Robotics as a Service Market Report Scope & Overview:

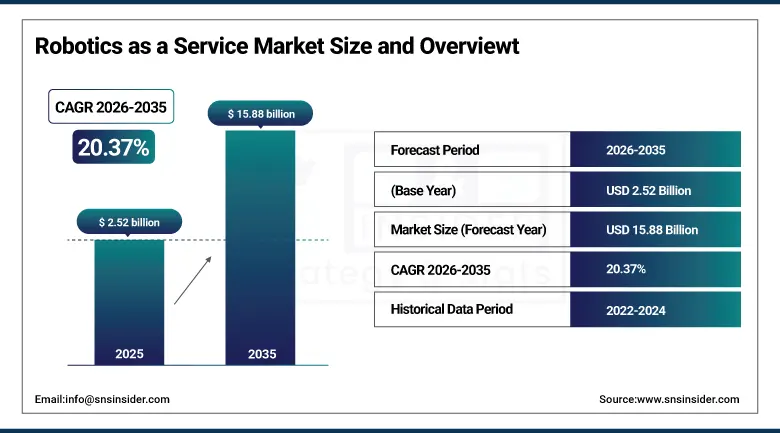

The Robotics as a Service Market was valued at USD 2.52 Billion in 2025 and is expected to reach USD 15.88 Billion by 2035, growing at a CAGR of 20.37% from 2026 to 2035.

The robotics as a service (raas) market is experiencing strong growth as organizations increasingly adopt flexible automation solutions that eliminate the need for large upfront investments in robotic infrastructure. Growing labor shortages, rising operational costs, and the need for higher productivity are encouraging businesses to deploy robots through subscription and pay-per-use models. The expansion of e-commerce, warehouse automation, smart manufacturing, and healthcare robotics is further accelerating demand. Advancements in artificial intelligence, machine vision, cloud connectivity, and autonomous mobile robots are improving robotic capabilities and accessibility. Additionally, scalable service agreements and remote fleet management are making automation more practical for businesses of all sizes.

The global Robotics-as-a-Service (RaaS) market continued to gain momentum in 2025 through strategic partnerships, technological innovation, and growing automation investments. DHL expanded its collaboration with Locus Robotics, deploying more than 5,000 autonomous mobile robots (AMRs) across warehouse and fulfillment operations to improve productivity and order accuracy. At the same time, Geek+ strengthened its global footprint by supporting over 770 customer projects across logistics, retail, and manufacturing sectors. Governments and industry organizations increased investments in smart manufacturing and digital transformation initiatives, encouraging wider robotics adoption. These developments enhanced operational efficiency, reduced deployment costs, and accelerated the transition toward scalable, subscription-based robotic automation solutions worldwide.

Market Size and Forecast

-

Market Size in 2026E: USD 2.99Billion

-

Market Size by 2035: USD 15.88 Billion

-

CAGR: 20.37% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Robotics as a Service Market - Request Free Sample Report

Robotics as a Service Market Trends

-

Shift to cloud-based fleet management platforms with zero-touch provisioning, edge AI inference, and role-based access controls to align with enterprise IT governance.

-

Interoperability initiatives enabling multi-vendor robot coordination via shared APIs and orchestration layers that reduce vendor lock-in and integration complexity.

-

Growth in outcome-based pricing tied to picks per hour, lines fulfilled, or station cycle time, distributing performance risk between providers and customers.

-

Uptake of predictive maintenance with sensor fusion, enabling providers to guarantee uptime and proactively dispatch field service under SLA terms.

-

Adoption of vision-as-a-service for inspection and quality control, allowing rapid deployment of defect detection models trained on anonymized cross-site datasets.

