Phosphate Fertilizer Market Report Scope & Overview:

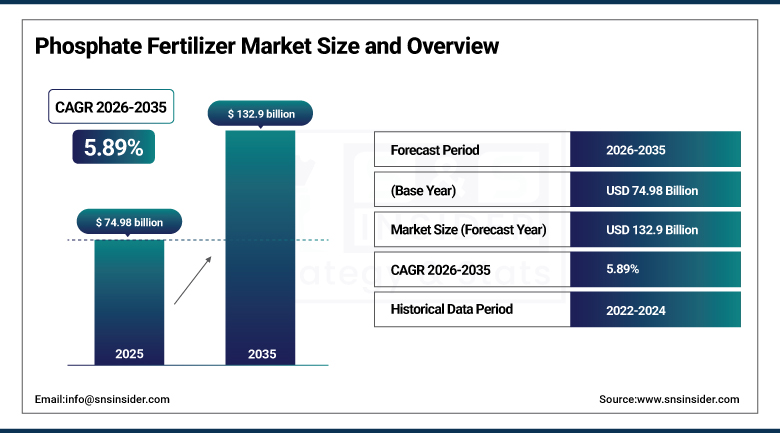

The Phosphate Fertilizer Market was valued at USD 74.98 billion in 2025 and is expected to reach USD 132.9 billion by 2035, growing at a CAGR of 5.89% from 2026–2035.

Market for Phosphate Fertilizers Growth is fuelled by rising demands for food globally, reduction in arable lands across the world, and the requirement to boost crop productivity levels. The growing trend towards practicing intensive farming, development of agriculture sector through modernization, and demands for higher yielding crops have boosted phosphate fertilizers consumption globally.

Morocco controls over 70% of the world's known phosphate rock reserves through the state-owned company OCP. This geographic concentration gives Morocco enormous influence over global phosphate supply and pricing, creating strategic considerations for importing nations and fertilizer companies that depend on Moroccan phosphate rock.

Market Size and Forecast

-

Market Size in 2025: USD 74.98 Billion

-

Market Size by 2035: USD 132.9 Billion

-

CAGR: 5.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Phosphate Fertilizer Market - Request Free Sample Report

Market Trends

-

Global population growth and rising food demand in developing countries are increasing the pressure on agricultural systems to produce more with better fertilizer management.

-

Precision agriculture and variable-rate fertilizer application technologies are improving phosphate use efficiency on farms.

-

Environmental regulations on fertilizer runoff are pushing farmers toward controlled-release and coated phosphate products.

-

Biostimulants and organic phosphate products are growing as farmers seek to complement or partially replace synthetic fertilizers.

-

Specialty phosphate fertilizers for high-value crops like fruits and vegetables are growing faster than bulk commodity products.

-

Supply chain diversification efforts by major agricultural economies are driving investment in new phosphate rock deposits and processing capacity.

-

Fertigation, the application of fertilizers through irrigation systems, is growing as a more efficient delivery method for phosphate.

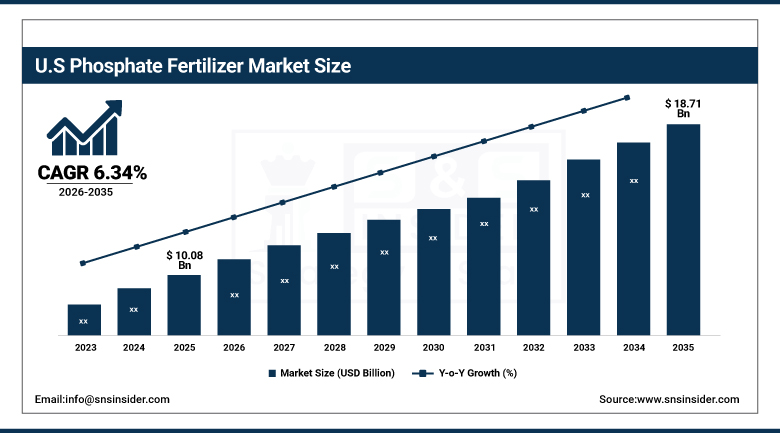

U.S. Phosphate Fertilizer Market was valued at USD 10.08 billion in 2025 and is expected to reach USD 18.71 billion by 2035, growing at a CAGR of 6.34% from 2026 to 2035.

