Sapphire Technology Market Report Scope & Overview:

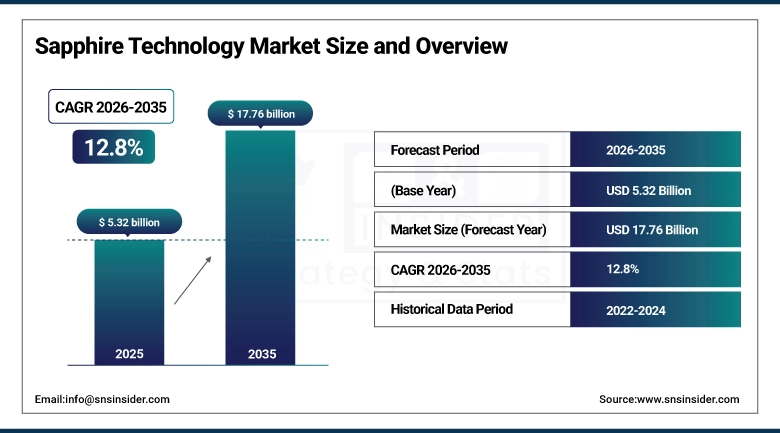

The Sapphire Technology Market was valued at USD 5.32 billion in 2025 and is expected to reach USD 17.76 billion by 2035, growing at a CAGR of 12.8% from 2026–2035.

There is an observed fast growth in the market of sapphire technology products caused by consumer electronics, aerospace, ICT, and power semiconductor industries. Characteristics like hardness (the second hardest substance only after diamonds), stability of temperatures, optical clarity, chemical neutrality, and insulation properties of sapphire make it a vital component in creating LEDs, semiconductors, and optical components of different technologies. One of the important innovations in this area, apart from switching to bigger wafers (upgrading from 6-inch wafer technology to 8-inch one), is related to new innovations in the manufacturing process of such materials, namely the application of Kyropoulos and Czochralski methods, resulting in increased effectiveness and reduced costs of manufacturing. The emergence of new markets through the implementation of sapphire substrates for technologies like 5G, data centers, optical communication, power semiconductors, and aerospace technologies is valid up to 2035.

According to industry data, the Consumer Electronics segment captured approximately 41% of Sapphire Technology Market revenue in 2025, driven by heavy deployment of sapphire in smartphone screens, camera lenses, and wearable device covers — while the ICT segment is forecasted to grow at the highest CAGR of 16.28% driven by rising adoption in 5G infrastructure and optical networks.

Sapphire Technology Market Size and Forecast

-

Market Size in 2025: USD 5.32 Billion

-

Market Size by 2035: USD 17.76 Billion

-

CAGR: 12.8% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Sapphire Technology Market - Request Free Sample Report

Sapphire Technology Market Trends

-

Rapid scaling of sapphire wafer sizes from 6-inch to 8-inch formats to maximize production efficiency, improve cost performance, and enable compatibility with next-generation semiconductor manufacturing processes.

-

Increasing utilization of sapphire substrate in 5G networks, optical devices, and data centers due to rising demands for high performance, thermal stability, and optical precision of materials.

-

Sapphire substrates gaining more prominence in optical systems used in aerospace and defense sectors, which include infrared sensor windows, dome cover of missiles, and robust optical components for military and aerospace industries.

-

Growing use of sapphire in power electronics devices for heat dissipation properties and electrical insulation properties due to the widespread adoption of power semiconductor devices in electric vehicle technology.

-

Development in AI and automation for the sapphire crystal manufacturing process, such as ML-assisted Kyropoulos furnace techniques, which will increase yields and cut down production expenses.

-

Increased use of sapphire for medical equipment such as surgical tools and implants, and biosensing equipment, due to their compatibility, hardness, and sterilizability.

-

Increase in the use of sapphire for wearable devices, such as smartwatch screens and fitness watch cases, and virtual and augmented reality optical equipment, as consumers look for scratch-resistant products.

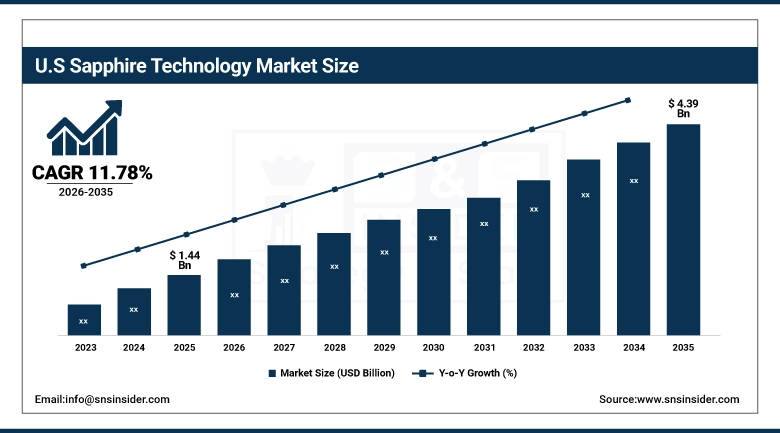

U.S. Sapphire Technology Market reached USD 1.44 billion in 2025 and is expected to reach USD 4.39 billion by 2035, registering a CAGR of 11.78% during 2026–2035.

