications including consumer electronics, automotive systems, telecommunications, and industrial equipment. Its dominance is bolstered by growth in demand for high-capacitance MLCCs and miniaturized designs, along with suitable energy storage and filtering. With ever-improving electronic devices and greater circuit sophistication, the footprint argument is further bolstered for wider capacitor usage in applications everywhere. However, the fastest growing segment is assumed to be from inductors driven from the increasing demand for power management systems, EV powertrains, 5G infrastructure and high-frequency applications. The increasing requirement of energy conversion, noise suppression and compact magnetic components across the globe is driving the demand for inductor at a whooping pace.

Consumer Electronics (Dominant) and Automotive (Fastest-Growing) – By End User

The consumer electronics segment is projected to continue to dominate, catalyzed by extensive penetration of smart phones, laptops, wearables and home appliances that cater heavily on passive electronic component. Its leading position is further cemented due to continuous innovation, miniaturization of products, and massive production cycles. The highest growth, however, is expected in the automotive segment, primarily driven by rapid electrification, increased adoption of EV and higher integration of ADAS and in-vehicle electronics. The demand for passive components among the next-generation of vehicles is growing rapidly due to increased use of capacitors, inductors, and sensors in safety, infotainment, and power management systems.

Surface Mount Device (SMD) Components (Dominant) and Chip Scale / Miniaturized Components (Fastest-Growing) – By Technology

The region will remain the largest and fastest growing segment of the SMD components market due to the dominance of compact, high-density electronic circuits in the consumer, automotive and industrial applications. This market dominance is also strengthened by their ease-of-products assembly, economical and suitability to automated manufacturing systems. Nevertheless, chip scale and miniaturized components are estimated to witness the fastest growth rate due to the rising need of ultra-compact, high-performance electronic systems. The new IoT devices, wearables, and advanced computing systems are driving manufacturers toward passive devices that are smaller, more efficient yet functional in less space.

Ceramic-based Components (Dominant) and Ferrite / Magnetic Core Inductors (Fastest-Growing) – By Material Type

ceramic-based components are projected to account for the largest share as they find significant application in capacitors, insulation applications and high-frequency electronic systems. They form a critical part of consumer electronics, automotive, and telecom industries given their stability, long life and cost effectiveness. On the other hand, the ferrite and magnetic core inductors is expected to achieve the highest growth rate as these components find their application for efficient power conversion, energy storage and electromagnetic interference suppression. The rapid growth in deployment of EVs, renewable energy systems and high−power electronics applications fuels the adoption of advanced magnetic materials into next−generation electronic designs.

Passive Electronic Components Market Regional Highlights:

-

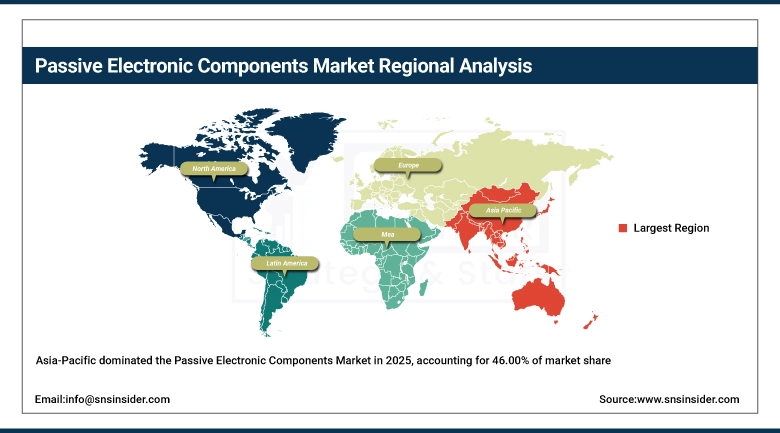

Asia-Pacific (Dominating – 46.00% in 2025 → 52.00% in 2035, CAGR 6.31%)

-

North America (22.00% in 2025 → 19.00% in 2035, CAGR 3.48%)

-

Europe (20.00% in 2025 → 17.00% in 2035, CAGR 3.32%)

-

Latin America (6.00% in 2025 → 5.00% in 2035, CAGR 3.11%)

-

Middle East & Africa (6.00% in 2025 → 7.00% in 2035, CAGR 6.64%)

