Fermented Food and Beverage Market Report Scope & Overview:

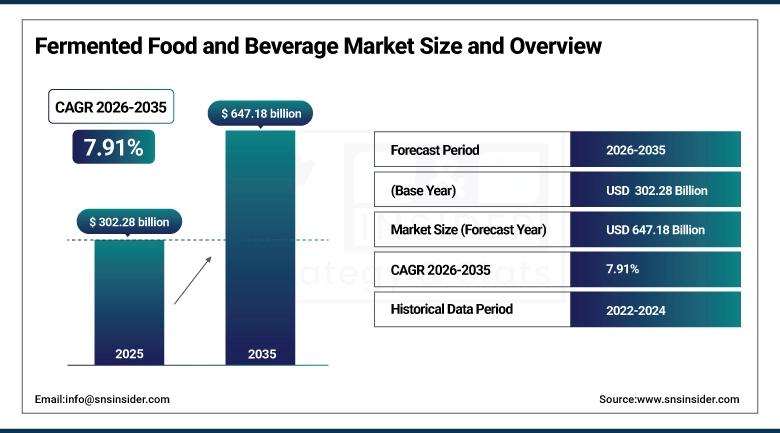

The Fermented Food and Beverage Market size was estimated at USD 302.28 Billion in 2025 and is expected to reach USD 647.18 Billion by 2035 and grow at a CAGR of 7.91% over the forecast period of 2026-2035.

The Fermented Food and Beverage Market is growing due to increasing consumer awareness of gut health, probiotics, and functional foods. Rising demand for dairy-free, plant-based, and natural fermented products is driving innovation and adoption. Additionally, expanding e-commerce channels, growing urban populations, and a shift toward convenient, ready-to-eat, and health-focused foods are fueling market growth. Advancements in fermentation technology and rising interest in traditional and artisanal products further support the market’s expansion globally.

Global consumer surveys indicate that over 65% now associate fermented foods with digestive wellness, and more than half actively seek out products labeled as natural, probiotic-rich, or traditionally fermented.

Market Size and Forecast

-

Market Size in 2025: USD 302.28 Billion

-

Market Size by 2035: USD 647.18 Billion

-

CAGR: 7.91% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Fermented Food and Beverage Market - Request Free Sample Report

Fermented Food and Beverage Market Trends

-

Rising consumer preference for gut-health products drives demand for probiotic-rich fermented foods globally

-

Increasing awareness of natural preservation methods fuels growth of traditionally fermented beverages and foods

-

Expansion of online retail channels accelerates accessibility and consumption of fermented food and beverage products

-

Innovation in flavors and functional ingredients enhances appeal of fermented products among younger consumers

-

Growing demand for plant-based and dairy-free fermented alternatives supports market diversification and product development

-

Rising adoption of fermented foods in culinary applications boosts restaurant and ready-to-eat meal offerings

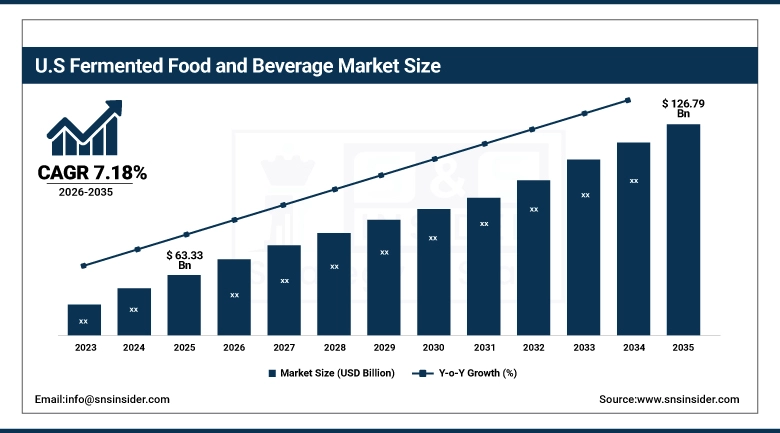

The U.S. Fermented Food and Beverage Market was valued at USD 63.33 billion in 2025 and is expected to reach USD 126.79 billion by 2035, growing at a CAGR of 7.18% from 2026-2035.

Growth in the U.S. Fermented Food and Beverage Market is driven by increasing consumer focus on gut health, immunity, and functional foods. Rising demand for probiotics, plant-based products, and convenient ready-to-eat options, along with expanding retail and e-commerce channels, is further supporting market expansion.

