Refurbished Computers and Laptops Market Report Scope & Overview:

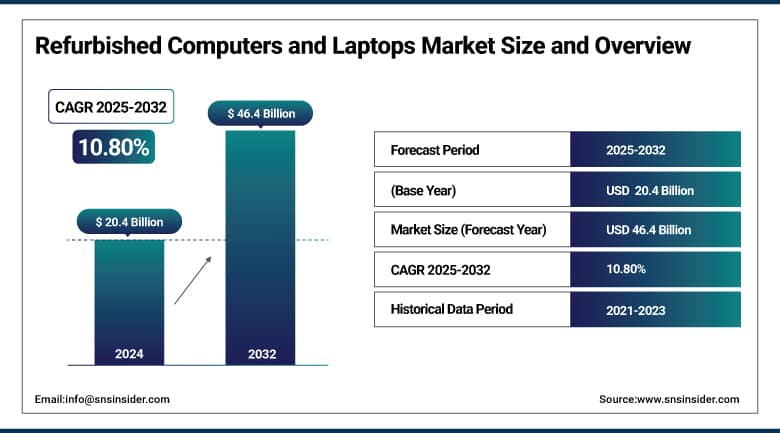

The Refurbished Computers and Laptops Market size was valued at USD 20.4 billion in 2024 and is expected to reach USD 46.4 billion by 2032, growing at a CAGR of 10.80% during 2025-2032.

The refurbished computers and laptops market growth is driven by the increasing environmental awareness, cost-effectiveness, and the global thrust for sustainable consumption. Some of the growing consumer and institutional confidence behind refurbished devices as a viable alternative to new hardware can be traced in part to higher refurbishment standards and longer warranties. The refurbished computers and laptops market trends, such as increased demand for refurbished computers and laptops in educational and small business sectors, a growing preference for online refurbished marketplaces, and growing government support for electronic waste reduction, are also explained in the research report. Secondly, market penetration is being hastened by hybrid work models and the adoption of e-learning. Refurbished Computers and Laptops Market analysis indicates that quality assurance, through data security and brand certification, continues to remain a key factor surrounding a company to achieve critical success. The future would be the introduction of more innovations in diagnostics and testing tools, which would not only bolster consumer confidence but would broaden utilization in emerging and developed economies as well.

To Get More Information On Refurbished Computers and Laptops Market - Request Free Sample Report

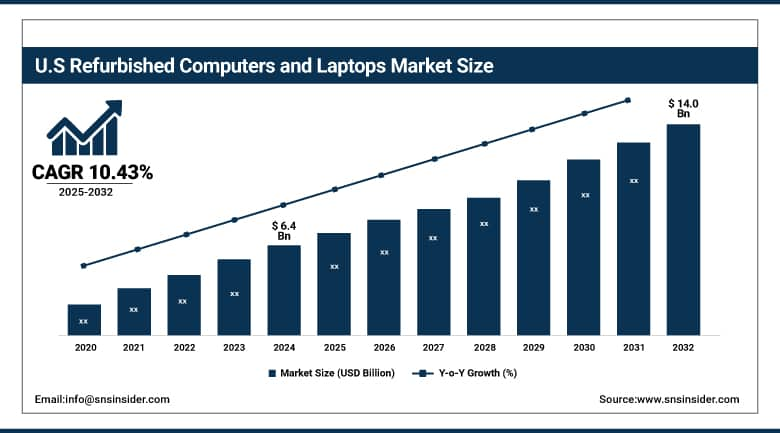

The refurbished computers and laptops market in the U.S. is anticipated to increase from USD 6.4 billion in 2024 to about USD 14.0 billion by 2032, at a CAGR of roughly 10.43% during the projected period. Increasing demand for low-cost technology, sustainability programs, and more continues to drive growth for the industry, which has become more of an allowable expense due to remote work trends. Future growth will be sustained by further improvement in refurbishment standards and the digital retail platforms.

Market Dynamics:

Drivers:

-

High Demand for Affordable Tech Solutions Increases Consumer Adoption of Refurbished Computers and Laptops

Refurbished PCs are a cost-effective option compared to new PCs, therefore making them an appealing purchase for price-sensitive consumers, students, startups, and SMEs alike. Inflationary pressures and new hardware prices spiking ever higher have more users in the market for solid, yet cheap devices. The refurbishment sector often offers warranties and certification testing of refurbished components, along with upgraded new components sold as refurb units, adding an element of consumer trust. The trend also correlates with the boom of remote learning and hybrid work. Secondly, with increasing awareness about sustainability, refurbished electronics provide a sustainable, economic option, without much loss in use, this is also driving adoption in personal and institutional spaces.

In June 2024, Lenovo implemented an AI-powered refurbishment process that boosted refurbished unit output by 116%, reflecting growing demand and operational scalability in the U.S.

