Proppants Market Report Scope & Overview:

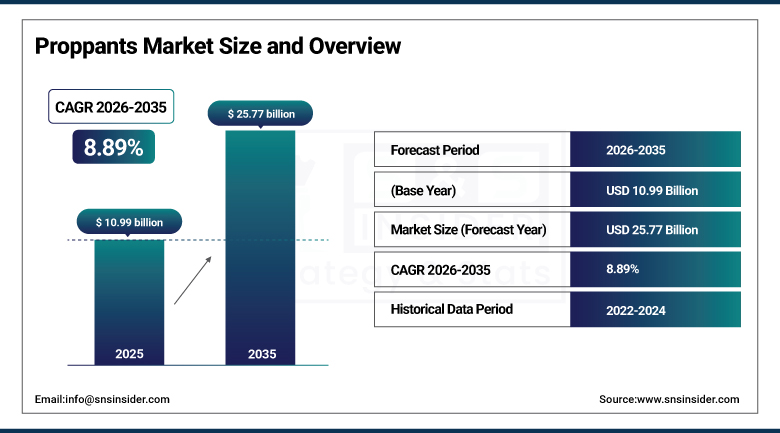

The Proppants Market size was USD 10.99 Billion in 2025 and is expected to reach USD 25.77 Billion by 2035, growing at a CAGR of 8.89% from 2026–2035.

The worldwide proppant industry is growing steadily because of hydraulic fracturing and horizontal drilling that have helped to develop unconventional sources such as shale gas, tight oil, and coal bed methane reserves globally. Proppants are granular substances such as frac sand, resin-coated sand, and ceramics that are used in hydraulically induced fractures in order to maintain their structural integrity, thus allowing for the free passage of hydrocarbons into the wellbore. The proppant market review highlights production capacity and utilization rates by nation and by proppant type along with changes in the prices of raw materials such as silica sand, bauxite, and resin that affect production costs. Moreover, the proppant market analyzes regulations in the frac sand mining and proppant use sectors, emphasizing environmental policies and emission standards.

In February 2024, Atlas Energy Solutions finalized an agreement to acquire Hi-Crush Inc.’s North American proppant production assets and logistics operations. The acquisition consolidated in-basin sand production capacity and last-mile delivery infrastructure under a single operator, reflecting the industry’s broader strategic shift toward vertically integrated proppant supply chains that combine mining, processing, and transportation logistics to reduce well-site delivery costs for oilfield operators across the Permian Basin and other major shale plays.

Market Size and Forecast

-

Market Size in 2026E: USD 11.97 Billion

-

Market Size by 2035: USD 25.77 Billion

-

CAGR: 8.89% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Proppants Market - Request Free Sample Report

Proppants Market Trends

-

Rising shale gas and tight oil exploration is driving sustained demand for frac sand, resin-coated, and ceramic proppants.

-

In-basin sand mining plants are reducing transportation costs and improving supply chain reliability near major shale formations.

-

Automated proppant delivery systems and mobile storage silos are improving well-site logistics efficiency and reducing wastage.

-

Enhanced oil recovery techniques are increasing proppant intensity per well across major North American shale plays.

-

Recyclable and biodegradable proppant coating materials are gaining traction amid tightening environmental regulations.

