Rum Market Report Scope & Overview:

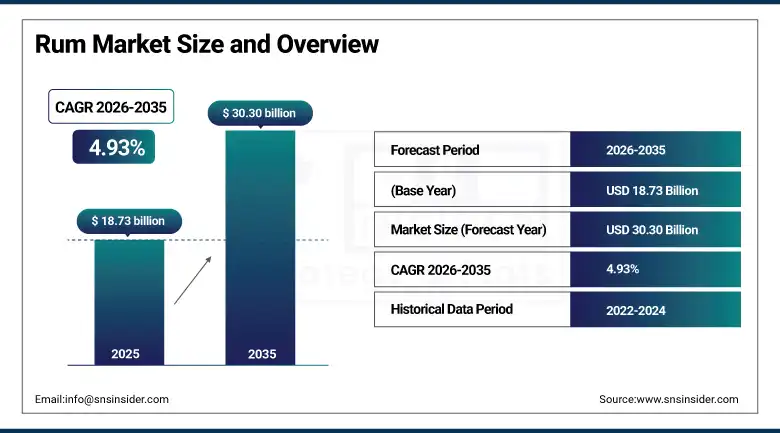

The Rum Market was valued at USD 18.73 Billion in 2025 and is expected to reach USD 30.30 Billion by 2035, growing at a CAGR of 4.93% from 2026–2035.

The rum category represents one of the largest spirits categories globally. It is derived from sugarcane juices or molasses through fermentation and distillation processes. Geographically, rum has its origins in the Caribbean, Latin American and Indian subcontinents, although it is currently manufactured across all inhabited continents of the world. In 2025, production levels for rum exceeded 45 million cases because of the growth in premium rums, cocktail use, and increased consumption through the bar, restaurant, and retail distribution channels. The diverse range of rums within this category – which extends from light and dry rum from Cuba and Puerto Rica to aged dark rums from Jamaica and Barbados and the flavored and spiced rums that propelled mainstream acceptance – ensures that rum is both a commercial success and an industry favorite.

The rum market is experiencing a premiumization wave that is reshaping the commercial and competitive landscape. Standard mass-market rum is growing slowly in developed markets while the super-premium aged rum segment is growing at above-category rates as whisky drinkers who have explored aged spirit complexity are discovering rum's equally sophisticated ageing possibilities at more accessible price points. The cocktail renaissance, driven by craft bartender culture and consumer interest in authentic ingredient provenance, is elevating demand for aged rums with documented origin stories and distillation heritage. India is the world's largest rum-consuming country by volume, sustaining commercial scale for domestic producers and providing a growth platform for premium import brands.

Rum production stood at 45 million cases in 2025. In fact, India constitutes more than 40% of the worldwide consumption of rum, and Old Monk, McDowell’s No.1, and Royal Stag Barrel Select are the major players of the mass market segment, while premium brands are trying to enter into the same.

Market Size and Forecast

-

Market Size in 2026E: USD 19.65 Billion

-

Market Size by 2035: USD 30.30 Billion

-

CAGR: 4.93% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Rum Market - Request Free Sample Report

Rum Market Trends

-

Premium and craft rum premiumization is accelerating as whisky-experienced drinkers discover aged rum's comparable complexity at lower price points, driving trade-up from standard to aged and single estate expressions across North American and European markets.

-

Flavored and spiced rum adoption among younger consumers is sustaining mainstream volume growth as pineapple, coconut, mango, and spice-infused variants expand the rum category's appeal to consumers who find standard rum's agricultural character too assertive.

-

Ready-to-drink rum cocktails including pre-mixed daiquiris, rum and cola, and mojito formats are growing rapidly in off-trade retail as the RTD premium spirits category expands and consumers seek convenient at-home versions of cocktails they encounter in bars and restaurants.

-

Caribbean rum tourism is creating direct-to-consumer experiences at distilleries in Barbados, Jamaica, Trinidad, and Puerto Rico that build brand stories and premium market positioning for export rum brands through experiential visitor education and limited-edition release programmes.

-

E-commerce rum sales are growing through specialist spirits retailers, direct distillery webstores, and premium subscription delivery services that provide access to limited edition and craft rum expressions unavailable in mainstream retail channels.

