Potash Fertilizers Market Report Scope & Overview:

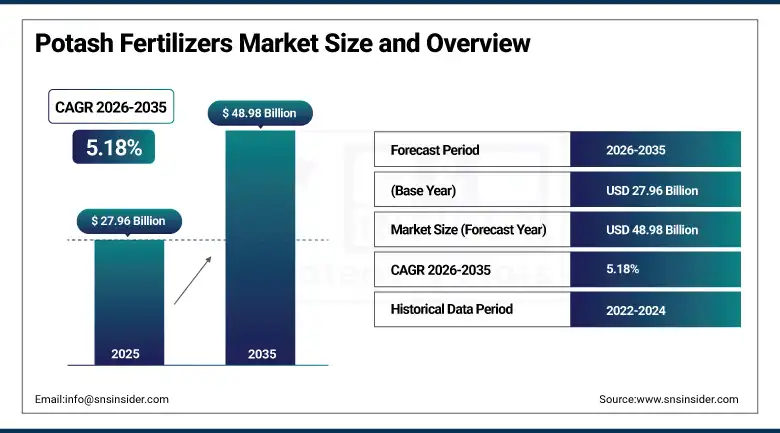

The Potash Fertilizers Market was valued at USD 27.96 Billion in 2025 and is expected to reach USD 48.98 Billion by 2035, growing at a CAGR of 5.18% from 2026–2035.

The global market for potash fertilizers is witnessing sustained growth. Potash fertilizers provide potassium, which is one of the three basic macronutrients necessary for plant growth. This mineral is involved in activating enzymes, controlling water content in plants, and protecting plants against drought; the quality of plant produce, including its productivity, depends on these functions of potassium. Some of the key factors influencing the market include increasing food demand due to population growth, depleting amounts of potassium in the soil, fertilization policies supported by governments, and developments in fertilizer technology.

In September 2024, ICL supplied 420,000 metric tons of premium potash fertilizer to India, supporting farmers with high-quality nutrients to enhance crop yields and soil health. The supply reflects India's strategic importance as one of the world's largest potash fertilizers importing nations. The premium grade specification reflects the commercial recognition that Indian farmers's crop quality and yield productivity improvement motivation creates demand for above-commodity potash fertilizer specifications.

Market Size and Forecast

-

Market Size in 2026E: USD 29.41 Billion

-

Market Size by 2035: USD 48.98 Billion

-

CAGR: 5.18% from 2026 to 2035

-

Fastest Growing Region: Europe

-

Largest Region: Asia Pacific

To Get more information On Potash Fertilizers Market - Request Free Sample Report

Potash Fertilizers Market Trends

-

Precision agriculture enables variable-rate potash application, improving potassium efficiency and reducing fertilizer costs.

-

Water-soluble and controlled-release potash fertilizers create premium segments with higher nutrient use efficiency and yield benefits.

-

SOP adoption increases over MOP in chloride-sensitive crops like fruits, vegetables, potato, and tobacco globally.

-

Fertigation systems enable precise root-zone potash delivery, improving efficiency in irrigated high-value crop production.

-

Government subsidies in India, China, Brazil, and Southeast Asia support balanced fertilization and stabilize potash demand trends.