The U.S. Robotics as a Service Market Outlook

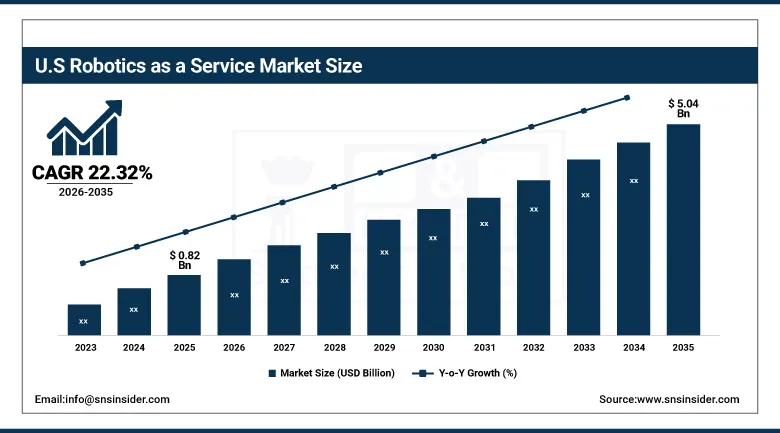

The U.S. robotics as a service market was valued at approximately USD 0.82 Billion in 2025 and is expected to reach approximately USD 5.04 Billion by 2035, growing at a CAGR of approximately 22.32%.

The U.S. robotics as a service market was valued at approximately USD 0.82 Billion in 2025 and is expected to reach approximately USD 5.04 Billion by 2035, growing at a CAGR of approximately 22.32%. The U.S. market benefits from a strong base of e-commerce fulfillment centers, advanced manufacturing hubs, and hospital networks seeking scalable automation. In 2025, a public–private program co-led by the National Institute of Standards and Technology and industry partners funded interoperability testbeds linking AMRs with warehouse management systems, improving cross-fleet traffic control. A consortium of providers and retailers piloted “throughput-guaranteed” RaaS contracts, delivering measurable reductions in dwell time and labor variability.

The U.S. robotics ecosystem strengthened significantly in 2025 through government-backed automation programs, private-sector investments, and large-scale deployment of Robotics as a Service (RaaS) solution. Advanced manufacturing and supply chain modernization initiatives accelerated adoption across logistics, warehousing, and industrial operations. The deployment of robotic automation systems across major fulfillment centers improved order processing efficiency by more than 30% while reducing manual material handling requirements by approximately 40%. In addition, AI-enabled robotics projects supported by federal and state innovation funding reduced deployment timelines by nearly 25%. Subscription-based robotics models also lowered initial automation investment costs by up to 50%, making advanced robotic technologies more accessible to businesses of all sizes.

Robotics as a Service Market Segment Analysis

-

By Type, the industrial robotics segment dominated the robotics as a service market with 41.39% share in 2025, while the collaborative robots (cobots) segment is the fastest growing type with the highest CAGR of 21.84% from 2026 to 2035.

-

By Application, the material handling segment dominated the robotics as a service market with 27.69% share in 2025, while the packaging & sorting segment is the fastest growing material type with the highest CAGR of 21.65% from 2026 to 2035.

-

By Deployment Type, the cloud-based robotics platforms segment dominated the robotics as a service market with 51.69% share in 2025, while the it is also the fastest growing deployment type with the highest CAGR of 20.86% from 2026 to 2035.

-

By End-User Industry, the manufacturing segment dominated the robotics as a service market with 32.58% share in 2025, while the logistics & warehousing segment is the fastest growing end user category with the highest CAGR of 21.82% from 2026 to 2035.

By Type, industrial robotics dominate the robotics as a service market, collaborative robots (cobots) grow faster

Industrial robotics accounted for the largest share of RaaS market with share of 41.39% in 2025, reflecting contracts that package high-duty-cycle arms, controls, and service into predictable operating expense. Providers combined rapid cell design, digital simulation, and ongoing optimization, helping factories adapt stations to volume shifts without capital strain. Meanwhile, collaborative robots and AMRs recorded the highest growth on the back of fast re-tasking and low integration friction. In 2025, a joint initiative between a leading cobot manufacturer and a tooling consortium delivered subscription kits for screwdriving, dispensing, and test operations, cutting station commissioning weeks to days and broadening midmarket adoption.

Collaborative Robots (Cobots) emerged as one of the fastest-growing segments within the Robotics as a Service (RaaS) market as manufacturers increasingly adopted flexible automation solutions that allow robots and human workers to operate safely side by side. Several cobot providers partnered with AI and machine vision companies to enhance real-time object recognition, adaptive task execution, and quality inspection capabilities. RaaS providers bundled deployment, programming, maintenance, and software updates into subscription-based service models, reducing implementation complexity for small and medium-sized enterprises. Cobots were increasingly deployed for assembly, material handling, packaging, and machine tending applications, while new AI-enabled models improved productivity and reduced training requirements.

