Healthcare Distribution Market Report Scope & Overview:

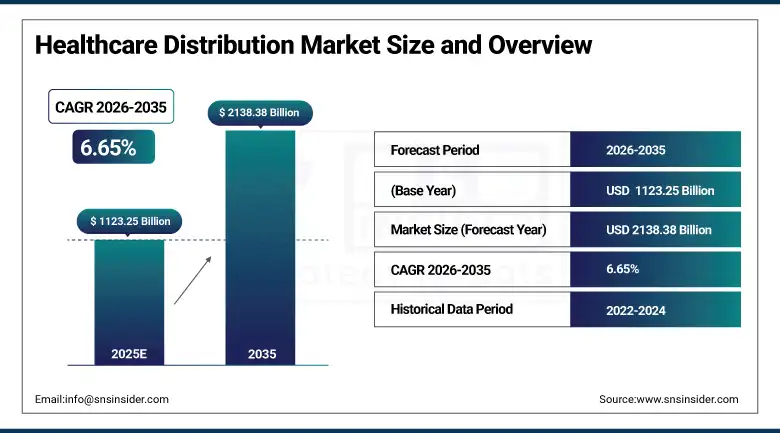

The Healthcare Distribution Market size is estimated at USD 1123.25 Billion in 2025 and is expected to reach USD 2138.38 Billion by 2035, growing at a CAGR of 6.65% over the forecast period of 2026-2035.

The global market for healthcare distribution is experiencing a steady growth rate due to an increase in demand for pharmaceuticals, biologics, and medical devices in healthcare systems around the globe. The increased cost of healthcare, pharmaceutical manufacturing activities, and access to pharmaceuticals are contributing to strengthening demand for healthcare distribution services. Additionally, the increased demand for specialty pharmaceuticals and biologics that demand special handling and storage conditions are fueling market growth.

Moreover, technological innovations are assisting to reshape the healthcare distribution landscape, supplying chain administration technologically, warehousing technological innovation, and digital logistics technological innovation. In supply chain but integration of data analytics, blockchain technology and advanced inventory management tools is allowing distributors to have better product visibility, reduce the risk of disruptions within the supply chain, and meet compliance requirements with regulations such as drug serialization and track and trace. Lack of scale in the pharmaceutical distribution industry, along with collaborations between distributors and manufacturers, is driving supply chain efficiencies and widening the scope of market presence.

In March 2025, a major pharmaceutical distribution network in the United States reported that the adoption of automated warehouse robotics improved order processing speed by nearly 35%, significantly enhancing supply chain efficiency for hospitals and retail pharmacies.

Healthcare Distribution Market Size and Forecast:

-

Market Size in 2025: USD 1123.25 Billion

-

Market Size by 2035: USD 2138.38 Billion

-

CAGR: 6.65% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Healthcare Distribution Market - Request Free Sample Report

Healthcare Distribution Market Trends:

-

Growing adoption of automated warehouse management systems and robotics in pharmaceutical distribution centers to improve operational efficiency.

-

Increasing demand for cold chain logistics solutions to support distribution of biologics, vaccines, and temperature-sensitive pharmaceuticals.

-

Expansion of specialty drug distribution channels driven by the rising prevalence of chronic diseases and biologic therapies.

-

Implementation of digital supply chain platforms for real-time inventory tracking and predictive demand forecasting.

-

Increasing regulatory focus on drug serialization and track-and-trace systems to prevent counterfeit medicines.

-

Growing consolidation among healthcare distributors through mergers, acquisitions, and strategic partnerships.

-

Rising use of data analytics and AI-enabled logistics optimization to enhance distribution efficiency and reduce operational costs.

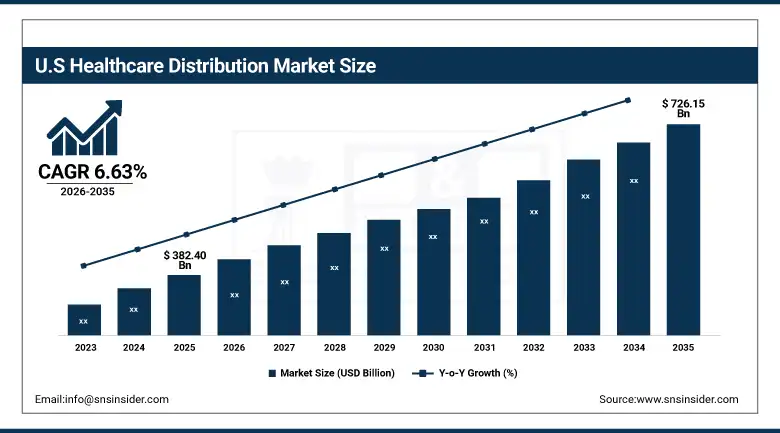

The U.S. Healthcare Distribution Market is estimated at USD 382.40 billion in 2025 and is expected to reach USD 726.15 billion by 2035, growing at a CAGR of 6.63% from 2026-2035. The US dominates the global market for healthcare distribution due to its well-developed pharmaceutical supply chain infrastructure, strong presence of key pharmaceutical distributors, and high levels of healthcare spending. Widespread use of digital supply chain technologies, retail pharmacy networks, and strong regulatory environments that support drug safety and traceability are also major contributors to market growth in the US.