The U.S. Rum Market Outlook

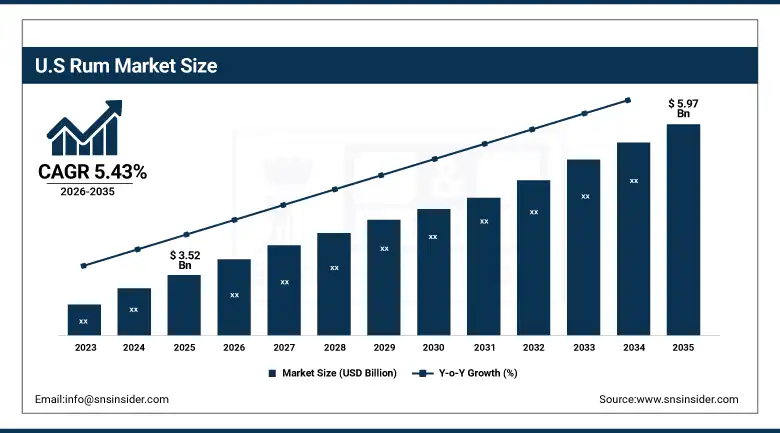

The U.S. Rum Market was valued at approximately USD 3.52 Billion in 2025 and is expected to reach approximately USD 5.97 Billion by 2035, growing at a CAGR of 5.43%.

The United States is the world's largest premium rum import market by value and the most commercially important international market for Caribbean and Latin American rum producers. Bacardi, Havana Club International, Appleton Estate, and Captain Morgan collectively dominate the U.S. mainstream rum market, while a growing constellation of craft and artisan rum producers including Plantation, Diplomático, and El Dorado are building premium segment positions through specialist spirits retail and cocktail bar placements. Rum-based cocktails including the Mojito, Daiquiri, Dark 'n' Stormy, and Rum Old Fashioned are among the most ordered cocktails at U.S. bars and restaurants, generating consistent on-trade demand across the full quality spectrum from well rum through aged premium expressions.

The U.S. market is bifurcating between volume decline in standard price-tier rum and strong value and volume growth in the premium and super-premium segments. This mirrors the pattern established in whisky a decade earlier, where total volume stabilized while value grew significantly through premiumization. North American consumers who have developed appreciation for single malt Scotch and bourbon aged expressions are demonstrating comparable interest in aged pot still Jamaican rum and vintage-dated Caribbean expressions. The DISCUS reported consistent growth in premium rum imports to the U.S. through 2024 and 2025 as craft spirits retailers expanded their rum selections to meet growing consumer demand.

The Distilled Spirits Council of the United States reported that rum-based cocktails including Mojitos, Daiquiris, and Dark 'n' Stormy hold consistently strong positions among the most-ordered cocktails at U.S. bars. This on-trade cocktail demand directly supports retail rum sales as consumers seek to recreate bar-quality cocktails at home.

Rum Market Segment Analysis

-

By Type, dark rum dominated with approximately 38.72% share in 2025 through strong consumer preference for its rich, complex flavor profile in cocktails and sipping occasions; flavored rum is the fastest-growing type at a CAGR of 6.14%, driven by flavor variety, cocktail versatility, and appeal to younger consumer demographics.

-

By Distribution Channel, off-trade held the largest share of approximately 49.58% in 2025 through retail convenience, value purchasing, and at-home cocktail preparation growth; e-commerce is the fastest-growing channel at a CAGR of 7.11% through specialist spirits retailers and direct distillery sales of premium and limited-edition expressions.

-

By End-Use, bars and restaurants hold a significant portion of rum revenues through cocktail culture driving consistent on-trade premium rum consumption; retail consumer is growing as at-home cocktail preparation and premium spirit collection expand beyond the hospitality channel.

-

By Category, standard rum dominates total volume through mass-market domestic consumption in India, the Philippines, and Latin America; premium and super-premium rum is the fastest-growing category through aged and craft expressions attracting consumers trading up from standard tier products.