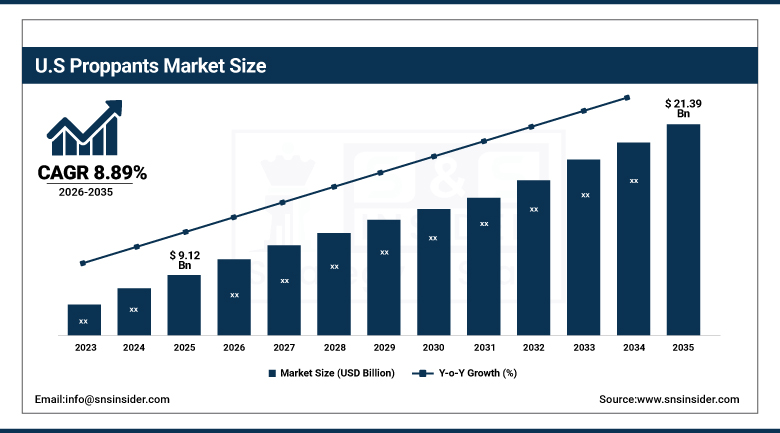

The U.S. Proppants Market Outlook

The U.S. Proppants Market was valued at approximately USD 9.12 Billion in 2025 and is expected to reach approximately USD 21.39 Billion by 2035, growing at a CAGR of approximately 8.89%.

The United States accounted majority of North American proppants revenues in 2023, owing to extensive shale gas and tight oil production in the Permian Basin, Marcellus, Eagle Ford, and Bakken formations. Fracking and horizontal drilling create massive demand for frac sand, resin-coated, and ceramic proppants across these unconventional plays. Nearby silica sand reserves, especially from Wisconsin and Texas, help reduce material costs and guarantee domestic supply for the country, supporting a mature in-basin sand production ecosystem that has substantially lowered well-site delivery costs over the past decade. The market is further propelled by government policies promoting domestic energy production and the development of enhanced oil recovery technologies that increase proppant intensity per well across major shale plays.

Major oilfield service providers including Halliburton, Schlumberger, and Baker Hughes reinforce the United States’ proppants industry through integrated drilling, completion, and proppant delivery service offerings. Halliburton’s SandCastle vertical storage silo and SandForce advanced proppant delivery system exemplify how leading service providers are investing in logistics innovation to reduce well-site delivery costs and improve fracturing operation efficiency across the country’s most active shale formations.

Proppants Market Segment Analysis

-

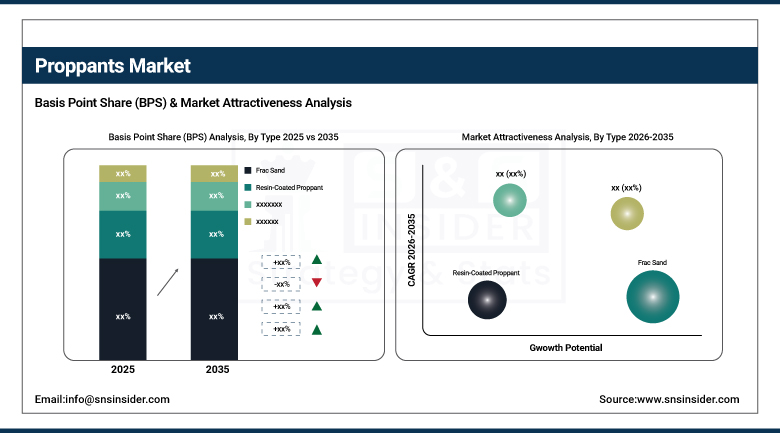

By Type, the Frac Sand segment dominated the proppants market with approximately 58% share in 2025, while the ceramic proppant segment is the fastest growing driven by demand for higher-strength, high-pressure well applications.

-

By Application, the shale gas segment dominated the proppants market with approximately 38% share in 2025, while the tight gas segment is the fastest growing driven by extreme downhole pressure well stimulation demand.

-

By End-Use Industry, the oil & gas exploration segment dominated the proppants market with the largest share in 2025, while other industrial applications are the fastest growing.

By Type, frac sand dominates, ceramic proppant grows fastest

Frac Sand held the largest market share at approximately 58% in 2025. It is relatively cost-effective, readily available, and performs well in hydraulic fracturing applications. Sand proppant is widely used, especially in shale gas and tight oil production, because it offers the best trade-off between permeability and conductivity at a lower price than resin-coated and ceramic alternatives. Operators have opted for high-purity silica sand following large deposits within the Midwest United States, including Wisconsin, Minnesota, and Illinois, and Canada’s Alberta Basin. Improvements in multi-stage fracturing and horizontal drilling techniques have increased the need for large volumes of frac sand to enhance well output, and its lower transportation costs versus alternative proppants sustain its leading position amid increased focus on domestic energy production.