Healthcare Distribution Market Growth Drivers:

-

Growing Pharmaceutical Production and Expanding Global Supply Chains Driving Market Growth

The constant expansion of pharmaceutical manufacturing, as well as the growing need for drugs in the global market, are significant contributors to the healthcare distribution market. Pharmaceutical distribution companies have an essential role to play in facilitating the smooth distribution of drugs, biologics, and medical devices from the manufacturer to the hospital, retail pharmacies, and healthcare facilities. In addition, the growing prevalence of chronic diseases like cardiovascular diseases, diabetes, and cancer has also fueled the need for drugs, thus strengthening the need for distribution services.

In addition also, the global pharmaceutical supply is more sophisticated and requires the distributors to use advanced technology in warehousing and transportation. Logistics management with temperature-controlled supply chains, warehouse automation, and supply chain monitoring technology have harnessed distributors to enhance the quality of goods and track compliance with regulations. These reforms have massively improved the productivity and the growth of the healthcare distribution market.

For example, in January 2025, a large pharmaceutical distributor implemented advanced predictive analytics for demand forecasting, reducing inventory shortages by nearly 28% across its national pharmacy distribution network.

Healthcare Distribution Market Restraints:

-

Supply Chain Disruptions and Regulatory Compliance Challenges Limiting Market Expansion

However, this market is facing various challenges, mainly in terms of supply chain disruptions. There are various stakeholders in the global healthcare supply chain, including manufacturers, distributors, wholesalers, and healthcare providers. These supply chains are often prone to transportation problems, inventory problems, and geopolitical issues. There are also issues related to changes in drug price regulations.

However, this market faces different challenges, especially in terms of supply chain disruptions. There are different stakeholders in the global healthcare supply chain. They include manufacturers, distributors, wholesalers, and healthcare providers. These supply chains are often exposed to different issues like transportation problems, inventory problems, and geopolitical problems. There are also issues concerning changes in drug price regulations.

Healthcare Distribution Market Opportunities:

-

Expansion of Specialty Pharmaceutical Distribution and Biologic Therapies Creating Growth Opportunities

The rapid expansion of specialty pharmaceuticals and biologic therapies presents Further, healthcare distribution companies could benefit from the growth of specialty pharmaceuticals and biologic therapies. Biologics, including monoclonal antibodies, recombinant proteins, and gene therapies, have distinct storage requirements that result in temperature-controlled transportation services during the distribution cycle. As new biologic therapies for complex diseases (for example, cancer, autoimmune diseases, and rare genetic disorders) are being developed by pharmaceutical companies, demand for specialized distribution infrastructure is increasing.

These are high value therapies that healthcare distributors are investing heavily in to provide cold chain logistics, development of digital tracking capabilities, specialty distribution centers and more to support. Additionally, the expansion capacity for direct to pharmacy and direct to hospital distribution models will further augment the efficiency of the supply chain and expediency to market for such life saving drugs. This will present huge growth opportunities for healthcare ecosystem services distributors over the long-run.

For example, in February 2025, a global pharmaceutical logistics company expanded its biologics distribution network with new temperature-controlled warehouses in Asia and Europe to support the growing demand for specialty therapeutics.

Healthcare Distribution Market Segment Analysis:

-

By type, pharmaceutical product distribution services accounted for the largest market share of 56.84% in 2025, while biopharmaceutical product distribution services are expected to grow at the highest CAGR of 7.41% during the forecast period.