By Type, dark rum dominates, flavored rum grows fastest

The dark rum accounted for 38.72% of the rum market by 2025. This market dominance can be attributed to the long history of the dark rum consumers as well as the crucial role it plays in the story of premium ageing, which is responsible for the transformation of rum into an increasingly commercially-oriented beverage. Dark rum ranges in terms of quality and price from the Caribbean mass-produced blends to the aged varieties produced at a single estate that rival aged whiskeys as connoisseurs' products. The complexity of taste, resulting from the prolonged ageing process and such characteristics as vanilla, caramel, tobacco, and dried fruit notes is favored by consumers who are more concerned with sipping the drink rather than mixing it with other beverages. There are three distinct styles of dark rum: Jamaican pot distillate, Barbadian column distillation, and the rhum agricole of Martinique.

Flavored rum is the fastest-growing type at a CAGR of 6.14% through 2035. Its growth is driven by the category's exceptional versatility and accessibility for consumers who are new to rum or who find traditional rum's agricultural character challenging. Pineapple, coconut, mango, passion fruit, and spiced variants each address specific cocktail occasions and consumer taste preferences that standard rum cannot serve as directly. Bacardi's Limon and Coconut expressions, Captain Morgan's Original Spiced, and Malibu's coconut rum have built the commercial template that hundreds of smaller brands are following with increasingly innovative flavor extensions. The ready-to-drink cocktail opportunity has further expanded the commercial relevance of flavored rum as RTD daiquiri and tropical cocktail products increasingly use flavored rum as their base spirit.

By Distribution Channel, off-trade dominates, e-commerce grows fastest

The share of revenue of distribution from the off-trade retail accounted for about 49.58% in the year 2025. In this channel, there are included such types as liquor stores, supermarkets, hypermarkets, convenience stores, and specialty alcohol shops which offer consumers access to rum at all levels of product availability. The off-trade channel is significant because of its commercial value, which is related to the level of consumption by the consumer at home and the ability of the retail shop to place the product on the shelves in order to increase sales. Specialization in specialty alcohol shops is beneficial for premium rum brands because staff education in this type of retail is helpful for consumer education regarding the product quality level.

E-commerce is the fastest-growing distribution channel at a CAGR of 7.11% through 2035. The digital channel's growth reflects several reinforcing trends. Specialist online spirits retailers including Master of Malt, The Whisky Exchange, and Caskers carry a breadth of rum expression that no physical retailer can match in shelf space terms. Direct distillery webstores allow Caribbean and Latin American producers to sell limited edition, vintage-dated, and exclusive expressions directly to international collectors without relying on traditional three-tier distribution infrastructure. Subscription delivery services for premium spirits introduce consumers to new rum expressions on a regular cadence that builds category knowledge and premium segment engagement over time.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.4% |

|

Europe |

United Kingdom |

28.7% |

|

Asia Pacific |

India |

43.8% |

|

Middle East & Africa |

South Africa |

28.3% |

|

Latin America |

Brazil |

38.4% |

North America Rum Market Insights

North America is the fastest-growing regional rum market with a CAGR of 5.82% through 2035. The United States accounts for approximately 82.4% of North American revenues as the most commercially significant premium rum import market globally. North American premiumization is the defining commercial trend in regional rum consumption. Consumers who developed premium spirit appreciation through craft whisky and bourbon exploration are bringing that quality-seeking behavior to the rum category. U.S. cocktail culture, sustained by a dense and innovative bartender community, continuously generates new rum consumption occasions through seasonal cocktail menus, heritage cocktail revivals, and creative original cocktail development.

Europe Rum Market Insights

Europe is a large and commercially sophisticated rum market with deep historical connections to Caribbean production through colonial trade relationships. The United Kingdom accounts for approximately 28.7% of European revenues as a major rum consumer market with strong Jamaican and Barbadian rum heritage and an active premium spirits specialist retail sector. Germany, Spain, Italy, and Scandinavia are each significant national rum markets. Spain's Canary Islands maintain their own rum production tradition. Germany has a particularly active specialist rum collector and enthusiast community that drives demand for high-end, vintage-dated Caribbean expressions.