By Application, material handling dominates the robotics as a service market, packaging & sorting grow faster

Material handling was the largest application segment with market share of 27.69% in 2025 given its ubiquity across manufacturing and logistics, with RaaS contracts covering transport, kitting, putwall replenishment, and line-side delivery. Providers leveraged modular workflows, standardized interfaces, and plug-ins to warehouse and manufacturing execution systems. Packaging & sorting posted the fastest growth, boosted by automated induction, item singulation, and mixed-SKU cartonization delivered under service models. A government-backed SME accelerator in Europe funded pilot lines using vision-enabled pick-and-place cobots offered as a service, demonstrating short paybacks with seasonal scaling. Inspection & quality control gained ground as vision subscriptions simplified model deployment and updates.

Packaging & Sorting emerged as a rapidly expanding application segment within the Robotics as a Service (RaaS) market as e-commerce growth, rising order volumes, and increasing labor shortages drove demand for automated fulfillment operations. Robotics providers expanded AI-powered packaging and sorting solutions capable of handling diverse product sizes, dynamic order flows, and high-throughput warehouse environments. Service-based offerings bundled robotic hardware, warehouse management software integration, predictive maintenance, and performance analytics under recurring subscription models. Advanced vision systems and machine learning algorithms improved package identification, sorting accuracy, and throughput efficiency while reducing manual handling requirements.

By Deployment Mode, cloud-based robotics platforms dominate the robotics as a service market, while it also grows faster

Cloud-based robotics platforms held the majority share in 2025 with 51.69% share and are expected to increase through 2035, driven by centralized fleet management, over-the-air updates, and scalable analytics. Providers implemented zero-trust architectures, role-based controls, and encrypted telemetry pipelines to meet enterprise IT standards. Hybrid deployments advanced where low-latency decision-making and data residency rules apply, running inference at the edge while using cloud for orchestration and lifecycle governance. In 2025, a collaboration between a robotics platform vendor and a hyperscaler introduced a managed robotics service that unified device onboarding, digital twins, and AIOps-based alerting, simplifying multi-site rollouts.

Cloud-Based Robotics Platforms also emerged as the fastest-growing deployment segment within the Robotics as a Service (RaaS) market as organizations increasingly sought centralized fleet management, remote monitoring, and scalable automation capabilities. Robotics providers expanded cloud-native platforms that enable real-time robot orchestration, predictive maintenance, software updates, and performance analytics across multiple sites from a single control interface. Strategic collaborations between robotics manufacturers, cloud service providers, and AI developers enhanced data-driven decision-making and autonomous task optimization. Subscription-based cloud robotics solutions reduced infrastructure complexity and accelerated deployment timelines while improving operational visibility.

By End-User Industry, manufacturing segment dominates, logistics & warehousing segment grow fastest

Manufacturing was the largest end-user segment in 2025 with share of 32.58%, where RaaS bridged skilled labor gaps and supported frequent line changes. Partnerships between robot OEMs, integrators, and machine vision firms produced turnkey cells for assembly, fastening, and inspection under monthly fees. Logistics & warehousing emerged as the fastest-growing end user, propelled by e-commerce peaks, SKU proliferation, and network redesigns. In 2025, a multi-retailer collaboration with service providers introduced shared AMR fleets across adjacent facilities, spreading costs and smoothing seasonality. Healthcare and pharmaceuticals adopted RaaS for material transport and cleanroom handling, safeguarded by specialized sterilization protocols and audit-ready reporting.

Logistics & Warehousing segment emerged as the fastest-growing end-user segment within the Robotics as a Service (RaaS) market, driven by the rapid expansion of e-commerce, increasing fulfillment complexity, and persistent labor shortages across distribution networks. Warehouse operators increasingly adopted subscription-based autonomous mobile robots (AMRs), robotic picking systems, and automated sorting solutions to improve throughput and operational flexibility. RaaS providers expanded cloud-connected fleet management platforms that enabled real-time task allocation, predictive maintenance, and multi-site coordination. Strategic partnerships between logistics companies and robotics vendors accelerated deployment across fulfillment centers, while AI-powered navigation and warehouse orchestration technologies enhanced inventory movement, order accuracy, and resource utilization.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.64% |