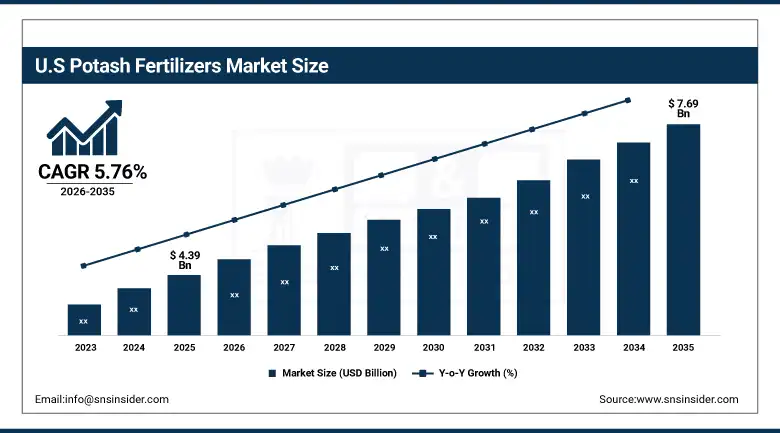

The U.S. Potash Fertilizers Market Outlook

The U.S. potash fertilizers market was valued at approximately USD 4.39 Billion in 2025 and is expected to reach approximately USD 7.69 Billion by 2035, growing at a CAGR of approximately 5.76%.

The U.S. is a commercially significant potash fertilizers market whose corn, soybean, and wheat production creates consistent above-average potassium nutrient requirements. Mosaic Company and Nutrien serve the domestic market through retail distribution and direct-to-farm sales whose combined infrastructure creates accessible potash supply across the Corn Belt, Great Plains, and Pacific Northwest agricultural regions. USDA's soil health programme and the 4R Nutrient Stewardship framework's precision potassium application guidance create institutional motivation for optimized potash use that sustains premium formulation procurement from technically engaged farmers.

Nutrien launched an enhanced controlled-release potash blend in 2024 targeting corn and soybean producers in the U.S. Corn Belt seeking to improve potassium use efficiency while reducing split-application labour cost. The controlled-release formulation's single-application nitrogen and potassium delivery reduces the field operation cost that conventional split-application programmes require while sustaining season-long nutrient availability whose combined economic value creates premium pricing justification for technically sophisticated farm operations.

Potash Fertilizers Market Segment Analysis

-

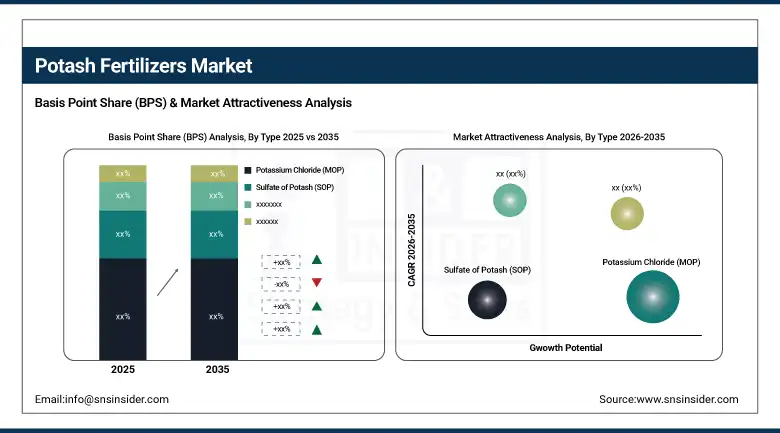

By Type, the potassium chloride/MOP segment dominated the market with approximately 62% share in 2025, while the potassium nitrate segment is the fastest growing as demand.

-

By Application, the broadcasting segment dominated the market with 50.3% share in 2025, while the fertigation segment is the fastest growing.

-

By Crop Type, the cereals & grains segment dominated the market with approximately 38% share in 2025, while the fruits & vegetables segment is the fastest growing.

-

By Form, the solid/granular segment dominated the market with approximately 72% share in 2025, while the Liquid segment is the fastest growing.

By Type, MOP dominates, potassium nitrate grows fastest

Potassium chloride (Muriate of Potash/MOP) retained the dominant type position with approximately 62% of the potash fertilizers market in 2025. MOP's high potassium content of 60-62% K₂O creates efficient nutrient delivery per tons of fertilizer product whose bulk logistics economics sustain its cost advantage over specialty potash alternatives. Cereal grain, oilseed, and sugarcane production's tolerance for chloride anion creates broad MOP applicability whose aggregate across the global field crop acreage sustains MOP's dominant commercial position across all agricultural seasons.