Fermented Food and Beverage Market Growth Drivers:

-

Rising consumer awareness about gut health and probiotics is fueling demand for fermented foods and beverages globally

Consumers are increasingly recognizing the importance of gut health and the role of probiotics in improving digestion, immunity, and overall wellness. This awareness has driven the popularity of fermented foods such as yogurt, kimchi, kefir, and kombucha. Health-conscious individuals are actively seeking products that promote a balanced microbiome, leading manufacturers to focus on probiotic-rich formulations. Additionally, educational campaigns and endorsements by nutritionists and health experts are further encouraging adoption, creating strong global demand and supporting growth of the fermented food and beverage market.

Over 60% of global consumers now consider gut health an important factor in their food and beverage choices, with fermented products like yogurt, kefir, kimchi, and kombucha cited as top sources of probiotics.

-

Growing popularity of functional and health-focused foods encourages manufacturers to expand fermented product portfolios

The rising trend of functional foods, which offer additional health benefits beyond basic nutrition, is encouraging companies to innovate within the fermented food and beverage space. Consumers increasingly prefer products that enhance immunity, aid digestion, and provide essential nutrients. In response, manufacturers are introducing fortified, flavored, and value-added fermented items to cater to evolving preferences. This trend is driving portfolio diversification, encouraging premium product offerings, and enabling companies to target health-conscious and wellness-focused segments, ultimately boosting market growth and expanding global consumption of fermented foods.

More than 70% of new fermented food and beverage launches in 2023 featured functional claims such as digestive support, immune health, or gut microbiome balance.

Fermented Food and Beverage Market Restraints:

-

High production costs and complex fermentation processes limit scalability and affordability for small-scale manufacturers in emerging markets

Producing fermented foods and beverages requires precise control over ingredients, temperature, and microbial activity, making the process labor-intensive and time-consuming. Small-scale manufacturers often struggle with high operational costs, including specialized equipment, quality testing, and skilled labor. These expenses limit their ability to scale production or offer products at competitive prices. As a result, affordability becomes a barrier for price-sensitive consumers, particularly in emerging markets. This financial constraint restricts market expansion and makes it challenging for smaller players to compete with large, established brands.

Small-scale producers in emerging markets often face 30–50% higher production costs compared to large manufacturers due to limited access to controlled fermentation technology and cold-chain infrastructure. The need for precise temperature, hygiene, and aging conditions makes scaling up fermented products challenging without significant capital investment.

-

Short shelf life and storage challenges hinder distribution and reduce consumer adoption in regions with limited cold chain infrastructure

Fermented foods and beverages are often highly perishable due to live cultures and minimal processing, requiring careful temperature control during storage and transport. In regions with inadequate cold chain facilities, maintaining product freshness and safety is difficult, leading to spoilage and quality degradation. Retailers and distributors face challenges in stocking and transporting these items efficiently. Consequently, consumer trust and adoption may decline. Limited storage infrastructure also increases operational costs, restricts market reach, and slows the growth of the fermented food and beverage market in regions lacking proper refrigeration and logistics support.

Fermented foods and beverages often require refrigeration to maintain live cultures and quality, with many products having a shelf life of just 14–30 days. In regions lacking reliable cold chain infrastructure

Fermented Food and Beverage Market Opportunities:

-

Increasing demand for plant-based and dairy-free fermented products offers innovation potential for new product development globally

Growing consumer interest in vegan, lactose-free, and plant-based diets is driving demand for alternative fermented products such as soy, almond, oat, and coconut-based yogurts and beverages. This trend encourages manufacturers to innovate and diversify product portfolios with functional, probiotic-rich, and flavored options. The shift toward sustainable and ethical consumption also supports market expansion. By leveraging plant-based fermentation, companies can attract health-conscious, environmentally aware, and niche consumer segments globally, creating opportunities for product differentiation, premium pricing, and long-term growth in the fermented food and beverage market.

Over 40% of global consumers now express interest in plant-based fermented options, with almond, oat, and coconut-based kefirs and yogurts among the fastest-growing alternatives

-

Expansion of online grocery platforms and direct-to-consumer sales channels enhances accessibility and market penetration of fermented foods

The rise of e-commerce, online grocery delivery, and subscription-based models has made fermented foods more accessible to consumers worldwide. Digital platforms allow manufacturers to reach urban and remote markets efficiently, bypassing traditional retail limitations. Personalized promotions, product recommendations, and home delivery services increase convenience and encourage trial among new customers. This digital transformation supports brand visibility, consumer engagement, and repeat purchases. As online shopping continues to grow, fermented food and beverage companies can expand market penetration, increase sales volume, and strengthen their presence in competitive global markets.