Restraints:

-

Concerns Over Reliability and Shorter Lifespan Limit Buyer Confidence and Slow Market Growth

While interest in refurbished devices is growing, many consumers still refrain from purchasing refurbished computers and laptops because of low reliability and a short service life. There are still some perceptions amongst users around the performance inconsistency or the vintage of pre-owned electronics that exist, especially on the professional and gaming end of the spectrum. Likewise, without trusted refurbishment certificates or obvious warranty terms, it might cause distrust among buyers in relation to the product situation or service support. That reluctance prevents mass uptake, especially in performance-oriented or enterprise environments. This restraint can be overcome by the implementation of strict quality checks, transparent refurbishment processes coupled with post-sale service supports offered by the vendors, which are expected to allay the uncertainties of buyers owing to the negative proclivity of refurbished electronics.

A 2024 survey found that nearly 30% of consumers still avoid purchasing refurbished laptops due to worries about hidden defects, shorter functional lifespans, and inconsistent quality assurance.

Opportunities:

-

Rising E-Waste Regulations and Circular Economy Initiatives Boost Market Potential for Refurbished Electronics Solutions

With e-waste regulations tightening around the world and nationally, the market for refurbished electronics is becoming strategically important. Also, legislation in the US stimulating electronic waste recycling and sustainable manufacturing helps in the resell of old computers and laptops. This makes the refurbished market a perfect fit for the circular economy, prolonging the product's life cycle and decreasing landfill impact and carbon emissions. More and more, tech companies are adding refurbishment to their sustainability game plan, providing trade-in programs and certified pre-owned lines. This provides the dual benefit of creating new revenue streams and increasing brand reputation. With sustainability-driven policy pressure tightening, coupled with peaking demand for eco-consciousness, the green business model vendors are set to capitalise on unlimited growth potential.

For Instance, Refurbishment and recycling centers in the U.S. processed 45 million laptops in 2024, up from 38 million in 2023—an 18% rise that reflects stronger circular‑economy initiatives

Challenges:

-

Lack of Standardized Refurbishment Practices Creates Inconsistency and Reduces Consumer Trust

A prominent issue with the refurbished market is that there are no universal refurbishment standards. Consumer confusion and scepticism prevail, quality checks are selective and often unstandardised, grading systems are vague (Grade A/B/C), and the warranty structure is also an alien concept. And this inconsistency also harms cross-platform product comparisons, or trust in independent refurbishers. The absence of well-defined industry benchmarks contributes to fragmented trust and creates reputation risks for the market. There is a need for collaboration between regulatory bodies and industry alliances to establish standardized refurbishment guidelines, the development of certification schemes, and consumer protection measures that support product transparency. This is the only way for the industry to scale and, in doing this, achieve wider acceptance from consumers and institutions.

Segmentation Analysis:

By Product:

The refurbished laptops segment dominated the market and accounted for 74% of the refurbished computers and laptops market share in 2024, owing to their portability, greater demand from consumers, including education and remote work, resale convenience, and online channels. smart phones, tablets and refurbished laptops – for mobility and affordability in remote learning and hybrid work. Steady adoption due to increasing demand for schools/startups/freelancers, low cost of ownership, and improving refurbishers' quality assurance. The ubiquitous expansion of e-commerce platforms, coupled with increasing awareness of sustainable technology consumption, also ensures the segment continues to dominate in both consumer and commercial markets.

Refurbished desktop computers are expected to gain the fastest CAGR during the forecast period. The keys to fast-tracking adoption are enhanced enterprise IT upgrades, digital lab, and other government-backed educational infrastructure construction, with refurbished desktop computers soon set to witness sharp growth. Demand is supported by their durability, greater processing capacity, and lower cost relative to new systems. Desktop refurbishment will be driven by rising interest from cost-conscious institutions and a growing demand for digital inclusivity in emerging markets and other constrained environments.

By Operating System:

Windows segment dominated the refurbished computers and laptops market in 2024 and accounted for 47% of revenue share. Windows OS has been the default operating system for personal computers everywhere, from consumer, educational, and enterprise environments, and thus provides the highest level of compatibility at the lowest price point available. With such a large worldwide user base, support for a range of applications and hardware, Windows OS tops the refurbished market. Windows has, by default, seemed to be the most preferred system for government, corporate, and educational purposes for standardization.

The Linux OS is projected to register the fastest CAGR. As preference for open-source platforms, which in their true nature are cheap, highly secure, and adaptable, increases, refurbished Linux systems will likely emerge as one of the fastest-growing domains in the market. Linux is being adopted in education, development, and government sectors, where even a small reduction in licensing fees can amount to significant savings. With the increase of digital literacy and the further improved refurbishing tools for Linux, this area will experience strong adoption in developing countries and innovative institutes.