The USA is not only one of the major producers but also the biggest agriculture sector in the world in terms of size. There is an internal mining of phosphorite rocks in states like Florida and Idaho which has resulted in the development of a robust internal fertilization industry. The use of phosphate-based fertilizers by the farmers is mainly on corn, soybean, and wheat crops, which are some of the crops that require high amounts of phosphate in the world.

Florida's phosphate mining industry is facing growing environmental and regulatory pressure around land reclamation requirements and water quality impacts. This is creating long-term supply constraints for U.S.-produced phosphate rock, making American fertilizer companies increasingly dependent on imports, particularly from Morocco.

Market Segment Insights

-

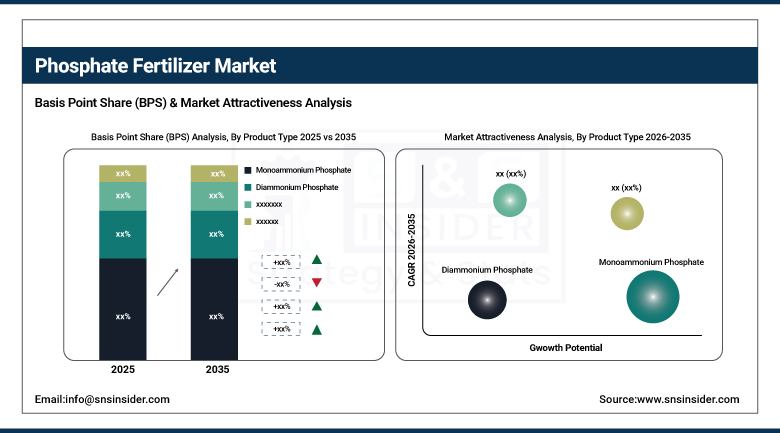

Based on Product Type, MAP (Monoammonium Phosphate) led with approximately 33% market share in 2025 due to high nutrient concentration and wide crop applicability.

-

Based on Crop Type, Cereals & Grains (corn, wheat, rice) are the largest consumers of phosphate fertilizers globally.

-

Based on Application, Soil Application dominates; Fertigation is growing fastest with precision agriculture adoption.

-

Based on End-Use, Agriculture accounts for over 95% of phosphate fertilizer consumption globally.

Market Segment Analysis

By Product Type: MAP Leads, DAP Closely Behind

Monoammonium Phosphate (MAP) is the foremost phosphate fertilizer product in the world. Comprising 11% nitrogen and 52% phosphate by composition, MAP serves as an efficient source of nutrients which are especially useful as a starter fertilizer or for crops that require high phosphorus availability at their early growth stages. Being granulated, MAP can be applied by broadcasting and precise placing methods. In 2025, the share of MAP in the global phosphate fertilizer market was 33%.

Diammonium Phosphate (DAP), containing 18% nitrogen and 46% phosphate, is the second phosphate fertilizer product used extensively in cereals and serving as a widely traded phosphate fertilizer product on international markets. The DAP and MAP combined market share in the global phosphate fertilizer market in 2025 is over 60%, acting as price setters for the market. Triple Superphosphate (TSP) is a phosphate-only fertilizer comprising 46% of P2O5 which does not contain any additional nitrogen. Single Superphosphate (SSP) is the simplest phosphate fertilizer and still in use mainly in low-cost markets and for sulfur supply in crop production in soils lacking sufficient sulfur.

By Crop: Cereals Dominant, High-Value Crops Growing Faster

It should be mentioned that cereals and grains such as corn, wheat, rice, and barley are the biggest users of phosphate fertilizers throughout the world. These are the crops that feed the planet, and they occupy millions of hectares where the requirement of phosphates is considerable. All big agricultural nations use large amounts of phosphate fertilizers to cultivate cereals.

