Personalized Cancer Vaccine Market Report Scope & Overview:

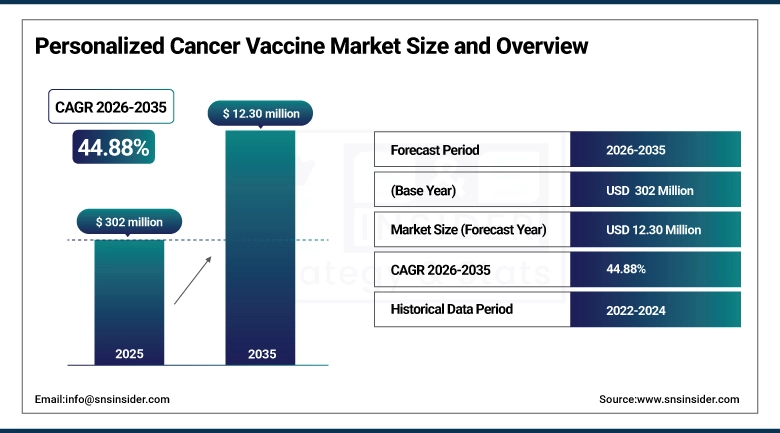

The Personalized Cancer Vaccine Market was valued at USD 302 million in 2025 and is expected to reach USD 12.30 billion by 2035, growing at a CAGR of 44.88% from 2026–2035.

The global personalized cancer vaccine market finds itself at one of the most disruptive inflection points that have been witnessed in the history of cancer, with the combination of mRNA vaccine technology, genomic sequencing technologies, AI-based neoantigen identification and precision medicine leading the way for the creation of treatments that are precisely designed to address each individual's unique tumor mutation profile. Whereas traditional forms of cancer treatments involve delivering the exact same formulation of drugs across all patients diagnosed with that particular type of cancer, personalized cancer vaccines can be created based on the tumor's genetic sequencing, where its distinct neoantigens that arise due to mutations within its genome can be identified, used to create a personalized vaccine formulation, and administered into the patient to train their body's immune system against those unique biomarkers. Precision oncology has been under development for more than ten years and is currently poised for an inflection point in terms of commercialization, thanks to significant clinical successes that have been made, such as the FDA awarding the Breakthrough Therapy designation to the Moderna/Merck mRNA-4157/V940 personalized neoantigen vaccine for high-risk resected melanoma, with a 49% reduced risk of recurrence or death compared to pembrolizumab alone.

The CAGR of 44.88% anticipated for the Personalized Cancer Vaccine Market between 2026 and 2035 is attributable to the compounded growth of an emerging technology platform entering clinical maturity, characterized by positive readouts from late-stage clinical trials conducted by companies such as Moderna, BioNTech, and Gritstone Bio, which will result in the momentum required from a regulatory perspective to approve commercial launch, enable insurance coverage, and drive hospital adoption, scaling revenues from initial commercialization in 2025 to billions of dollars in 2035.

Personalized Cancer Vaccine Market Size and Forecast:

-

Market Size in 2025: USD 302 Million

-

Market Size by 2035: USD 12.30 Billion

-

CAGR: 44.88% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Personalized Cancer Vaccine Market - Request Free Sample Report

Personalized Cancer Vaccine Market Trends

-

Accelerating clinical progress of mRNA-based personalized cancer vaccines, with Moderna and Merck's mRNA-4157/V940 demonstrating a 49% reduction in melanoma recurrence risk and now advancing into additional indication studies across lung cancer, colorectal cancer, and renal cell carcinoma.

-

Growing integration of AI and machine learning into neoantigen prediction workflows, enabling faster and more accurate identification of immunogenic tumor-specific antigens from whole-exome sequencing data, reducing vaccine design timelines from months toward weeks.

-

Rising adoption of combination therapy approaches pairing personalized cancer vaccines with immune checkpoint inhibitors including pembrolizumab and nivolumab, with clinical evidence demonstrating synergistic immune activation that produces superior outcomes compared to either modality alone.