Potassium nitrate is the fastest-growing type because the global expansion of greenhouse horticulture, drip-irrigated fruit production, and precision agriculture for high-value specialty crops creates growing demand for chloride-free, highly water-soluble potassium combined with nitrogen nutrition. Each new greenhouse facility and each drip-irrigated vineyard, orchard, or vegetable operation that specifies potassium nitrate for fertigation creates procurement whose premium pricing over MOP reflects the crop quality benefits that chloride-free nutrition provides in chloride-sensitive crops.

By Application, broadcasting dominates, fertigation grows fastest

Broadcasting retained the dominant application position with 50.3% of the potash fertilizers market in 2025. The economic and operational simplicity of mechanical spreading over large field acreage creates the most commercially accessible potash application approach for grain and oilseed producers whose per-ton fertilizer cost and machinery compatibility determines agronomic practice selection. Each combine-equipped grain farms whose potash application is incorporated into pre-plant field preparation creates broadcasting procurement whose aggregate across global cereal and oilseed acreage defines the most commercially significant application category.

Fertigation is the fastest-growing application because the global expansion of drip irrigation in water-scarce agricultural regions, the progressive adoption of precision nutrient management in high-value crop production, and the efficiency advantage of root-zone liquid potash delivery over broadcast surface application create structured above-average demand growth. Each new drip irrigation system installation in a water-constrained agricultural region creates a fertigated potash procurement transition whose nutrient use efficiency improvement sustains the investment.

By Crop Type, cereals dominate, fruits & vegetables grow fastest

Cereals and grains retained the dominant crop type position with approximately 38% of the potash fertilizers market in 2025. The extraordinary cultivation area of wheat, rice, corn, and barley whose combined global acreage exceeds 700 million hectares creates aggregate potash consumption that no other crop category approaches. Each hectare of cereal production whose potassium removal through grain harvest creates replacement requirement that sustains consistent annual potash procurement creates commercial demand whose stability across commodity price and weather cycle variation provides commercial predictability that potash producers value in supply planning.

Fruits and vegetables are the fastest-growing crop type because the extraordinary per-hectare potassium consumption of intensive horticultural production, combined with potassium's direct impact on fruit quality attributes including sugar content, color development, shelf life, and marketable yield, creates premium potash formulation procurement whose per-ton commercial value substantially exceeds cereal production economics.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Potash Fertilizers Market Insights

North America is a significant potash fertilizers market anchored by the U.S. Corn Belt's corn and soybean production, the Great Plains' wheat production, and Canada's prairie agriculture. The United States accounts for approximately 87.4% of North American revenues through Mosaic Company's retail distribution network, Nutrien's dealer infrastructure, and the progressive adoption of precision nutrient management whose variable rate potash application creates structured procurement.

Canada contributes approximately 12.6% of North American revenues through its prairie grain and oilseed production's potash consumption and the domestic potash mining sector's world-class supply position. Saskatchewan's extraordinary potash reserve base, representing approximately one-third of global potash reserves, sustains North American supply security whose commercial availability creates competitive pricing that sustains North American farmer procurement.

Europe Potash Fertilizers Market Insights

The Europe region is the most rapidly developing market for potash fertilizers due to the increasing trend towards organic farming and the adoption of precision agriculture; the focus on soil health under the EU’s “Farm to Fork” Strategy; and high levels of investment in technology and nutrient management in the European agricultural industry. Germany makes up about 22.3% of the revenues of the European market through its high-intensity agriculture and K+S AG’s potash output.

France, Poland, and Spain are significant secondary European markets where cereal, vegetable, and vineyard production create consistent potash procurement. The EU's Common Agricultural Policy's soil health provisions and member state agri-environment scheme's balanced fertilization requirements create structured institutional motivation for potash programme adoption that sustains European market growth above the global average.