-

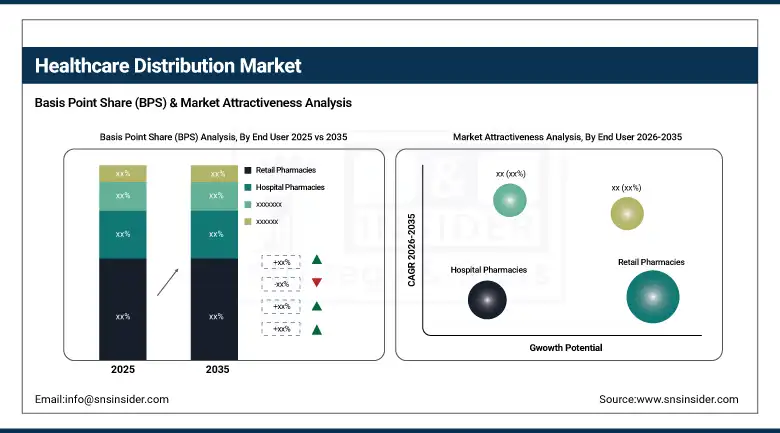

By end user, retail pharmacies held the largest share of 48.72% in 2025, while hospital pharmacies are expected to grow at the fastest CAGR of 6.98% between 2026 and 2035.

By Type, Pharmaceutical Product Distribution Services Lead the Market While Biopharmaceutical Distribution Shows Strong Growth

Pharmaceutical product distribution services accounted for the largest revenue share of approximately 56.84% in 2025 due to the extensive global demand for prescription medicines, over-the-counter drugs, and generic pharmaceuticals. The segment benefits from the large volume of pharmaceutical products distributed through retail pharmacies and healthcare institutions worldwide. Increasing consumption of generic drugs, rising healthcare awareness, and expanding pharmaceutical manufacturing capacity are major factors contributing to the growth of this segment.

The segment of biopharmaceutical product distribution services is also expected to have the fastest growth with the CAGR around 7.41% over the forecast period. Growth in this particular segment is primarily attributed to an increasing number of biologic therapies, such as monoclonal antibodies, vaccines, recombinant proteins, and blood-based therapeutics, being developed and tested for clinical efficacy and safety. Such products need adequate means of storage conditions, advanced cold chain logistics, and are usually transportation regulatory sensitive. The expansion of biologics pipelines by pharmaceutical companies will drive additional demand for these specialty distribution services over the next two decades.

By End User, Retail Pharmacies Dominate While Hospital Pharmacies Show Rapid Growth

In 2025, retail pharmacies contributed to over 48.72% of total market share owing to their widespread distribution channels and direct access to consumers. Retail pharmacy chains provide a crucial link in the delivery of prescription medications, over-the-counter medications and healthcare products to patients in urban and rural areas, representing the enduring importance of pharmaceutical distributors. With the evolution of digital pharmacies and home delivery services, the role of retail pharmacies has been additional buoyed in the healthcare distribution systems.

It is expected that during the period of forecast, hospital pharmacies will achieve the maximum growth with a CAGR of around 6.98%. Key factors fueling growth of the segment include increasing hospital admissions, rising demand for specialty medicines and continuously expanding hospital infrastructure. In order to meet demands for critical medicines, surgical products and emergency therapeutics, hospital pharmacies need a well-functioning supply chain system in place. Hence, hospital supply networks are even being strengthened, while the logistics capabilities are upgraded to suit the requirements of healthcare institutions.

Healthcare Distribution Market Regional Highlights:

Asia Pacific Healthcare Distribution Market Insights:

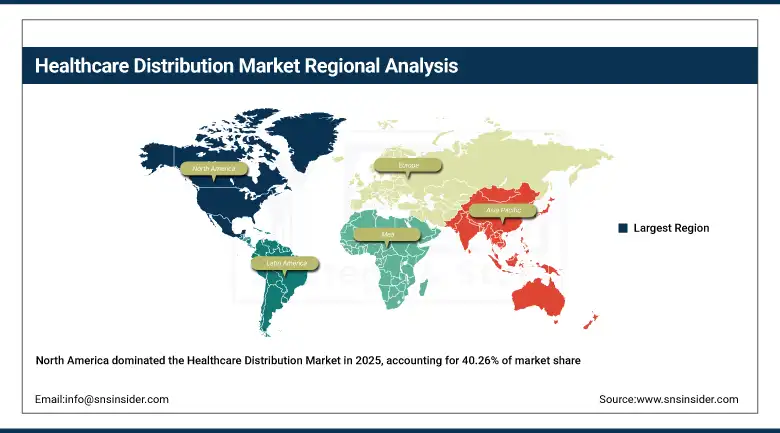

The Asia Pacific healthcare distribution market is the fastest-growing regional market, with a CAGR of 7.18% during the forecast period. Rapid growth in pharmaceutical manufacturing, expanding healthcare infrastructure, and increasing healthcare expenditures in countries such as China, India, and Japan are major drivers of regional market expansion. The region also benefits from a large patient population, growing demand for generic drugs, and increasing government initiatives to improve access to healthcare services.

