Pyridine & Pyridine Derivatives Market Report Scope & Overview:

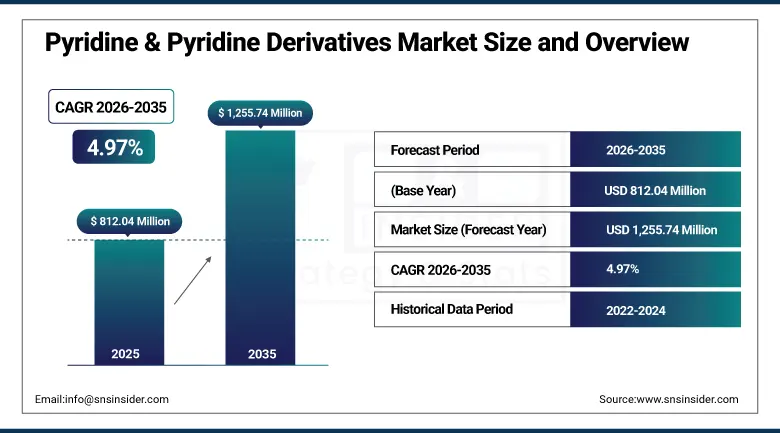

The Pyridine & Pyridine Derivatives Market was valued at USD 812.04 Million in 2025 and is expected to reach USD 1,255.74 Million by 2035, growing at a CAGR of 4.97% from 2026 to 2035.

The global pyridine and pyridine derivatives market forms an important part of the specialty chemicals and pharmaceutical intermediates markets. Pyridine and its derivatives are heterocyclic organic chemicals widely utilized as solvents, reagents and intermediates. The special structure of the compound makes it highly reactive and stable, which makes it crucial in complex formulations. The report covers detailed analysis of global usage rate among key producers and types of products. The report mentions regulatory issues associated with application in agrochemicals and pharmaceuticals and environmental performance in terms of emissions and sustainable measures taken by key players. The innovations in R&D cover developments in bio-pyridine and green syntheses.

By 2024, Jubilant Ingrevia will be expanding its pyridine and picoline production facilities in its Gajraula, India site, with annual capacity enhanced to meet the rising demands from agrochemical and pharmaceutical intermediates consumers from both Asia and foreign exporters. This is a result of the inherent competitive benefit possessed by vertically integrated pyridine derivative manufacturers, in which the backward integration of beta picoline and other critical intermediates provides significant advantages over merchant producers relying on third-party intermediates.

Market Size and Forecast

-

Market Size in 2026E: USD 852.40 Million

-

Market Size by 2035: USD 1,255.74 Million

-

CAGR: 4.97% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Pyridine & Pyridine Derivatives Market - Request Free Sample Report

Pyridine & Pyridine Derivatives Market Trends

-

Bio-based pyridine production technologies are gaining traction as manufacturers adopt renewable feedstocks to support sustainable chemical manufacturing.

-

Rising demand for high-purity pyridine derivatives is supporting pharmaceutical intermediate production, particularly for vitamins, APIs, and specialty drug formulations.

-

Innovation in agrochemical formulations is increasing the use of pyridine derivatives to improve crop protection efficiency and product performance.

-

Expanding applications in electronics and specialty chemicals are creating new growth opportunities for pyridine-based catalysts, solvents, and corrosion inhibitors.

-

Digital process optimization and advanced manufacturing technologies are improving production efficiency, quality consistency, and regulatory compliance across pyridine manufacturing facilities.