|

Europe |

Germany |

35.47% |

|

Asia Pacific |

China |

52.34% |

|

Middle East & Africa |

UAE |

21.10% |

|

Latin America |

Brazil |

38.16% |

North America Robotics as a Service Market Insights

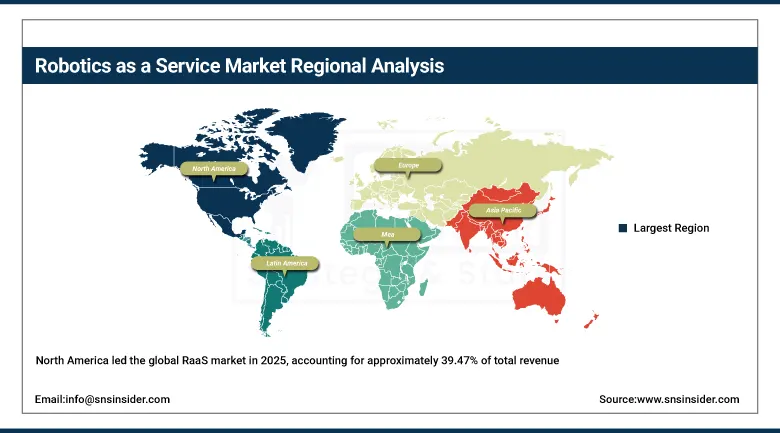

North America led the global RaaS market in 2025, accounting for approximately 39.47% of total revenue, with the United States contributing the vast majority of regional demand. The region’s advantage stems from deep e-commerce penetration, advanced manufacturing clusters, and robust venture and corporate investment in automation. In 2025, a tri-partite collaboration between a major retailer, an AMR platform provider, and a cloud company launched a cross-site orchestration layer that balanced missions among heterogeneous fleets, reducing average fulfillment cycle time. State-backed workforce grants helped reskill associates to robot operator roles, enhancing adoption and change management outcomes.

In 2025, the United States reinforced its leadership in the Robotics as a Service (RaaS) market through continued investment in advanced robotics and artificial intelligence under the National Robotics Initiative (NRI). The program has supported more than 300 robotics research projects, fostering collaboration among universities, technology companies, and industrial organizations. Federal and state-backed automation initiatives increasingly focused on healthcare robotics, defense modernization, and logistics automation, driving broader adoption of subscription-based robotic solutions. Several deployments reported productivity improvements exceeding 20%, while cloud-connected robotic systems expanded across warehouses, manufacturing facilities, and healthcare settings. These developments strengthened innovation, improved operational efficiency, and accelerated automation adoption throughout the U.S. market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Robotics as a Service Market Insights

Europe accounted for approximately 22.10% of global RaaS revenue in 2025, supported by a sophisticated industrial base, stringent safety norms, and strategic initiatives to digitize SMEs. Policymakers prioritized automation grants and tax incentives for cloud-managed robotics, enabling broader access to subscription models. In 2025, a national robotics program partnered with automotive tier suppliers and cobot vendors to qualify pre-engineered assembly cells delivered as a service, cutting time-to-value while meeting CE and functional safety standards. Germany, the UK, France, and Italy anchored regional demand, with growing activity in Spain and the Nordics.

The European Union's digital transformation and industrial automation initiatives, supported through programs allocating more than USD 95 billion for digitalization, AI, and advanced manufacturing technologies through 2030, have accelerated adoption of Robotics as a Service (RaaS) solutions across manufacturing, logistics, and healthcare sectors. In 2025, Germany's, ABB Robotics and Mercedes-Benz expanded AI-enabled robotic automation initiatives in European production facilities, while warehouse automation providers conducted large-scale robotic fleet deployments across regional distribution networks. Early implementation programs reported productivity improvements of up to 25%, reductions in manual material handling tasks exceeding 30%, and faster automation deployment through subscription-based robotics service models.

Asia Pacific Robotics as a Service Market Insights

Asia Pacific represented fastest growing region for global robotics as a service market in 2025 with CAGR of 21.38% through 2025 - 2035. China led regional demand, driven by large-scale manufacturing modernization, government-backed smart factory initiatives, and logistics network expansion. In 2025, a collaboration between leading AMR manufacturers and cloud providers delivered city-scale orchestration pilots across industrial parks, optimizing inter-warehouse flows under subscription. Japan and South Korea advanced cobot-as-a-service in precision manufacturing, while Australia and ASEAN markets accelerated warehouse automation to support cross-border e-commerce.

