Software Defined Data Center Market Report Scope and Overview:

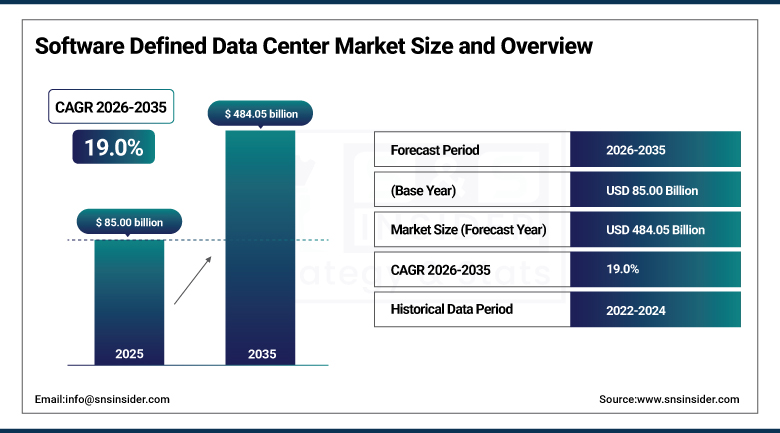

The Software Defined Data Center Market was valued at USD 85.00 Billion in 2025 and is projected to reach USD 484.05 Billion by 2035, registering a CAGR of 19.0% from 2026 to 2035.

The growth of the Software Defined Data Center Market is driven by rising requirement for scalable, automated, and virtualized infrastructure solutions within enterprises. The adoption of software-defined technologies is leading to better utilization of resources, lower costs of operations, and increased flexibility of workloads in cloud and hybrid environments. Investment in digital transformation, edge computing, AI, and data-intensive applications is further aiding the market growth. Apart from that, the rising demand for infrastructure management, enhanced cybersecurity measures, and rapid application deployments is another major factor boosting the adoption rates. Modernization of legacy data centers in order to improve efficiencies and business continuity is also contributing to this growth trend.

According to a Computer World white paper, up to 13% of servers acquired over the coming years would be used to handle machine learning, predictive analytics, and artificial intelligence in software-defined data centers, reflecting the genuinely accelerating convergence between AI workload demands and the flexible, automated infrastructure that software-defined data center architecture is specifically designed to deliver.

Market Size and Forecast

-

Market Size in 2026E: USD 101.15 Billion

-

Market Size by 2035: USD 484.05 Billion

-

CAGR: 19.0% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America (40% share in 2025)

To Get more information Software Defined Data Center Market - Request Free Sample Report

Software Defined Data Center Market Trends

-

Orchestration engines and policy-based controllers continue expanding rapidly, underlining enterprise appetite for hands-free provisioning.

-

Early adopters continue recording sub-12-month paybacks on workflow automation and drift remediation investment.

-

Security plug-ins, AI observability modules, and developer tool chains continue widening the addressable base as ecosystems mature.

-

Providers continue bundling migration playbooks, reference architectures, and consumption-based billing to ease entry for heavily regulated verticals.

-

The ability to significantly reduce hardware costs continues augmenting SDDC adoption across organizations of every size.