Asia-Pacific Passive Electronic Components Market Insights:

The passive electronic components market is dominated by Asia Pacific region because of high demand for electronics manufacturing, strong potential semiconductor, and high OEMs companies in China, Japan, South Korea, and Taiwan. Regional domination is further reinforced by rapid growth in consumer electronics, automotive electronics, and 5G infrastructure. Similarly, demand is also enhanced due to the growing industrial automation and government support for localizing electronics production. Low-cost manufacturing capabilities and large-scale supply chain networks further position Asia Pacific as a center for passive component production and consumption globally, strengthening its leadership in the global passive electronic components market.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Passive Electronic Components Market Insights:

China is the leading country here, since China has one of the strongest electronic manufacturing sectors in the world alongside an increasing demand for consumer devices owing to which it is a rapid growing market, along with the 5G expansion and EV growth. This further solidifies its edge in the global passive electronic components industry with the government backing and high production volume.

North America Passive Electronic Components Market Insights:

Passive Electronic Components Market in North America is anticipated to offer lucrative opportunities for passive electronic component manufacturers owing to growing demand for advanced electronics, and robust adoption of automotive electronics and 5G infrastructure in the region, making it one of the fastest growing region in the passive electronic components market over the anticipated period. High-performance passive components are found in many sectors of the current market, and growing investments in electric vehicles, aerospace, and defense systems are only adding to the demand in the region. On account of such factors rapid expansion of data centers and industrial automation is increasing component consumption. In addition, accelerating market growth throughout the US and Canada further contributes to government support of domestic semiconductor manufacturing and bolsters resilience in the supply chain.

U.S. Passive Electronic Components Market Insights:

The U.S. passive electronic components market dominates due to strong demand from automotive, aerospace, defense, and electronics sectors, supported by 5G expansion, EV growth, and increasing semiconductor manufacturing investments.

Europe Passive Electronic Components Market Insights:

Growing demand from automotive electronics, industrial automation, and renewable energy systems is contributing to a gradual expansion of the Europe passive electronic components market. The growing adoption of electric vehicles and advanced driver assistance systems (ADAS) is also leading to a booming consumption of components across the region. Rise in investments in 5G infrastructure coupled with demand of aerospace and defense technologies are also anticipated to fuel the need for high-performance passive components. The rigorous energy efficiency and sustainable electronics measures initiated in European Union (EU), are also buttressing the market growth. The European passive electronic components market continues to be primarily driven by the ongoing growth of semiconductor manufacturing initiatives and digital transformation across various industries.

Germany Passive Electronic Components Market Insights:

Germany’s passive electronic components market is growing industrial automation and the uptrend in investments towards Industry 4.0 and smart manufacturing technologies, the passive electronic components market in Germany holds a significant share in the European market.

Latin America Passive Electronic Components Market Insights:

The Latin America passive electronic components market is slowly picking momentum as their adaptability is getting high across a wide range of electrical systems such as consumer electronics, automotive electronics, and growing telecommunications infrastructure. Evolving investments are investing in 4G and forthcoming 5G networks to stimulate capacitors, resistors, and inductors industry requirements. New usage of components through manufacturing sectors too, is supported through industrial automation and renewable energy projects. The rise of urbanization and digital transformation in the likes of Brazil and Mexico also helps market growth. Additionally, government efforts to enhance the capabilities of electronics manufacturing and foreign direct investment (FDI) in regional production facilities are boosting overall market growth.

Brazil Passive Electronic Components Market Insights:

Brazil is the largest market in Latin America’s passive electronic components industry due to strong automotive production, expanding consumer electronics demand, and growing telecom infrastructure investments. Industrial modernization and increasing adoption of renewable energy systems further support component consumption and market growth in the country.

Middle East & Africa Passive Electronic Components Market Insights:

The Passive Electronic Component Market in Middle East & Africa is experiencing steady growth attributed to rising investments in sectors such as telecom, consumer electronics, and industrial automation. Additionally, rising adoption of renewable energy projects and smart grid systems is boosting component usage. Furthermore, increased penetration of renewable energy projects coupled with the development of a smart grid systems, continues to proliferate utilization of the components. Rising construction activities, increasing urbanization, and diversification of economies from oil dependency are also aiding the market growth. Furthermore, government subsidies for domestic production and foreign investments in electronics industries boost the overall passive electronic components market in the region.