China's 14th Five-Year Plan, which prioritizes advanced manufacturing, artificial intelligence, and industrial digitalization with investments exceeding USD 10 trillion across strategic technology sectors, has significantly accelerated Robotics as a Service (RaaS) adoption throughout the country. In 2025, major automation providers including Geek+ and ABB Robotics expanded AI-powered warehouse automation and autonomous mobile robot deployments across manufacturing and e-commerce fulfillment centers, with several pilot projects reporting productivity gains of nearly 20% and order processing improvements exceeding 25%. Meanwhile, in Southeast Asia, governments including Indonesia continued supporting smart manufacturing initiatives under Industry 4.0 programs, encouraging partnerships between robotics providers and industrial operators.

Middle East & Africa and Latin America Robotics as a Service Market Insights

Middle East & Africa and Latin America posted strong growth trajectories in 2025, supported by national diversification agendas, logistics infrastructure investment, and rising modern retail formats. In the Middle East, the UAE and Saudi Arabia sponsored innovation hubs that paired AMR vendors with third-party logistics providers to trial RaaS models in bonded and temperature-controlled facilities. Service contracts emphasized rapid commissioning, site acceptance testing, and measured improvements in dock-to-stock cycles. In Africa, retail distribution networks piloted subscription robots to stabilize service levels amid labor and transport variability.

The UAE's National Strategy for Artificial Intelligence 2031 and broader smart industry initiatives have accelerated adoption of Robotics as a Service (RaaS) solutions across logistics, manufacturing, energy, and public service sectors. In 2025, government-backed digital transformation programs supported the deployment of autonomous mobile robots and AI-enabled automation systems in major logistics hubs and industrial facilities, contributing to operational efficiency improvements of up to 30% in selected projects. In East Africa, digital industrialization initiatives and logistics modernization programs supported pilot deployments of cloud-connected robotic systems, helping reduce manual material handling activities by over 20% and accelerating automation adoption across emerging markets.

Market Dynamics

Growth Drivers: Flexible pricing and workforce augmentation unlock enterprise-scale RaaS adoption

Enterprises face persistent labor shortages, variable demand, and pressure to compress payback periods for automation. RaaS lowers barriers by replacing capex with opex and embedding service-level commitments for uptime and performance. In 2025, a consortium of providers and policy agencies launched a co-funding program that subsidized first-year service fees for SME automation pilots, catalyzing adoption in light manufacturing and regional logistics hubs. Vendors introduced standardized cells and AMR kits that integrate into existing workflows without major facility overhauls, improving initial returns and encouraging incremental fleet expansion under multi-year agreements.

The rapid expansion of e-commerce, smart manufacturing, and warehouse automation initiatives is driving strong growth in the Robotics as a Service (RaaS) market across the Middle East. In 2025, regional governments invested over USD 25 billion in industrial digitalization, logistics modernization, and Industry 4.0 programs to support economic diversification strategies. This has accelerated deployment of autonomous mobile robots (AMRs) and AI-powered sorting systems across large fulfillment centers and logistics hubs, with some facilities achieving throughput improvements of more than 35% and labor productivity gains of nearly 25%. Increasing adoption of subscription-based robotics models is further reducing upfront costs, enabling faster and scalable automation adoption across logistics, manufacturing, and retail sectors.

Restraints: Integration complexity, cybersecurity, and change management remain adoption hurdles

Despite strong market momentum, several challenges continue to restrain wider adoption of Robotics as a Service (RaaS) solution. Integration with legacy enterprise software, warehouse management systems, and industrial control infrastructure can increase deployment complexity and implementation timelines. Organizations also require robust assurances regarding data privacy, cybersecurity, and cloud platform reliability before scaling connected robotic operations. In 2025, multiple industry assessments highlighted gaps in network security configurations and interoperability standards across automation environments, prompting vendors to strengthen security frameworks, remote monitoring capabilities, and compliance services. Additionally, workforce training requirements, operational change management, and evolving safety regulations remain key considerations as businesses transition toward large-scale robotic automation.

Opportunities: Multi-vendor orchestration, domain-specific AI, and emerging verticals

As fleets scale, demand is rising for orchestration that manages heterogeneous robots, lifts, and conveyors via standardized interfaces. Providers are investing in APIs and joint certification programs to ensure safe interoperation. In 2025, a public–private lab in Asia ran large-scale trials blending AMRs, cobots, and automated storage systems under a single cloud scheduler, proving throughput gains in multi-modal flows. Domain-specific AI offers further upside: vision models for defect detection, AI-driven slotting for fulfillment, and reinforcement learning for path planning increase value per subscription and differentiate service offerings.