Asia Pacific Rum Market Insights

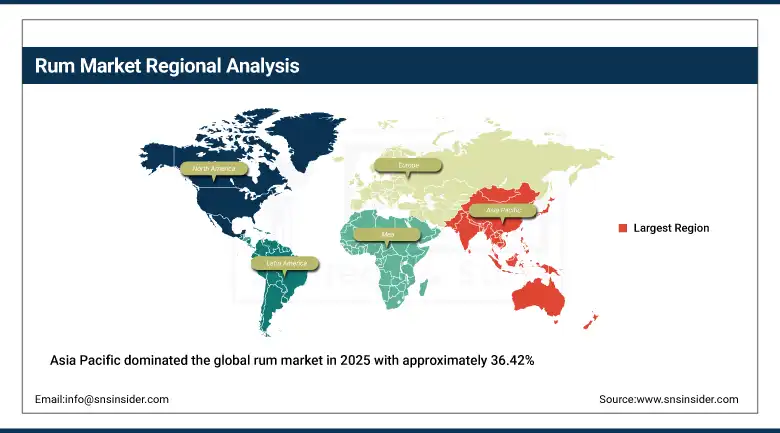

Asia Pacific dominated the global rum market in 2025 with approximately 36.42% of revenues. India accounts for approximately 43.8% of Asia Pacific revenues and is the world's single largest rum-consuming country by volume. Indian rum consumption is dominated by domestic producers operating large-scale distilleries producing mass-market expressions including Old Monk, McDowell's No.1, and Royal Challenge. These brands generate extraordinary volume from India's young, large, and increasingly urban consuming population. The Philippines is the world's second-largest rum-consuming country through Tanduay, the world's best-selling rum brand by volume globally. Australia and Japan represent sophisticated premium import rum markets with growing craft spirit appreciation communities.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Rum Market Insights

The Middle East, Africa, and Latin America are important rum markets with different commercial characteristics. South Africa leads MEA revenues at approximately 28.3% of the regional share through its substantial spirits-consuming population and well-developed modern trade retail infrastructure. The Caribbean and Latin America are the world's rum heartland, producing the majority of global supply. Brazil leads Latin American consumer revenues at approximately 38.4% through its large domestic spirit’s market. However, the Caribbean islands including Jamaica, Barbados, Trinidad, Cuba, and Puerto Rico are commercially significant as production centers and brand origin markets whose geographic designations carry premium commercial value in international markets.

Market Dynamics

Growth Drivers: Rising cocktail culture, premium rum premiumization, and India's large-volume domestic market are the primary drivers of rum market growth.

Cocktail culture is a structural growth driver for rum that operates independently of overall alcohol volume trends. Bars and restaurants consistently list rum-based cocktails among their highest-margin and most popular menu items. The Mojito remains one of the world's most ordered cocktails globally. The Dark 'n' Stormy, Daiquiri, Rum Old Fashioned, and Jungle Bird are each building consumer followings through bartender advocacy and social media recipe content. Each drink occasion that features rum builds consumer familiarity with the category and drives subsequent retail purchase for home recreation of the bar experience.

Premiumization is creating above-average revenue growth within a category whose overall volume growth is moderate. Consumers who are drinking less overall are spending more per occasion on higher-quality spirits. Aged rum positioned at premium price points is attracting consumers from aged whisky who have discovered that the rum category offers comparable complexity and craftsmanship at price points often 20 to 40% below comparable aged whisky expressions. This whisky-to-rum consumer migration is the most commercially significant trade-up trend in the spirits category and directly supports premium rum value growth that outpaces volume growth.

Restraints: Health-driven alcohol reduction trends, regulatory restrictions on advertising in key markets, and competition from whisky and tequila for premium spirits spending are restraining rum market growth.

The practice of alcohol moderation by the younger generation in developed countries is resulting in pressure on volumes in all spirit types, including rum. The non-alcoholic movement has gained popularity quickly in North America, Europe, and Australia, where consumers are drinking less frequently. The development of alcohol-free rum options such as Lyre's Dark Cane Spirit, as well as other low-alcohol rum variants, can be seen as a result of this trend.

Premium spirit competition in terms of tequila and whisky becomes an obstacle towards achieving premiumization in rum. The success of premium tequilas as a spirits category story is evident as they have been the most commercially viable spirits category story within the last ten years thanks to endorsement, limited supply, and consumers' eagerness to purchase them at ultra-premium prices. Whisky's advantage within premium spirit consumption settings is attributed to its background and investment value compared to rum. Rum's premiumization path requires more sustained category education investment than categories that benefit from entrenched consumer quality perception.