U.S. Pyridine & Pyridine Derivatives Market Outlook

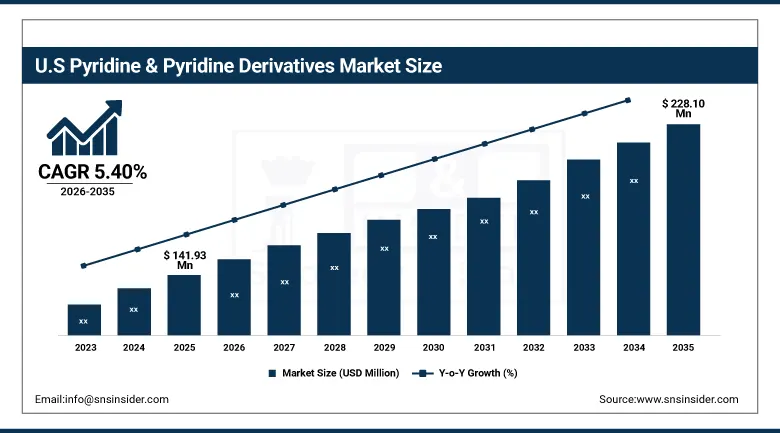

The U.S. Pyridine & Pyridine Derivatives Market was valued at approximately USD 141.93 Million in 2025 and is expected to reach approximately USD 228.10 Million by 2035, growing at a CAGR of approximately 5.40%.

In 2025, the largest share was accounted for by the United States in the pyridine & pyridine derivatives market. This market dominance can be mainly credited to the presence of strong pharmaceutical and agrochemical industries in the country, which are significant end users of pyridine derivatives. Availability of major market players, advanced research and development infrastructure, and continuous innovation-friendly regulatory policies for crop protection chemicals and pharmaceutical formulations help in boosting the demand further. The United States enjoys the advantage of advanced technology for chemical synthesis, skilled labor force, and established supply chain systems, thus resulting in improved efficiency in production and faster commercialization of new derivatives.

Vertellus Holdings increased the production capacity for specialty intermediates at its plant located in Indianapolis, Indiana in the year 2023 in order to increase the capacity for producing high purity pyridine derivatives used by pharmaceutical companies in their manufacturing operations to produce active pharmaceutical ingredients under strict quality guidelines. This indicates the efforts made by domestic suppliers in the U.S. in terms of investing in high specification pyridine derivatives.

Pyridine & Pyridine Derivatives Market Segment Analysis

-

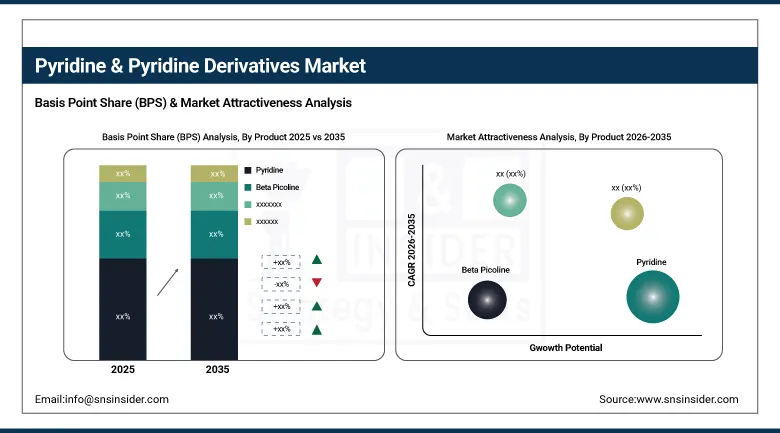

By Product, the pyridine segment dominated the pyridine & pyridine derivatives market with approximately 41.0% share in 2025, while the beta picoline segment is the fastest growing.

-

By Application, the herbicides segment dominated the pyridine & pyridine derivatives market with approximately 36.8% share in 2025, while the pharmaceuticals and APIs segment is the fastest growing.

-

By Production Process, the chemical synthesis segment dominated the pyridine & pyridine derivatives market with approximately 91.5% share in 2025, while the bio-based production segment is the fastest growing.

-

By End-Use, the agrochemicals segment dominated the pyridine & pyridine derivatives market with approximately 44.7% share in 2025, while the pharmaceuticals segment is the fastest growing.

By Product, pyridine dominates, beta picoline grows fastest

Pyridine retained the dominant product position with approximately 41.01% of the pyridine and pyridine derivatives market in 2025. Pyridine is an organic compound that belongs to the heterocyclic category and serves as a basic compound for the manufacture of various chemicals. Pyridine is mainly dominant due to the high need of pyridine in pesticides, especially in herbicides like paraquat and insecticides like chlorpyrifos. The commercial value of pyridine is also extended through its function as a solvent and reagent for organic synthesis and utilization in vitamin B3, also known as niacin, and antihistamine agent manufacturing.