Brazil's digital transformation and industrial modernization initiatives, supported through federal innovation programs and private-sector automation investments, accelerated adoption of Robotics as a Service (RaaS) solutions across logistics, manufacturing, and retail operations in 2025. Major warehouse operators and e-commerce companies expanded deployments of autonomous mobile robots (AMRs) and AI-powered fulfillment systems across distribution centers serving Brazil's rapidly growing online retail sector. Pilot implementations demonstrated productivity improvements of approximately 28%, reductions in order processing times exceeding 22%, and labor cost savings of nearly 20% compared with conventional warehouse operations. Additionally, subscription-based robotics models enabled faster automation deployment and reduced upfront investment requirements.

Recent Developments:

-

2026: ABB Robotics expanded its cloud-connected robotics portfolio by introducing enhanced subscription-based robotic automation packages integrating AI-powered predictive maintenance, remote fleet monitoring, and performance analytics. The new offering enables manufacturers and logistics operators to optimize robot utilization rates, reduce unplanned downtime, and accelerate automation deployment without significant upfront capital investments.

-

2026: KUKA strengthened its Robotics-as-a-Service capabilities through the expansion of its cloud-enabled robotic fleet management platform, allowing customers to remotely manage, monitor, and optimize multiple industrial robots across distributed production facilities. The solution supports flexible automation scaling and real-time operational performance tracking for smart manufacturing environments.

-

2025: FANUC launched an upgraded robotic automation service model featuring advanced condition monitoring and predictive maintenance capabilities powered by machine learning algorithms. The platform enables customers to improve robot uptime, minimize maintenance costs, and enhance production efficiency through proactive equipment health management and remote diagnostics.

-

2025: Yaskawa Electric expanded its collaborative robot (cobot) service offerings by introducing flexible subscription-based deployment programs for small and medium-sized manufacturers. The initiative provides access to robotic welding, assembly, and material handling solutions with integrated software support, training services, and lifecycle maintenance under a recurring service model.

Robotics as a Service Market Key Players are:

-

ABB

-

KUKA

-

Fanuc

-

Yaskawa Electric

-

Omron Corporation

-

Siemens

-

Boston Dynamics

-

Amazon Robotics

-

Locus Robotics

-

Geek+

-

Fetch Robotics

-

Zebra Technologies

-

Teradyne (Universal Robots)

-

Kawasaki Robotics

-

Mitsubishi Electric

-

Honeywell

-

Dematic

-

AutoStore

-

GreyOrange

-

Swisslog

Robotics as a Service Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.52 Billion |

| Market Size by 2035 | USD 15.88 Billion |

| CAGR | CAGR of 20.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Industrial Robotics, Service Robotics, Collaborative Robots (Cobots), Autonomous Mobile Robots (AMRs), Others), • By Application (Material Handling, Welding & Soldering, Dispensing & Coating, Packaging & Sorting, Inspection & Quality Control, Processing, Others), • By Deployment Type (Cloud-based Robotics Platforms, On-premises Robotics Systems, Hybrid), • By End-User Industry (Manufacturing, Automotive, Logistics & Warehousing, E-commerce Fulfillment, Healthcare & Pharmaceuticals, Food & Beverage, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB, KUKA, Fanuc, Yaskawa Electric, Omron Corporation, Siemens, Boston Dynamics, Amazon Robotics, Locus Robotics, Geek+, Fetch Robotics, Zebra Technologies, Teradyne (Universal Robots), Kawasaki Robotics, Mitsubishi Electric, Honeywell, Dematic, AutoStore, GreyOrange,D24 Swisslog. |

Frequently Asked Questions

The Robotics as a Service market is expected to grow at a CAGR of 20.37% from 2026 to 2035.

The Robotics as a Service market was valued at USD 2.52 Billion in 2025.

The primary growth factors include the increasing demand for flexible and cost-effective automation solutions, rising labor shortages across manufacturing and logistics industries, and growing adoption of subscription-based robotics models.

The material handling segment dominated the Robotics as a Service market with 27.69% share in 2025.

North America dominated the Robotics as a Service market in 2025, holding approximately 39.47% of global revenues.

Get in Touch