Oilseeds such as soybeans and canola represent a significant user of phosphates due to a large amount of phosphorus contained within seeds. Crops of legumes produce their nitrogen supply, but they need other nutrients, such as phosphorus. Soybean cultivation increases around the globe in countries like Brazil and the United States, which results in an increasing requirement for phosphates. The fruits and vegetables are cultivated in less area but have a higher consumption rate and are usually grown through modern fertigation systems which make it possible to use fertilizers efficiently.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

78% |

|

Europe |

France |

25% |

|

Asia Pacific |

India |

38% |

|

Middle East & Africa |

Morocco |

65% |

|

Latin America |

Brazil |

62% |

North America

The US enjoys the greatest market share in North America, along with other nations in the region. Farming in the US is characterized by high productivity as well as intensive use of phosphate especially in the farming of corn and soybeans in the Midwest. The country has domestic sources of phosphate rocks that include Florida and Idaho, apart from importing from Morocco and Canada.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe

Europe already has an established and stable market for phosphate fertilizers under rigorous environmental regulations that dictate nutrient management practices. The EU’s Farm to Fork Strategy seeks to cut down fertilizer usage by 20% by 2030 without compromising food production, making it necessary to develop better phosphate fertilizers and application techniques. Eastern Europe is made up of important agricultural economies like Ukraine and Poland.

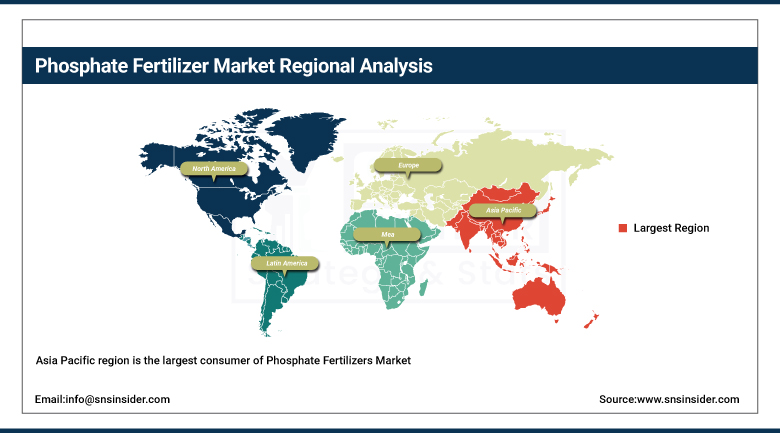

Asia Pacific

The Asia Pacific region is the largest consumer of phosphate fertilizers due to the large-scale agriculture industries found in countries such as India, China, and Southeast Asia. India happens to be among the biggest consumers of phosphate fertilizers across the globe, owing to its inadequate supply of domestic phosphate rocks and huge agricultural needs. China, on the other hand, used to be a leading producer as well as exporter of phosphate fertilizers.

Middle East & Africa

Indeed, the most prominent force in this region and even across the globe is Morocco because of the OCP Group being the custodian of the biggest phosphate rock deposits in the world. The company has put lots of effort into building their manufacturing capacities and establishing integrated fertilizer factories. Sub-Saharan Africa provides an important potential market since the soils on the continent lack phosphates and their fertilization levels are still below required levels.

Latin America

Brazil is the largest consumer of phosphate fertilizers in Latin America, and one of the largest consumers globally. This is because Brazil has large-scale soybeans, maize, and sugarcane production that depend on phosphate fertilizers due to the phosphorus deficiency in the majority of the soil in Brazil. Brazil has been working on its ability to produce phosphate fertilizers domestically.

Market Growth Drivers

-

Global food demand growth requires higher crop yields from existing agricultural land

Market for Phosphate Fertilizer is showing a steady growth pattern due to the increasing demand for food in the world and the necessity to obtain greater yields from the available agricultural lands. The phosphate fertilizers help in promoting root development and increasing the quality of crops harvested. Due to the increase in the number of people, decrease in arable land and use of intensive farming systems, farmers have been encouraged to use fertilizers which are rich in nutrients.

Climate change is adding urgency to the need for efficient phosphate use. Drought conditions, changing rainfall patterns, and more frequent extreme weather events are making precision nutrient management more important. Farmers who apply the right amount of phosphate at the right time and place get better returns and also protect water quality by reducing runoff.