Beta picoline is the fastest growing product because its applications span both pharmaceutical and agrochemical sectors whose combined demand growth outpaces other derivative categories. Beta picoline is a vital feedstock in the synthesis of vitamin B6, pyridoxine, which is highly sought after in nutritional supplements and food fortification programmes. The chemical is also widely used in the manufacturing of herbicides such as picloram, an agrochemical that is highly effective in protecting crops and controlling weeds across major agricultural economies. The wide range of application areas and the important role beta picoline plays in both the agro based and pharmaceutical industries explain its accelerating commercial growth trajectory throughout the forecast period.

By End-Use, agrochemicals dominates, pharmaceuticals grows fastest

Agrochemicals retained the dominant end use position in the pyridine and pyridine derivatives market in 2025. Pyridine is a building block in the manufacture of crop protection chemicals including paraquat, diquat, and chlorpyrifos. As populations continue growing, demand for larger crop yields is required, and with the dearth of additional arable land, the usage of agrochemicals has expanded, especially in developing economies. In addition, rising interests in the formulation of improved agrochemical products have contributed to an ongoing demand for pyridine derivatives owing to the advantageous properties possessed by the pyridine group. Regulations in favor of superior agricultural products and knowledge about superior farming techniques have further strengthened the commercial position of this segment within the global agrochemical value chain.

Pharmaceuticals is the fastest growing end use because the expanding pharmaceutical industry continues driving demand for pyridine derivatives in drug synthesis applications, particularly as the increasing prevalence of chronic diseases creates rising demand for novel effective treatment solutions. Pyridine's chemical properties enable complex molecule synthesis, which supports pharmaceutical innovation and the development of new therapeutic solutions aligned with global healthcare needs. The pharmaceutical field application of pyridine, mainly for the synthesis of drugs and advanced intermediates, continues trending upward as the geriatric population expands and demand for generic drug production in developing economies sustains above average procurement growth for pyridine derivative manufacturers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Pyridine & Pyridine Derivatives Market Insights

North America is a technically sophisticated pyridine and pyridine derivatives market where robust demand from the pharmaceutical and agrochemical sectors sustains consistent commercial procurement. Increased regulatory policies and improved technology in synthesis processes contribute to the growth of the regional market as well. The United States generates around 87.4% of the revenue of North America via Vertellus Holdings, Lonza Group, and other leading chemical companies' commercial activities in their domestic market.

Canada contributes complementary North American revenue through its agrochemical manufacturing sector's pyridine derivative procurement and the growing pharmaceutical contract manufacturing industry's demand for high purity chemical intermediates serving cross border pharmaceutical supply chains.

Europe Pyridine & Pyridine Derivatives Market Insights

Europe moves along the same path as North America, albeit with the major contributions coming from the chemical and healthcare industries. The stricter environmental laws in Europe further encourage the production of bio-based pyridine derivatives in conformity with sustainable practices that provide differentiation in business for companies able to prove their eco-friendly production process. Germany contributes about 22.3% of European sales due to its robust pharmaceuticals and agrochemical manufacturing industry, as well as the presence of chemical companies.

The United Kingdom and France are significant secondary markets where pharmaceutical manufacturing and agrochemical formulation create consistent procurement. Lonza Group's Swiss headquartered operations and other European chemical manufacturers sustain regional commercial supply across the continent's pyridine derivative landscape.