U.S. Software Defined Data Center Market Outlook

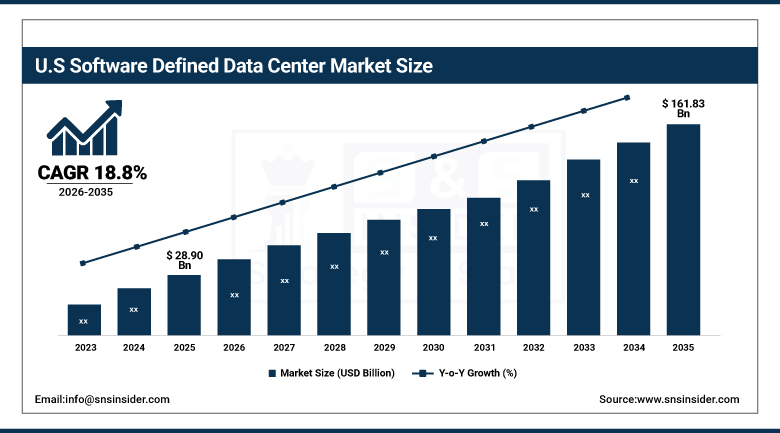

The U.S. Software Defined Data Center Market was valued at approximately USD 28.90 Billion in 2025 and is projected to reach approximately USD 161.83 Billion by 2035, registering a CAGR of approximately 18.8% from 2026 to 2035.

The U.S. Software Defined Data Center Market maintained a significant advantage owing to its developed digital infrastructure, a high level of use of cloud computing, and strong development of technology companies and innovative startups. The country remained a leader in this sector due to its established industry players and the timely adoption of data automation and cloud computing technologies. Enterprises’ increasing awareness of the benefits of using AI-based analytics for managing resources, predicting failures, and running the company autonomously has been driving the demand on the domestic market. Enterprises strive to achieve workload balancing in hybrid or multi-cloud systems in real time, which leads to reduced downtime and costs at the largest data centers in the country.

VMware continued expanding its software-defined data center virtualization and cloud management platform throughout 2025, targeting American enterprise customers seeking comprehensive infrastructure automation capability spanning software-defined networking, storage, and compute across hybrid and multi-cloud environments.

Software Defined Data Center Market Segment Analysis

-

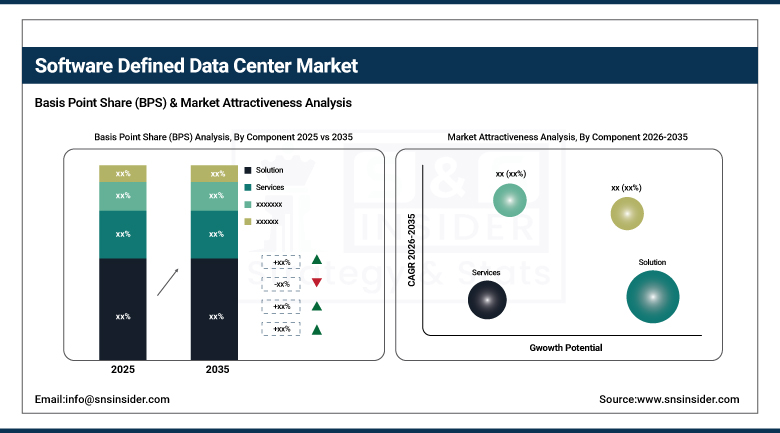

By Component, Solution segment dominated the Software Defined Data Center Market in 2025 with 69% share; Services segment is the fastest growing segment.

-

By Type, Software Defined Compute segment dominated the market in 2025 with 39% share; Software Defined Networking segment is the fastest growing segment.

-

By Deployment, Public segment dominated the market in 2025 with 45% share; Hybrid segment is the fastest growing segment.

-

By Industry, IT & Telecom segment dominated the market in 2025 with 28% share; Healthcare segment is the fastest growing segment.

By Component, Solutions Dominate the Software Defined Data Center Market While Services Register the Fastest Growth

The Solution segment dominated the Software Defined Data Center Market in 2025 due to increasing demand for comprehensive software systems which will help in virtualizing computing, storage, and network resources. Companies have started opting for software-defined data centers in order to make their infrastructure flexible and efficient for resource management. The adoption of these software solutions will help in centralizing the control of workloads. Increasing investments in virtualization technologies and digital transformation projects are boosting the growth of software-defined data center solutions.

The Services segment is the fastest growing segment due to increased demand for consulting, implementation, integration, and managed services to implement software-defined data centers. Companies need specific skills and competencies to move away from existing infrastructure, optimize the performance of systems, and integrate various technologies. Service providers not only provide help in deploying software-defined data center but also in maintenance, security, and management of technology. Increasing complexity of modern data center environment and adoption of virtualization technologies are boosting the demand for services.