-

Expanding clinical investigation of personalized vaccines across a broadening range of cancer types including non-small cell lung cancer, microsatellite-stable colorectal cancer, pancreatic cancer, and glioblastoma, extending the addressable patient population beyond the initial melanoma focus.

-

Rapid decline in genomic sequencing costs, with whole-exome sequencing now achievable at under USD 1,000 per patient, making the foundational genomic analysis required for personalized vaccine design increasingly economically accessible for widespread clinical application.

-

Growing investment in automated, modular personalized vaccine manufacturing platforms that can produce individual patient-specific vaccine constructs within clinically acceptable turnaround times of two to four weeks using standardised lipid nanoparticle formulation technologies.

-

Increasing number of breakthrough therapy designations, priority review vouchers, and accelerated regulatory approvals for personalized cancer vaccine candidates, reflecting global regulatory bodies' recognition of the transformative therapeutic potential in this category.

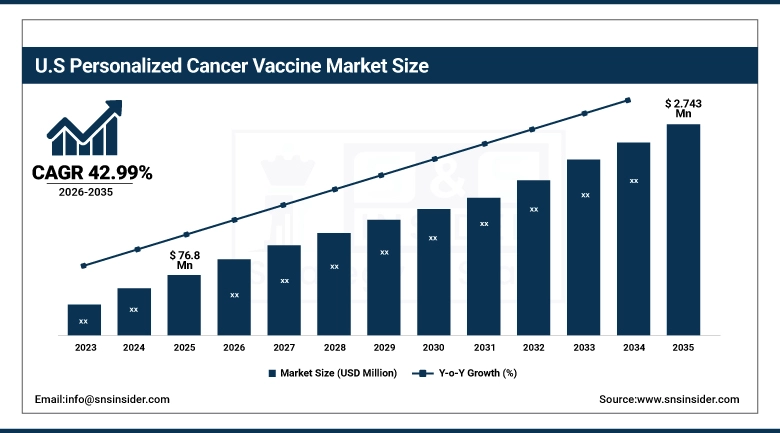

The U.S. Personalized Cancer Vaccine Market was valued at USD 76.8 million in 2025 and is expected to reach USD 2.743 billion by 2035, registering a CAGR of 42.99% during 2026–2035.

U.S. is considered the most technologically advanced market for personalized cancer vaccines along with being commercially relevant due to the high number of clinical trials conducted in this country, an extensive budget of the National Cancer Institute for cancer-focused research & development exceeding USD 7.2 billion in 2024, and the leading companies that develop personalized vaccines in the world like Moderna, Gritstone Bio, and Nouscom being situated there. Given the ability of the American healthcare system to invest highly in oncology, together with the proven track record in covering cancer breakthrough treatments with insurance payments, the country has an excellent potential to overcome the high costs associated with personalized vaccines during the launch period. FDA breakthrough therapy designations for some top players' products like mRNA-4157/V940 ensure a smooth regulatory path ahead.

The National Cancer Institute's USD 7.2 billion cancer R&D budget in 2024, combined with Moderna and Merck's continued advancement of mRNA-4157/V940 through Phase 2 and toward Phase 3 clinical development, and Gritstone Bio's November 2024 interim Phase 2 results for its GRANITE personalized neoantigen vaccine showing a 27% relative reduction in progression or death in microsatellite-stable colorectal cancer, collectively confirm that the U.S. is generating the clinical evidence base that will support commercial launch approval and rapid insurance coverage adoption across the major personalised cancer vaccine candidates through the 2026 to 2035 forecast period.