Saudi Arabia Passive Electronic Components Market Insights:

The passive electronic components market in Saudi Arabia is expanding due to the increasing telecommunications infrastructure, rising adoption of consumer electronics, growing industrial automation, and robust investments in smart city and digital transformation projects.

Passive Electronic Components Market Competitive Landscape:

Murata Manufacturing Co., Ltd. was established in 1944 and is a world-leading electronic components manufacturer based in Japan. The company's main products include multilayer ceramic capacitors (MLCCs), sensors and communication modules. The company now serves automotive, consumer electronics, and industrial markets and enables global innovation in miniaturization, connectivity and high-performance passive electronic components.

-

In April 2026 – Murata Manufacturing Co., Ltd. announced the mass production of seven automotive-grade MLCCs with world-leading capacitance for their rated voltage and size, targeting ADAS and autonomous driving systems. These AEC-Q200-qualified components improve capacitance density, reduce PCB space usage by up to 61%, and enhance power stability and design flexibility in next-generation in-vehicle electronic systems.

TDK Corporation, established in 1935, is a Japan-based global leader in electronic components. The company specializes in inductors, capacitors, magnetic devices, and sensors. It serves automotive, industrial, and consumer electronics markets, focusing on advanced passive components that enhance energy efficiency, miniaturization, and high-performance electronic system integration worldwide.

-

In July 2025 – TDK Corporation has extended its TFM201612BLEA series of thin-film power inductors for automotive applications to higher rated current with up to 5.6 A rating at >96% efficiency and with a 31% reduction in DC resistance. The new inductors, designed for EV & ADAS power circuits, offer high-reliability under harsh conditions and operate at up to +150°C, making them suitable for compact, high-performance automotive electronic systems.

Passive Electronic Components Companies are:

-

TDK Corporation

-

Vishay Intertechnology, Inc.

-

Yageo Corporation

-

Samsung Electro-Mechanics

-

Taiyo Yuden Co., Ltd.

-

KEMET Corporation (Yageo Group)

-

Walsin Technology Corporation

-

Panasonic Industry Co., Ltd.

-

Nippon Chemi-Con Corporation

-

Nichicon Corporation

-

Rubycon Corporation

-

Eaton Corporation plc

-

TE Connectivity Ltd.

-

Coilcraft, Inc.

-

Bourns, Inc.

-

AVX Corporation

-

Johanson Technology, Inc.

-

Delta Electronics, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 40.28 Billion |

| Market Size by 2035 | USD 65.73 Billion |

| CAGR | CAGR of 5.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type(Capacitors, Resistors and Inductors) • By End User(Consumer Electronics, Automotive, Healthcare, Telecommunications, Aerospace, Defense and Others) • By Technology(Surface Mount Device (SMD) Components, Through-Hole Components, Chip Scale / Miniaturized Components and Hybrid / Integrated Passive Devices (IPDs)) • By Material Type(Ceramic-based Components, Tantalum-based Components, Aluminum Electrolytic Components, Film-based Components (Polyester, Polypropylene, etc.), Carbon / Metal Film Resistors and Ferrite / Magnetic Core Inductors) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Murata Manufacturing Co., Ltd., TDK Corporation, Vishay Intertechnology, Inc., Yageo Corporation, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd., KYOCERA AVX Components Corporation, KEMET Corporation (Yageo Group), Walsin Technology Corporation, Panasonic Industry Co., Ltd., Nippon Chemi-Con Corporation, Nichicon Corporation, Rubycon Corporation, Eaton Corporation plc, TE Connectivity Ltd., Coilcraft, Inc., Bourns, Inc., AVX Corporation, Johanson Technology, Inc., Delta Electronics, Inc. |

Frequently Asked Questions

Asia-Pacific dominated the Passive Electronic Components Market in 2025.

The “Capacitors” segment dominated during the projected period.

The passive electronic components market is driven by rising demand for EVs, 5G infrastructure, consumer electronics, industrial automation, renewable energy systems, and continuous miniaturization of high-performance electronic devices.

The Market was valued at USD 40.28 Billion in 2025 and is projected to reach USD 65.73 Billion by 2035.

The Market is expected to grow at a CAGR of 5.02% during 2026–2035.

Get in Touch