By Type, Software Defined Compute Dominates the Market While Software Defined Networking Emerges as the Fastest-Growing Segment

The Software Defined Compute segment dominated the Software Defined Data Center Market in 2025 owing to the prevalent use of server virtualization and resource allocation software. Organizations require software-defined compute solutions for better management of hardware, better workload management, and better efficiency in operations. The software enables flexible provisioning, centralized management, and scalability within the data centers. High demand for computing resources and virtualization solutions drives the use of software-defined computing solutions.

The Software Defined Networking segment is the fastest growing segment because of the rising demand for programmable networks, centralization of management, and increased traffic optimization capabilities. Software-defined networking helps organizations to achieve network agility, better security, and centralized management of the network infrastructure. The rising demand for cloud computing, virtualization, and hybrid IT is leading to implementation of software-defined networking solutions. Increasingly, organizations are using software-defined networking for dynamic workloads and improved network performance.

By Deployment, Public Deployment Dominates the Software Defined Data Center Market While Hybrid Deployment Witnesses the Fastest Growth

The Public segment dominated the Software Defined Data Center Market in 2025 owing to its cost effectiveness, scalability, and capacity to manage ever-increasing digital workloads. Businesses are opting for public deployment as it helps them lower infrastructure costs while offering computing, storage, and networking capabilities. The benefits of using public deployment include easy provision of resources, business continuity, and fast application deployment. Growth in the adoption of cloud services and the need for agile IT infrastructure will continue to drive the dominance of public deployment.

The Hybrid segment is the fastest growing segment because of increasing demands for flexible infrastructure that combines both public and private infrastructure. The adoption of hybrid deployment allows organizations to maintain a balance between security, compliance, workload balancing, and efficient operations. In addition, it makes possible for seamless movement of applications and data along with business continuity and scalability. The increasing trend towards digital transformations, growing cloud deployments, and need for flexibility in infrastructure have been contributing to the fast growth of hybrid deployments.

By Industry, IT & Telecom Dominates the Software Defined Data Center Market While Healthcare Records the Fastest Growth

The IT & Telecom segment dominated the Software Defined Data Center Market in 2025 owing to regular investments made in cloud computing, virtualization, and high-performance network systems. The enterprises belonging to the industry need scalable and automated data center technology due to increased digital services, massive data processing, and network management. Software-defined infrastructure leads to efficient usage of resources, operational performance, and service delivery. Increased demands for advanced connections and digital services keep on fueling the adoption of software-defined data centers in IT and telecom industries.

The Healthcare segment is the fastest growing segment due to increased digitalization in the healthcare sector, increased use of electronic health records, and increased data security needs. The software-defined data center solutions help the healthcare enterprises to increase infrastructure scalability and cyber security, as well as advance healthcare applications. Increased use of telemedicine, medical imaging, artificial intelligence, and other advanced healthcare technology helps accelerate infrastructure modernization.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.05% |