By Sales Channel:

The offline/Brick & Mortar Stores dominated the market in 2024 and accounted for a significant revenue share, as most of the consumers still prefer checking the product before purchasing it, which creates a very high level of confidence among the buyers when purchasing from a physical location. Refurbished sales by brick & mortar stores take the lead as customers choose to have physical inspection, in-house tech support, and immediate pickup. People buy systems they can walk into and buy, and get after-sales service; retailers who sell certified refurbished systems with a warranty do just that. In developing regions where the digital divide remains high and online payment trust is low, it is quite common that buyers will want to test hardware first before buying it.

Driven by a rise in digital accessibility and ease of use, the Online/e-commerce segment is expected to register the fastest CAGR. Higher acceptance of certified refurbished products is driving online/e-commerce sales due to reach, dynamic pricing, and easier comparison. You can buy either via marketplaces like Amazon Renewed with detailed specs and a verification of refurbishment and return policies, or from OEM-run outlets. Rising smartphone penetration, the use of digital wallets, and rapid delivery services are helping online sales grow, particularly among the digitally savvy youth and small business buyers.

Regional Analysis:

North America holds the largest market share owing to mature refurbishment infrastructure, robust ITAD practices, and increasing awareness around sustainability. High adoption is supported by the institutional buyers and government-backed initiatives. Circular economy policies, increasing hybrid work policies, and further partnerships between OEMs and refurbishers will keep these two segments dominant, especially the education, enterprise, and public sector segments, where the device is used most often, but not exclusively, in a one-to-many use case.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia-Pacific is well on course to registering the fastest growth, supported by digital inclusion initiatives, a large cost-sensitive population, and rapid growth of e-commerce in the region. Demand from schools, startups, and rural digitization programs boosts its adoption. With the introduction of government incentives, increasing technology penetration, and online resale platforms that can be replicated almost anywhere, the region will transform into a global hub for the demand and reselling of used devices by 2032.

The development is favored by strong e-waste regulations, circular economy policies, and high digital awareness in Europe. Sustainable use of technology among governments and enterprises is growing, and this is driving demand for refurbished devices. High confidence from consumers, ongoing digital education programs, and the development of EU-wide refurbishment standards will sustain strong growth through to 2032, with Germany, the UK, France, and Nordic countries focused on green IT adoption.

Due to robust environment policy, broad digital infrastructure, and high consumer confidence in certified refurbishers, Germany was by far the strongest market for refurbished computers and laptops in Europe. Stable market growth will be maintained by government-driven sustainability objectives, increasing IT circularity in education, and the adoption of circular tech at an enterprise level through 2032.

Key Players:

The major refurbished computers and laptops market companies are Apple Inc., Lenovo Group Ltd., HP Inc., Dell Technologies Inc., ASUSTeK Computer Inc., Samsung Electronics Co. Ltd., Acer Inc., Sony Corporation, LG Electronics Inc., Microsoft Corporation, Toshiba Corporation and others

Recent Developments:

In February 2024, Apple Inc. Added the first M3 Pro/Max MacBook Pro models to its official Refurbished Store at launch‑price discounts (e.g., 14″ M3 Pro at $1,699)

In Jun 2025, Apple Inc. Refurbished Grade A MacBook Air 2017 being sold for just $199.97, showcasing Apple’s aggressive pricing to expand refurbished reach

In Mar 2025, Lenovo Group Ltd. Launched ThinkPad X9 Gen 1 series (laptops with AI features), enhancing potential for certified refurbishment

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | US$ 20.4 Billion |

| Market Size by 2032 | US$ 46.4 Billion |

| CAGR | CAGR of 10.80% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Refurbished Laptops, Refurbished Desktop Computers), • By Operating System (Windows OS, Mac OS, Linux OS), • By Sales Channel (Online/eCommerce, Offline/Brick & Mortar Stores) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Apple Inc., Lenovo Group Ltd., HP Inc., Dell Technologies Inc., ASUSTeK Computer Inc., Samsung Electronics Co. Ltd., Acer Inc., Sony Corporation, LG Electronics Inc., Microsoft Corporation, Toshiba Corporation and others in the report |

Frequently Asked Questions

North America region dominated the Refurbished Computers and Laptops Market with 40% of revenue share in 2024.

The refurbished laptops segment dominated the market and accounted for 74% of the refurbished computers and laptops market share in 2024

High Demand for Affordable Tech Solutions Increases Consumer Adoption of Refurbished Computers and Laptops

The Refurbished Computers and Laptops Market size was valued at USD 20.4 billion in 2024 and is expected to reach USD 46.4 billion by 2032

The expected CAGR of the Refurbished Computers and Laptops Market over 2025-2032 is 10.80%.

Get in Touch