Personalized Cancer Vaccine Market Segment Insights

-

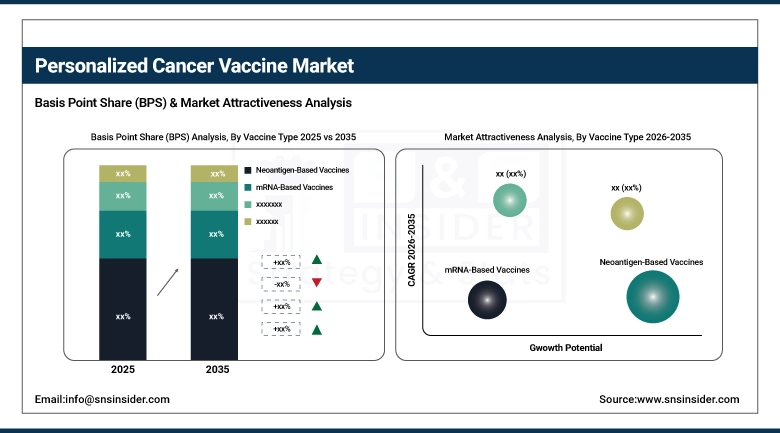

According to Vaccine Type, Neoantigen-Based Vaccines dominated with approximately 48% revenue share in 2025 and are also expected to grow at the fastest CAGR during the forecast period due to strong pipeline advancements and precision antigen targeting efficacy.

-

In terms of Cancer Type, Melanoma held the largest revenue share of approximately 26% in 2025; Lung Cancer is the fastest-growing cancer type with the highest CAGR driven by its rising global incidence and strong pipeline expansion.

-

By Technology Platform, mRNA-based platforms held approximately 38% revenue share in 2025 and are expected to grow at the fastest CAGR driven by manufacturing scalability and proven clinical efficacy advantages.

-

By Treatment Approach, Combination Therapy dominated with approximately 66% revenue share in 2025 and is expected to maintain the fastest growth as evidence of synergistic immune activation with checkpoint inhibitors accumulates across multiple tumor types.

By Vaccine Type, Neoantigen-Based Vaccines dominate and expected to grow fastest

Neoantigen vaccines were estimated to have a market share of nearly 48% of the Personalized Cancer Vaccines market in 2025 due to their intrinsic relevance to the precision oncology concept, wherein the vaccine is developed using the patient-specific somatic mutations in the tumor. Neoantigen vaccines target the exact protein sequences that are uniquely expressed only in cancer cells and not in healthy cells, making the vaccine highly efficient in targeting cancer cells while causing minimal toxicity to other cells. The proof-of-concept provided by the clinical trial results of Moderna and Merck's mRNA-4157/V940 program is regarded as the strongest demonstration thus far that neoantigen-based vaccines are capable of generating tangible results for patients and setting benchmarks for future neoantigen vaccines. The continued development pipeline for neoantigen vaccines and the increasing use of AI-based prediction methods to select neoantigens with higher immunogenicity potential are contributing factors to the sustained commercial success of neoantigen vaccines.

mRNA-based vaccines represent both the fastest-growing platform technology and the most scalable manufacturing pathway for personalised cancer vaccines, inheriting the extraordinary manufacturing infrastructure developed during the COVID-19 pandemic. mRNA vaccine platforms enable rapid sequence-to-synthesis turnaround, highly flexible multi-antigen encoding within a single construct, and demonstrated lipid nanoparticle delivery efficacy that has been validated across billions of vaccine doses administered globally. The combination of clinical efficacy data, manufacturing scalability, and the growing ecosystem of mRNA delivery optimisation research positions mRNA-based personalised cancer vaccines as the dominant commercial platform through the 2035 forecast horizon.

By Cancer Type, Melanoma dominates, Lung Cancer expected to grow fastest

Melanoma retained the largest cancer type revenue share at approximately 26% of the Personalized Cancer Vaccine Market in 2025, reflecting its status as the lead indication for personalised cancer vaccine clinical development. Melanoma's high mutational burden relative to most other solid tumors makes it particularly suitable for neoantigen-based vaccines, as more somatic mutations generate a larger pool of potential neoantigens that can be selected for vaccine construction. The clinical success of mRNA-4157/V940 in resected stage III and IV melanoma has validated melanoma as the reference indication for personalised vaccine development and has defined the regulatory approval pathway that subsequent programs in other indications are using as their blueprint.