Market Restraints

-

Geographic concentration of phosphate rock reserves creates supply and price risks

The biggest structural challenge for the phosphate fertilizer market is that the key raw material, phosphate rock, is heavily concentrated in a very small number of countries. Morocco alone controls over 70% of global reserves. When any major supplier restricts exports or experiences production disruptions, it can cause significant global price volatility that disrupts agricultural planning and threatens food security in import-dependent countries. This concentration risk is a persistent concern for the market.

Market Opportunities

-

Phosphate recovery from wastewater and organic waste creates circular economy potential

One exciting opportunity is recovering phosphorus from wastewater treatment, sewage sludge, and food processing waste. These waste streams contain significant concentrations of phosphorus that is currently discharged into waterways, causing pollution. Technologies that can extract this phosphorus and convert it into usable fertilizer products could both reduce environmental damage and create alternative supply sources that reduce dependence on mined phosphate rock. Several European countries and companies are investing actively in this approach.

Recent Developments

-

2025: OCP Group announced a major expansion of its Jorf Lasfar fertilizer complex in Morocco, adding production capacity of over 1 million tonnes per year of DAP and MAP, the largest single phosphate fertilizer capacity addition globally in over a decade.

-

2024: Mosaic Company completed a major expansion of its MicroEssentials specialty phosphate fertilizer production capacity, responding to strong farmer demand for products that combine phosphate with sulfur and other micronutrients in a single granule for improved crop nutrition efficiency.

-

2023: The European Commission adopted new regulations on organic and recycled nutrient products under the EU Fertiliser Products Regulation, creating a legal framework for recovered phosphorus products to be sold as certified fertilizers, opening a new market for circular economy phosphate recovery.

Key Players

Leading companies in the Phosphate Fertilizer Market:

-

OCP Group (Morocco) – Phosphate Rock and Fertilizer Producer

-

The Mosaic Company (USA) – MicroEssentials, Potash and Phosphate

-

PhosAgro (Russia) – MAP, DAP, and Specialty Phosphates

-

Nutrien Ltd. (Canada) – DAP and MAP Production

-

CF Industries Holdings – Nitrogen and Phosphate Fertilizers

-

Jordan Phosphate Mines Company – Phosphate Rock and DAP

-

Coromandel International (India) – DAP and SSP Fertilizers

-

Israel Chemicals Ltd. – Specialty Phosphate Fertilizers

-

Yara International ASA – Phosphate Fertilizer Blends

-

Groupe Chimique Tunisien – Phosphate and Triple Superphosphate

-

Ma'aden Saudi Arabian Mining Company – DAP Production

-

Simplot Company – Phosphate Mining and Processing

-

Agrium Inc. (merged into Nutrien) – Crop Nutrition Solutions

-

Bunge Limited – Fertilizer and Agricultural Trading

-

Koch Fertilizer LLC – Phosphate Fertilizer Distribution

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 74.98 Billion |

| Market Size by 2035 | USD 132.9 Billion |

| CAGR | CAGR of 5.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Monoammonium Phosphate (MAP), Diammonium Phosphate (DAP), Triple Superphosphate (TSP), Single Superphosphate (SSP), Others) • By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others) • By Application (Soil Application, Foliar Application, Fertigation) • By End-Use (Agriculture, Non-Agricultural) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | OCP Group, The Mosaic Company, PhosAgro, Nutrien Ltd., CF Industries Holdings, Jordan Phosphate Mines Company, Coromandel International, Israel Chemicals Ltd., Yara International ASA, Groupe Chimique Tunisien, Ma'aden Saudi Arabian Mining Company, Simplot Company, Agrium Inc., Bunge Limited, Koch Fertilizer LLC |

Frequently Asked Questions

Ans: Growing global food demand, population growth, and the irreplaceable role of phosphorus in plant nutrition are the fundamental drivers.

Ans: Asia Pacific is the largest consuming region, with India and China being the two largest individual country markets.

Ans: MAP (Monoammonium Phosphate) leads with approximately 33% market share due to high nutrient concentration and versatility across crop types.

Ans: The market was valued at USD 74.98 billion in 2025.

Ans: The market is expected to grow at a CAGR of 5.89% from 2026 to 2035.

Get in Touch