Online sales of fermented foods and beverages more than doubled between 2020 and 2023, with over 60% of repeat buyers citing convenience and consistent product availability as key factors. Direct-to-consumer models, including subscription boxes and curated wellness bundles, have enabled niche brands to reach health-conscious consumers in both urban and underserved rural areas.

Fermented Food and Beverage Market Segment Analysis

-

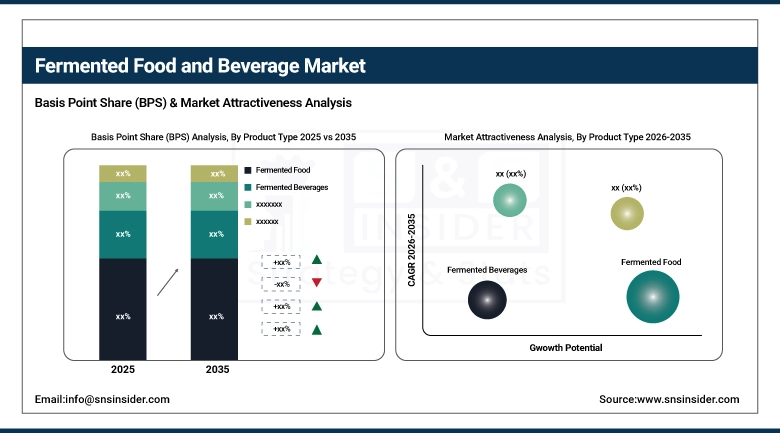

By Product Type: In 2025, Fermented Food led the market with 64% share, while Fermented Beverages is the fastest-growing segment with the highest CAGR (2026–2035)

-

By Distribution Channel: In 2025, Supermarkets/Hypermarkets led the market with 52% share, while Online Retail is the fastest-growing segment with the highest CAGR (2026–2035)

-

By Ingredient Source: In 2025, Dairy-based led the market with 52% share, while Plant-based is the fastest-growing segment with the highest CAGR (2026–2035

-

By Application: In 2025, Health & Wellness led the market with 45% share, while it is also the fastest-growing segment with the highest CAGR (2026–2035)

By Product Type: Fermented Food segment led in 2025; Fermented Beverages segment expected fastest growth 2026–2035

Fermented Food segment dominated the Fermented Food and Beverage Market with the highest revenue share of about 64% in 2025 due to its long-standing presence in traditional diets and widespread consumer acceptance. Products like yogurt, kimchi, and pickles are widely consumed for their flavor and health benefits. High demand for ready-to-eat, probiotic-rich options further strengthened its market dominance globally.

Fermented Beverages segment is expected to grow at the fastest CAGR from 2026-2035, driven by increasing consumer focus on health and wellness, particularly gut health. Rising popularity of kombucha, kefir, and other probiotic drinks, along with innovative flavors, convenient packaging, and expanding availability in modern retail channels, is fueling strong demand and rapid adoption worldwide.

By Distribution Channel: Supermarkets/Hypermarkets segment led in 2025; Online Retail segment expected fastest growth 2026–2035

Supermarkets/Hypermarkets segment dominated the Fermented Food and Beverage Market with the highest revenue share of about 52% in 2025 due to their extensive reach, competitive pricing, and convenience for bulk purchasing. Large product assortments, promotional offers, and loyalty programs attract a wide consumer base. These factors make supermarkets and hypermarkets the primary distribution channels for fermented products globally.

Online Retail segment is expected to grow at the fastest CAGR from 2026-2035, fueled by increasing internet penetration, changing consumer lifestyles, and demand for doorstep delivery. Growing preference for premium, niche, and organic fermented food and beverage products, combined with subscription services and targeted online marketing, is accelerating adoption and expanding the online retail channel’s share in the market.

By Ingredient Source: Dairy-based segment led in 2025; Plant-based segment expected fastest growth 2026–2035

Dairy-based segment dominated the Fermented Food and Beverage Market with the highest revenue share of about 52% in 2025 due to strong consumer familiarity, nutritional value, and extensive use in products like yogurt, kefir, and cheese. Established production infrastructure, distribution networks, and consistent demand for dairy-based fermented products contributed to its market dominance across regions.