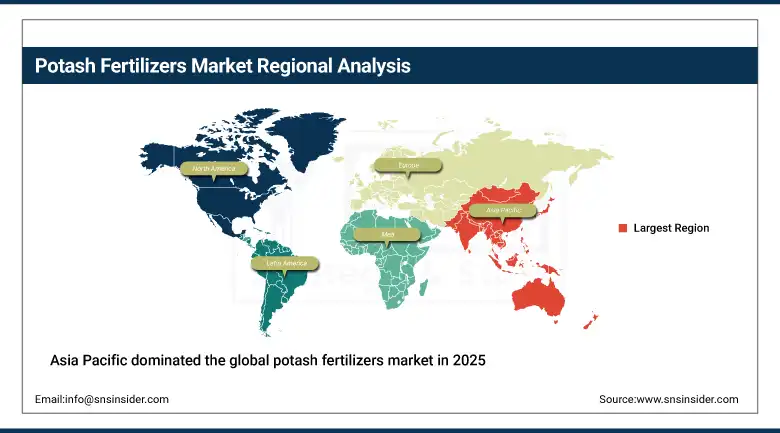

Asia Pacific Potash Fertilizers Market Insights

Asia Pacific dominated the global potash fertilizers market in 2025 as the world's largest potash consuming region. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary rice and wheat production whose combined cereal acreage creates the world's largest single national potash consumption requirement. India and Southeast Asia are the most commercially dynamic emerging markets where growing food demand, expanding commercial farming, and government fertilizer subsidy programmes create above-average potash procurement growth that compounds with agricultural intensification investment.

The region's commercial dominance reflects the concentration of the world's most potassium-deficient agricultural soils in South and Southeast Asia whose legacy of potassium extraction without adequate replacement creates structural fertilizer demand that sustains above-average potash procurement independently of commodity price cycles. Japan and South Korea's intensive greenhouse horticulture and premium produce production create above-average per-hectare potash consumption that sustains secondary Asia Pacific market contributions.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Potash Fertilizers Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its commercial horticultural production, the date palm sector's potassium requirement, and Vision 2030's agricultural intensification programme creating structured potash procurement. Brazil leads Latin American revenues at approximately 44.2% through its extraordinary soybean, corn, sugarcane, and coffee production whose combined agricultural sector creates the world's third-largest potash importing nation. Brazil consumed approximately 7.11 million metric tons of potash fertilizer in 2022, reflecting the commercial scale whose growth sustains Latin American market leadership.

Argentina's soybean and corn production creates significant secondary Latin American market procurement, while Colombia and Chile's fruit and vegetable export sectors create premium potash formulation demand from high-value crop production oriented toward quality-sensitive export markets.

Market Dynamics

Growth Drivers: Rising global food demand and soil potassium depletion creating systematic fertilization requirement

Rising global food demand is the potash fertilizers market's most structurally certain commercial growth driver. The World Bank's projection that global food demand will increase 50% by 2050 as population grows toward 10 billion creates non-discretionary agricultural productivity investment whose potash component grows with crop production intensification. Each new incremental crop yield per hectare that population growth requires creates proportional potassium nutrient demand whose replacement of soil potassium removal sustains annual potash procurement. The FAO's documentation that over two billion people suffer micronutrient deficiencies whose dietary quality improvement requires above-average food nutritional quality creates additional potash demand motivation beyond mere caloric volume production.

Soil potassium depletion from decades of intensive cultivation without adequate potassium replacement creates a structural deficit in global agricultural soils whose agronomic consequence is yield reduction and crop quality deterioration. Each soil test that documents potassium deficiency in previously adequate soils creates corrective potash application procurement whose correction requirement compounds with the progressive extent of soil potassium mining across intensively farmed regions globally.

Restraints: Potash price volatility from geopolitical supply concentration and environmental regulation of fertilizer runoff

Potash supply's extraordinary geographic concentration in Canada, Russia, and Belarus, whose combined reserves represent approximately 70% of global potash production, creates geopolitical price volatility whose commercial impact on farm input cost creates procurement uncertainty. The Russia-Belarus supply disruption following 2022 geopolitical events created extraordinary potash price increases that substantially reduced farmer procurement volumes and demonstrated the commercial risk of supply concentration. Each geopolitical event that restricts Canadian or FSU potash export creates price volatility whose downstream impact on farmer purchasing decisions moderates potash application rates in cost-sensitive emerging market agricultural systems.