Asia Pacific Pyridine & Pyridine Derivatives Market Insights

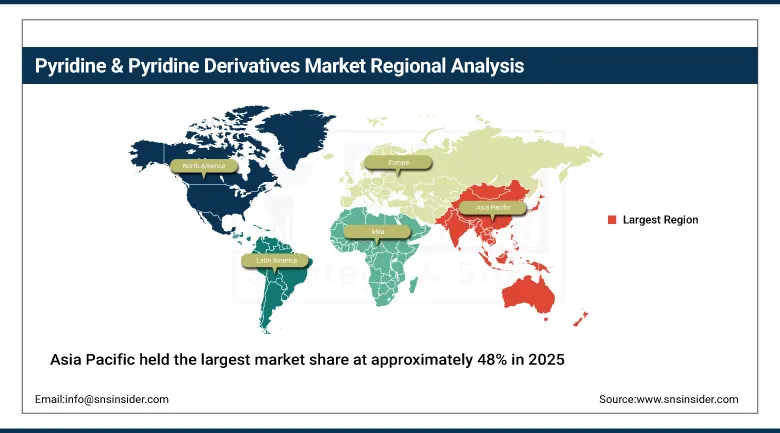

Asia Pacific held the largest market share at approximately 48% in 2025. This is because of the existence of an already established manufacturing base, developing agricultural sector, and the growing industries of pharmaceutical and chemical in this region. The major use and production of pyridine takes place in nations such as China and India since there is a huge consumption of chemicals in their regions for the manufacture of pesticides. In Asia Pacific, China makes about 44.8% of the revenue since it has a strong chemical industry base and it produces a lot of pyridine.

Market growth has further been boosted by the region's ability to produce cost effective units, the abundance of raw materials in the region, and government initiatives to promote growth in the industrial sector. In addition, the increasing food demand coupled with further penetration of modern agricultural practices in Southeast Asia has boosted demand for pyridine-based crop protection products. India represents a particularly dynamic emerging market within Asia Pacific where rapid agriculture development and growth in the agricultural sector backed by demand for pyridine-based herbicides sustain above average regional procurement growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Pyridine & Pyridine Derivatives Market Insights

Latin America and the Middle East and Africa are emerging as potential growth markets, supported by increasing investments in agriculture and industrialization. Saudi Arabia leads MEA revenues through its growing chemical manufacturing sector and agricultural development investment under Vision 2030 diversification programmes. The UAE's expanding chemical processing industry adds complementary Gulf demand.

Brazil leads Latin American revenues through its large agrochemical manufacturing sector whose pesticide and herbicide production creates substantial domestic pyridine derivative procurement. Argentina's agricultural sector and Mexico's growing chemical industry collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Rising agrochemical demand and expanding pharmaceutical applications

There has been an increase in the demand for agrochemicals globally owing to the increased demand for crop protection and agricultural productivity. Pyridine and its derivatives serve as important intermediaries in the manufacture of herbicides, insecticides, and fungicides, including chlorpyrifos and paraquat. With increasing agricultural production by developing nations due to food security concerns, the demand for chemical compounds derived from pyridine is expected to keep increasing. The utility of pyridine in improving the efficiency and bioavailability of crop protection chemicals makes pyridine one of the more preferred chemicals amongst agrochemical manufacturers. The government policies encouraging the adoption of modern farming methods and pest management systems in nations such as India and Brazil will also contribute to this demand growth.

The expanding pharmaceutical industry represents the second most significant structural growth driver for the pyridine and pyridine derivatives market. Growing demand for increased production from smaller amounts of arable lands will be expected to keep driving the use of agrochemicals, whereas growing use of pyridine by pharmaceutical companies in the manufacturing of active pharmaceutical ingredients will keep driving demand in chronic illness treatments, vitamins, and antihistamines.

Restraints: Raw material price volatility and stringent environmental regulations

The production of pyridine is heavily dependent on key petrochemical-based feedstocks such as acetaldehyde, ammonia, and formaldehyde. Volatility in the prices of these raw materials due to crude oil price fluctuations and geopolitical tensions poses a serious challenge for pyridine manufacturers. In addition to this, any disruptions in the supply chain and limited availability of high purity feed stocks may affect the capacity to produce and cost structure. The changes in profitability are particularly affected by these changes, especially for smaller companies which depend on consistent input costs for competitiveness.

Pyridine is considered to be a dangerous chemical owing to its flammable, volatile, and toxic nature, particularly when dealing with larger volumes. Various organizations, including the U.S. EPA, REACH in the European Union, and the Ministry of Ecology and Environment in China, have formulated rigorous environmental and occupational safety standards for the manufacturing, transportation, and storage of pyridine. Adhering to these standards calls for huge investment from firms operating in emerging nations with scarce resources.

Opportunities: Bio based pyridine development and emerging market agricultural expansion

The growing focus on sustainable chemical manufacturing and reducing dependency on fossil-based resources is opening new avenues for the pyridine and pyridine derivatives market. There is a growing trend among manufacturers to focus on developing pyridine from bio-resources like glucose and biomass sources. Such trends are in keeping with the increasing green chemistry movement and the need for manufacturers to cut down on carbon emissions within the chemicals industry. Not only does bio-based production help in reducing the environmental impact, but it also helps address the problem of fluctuating feedstock prices, which has been a major issue with pyridine manufacturing before.