Lung Cancer is projected to be the fastest-growing cancer type segment through 2035, driven by its extraordinary global incidence as the leading cause of cancer mortality worldwide, the growing identification of neoantigen-rich molecular subtypes responsive to immunotherapy, and the strong clinical pipeline of personalised vaccine programs being investigated in non-small cell lung cancer as an adjuvant to PD-1 blockade. The clinical and commercial opportunity in lung cancer vastly exceeds that of melanoma given the far greater patient population, and the first clinical successes demonstrating personalised vaccine benefit in lung cancer will trigger a rapid market expansion that will fundamentally reshape the personalised cancer vaccine market's revenue mix through the forecast period.

Personalized Cancer Vaccine Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~85% |

|

Europe |

Germany |

~32% |

|

Asia Pacific |

China |

~44% |

|

Middle East & Africa |

UAE |

~26% |

|

Latin America |

Brazil |

~42% |

North America Personalized Cancer Vaccine Market Insights

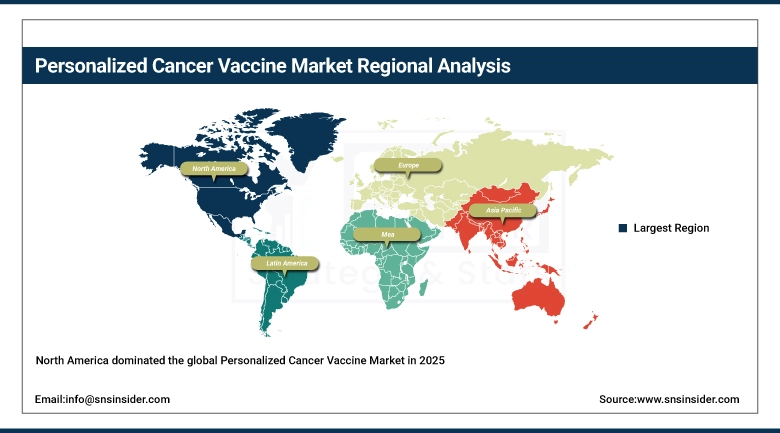

North America dominated the global Personalized Cancer Vaccine Market in 2025, led overwhelmingly by the United States with approximately 85% of North American revenues. U.S. market leadership is underpinned by the world's most advanced cancer immunotherapy research ecosystem, the highest NCI funding for cancer research globally, the commercial presence of leading personalized vaccine developers including Moderna, Gritstone Bio, and Nouscom, and the most favourable regulatory environment for breakthrough cancer therapy designations. Canada is emerging as a complementary market through its supportive AI-driven drug discovery regulatory environment and strong academic-industry partnerships in precision oncology.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Personalized Cancer Vaccine Market Insights

Europe represents the second-largest regional market for personalized cancer vaccines, supported by strong collaborative research networks through the European Cancer Organisation and ECOG-ACRIN, the European Medicines Agency's PRIME designation pathway that has already been applied to Moderna and Merck's mRNA-4157/V940 in advanced melanoma, and the concentration of leading cancer genomics research centers in Germany, the UK, France, and the Netherlands. Germany leads European market development through its advanced precision oncology clinical infrastructure and the commercial presence of BioNTech, one of the world's leading personalised mRNA vaccine developers, within its scientific ecosystem.