Ceramic Proppant is the fastest-growing type, driven by demand for higher crush strength and conductivity in deeper, higher-pressure wells where frac sand and even resin-coated alternatives experience structural failure. CARBO Ceramics, Saint-Gobain Proppants, and CoorsTek’s sintered bauxite and kaolin ceramic proppant offerings provide superior performance in extreme downhole pressure environments common to the Permian Basin’s deeper formations and emerging international shale plays. Rising well stimulation complexity and the push toward extended-reach lateral drilling are increasing operator willingness to pay premium pricing for ceramic proppant’s durability and consistent fracture conductivity over a well’s productive lifetime.

By Application, shale gas dominates, tight gas grows fastest

The share of the application market was dominated by shale gas at nearly 38% in 2025 due to production in major basins such as Permian, Marcellus, Eagle Ford, and the Sichuan Basin, driving proppant demand. Shale gas recovery needs an abundant amount of proppants, including frac sand, resin coated proppants, and ceramic proppants. They play a significant role in keeping fractures opened to enable the flow of hydrocarbons. In North America, the exploration of shale gas has been encouraged due to the policies of the government and energy security policies, leading to reduced dependence on energy imports in the region. This coupled with the cheaper production cost of shale gas than conventional gases and increasing demand for clean energy sources globally ensures its dominance.

The tight gas application is the most rapidly growing application which needs highly strong proppants that can endure extremely high pressures encountered in wells. The application is witnessing growth because of the rise in exploration activities in such geographical locations as the Middle East and some parts of the Asia Pacific. This is mainly because of the effectiveness of the improved stimulation technologies and pressure optimization strategies used in the process of extracting natural resources. With the advent of economic alternatives like resin coated proppants and ceramic proppants, tight gas operations have become economically feasible.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.0% |

|

Europe |

Russia |

28.4% |

|

Asia Pacific |

Australia |

34.6% |

|

Middle East & Africa |

Saudi Arabia |

26.8% |

|

Latin America |

Argentina |

41.2% |

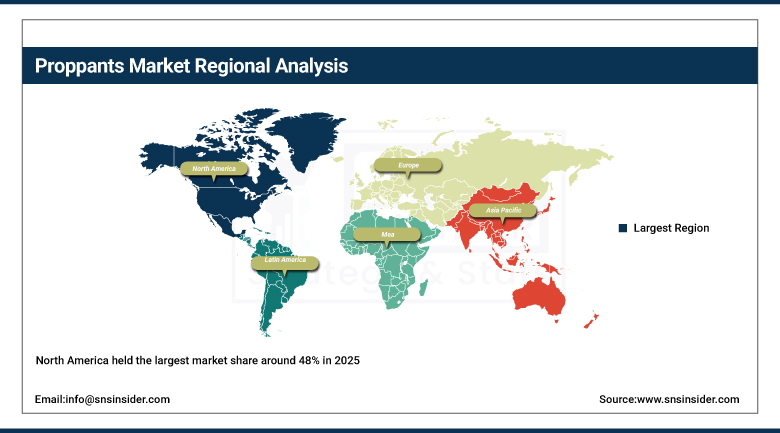

North America Proppants Market Insights

North America held the largest market share around 48% in 2025, driven by extensive shale gas and tight oil production across the United States and Canada. The hydraulic fracturing and horizontal drilling process increased demand for frac sand, resin-coated proppants, and ceramic proppants to enhance well production, with major shale formations including the Permian Basin, Marcellus, Eagle Ford, and Montney fuelling sustained proppant consumption.