|

Europe |

Germany |

24.10% |

|

Asia Pacific |

China |

31.40% |

|

Middle East and Africa |

UAE |

26.70% |

|

Latin America |

Brazil |

34.05% |

North America Software Defined Data Center Market Insights

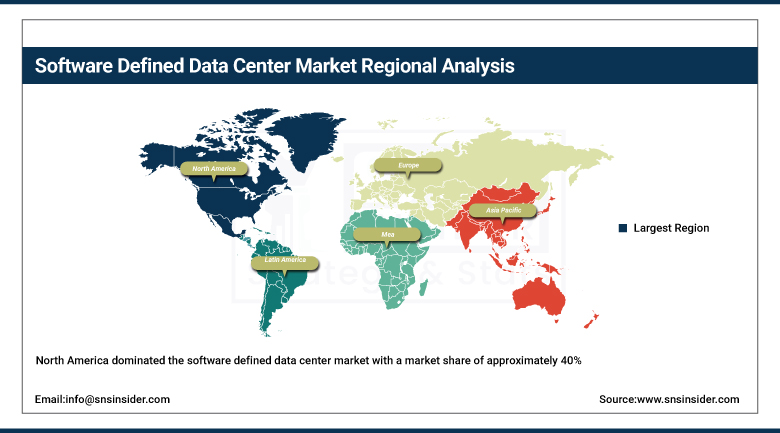

North America dominated the software defined data center market with a market share of approximately 40%, due to the presence of major players and the early adoption of data automation and cloud computing technologies. That combination of established technology industry concentration and mature enterprise cloud infrastructure kept the continent firmly positioned as the market's clear leader by a considerable margin over every other region tracked in this report.

The United States accounted for roughly 82.05% of regional revenue, anchored by the presence of major industry players and early adoption of data automation and cloud computing technologies. Canada added further regional demand through its own growing enterprise cloud infrastructure sector, and that combined strength kept North America the largest addressable market for software defined data center vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Software Defined Data Center Market Insights

Europe held a meaningful share of global revenue, supported by strong enterprise digital transformation investment and continued adoption of hybrid IT infrastructure across the region's major economies. Growing emphasis on centralized management and improved resource utilization kept reinforcing steady European demand throughout the year.

Germany led demand at roughly 24.10% of European revenue, supported by its substantial enterprise data center and industrial technology infrastructure. The UK and France contributed substantial additional demand, and continued European investment in cloud-first infrastructure strategies should keep regional demand climbing through the forecast period.

Asia Pacific Software Defined Data Center Market Insights

The Asia Pacific market is projected to register a substantial CAGR during the forecast period, driven by rising investments from end users across various industries, particularly in cloud services, IT infrastructure, and data center modernization. That combination of expanding enterprise cloud adoption and government-backed digital infrastructure investment kept the region's growth trajectory well ahead of every other region tracked in this report.

China led the pack, supported by its massive enterprise technology sector and rapidly growing domestic cloud computing and data center modernization investment. India is expected to experience a substantial CAGR during the forecast period, attributed to surging investments in technology adoption, and together with Japan continued contributing meaningful additional demand that reinforced Asia Pacific's position as the fastest-growing market tracked in this report.

MEA and Latin America Software Defined Data Center Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding enterprise cloud computing investment, growing data center modernization activity, and rising government focus on digital infrastructure development across both areas. As these markets continued developing modern enterprise IT infrastructure, software defined data center adoption grew correspondingly from a considerably smaller base than in more mature markets.

The UAE led Middle East and Africa demand, supported by substantial cloud computing and data center investment tied to the region's continued digital transformation agenda. Saudi Arabia contributed further demand through its own digital infrastructure development programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing enterprise cloud adoption continuing to anchor regional demand for software defined data center solutions.

Market Dynamics

Growth Drivers: Cloud-First Infrastructure Strategy and Hardware Cost Reduction

The market growth is largely fueled by the increasing adoption of cloud computing, virtualization, and hybrid IT infrastructures across enterprises, leading to higher demand for flexible, scalable, and automated data center operations. The ability to significantly reduce hardware costs continues augmenting SDDC adoption across organizations, as businesses increasingly seek to eliminate the need to purchase dedicated hardware and acquire vendor-specific skills to manage physical infrastructure changes.

Rising enterprise requirements for centralized management, improved resource utilization, and enhanced security continue establishing software-defined data center solutions as the preferred choice for modern IT infrastructure. That combination of genuine cost efficiency and expanding automation capability is exactly what keeps demand climbing at such a rapid, sustained pace across virtually every major enterprise category this market serves.