Asia Pacific Personalized Cancer Vaccine Market Insights

Asia Pacific is projected to grow at the fastest regional CAGR through 2035, driven by rapidly expanding cancer burden across China, India, Japan, and South Korea, increasing government investment in precision medicine and genomic medicine infrastructure, and growing academic-industry collaboration in cancer immunotherapy research. China's substantial domestic biotech investment in mRNA platform development and neoantigen vaccine research is creating an increasingly sophisticated domestic personalised vaccine pipeline. Japan's advanced regulatory pathway for regenerative and cellular therapies provides a supportive framework for personalised cancer vaccine approval that is accelerating clinical development investment in the country.

Middle East & Africa and Latin America Personalized Cancer Vaccine Market Insights

MEA and Latin America represent early-stage but growing personalized cancer vaccine markets, with adoption initially concentrated in premium private oncology centres and academic medical centres with genomic medicine capabilities. The UAE leads MEA adoption through its advanced healthcare system and growing investment in precision medicine infrastructure, while Saudi Arabia's Vision 2030 health sector initiatives are creating expanding genomic medicine capabilities. Brazil leads Latin American market participation through its well-developed private oncology sector and growing academic cancer research programmes in collaboration with U.S. and European institutions.

Personalized Cancer Vaccine Market Growth Drivers:

-

Clinical validation of mRNA neoantigen vaccine efficacy and breakthrough therapy regulatory designations accelerating commercial development timelines

The primary structural growth driver for the Personalized Cancer Vaccine Market is the compounding momentum of positive clinical trial readouts validating the core scientific hypothesis that patient-specific neoantigen vaccines can generate durable, clinically meaningful anti-tumor immune responses. Moderna and Merck's mRNA-4157/V940 demonstrating a 49% reduction in melanoma recurrence risk, Gritstone Bio's GRANITE vaccine showing a 27% relative reduction in colorectal cancer progression or death, and February 2025 Dana-Farber data confirming durable anti-tumor immunity in all nine renal cell carcinoma patients with zero recurrences at median 34.7-month follow-up collectively establish a multi-indication evidence base that is rapidly building the regulatory and commercial foundation for personalised cancer vaccine approvals through the forecast period.

Evaxion's May 2025 confirmation of dosing the first patient in the one-year extension of its Phase 2 EVX-01 trial targeting advanced melanoma, combined with the Icahn School of Medicine's March 2025 Phase 1 data on PGV001 demonstrating safety and immunogenicity in a personalised multi-peptide neoantigen vaccine, confirm that the personalised cancer vaccine clinical development pipeline spans multiple companies and platforms across the maturity spectrum, creating a self-reinforcing scientific momentum that sustains investor confidence, regulatory engagement, and commercial development investment through the 2026 to 2035 forecast period.

Personalized Cancer Vaccine Market Restraints

-

High manufacturing complexity and cost, lengthy individual vaccine production timelines, and reimbursement pathway uncertainty for novel precision oncology therapies

A significant restraint on the Personalized Cancer Vaccine Market is the inherent manufacturing complexity of producing a unique vaccine construct for each individual patient within a clinically acceptable timeframe. The process requires tumor biopsy, whole-exome sequencing, bioinformatic neoantigen prioritization, sequence-to-synthesis conversion, formulation, quality control, and delivery to the treating institution, each representing a potential bottleneck that can delay treatment initiation in a population of cancer patients where time to treatment is clinically significant. The very high per-patient manufacturing costs associated with this fully customised production process will require novel reimbursement frameworks that insurers, health technology assessment bodies, and government healthcare programmes have not yet fully developed. Uncertainty around coverage and reimbursement pathways in markets outside the U.S. may slow commercial uptake in the early commercial launch phase.

Personalized Cancer Vaccine Market Opportunities

-

Adjuvant treatment expansion, combination immunotherapy programmes, and cancer prevention vaccine development

The adjuvant treatment setting, where personalised cancer vaccines are administered following curative-intent surgery to reduce recurrence risk in patients with resected early-stage tumors, represents the most immediately accessible large-scale commercial opportunity for personalised cancer vaccines, with patient populations across multiple solid tumor types numbering in the hundreds of thousands annually in the U.S. alone. The combination of personalised vaccines with existing immune checkpoint inhibitors is generating clinical synergies that exceed the efficacy of either modality independently, creating premium combination therapy pricing opportunities. The long-term potential for personalised cancer vaccines administered in a minimal residual disease or cancer interception setting represents a transformative prevention market opportunity that could ultimately reach patient populations far larger than those currently qualifying for adjuvant treatment.