Opportunities: Aged rum collector market development, RTD premium rum cocktail expansion, and India's premium import segment growth.

The aged rum collector market is at an early stage of development relative to the mature aged whisky collector market. Vintage-dated Caribbean rum expressions from closed distilleries including Port Mourant, Caroni, and Uitvlugt are already commanding extraordinary prices at specialist auctions. Living distilleries including Hampden Estate, Foursquare, and Barbancourt are building collector followings through limited annual releases, distillery exclusives, and independent bottler bottlings that create excitement and investment motivation comparable to the limited-edition bourbon and single malt markets. The infrastructure for rum collecting, including specialist retailers, auction houses, and online communities, is expanding rapidly.

The premium RTD rum cocktail opportunity is substantial and largely underdeveloped. The RTD category's fastest commercial success has been in vodka soda and hard seltzer formats that do not feature rum prominently. Premium RTD rum cocktails including pre-mixed Mojitos, Daiquiris, and aged rum Old Fashioneds made with quality base spirits represent a natural extension that few brands have executed with the ingredient quality and packaging presentation that the premium RTD consumer expects. Brands that invest in RTD rum cocktail quality using genuine aged rum expressions as the base spirit can capture premium pricing that positions them distinctively from the mass-market RTD sector.

Recent Developments:

-

2025: Bacardi launched a new ultra-premium aged rum expression under its Bacardi Reserve Ocho Eight-Year-Old range with expanded distribution into key European and North American premium spirits retail channels.

-

2025: Diplomatico Rum from Venezuela reported continued double-digit growth in U.S. premium retail, with its Reserva Exclusiva expression establishing one of the strongest consumer loyalty profiles of any premium rum brand in the specialist spirit’s sector.

-

2025: Khukri Rum from Nepal's MCKT Beverages entered the Indian market with its three premium expressions including Khukri XXX Rum, Khukri Spiced Rum, and Khukri White Rum, targeting the growing premium import segment in India's large domestic rum market.

-

2025: Appleton Estate launched its 21-year-old Nassau Valley Casks expression as a limited release aimed at the growing ultra-premium Jamaican rum collector segment, priced to compete with premium aged whiskies and positioning Appleton as a luxury spirits brand.

Rum Market Key Players are:

-

Bacardi Limited

-

Diageo plc

-

Pernod Ricard SA

-

Beam Suntory

-

William Grant & Sons

-

Tanduay Distillers Inc.

-

United Spirits

-

Radico Khaitan Ltd.

-

Demerara Distillers Ltd.

-

Foursquare Rum Distillery

-

Hampden Estate Distillery

-

Diplomatico

-

Ron Barcelo

-

Appleton Estate

-

Plantation Rum

-

Brugal & Co.

-

Havana Club International SA

-

Mount Gay Distilleries

-

Santa Teresa

-

Angostura Holdings Ltd.a

Rum Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.73 Billion |

| Market Size by 2035 | USD 30.30 Billion |

| CAGR | CAGR of 4.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Dark Rum, Light/White Rum, Flavored Rum, Spiced Rum, Others) • By Distribution Channel (Off-Trade, On-Trade, E-Commerce) • By End-Use (Bars & Restaurants, Retail Consumers, Hotels & Clubs, Others) • By Category (Premium & Super-Premium, Standard, Economy) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Bacardi Limited, Diageo plc, Pernod Ricard SA, Beam Suntory, William Grant & Sons, Tanduay Distillers Inc., United Spirits, Radico Khaitan Ltd., Demerara Distillers Ltd., Foursquare Rum Distillery, Hampden Estate Distillery, Diplomatico, Ron Barcelo, Appleton Estate, Plantation Rum, Brugal & Co., Havana Club International SA, Mount Gay Distilleries, Santa Teresa, Angostura Holdings Ltd. |

Frequently Asked Questions

Asia Pacific dominated the rum market in 2025, holding approximately 36.42% of global revenues.

Dark Rum dominated with approximately 38.72% of revenues in 2025.

Rising cocktail culture and premium rum premiumization are the primary growth drivers.

The rum market was valued at USD 18.73 Billion in 2025.

The rum market is expected to grow at a CAGR of 4.93% from 2026 to 2035.

Get in Touch