Restraints: Legacy Infrastructure Migration Complexity and Skills Gap

Firms may underestimate the challenges of employing obsolete platforms and maintaining new IT infrastructure, posing a genuine restraint on faster market-wide migration from legacy data center architectures. That underestimation risk keeps some enterprises encountering unexpected implementation costs and timeline extensions during their software-defined infrastructure transition.

The genuine technical skills gap required to properly design, deploy, and operate sophisticated software-defined data center architecture continues posing a further restraint, as organizations often lack in-house expertise across networking, storage, and compute virtualization simultaneously. That skills shortage keeps professional services demand consistently strong even as core software licensing costs continue trending toward greater accessibility.

Opportunities: AI Workload Integration and Edge Computing Expansion

The genuinely accelerating convergence between AI workload demands and flexible, automated infrastructure represents a significant opportunity, as up to 13% of servers acquired over coming years are expected to handle machine learning, predictive analytics, and artificial intelligence in software-defined data centers. Vendors offering genuinely proven, AI-optimized SDDC infrastructure stand to capture meaningful share as this workload category continues expanding across enterprise data center deployments.

Hyperscaler build-outs and colocation and edge operator expansion offer a second substantial opportunity, as rapid algorithmic workloads continue prompting record capital spending that spills over well beyond traditional centralized data center deployment. Vendors positioned to serve this expanding edge and colocation infrastructure category stand to capture meaningful share as software-defined architecture continues extending beyond its traditional core data center stronghold.

Recent Developments:

-

2025: Cisco Systems continued expanding its software-defined networking and data center automation portfolio, targeting enterprise customers seeking integrated network virtualization and policy-based orchestration capability.

-

2025: Nutanix continued advancing its hyperconverged infrastructure and software-defined storage platform, targeting enterprises seeking simplified, scalable data center virtualization capability across hybrid cloud environments.

-

2024: Dell Technologies continued expanding its software-defined data center hardware and integration portfolio, targeting large enterprises seeking comprehensive infrastructure automation capability spanning compute, storage, and networking.

Software Defined Data Center Market key players are:

-

Fujitsu

-

IBM

-

Microsoft

-

Commvault

-

Dell Technologies

-

Oracle

-

Nutanix

-

Cisco

-

Citrix

-

Huawei

-

VMware

-

Juniper Networks

-

Arista Networks

-

DataCore Software

-

Scality

-

Hewlett Packard Enterprise (HPE)

-

SUSE

-

DriveNets

-

Lightbits

-

NetApp

Software Defined Data Center Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 85.00 Billion |

| Market Size by 2035 | USD 484.05 Billion |

| CAGR | CAGR of 19.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Services) • By Type (Software Defined Compute, Software Defined Networking, Software Defined Storage, Others) • By Deployment (Public, Private, Hybrid) • By Industry (IT & Telecom, BFSI, Government, Healthcare, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | VMware (Broadcom Inc.), Microsoft Corporation, IBM Corporation, Cisco Systems, Inc., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), Nutanix, Inc., Oracle Corporation, Red Hat, Inc. (IBM), Fujitsu Limited, Huawei Technologies Co., Ltd., NetApp, Inc., Juniper Networks, Inc., Arista Networks, Inc., SUSE S.A., DataCore Software, Scality, Citrix Systems, Commvault Systems, Inc., DriveNets Ltd. |

Frequently Asked Questions

The Software Defined Data Center Market is expected to grow at a CAGR of approximately 19.0% from 2026 to 2035, based on triangulated secondary research estimates.

The Software Defined Data Center Market was valued at approximately USD 85.00 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is increasing adoption of cloud computing, virtualization, and hybrid IT infrastructures across enterprises seeking flexible, scalable, and automated data center operations.

The Software component segment dominated the Software Defined Data Center Market, reflecting its core role in enabling automation, virtualization, and orchestration in 2025.

North America dominated the Software Defined Data Center Market in 2025, holding an estimated 40% share of total global market revenue.

Get in Touch