Recent Developments:

-

May 2025: Evaxion confirmed dosing the first patient in the one-year extension of its Phase 2 EVX-01 trial targeting advanced melanoma, designed to assess long-term immune durability and monitor clinical outcomes up to three years post-vaccination.

-

March 2025: The Icahn School of Medicine at Mount Sinai released Phase 1 data on PGV001, a personalised multi-peptide neoantigen vaccine, demonstrating safety and immunogenicity across multiple tumor types and supporting advancement into Phase 2 combination studies.

Personalized Cancer Vaccine Market Key Players:

-

Moderna Inc.

-

BioNTech SE

-

Merck & Co. Inc.

-

Gritstone Bio Inc.

-

Nouscom S.r.l.

-

Evaxion Biotech A/S

-

CureVac SE

-

Immatics N.V.

-

NantKwest Inc. (ImmunityBio)

-

Personalis Inc.

-

Genocea Biosciences Inc.

-

ISA Pharmaceuticals BV

-

Transgene SA

-

Neogene Therapeutics Inc.

-

Achilles Therapeutics plc

-

Astellia (Novartis)

-

OSE Immunotherapeutics

-

Agenus Inc.

-

Neon Therapeutics (BioNTech)

-

Roche Holding AG

Personalized Cancer Vaccine Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 302 Million |

| Market Size by 2035 | USD 12.30 Billion |

| CAGR | CAGR of 44.88% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Vaccine Type (mRNA-Based Vaccines, Neoantigen-Based Vaccines, Dendritic Cell Vaccines, Peptide-Based Vaccines, Others) •By Cancer Type (Melanoma, Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Others) •By Technology Platform (mRNA PCV, Cell-Based, Others) •By Treatment Approach (Monotherapy, Combination Therapy) •By End-User (Hospitals, Cancer Research Centers, Biotechnology and Pharmaceutical Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Moderna Inc., BioNTech SE, Merck & Co. Inc., Gritstone Bio Inc., Nouscom S.r.l., Evaxion Biotech A/S, CureVac SE, Immatics N.V., NantKwest Inc. (ImmunityBio), Personalis Inc., Genocea Biosciences Inc., ISA Pharmaceuticals BV, Transgene SA, Neogene Therapeutics Inc., Achilles Therapeutics plc, Astellia (Novartis), OSE Immunotherapeutics, Agenus Inc., Neon Therapeutics (BioNTech), and Roche Holding AG |

Frequently Asked Questions

The Personalized Cancer Vaccine Market is expected to grow at a CAGR of 44.88% from 2026 to 2035.

The Personalized Cancer Vaccine Market was valued at USD 302 million in 2025.

Neoantigen-Based Vaccines dominated the market in 2025 with approximately 48% of revenues, driven by their direct alignment with the precision oncology paradigm, strong clinical pipeline support, and compelling clinical evidence of tumor-specific immune activation with minimal off-target toxicity.

Lung Cancer is expected to grow at the fastest CAGR through 2035, driven by its status as the leading cause of cancer mortality globally creating the largest potential patient population, the growing identification of neoantigen-rich lung cancer subtypes responsive to immunotherapy, and an expanding clinical pipeline of personalised vaccine programs in non-small cell lung cancer.

North America dominated the Personalized Cancer Vaccine Market in 2025, led by the United States with approximately 85% of North American revenues, driven by the world's highest NCI cancer research budget, the most active personalised vaccine clinical development ecosystem, and the most favourable regulatory environment for breakthrough cancer therapy designations.

Get in Touch