Plant-based segment is expected to grow at the fastest CAGR from 2026-2035, driven by increasing consumer adoption of vegan, lactose-free, and environmentally sustainable diets. Innovations in plant-based fermented products, including yogurt, kefir, and cheese alternatives, along with rising awareness of ethical consumption and health benefits, are fueling rapid growth in this segment globally.

By Application: Health & Wellness segment led in 2025; same segment expected fastest growth 2026–2035

Health & Wellness segment dominated the Fermented Food and Beverage Market with the highest revenue share of about 45% in 2025 due to growing consumer focus on gut health, immunity, and overall well-being. The segment is expected to grow at the fastest CAGR from 2026-2035, driven by rising demand for functional foods, probiotics, and nutraceutical-enriched fermented products. Increased health consciousness, preventive healthcare trends, and product innovation continue to propel growth in this segment across global markets.

Regional Insights

Asia Pacific Fermented Food and Beverage Market Insights

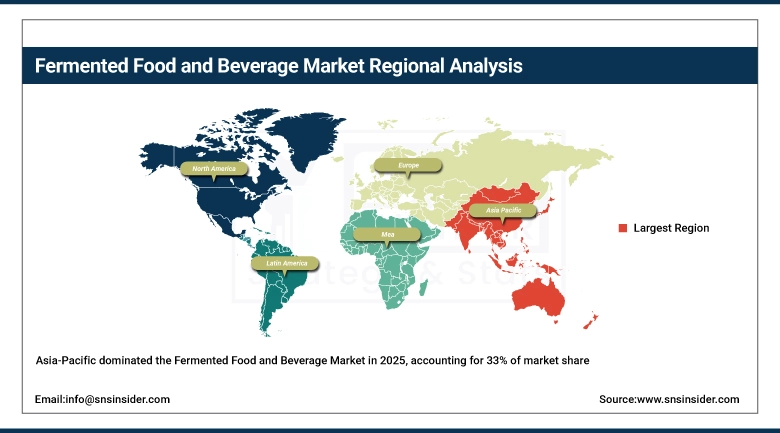

Asia Pacific dominated the Fermented Food and Beverage Market with a 33% share in 2025 due to the region’s strong cultural preference for traditional fermented foods, high population base, and well-established production and consumption practices. The market is also expected to grow at the fastest CAGR of about 9.60% from 2026–2035, driven by rising health awareness, increasing demand for probiotic-rich foods and beverages, growing urbanization, expanding modern retail channels, and the adoption of innovative fermented products by younger, health-conscious consumers.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Fermented Food and Beverage Market Insights

North America held a significant share in the Fermented Food and Beverage Market in 2025, supported by growing consumer awareness of gut health, high demand for probiotic and functional foods, and strong presence of organized retail and e-commerce channels. Increasing product innovation, health-conscious lifestyles, and rising adoption of fermented beverages further strengthened the region’s market position.

Europe Fermented Food and Beverage Market Insights

Europe held a strong position in the Fermented Food and Beverage Market in 2025, driven by high consumer preference for functional and probiotic-rich foods, well-established food processing infrastructure, and widespread adoption of fermented beverages. Increasing health awareness, supportive regulatory frameworks, and continuous product innovation further reinforced Europe’s leadership in the fermented food and beverage sector.

Middle East & Africa and Latin America Fermented Food and Beverage Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Fermented Food and Beverage Market in 2025, driven by rising health awareness, growing urban populations, and increasing demand for functional and probiotic-rich foods. Expanding modern retail and e-commerce channels, along with changing dietary habits and government initiatives promoting nutritious diets, further supported the regions’ emerging market presence.

Fermented Food and Beverage Market Competitive Landscape:

Nestlé S.A.

Nestlé S.A. continues to lead in the fermented food and beverage market, focusing on innovations in precision fermentation for alternative proteins, particularly animal-free dairy products. In 2024, Nestlé expanded its portfolio by integrating fermented ingredients that align with consumer demands for sustainability and health benefits. The company reported steady organic growth driven by healthier, plant-based alternatives and advanced fermentation technologies to boost nutritional profiles and taste. Its strategy includes ongoing investments in research and development for fermented product categories worldwide.