The United States accounts for approximately 83% of North American revenues through its mature supply chain, large silica sand deposits, and strong investment from major oilfield service providers. Continued exploration and production activities have been supported by favourable government policies, technological developments, and energy security initiatives that establish North America as the primary player in the global proppants sector.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Proppants Market Insights

Europe is a smaller proppants market constrained by regulatory restrictions on hydraulic fracturing across several major economies, though Eastern European unconventional gas exploration sustains modest demand. Russia accounts for approximately 28.4% of European revenues through its substantial unconventional gas reserves and ongoing shale formation development activity.

Poland’s Lubocino shale formation exploration, Romania’s growing unconventional gas interest, and limited proppant demand from the United Kingdom’s restricted onshore fracking framework collectively shape European market development. European environmental policy uncertainty continues to constrain large-scale proppant procurement relative to North America and Asia Pacific markets, with most Western European nations maintaining moratoria or outright bans on hydraulic fracturing that limit the region's addressable proppant demand to imported volumes and specialized industrial filtration applications.

Asia Pacific Proppants Market Insights

Asia Pacific held a significant market share in 2025 and is projected to grow at the highest CAGR from 2026 to 2035, driven by increasing regional industrialization and ongoing energy security concerns. Domestic gas production demand propels the market in Australia, where the Cooper Basin and Canning Basin sustain growing proppant consumption.

Australia accounts for approximately 34.6% of Asia Pacific revenues through its expanding unconventional gas exploration and production infrastructure. China’s Sichuan Basin shale gas development and growing oilfield service provider investment in fracking technique advancement further sustain the region’s position as a backbone of future oil and gas exploration growth.

MEA & Latin America Proppants Market Insights

Saudi Arabia leads MEA revenues through its growing unconventional gas exploration programme and substantial government investment in diversifying domestic energy production beyond conventional reserves. The UAE’s growing interest in unconventional gas development contributes additional regional demand.

Argentina leads Latin American revenues through its world-class Vaca Muerta shale formation, whose extensive development has positioned the country as the region’s leading unconventional oil and gas producer. Brazil and Colombia contribute growing secondary demand through expanding exploration and production investment in their respective unconventional reserve basins, with both countries progressively building the in-basin sand processing and proppant logistics infrastructure that has proven essential to cost-effective shale development in North American markets.

Market Dynamics

Growth Drivers: Rising shale gas and tight oil exploration accelerating fracking activity and proppant intensity per well

An increase in shale gas and tight oil exploration is one of the major factors driving growth in the proppants market, due to wider acceptance of hydraulic fracturing technology in key oil-producing regions. U.S. shale production, especially in the Permian Basin, Eagle Ford, and Bakken formations, has grown immensely due to government backing and technological innovation. Canada’s development of unconventional oil and gas reserves in the Montney and Duvernay formations, and China’s Sichuan Basin activity, further support this trend, with demand for frac sand, resin-coated, and ceramic proppants climbing as fracking operations become more aggressive.

The worldwide energy transition and energy security concerns have converted increased domestic oil and gas production efforts into rising demand for proppants. As operators pursue enhanced oil recovery techniques and extended-reach lateral drilling, proppant intensity per well continues climbing, with multi-stage fracturing requiring substantially larger proppant volumes than conventional single-stage completions. This trend sustains structural demand growth that compounds with rising well count across active shale formations worldwide.

Restraints: High operational and transportation costs limiting growth, particularly for premium resin-coated and ceramic proppants

High operation and logistics costs adversely impact the proppants industry since frac sand is typically extracted from important regions such as the American Midwest. After extraction of frac sand, the process of washing and drying the sand takes place before transportation to the oil and gas fields including Permian, Bakken, and Eagle Ford. During times when there are low productions of oil and gas, logistics costs, which include transportation and storage of the frac sand, are a component of the total costs associated with the well, thus making the use of proppants less economic.

Transport costs can be exacerbated even further because of limited rail and trucking capacities. Resin-coated and ceramic proppants, which perform better, are also more expensive because of the highly involved production process. High production costs make it less likely that such proppants will be widely adopted in oil fields. As a result, there is growing interest in local basin sand among oil and gas corporations, limiting the expansion potential of other proppants.