North America Healthcare Distribution Market Insights:

Around 40.26% of revenue was attributed to North America owing to a more developed pharmaceutical distribution network and a more advanced supply chain for healthcare products and services. The U.S. is dominating the regional market owing to high concentration of major pharmaceutical distributor, large number of retail pharmacy chains, and high pharmaceutical consumption. Regional market growth is also being fueled by the adoption of advanced logistics technologies and regulation frameworks that support drug traceability.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Healthcare Distribution Market Insights:

Europe represents the second-largest market for healthcare distribution, supported by a well-regulated pharmaceutical supply chain and strong healthcare systems across the region. Countries such as Germany, France, and the United Kingdom have well-developed distribution networks that ensure efficient delivery of pharmaceuticals and medical products. Increasing adoption of digital logistics technologies and strong regulatory standards for pharmaceutical safety are further supporting market expansion in the region.

Latin America (LATAM) and Middle East & Africa (MEA) Healthcare Distribution Market Insights:

Healthcare distribution market of LATAM and MEA are expected to grow gradually With better health care infrastructure and increasing access to pharmaceutical products in the region. The market growth is attributed to government initiatives to strengthen national healthcare supply chains and to boost investments in pharmaceutical logistics. At the same time, the partnerships between world distributors and regional healthcare providers are enhancing product availability and the supply chain across emerging markets.

Healthcare Distribution Market Competitive Landscape:

McKesson Corporation (founded in 1833) is one of the largest healthcare distribution companies globally, providing pharmaceutical distribution services, medical supply logistics, and healthcare technology solutions to hospitals, pharmacies, and healthcare providers.

-

In February 2025, the company expanded its automated distribution center network in North America to improve pharmaceutical delivery efficiency and reduce supply chain delays.

Cardinal Health (founded in 1971) operates a large healthcare logistics network offering pharmaceutical distribution, medical product supply, and integrated healthcare services to healthcare providers across multiple global markets.

-

In January 2025, the company introduced a new digital supply chain analytics platform to optimize inventory management and improve order visibility for hospital clients.

AmerisourceBergen (founded in 2001) specializes in pharmaceutical sourcing, distribution, and logistics services, supporting manufacturers and healthcare providers with advanced supply chain solutions.

-

In March 2025, the company announced the expansion of its specialty pharmaceutical distribution services to support the growing demand for biologic therapies.

Healthcare Distribution Market Key Players:

-

McKesson Corporation

-

Cardinal Health

-

Cencora (AmerisourceBergen)

-

Walgreens Boots Alliance

-

CVS Health

-

Fresenius SE & Co. KGaA

-

Henry Schein Inc.

-

Owens & Minor

-

Shanghai Pharmaceuticals

-

Sinopharm Group

-

Medline Industries

-

Zuellig Pharma

-

Roche Diagnostics Distribution

-

GE Healthcare Supply Chain

-

Philips Healthcare Logistics

-

DB Schenker Healthcare

-

DHL Life Sciences & Healthcare

-

Kuehne + Nagel Healthcare Logistics

-

UPS Healthcare

-

FedEx HealthCare Solutions

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1123.25 Billion |

| Market Size by 2035 | USD 2138.38 Billion |

| CAGR | CAGR of 6.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Pharmaceutical Product Distribution Services (OTC Drugs/Vitamins, Generic Drugs, and Brand-name/Innovator Drugs), Biopharmaceutical Product Distribution Services (Monoclonal Antibodies, Vaccines, Recombinant Proteins, Blood and Blood Products, and Other Products), and Medical Device Distribution Services) • By End User (Retail Pharmacies, Hospital Pharmacies, and Other End Users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | McKesson Corporation, Cardinal Health, Cencora, Walgreens Boots Alliance, CVS Health, Fresenius SE & Co. KGaA, Henry Schein Inc., Owens & Minor, Shanghai Pharmaceuticals, Sinopharm Group, Medline Industries, Zuellig Pharma, Roche Diagnostics Distribution, GE Healthcare Supply Chain, Philips Healthcare Logistics, DB Schenker Healthcare, DHL Life Sciences & Healthcare, Kuehne + Nagel Healthcare Logistics, UPS Healthcare, FedEx HealthCare Solutions |

Frequently Asked Questions

The healthcare distribution market was valued at USD 1123.25 billion in 2025 and is projected to reach USD 2138.38 billion by 2035.

The market is expected to grow at a CAGR of 6.65% during the forecast period from 2026 to 2035.

Pharmaceutical product distribution services held the largest share of 56.84% in 2025 due to high demand for prescription drugs and generic medicines.

Retail pharmacies accounted for the largest market share of 48.72% in 2025, supported by extensive pharmacy networks and direct patient access.

North America holds the largest share of 40.26% in 2025, driven by advanced pharmaceutical supply chain infrastructure and strong distributor presence.

Get in Touch