-

2024, Nestlé S.A. launched “Better Whey,” its first precision fermentation-derived dairy protein powder under the Orgain brand, delivering animal-free and lactose-free whey isolate with 21 grams of protein per serving

Danone S.A

Danone S.A. reported solid financial growth in 2024 with a focus on essential dairy and plant-based fermented products, including yogurts and kefirs. Danone’s Renewed strategy emphasizes science-based, health-forward segments, driving sales through high-protein and medical nutrition fermented offerings. The company leverages growing consumer trends toward health through food with strong volume growth in its essential dairy and plant-based portfolios. Danone also expanded sales in emerging markets and improved operating leverage while reinforcing sustainability commitments linked to fermented foods.

-

2024, Danone launched Actimel+ Triple Action — a fortified probiotic yogurt‑drink shot enriched with vitamins D, B6, C and magnesium for improved immunity and gut health. It rolled out across 20 European countries

Yakult Honsha Co. Ltd.

Yakult Honsha Co. Ltd. remains a dominant leader in probiotic fermented drinks, pioneering gut health innovations with its flagship products. In 2024, Yakult expanded into the plant-based segment, launching “The Power of Soy Milk,” a fermented plant-based yogurt line targeting health-conscious consumers. Yakult focuses on functional beverages enriched with probiotics aimed at digestive and immune health. Its expansion into plant-based fermented foods reflects broader consumer demand for natural, wellness-oriented products, supported by clinical research and global market reach in Asia, Latin America, and Europe.

-

2024, Yakult launched a new fermented‑milk drink called Yakult Plus Peach — a fat‑free, gluten‑free probiotic drink with dietary fiber and vitamin C, offering a lighter, lower‑sugar fermented option.

The Coca-Cola Company

leveraged its broad beverage portfolio in 2024 to support growth in functional and fermented beverage categories indirectly. While no direct fermented product launches were highlighted, Coca-Cola expanded sustainable packaging initiatives with more returnable glass bottles, facilitating healthier and diverse beverage consumption. The company also grew its global outlet presence, helping increase consumer access to functional and fermented beverages aligned with wellness trends. Coca-Cola’s ongoing investment in variety and sustainability supports its position in the fermented functional drinks market ecosystem.

-

2025, The Coca-Cola Company launched Simply Pop, its first prebiotic soda line featuring five fruit flavors made with real fruit juice, no added sugar, prebiotic fiber for gut health support, and added Vitamin C and zinc for immune benefits. This zero-calorie, bubbly functional beverage, debuting regionally in the U.S.

Fermented Food and Beverage Market Key Players

-

Danone S.A.

-

PepsiCo Inc.

-

Mondelez International

-

Anheuser-Busch InBev

-

The Coca-Cola Company

-

Kraft Heinz Company

-

Kerry Group

-

Arla Foods

-

General Mills Inc.

-

Unilever PLC

-

Constellation Brands Inc.

-

Carlsberg Group

-

Heineken N.V.

-

Fonterra Co-operative Group

-

Meiji Holdings Co. Ltd.

-

Chr. Hansen Holding A/S

-

Suntory Holdings Ltd.

-

Lifeway Foods Inc.

Fermented Food and Beverage Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 302.28 Billion |

| Market Size by 2035 | USD 647.18 Billion |

| CAGR | CAGR of 7.91% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Fermented Food, Fermented Beverages) • By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Other Channels) • By Ingredient Source (Dairy-based, Plant-based, Grain-based, Others Source) • By Application (Health & Wellness, Culinary/Ready-to-Eat, Alcoholic Beverages, Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Nestlé S.A., Danone S.A., PepsiCo Inc., Yakult Honsha Co. Ltd., Mondelez International, Anheuser-Busch InBev, The Coca-Cola Company, Kraft Heinz Company, Kerry Group, Arla Foods, General Mills Inc., Unilever PLC, Constellation Brands Inc., Carlsberg Group, Heineken N.V., Fonterra Co-operative Group, Meiji Holdings Co. Ltd., Chr. Hansen Holding A/S, Suntory Holdings Ltd., Lifeway Foods Inc. |

Frequently Asked Questions

Asia Pacific dominated the Fermented Food and Beverage Market in 2025 with a 33% share due to cultural preference and consumption practices.

Fermented Food type, Supermarkets/Hypermarkets channel, Dairy-based ingredient, and Health & Wellness application segments dominated with highest revenue globally.

Rising consumer awareness of gut health, probiotics, and functional, plant-based, and dairy-free fermented products is driving market growth globally.

The Fermented Food and Beverage Market was valued at USD 302.28 billion in 2025, driven by increasing demand for functional foods.

The Fermented Food and Beverage Market is expected to grow at a CAGR of 7.91% from 2026 to 2035 globally.

Get in Touch