Opportunities: Rising investments in oilfield infrastructure and logistics creating supply chain efficiency opportunities

Investments in oilfield infrastructures and logistics are increasing, presenting significant opportunities within the proppants sector, as players continue to seek least-cost logistics channels by way of securing supply chain and minimizing logistics costs. With the expanding trend of hydraulic fracturing operations, there is a corresponding increase in the need for efficient transportation, safe storage, and easy handling of the proppants at sites. Significant investments in automated proppant delivery, in-basin sand mining facilities, and rail/road transport are cutting down logistics cost and time and enabling greater efficiency at wellsites.

The construction of unit train facilities and last-mile trucking services by North American players guarantees that proppants will be affordable and available in abundant quantities for any shale play operations. Mobile proppant silos and proppant inventory management systems are among the innovations being adopted today in order to enhance logistics performance and cut down waste. Oilfield services companies as well as proppant manufacturers have invested heavily in logistics, creating greater supply chain efficiencies and opportunities within the global proppants industry.

Recent Developments:

-

2024: Atlas Energy Solutions finalised an agreement to acquire Hi-Crush Inc.’s North American proppant production assets and logistics operations, consolidating in-basin sand mining capacity and last-mile delivery infrastructure under a single integrated operator.

-

2023: Covia Holdings expanded its Unifrac resin-coated proppant production capacity to meet growing demand for higher-conductivity solutions in deeper, higher-pressure shale well completions across North American unconventional basins.

-

2023: CARBO Ceramics introduced enhanced ceramic proppant formulations targeting extreme downhole pressure applications in the Permian Basin’s deepest unconventional formations, strengthening its premium product portfolio.

Proppants Market Key Players are:

-

CARBO Ceramics Inc.

-

U.S. Silica Holdings Inc.

-

Covia Holdings LLC

-

Hi-Crush Inc.

-

Hexion Inc.

-

Saint-Gobain Proppants

-

Badger Mining Corporation

-

Emerge Energy Services LP

-

Preferred Sands

-

Fairmount Santrol Holdings Inc.

-

Atlas Sand Company LLC

-

Mineração Curimbaba

-

Xinmi Wanli Industry Development Co. Ltd.

-

China GengSheng Minerals Inc.

-

ChangQing Proppant

-

CoorsTek Inc.

-

Eagle Materials Inc.

-

Fores LTD

-

Halliburton Company

-

Baker Hughes Company

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.99 Billion |

| Market Size by 2035 | USD 25.77 Billion |

| CAGR | CAGR of 8.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Frac Sand, Resin-Coated Proppant, Ceramic Proppant) • By Application (Shale Gas, Tight Gas, Coal Bed Methane, Others) • By End Use Industry (Oil & Gas, Geothermal Energy, Other Industrial Applications) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CARBO Ceramics Inc., U.S. Silica Holdings Inc., Covia Holdings LLC, Hi-Crush Inc., Hexion Inc., Saint-Gobain Proppants, Badger Mining Corporation, Emerge Energy Services LP, Preferred Sands, Fairmount Santrol Holdings Inc., Atlas Sand Company LLC, Mineração Curimbaba, Xinmi Wanli Industry Development Co. Ltd., China GengSheng Minerals Inc., ChangQing Proppant, CoorsTek Inc., Eagle Materials Inc., Fores LTD, Halliburton Company, and Baker Hughes Company |

Frequently Asked Questions

The Proppants Market is expected to grow at a CAGR of 8.89% from 2026 to 2035.

The Proppants Market was valued at USD 10.99 Billion in 2025.

Rising shale gas and tight oil exploration, growing investment in oilfield infrastructure and logistics, and demand for enhanced oil recovery techniques are the primary growth factors.

The Frac Sand segment dominated the Proppants Market with approximately 58% share in 2025.

North America dominated the Proppants Market with approximately 48% revenue share in 2025.

Get in Touch