Environmental regulation of potassium runoff and leaching in water-sensitive watersheds creates application restriction in some high-value agricultural regions whose soil health and water quality regulations limit potash application rates below agronomic optima.

Opportunities: Precision potash application and water-soluble specialty potash for high-value horticulture

Precision potash application through variable rate technology represents the most commercially differentiated near-term opportunity whose soil sampling, GPS mapping, and prescription-based application optimizes potassium placement whose efficiency improvement creates both agronomic and environmental value. Each farm that adopts variable rate potash application creates above-average per-hectare procurement from the premium formulations that precision placement justifies while improving overall nutrient use efficiency. The precision agriculture sector's above-average growth creates proportional premium potash formulation procurement opportunity.

Each new drip-irrigated fruit, vegetable, or greenhouse operation that specifies water-soluble SOP or potassium nitrate for fertigation creates premium potash procurement whose per-ton commercial value substantially exceeds commodity MOP economics. The global expansion of protected horticulture and irrigated export fruit production creates the most commercially dynamic specialty potash demand growth that sustains premium product investment.

Recent Developments:

-

2026: Nutrien reported stronger potash demand outlook supported by tight global supply, improved crop returns, and steady fertilizer pricing stability.

-

2026: Belaruskali sanctions easing improved global potash trade flows, increasing supply accessibility and stabilizing export routes for key importing countries.

-

2026: Mosaic reduced phosphate output and capital spending due to cost pressures, reflecting volatility in fertilizer pricing and margins.

Potash Fertilizers Market key players are:

-

Nutrien Ltd.

-

The Mosaic Company

-

K+S Aktiengesellschaft

-

Israel Chemicals Ltd. (ICL)

-

JSC Belaruskali

-

Eurochem Group AG

-

SQM S.A.

-

Yara International ASA

-

Compass Minerals International

-

Helm AG

-

Borealis AG

-

Sinofert Holdings Limited

-

Haifa Chemicals Ltd.

-

Uralkali

-

Arab Potash Company

-

CF Industries

-

Intrepid Potash Inc.

-

Migao Corporation

-

Tessenderlo Group

-

China BlueChemical Ltd

Potash Fertilizers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.96 Billion |

| Market Size by 2035 | USD 48.98 Billion |

| CAGR | CAGR of 5.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Potassium Chloride/MOP, Sulfate of Potash/SOP, Potassium Nitrate, Others) • By Form (Solid/Granular, Liquid, Powder) • By Application (Broadcasting, Fertigation, Foliar Spray, Others) • By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Plantation Crops, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nutrien Ltd., The Mosaic Company, K+S Aktiengesellschaft, Israel Chemicals Ltd. (ICL), JSC Belaruskali, Eurochem Group AG, SQM S.A., Yara International ASA, Compass Minerals International, Helm AG, Borealis AG, Sinofert Holdings Limited, Haifa Chemicals Ltd., Uralkali, Arab Potash Company, CF Industries, Intrepid Potash Inc., Migao Corporation, Tessenderlo Group, China BlueChemical Ltd. |

Frequently Asked Questions

The Potash Fertilizers Market is expected to grow at a CAGR of 5.18% from 2026 to 2035.

The Potash Fertilizers Market was valued at USD 27.96 Billion in 2025.

Rising global food demand requiring above-average crop productivity investment, and soil potassium depletion from intensive cultivation.

Broadcasting dominated the Potash Fertilizers Market with 50.3% share in 2025, while the Fertigation segment is the fastest growing.

Asia Pacific dominated the Potash Fertilizers Market in 2025 as the world's largest potash consuming region, with China accounting for approximately 44.8% of Asia Pacific revenues. Europe is the fastest-growing region.

Get in Touch