Increasing investments in agriculture and industrialization across emerging Latin American and Middle Eastern markets represent a significant near-term growth opportunity. With increasing support from government policies and consumer preference for environmentally responsible products, the commercial viability of green pyridine production is expected to improve significantly in the coming years, creating differentiated market positioning for manufacturers capable of demonstrating sustainable production credentials.

Recent Developments:

-

2026: Jubilant Ingrevia Limited expanded its pyridine and pyridine derivatives production capacity to meet rising demand from agrochemical and pharmaceutical intermediate manufacturers.

-

2026: Vertellus Holdings LLC introduced high-purity pyridine derivative grades for pharmaceutical and specialty chemical applications, strengthening its advanced intermediates portfolio.

-

2026: Resonance Specialties Limited enhanced its pyridine derivatives manufacturing capabilities through process optimization and capacity expansion to support growing domestic and export demand.

-

2026: Lonza Group AG expanded the use of high-purity pyridine-based intermediates within its pharmaceutical manufacturing network to support increasing demand for active pharmaceutical ingredient (API) production.

Pyridine & Pyridine Derivatives Market Key Players are:

-

Jubilant Ingrevia Limited

-

Vertellus Holdings LLC

-

Lonza Group AG

-

Resonance Specialties Limited

-

Shandong Luba Chemical Co., Ltd.

-

Chang Chun Petrochemical Co., Ltd.

-

Koei Chemical Co., Ltd.

-

C-Chem Co., Ltd.

-

Jiangsu Yangnong Chemical Co., Ltd.

-

Red Sun Group

-

Mitsubishi Chemical Corporation

-

Nippon Shokubai Co., Ltd.

-

Tokyo Chemical Industry Co., Ltd.

-

Shandong Hongda Biotechnology Co., Ltd.

-

Hefei TNJ Chemical Industry Co., Ltd.

-

Lasons India Private Limited

-

Jiangsu Jiannong Agrochemical Co., Ltd.

-

Merck KGaA

-

Thermo Fisher Scientific Inc.

-

Tokyo Chemical Industry (India) Pvt. Ltd.

Pyridine & Pyridine Derivatives Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 812.04 Million |

| Market Size by 2035 | USD 1,255.74 Million |

| CAGR | CAGR of 4.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Pyridine, Beta Picoline, Alpha Picoline, Gamma Picoline, Others) • By Application (Herbicides, Insecticides, Vitamins and Nutritional Supplements, Pharmaceuticals and APIs, Solvents and Chemical Intermediates, Others) • By Production Process (Chemical Synthesis, Coal Tar Extraction, Bio-based Production, Others) • By End-Use (Agrochemicals, Pharmaceuticals, Electronics, Food and Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Jubilant Ingrevia Limited, Vertellus Holdings LLC, Lonza Group AG, Resonance Specialties Limited, Shandong Luba Chemical Co., Ltd., Chang Chun Petrochemical Co., Ltd., Koei Chemical Co., Ltd., C-Chem Co., Ltd., Jiangsu Yangnong Chemical Co., Ltd., Red Sun Group, Mitsubishi Chemical Corporation, Nippon Shokubai Co., Ltd., Tokyo Chemical Industry Co., Ltd., Shandong Hongda Biotechnology Co., Ltd., Hefei TNJ Chemical Industry Co., Ltd., Lasons India Private Limited, Jiangsu Jiannong Agrochemical Co., Ltd., Merck KGaA, Thermo Fisher Scientific Inc., Tokyo Chemical Industry (India) Pvt. Ltd. |

Frequently Asked Questions

Asia Pacific dominated the Pyridine & Pyridine Derivatives Market with approximately 48% of revenues in 2025.

The Pyridine & Pyridine Derivatives Market was valued at USD 812.04 Million in 2025.

The market is expected to grow at a CAGR of 4.97% from 2026 to 2035.

Rising global demand for agrochemicals as developing countries increase agricultural output to meet food security demands.

Pyridine dominated the Pyridine & Pyridine Derivatives Market with approximately 41.01% share in 2025.

Get in Touch