The reason that America enjoys dominance in the market of sapphire technology is due to its well-developed semiconductor sector, its leading market companies, and heavy investments made in research and development of sapphire-based technology. The American aerospace and defense industries comprise an important consumer base for sapphire optical products, whereas the robust domestic consumer electronics manufacturing chain ensures continued demand for sapphire technologies. The government funding of domestic semiconductor production through the CHIPS Act is another factor contributing to the dominance of the United States within advanced materials technologies, such as sapphire technology.

However, the transition within the entire industry towards using sapphire wafers in 8-inch dimensions, as opposed to the previous 6-inch dimension, represents a truly revolutionary development, which will allow for better economics of production, thus opening new opportunities for the use of this technology across multiple areas until 2035.

Sapphire Technology Market Segment Insights

-

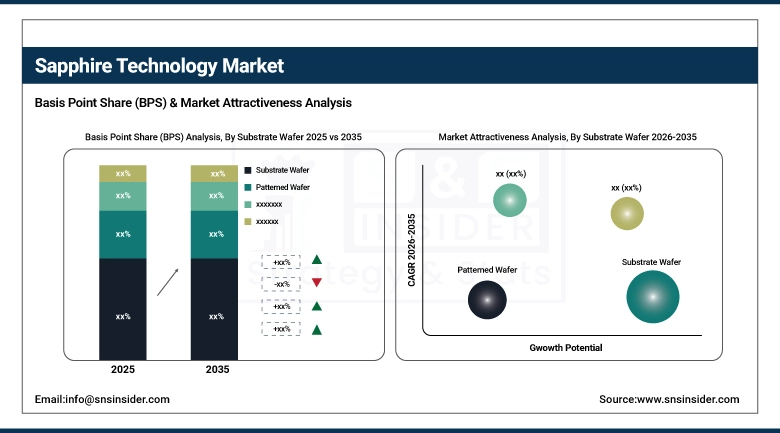

Based on Substrate Wafer, Substrate Wafer accounted for the largest market share (~42.31%) in 2025; Wafer Size expected to be the fastest-growing segment (CAGR of 15.63%).

-

Based on Devices, Opto-Semiconductor accounted for the largest market share (~30.59%) in 2025; Power Semiconductor expected to be the fastest-growing segment (CAGR of 15.13%).

-

Based on Application, Consumer Electronics accounted for the largest market share (~41%) in 2025; ICT expected to be the fastest-growing segment (CAGR of 16.28%).

Sapphire Technology Market Segment Analysis

By Substrate Wafer, Substrate Wafer dominates, Wafer Size expected to grow fastest

The Substrate Wafer segment had the largest market share of around 42.31% in terms of revenue generated in the sapphire technology market in 2025, which was attributed mainly to the use of single crystal substrate wafers in various applications in LEDs, semiconductors, and optoelectronics. Substrate wafers make up the base material structure on which epitaxial films can be deposited for the development of LEDs and semiconductors.

The Wafer Size segment is anticipated to experience the fastest CAGR of 15.63% during 2026–2035. The Wafer Size segment is projected to register the fastest CAGR at 15.63%. The growth in wafer diameter from 4 inches to 6 inches and moving further to 8 inches is influenced by the need for higher throughput and improved yield of devices per wafer while also lowering the cost-per-device. Such an evolution is helping the material of choice to be more competitive with other substrates used in the industry.

By Devices, Opto-Semiconductor dominates, Power Semiconductor expected to grow fastest

The Opto-Semiconductor segment dominated with approximately 30.59% revenue share in 2025. Optoelectronic devices including LEDs, laser diodes, and photodetectors extensively utilize sapphire substrates due to their optical clarity, thermal stability, and lattice compatibility with gallium nitride (GaN) epitaxial layers — the material foundation for high-brightness LEDs and laser applications. The switch towards LED lighting on the global scale and the rising use of solid state lighting technologies will keep up the demand for opto-semiconductor grade sapphire.

The power semiconductor market is predicted to show the highest growth rate with a CAGR of 15.13% in 2026-2035. The increasing application of sapphire substrates in the production of power electronic devices that need heat conductivity and electrical isolation is what has led to the growth of this trend. Some of the factors leading to this trend include the electrification of car production, renewable energy, and industrial power management.

By Application, Consumer Electronics dominates, ICT expected to grow fastest

Consumer Electronics dominated with approximately 41% revenue share in 2025 due to heavy usage of sapphire across smartphone camera lens covers, screen protection glass for premium wearables, and optical components in high-end smartphones and smartwatches. Major consumer electronics brands continue to deploy sapphire for its superior scratch resistance and optical properties in flagship device lines.

The ICT segment is expected to grow at the highest CAGR of 16.28% during 2026–2035, driven by the rapidly increasing adoption of sapphire components in 5G infrastructure — including optical transceivers, base station windows, and high-frequency optical communication components — as well as in data center optical interconnects and semiconductor photonic devices.

Sapphire Technology Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

UAE |

28% |

|

Latin America |

Brazil |

40% |

North America Sapphire Technology Market Insights

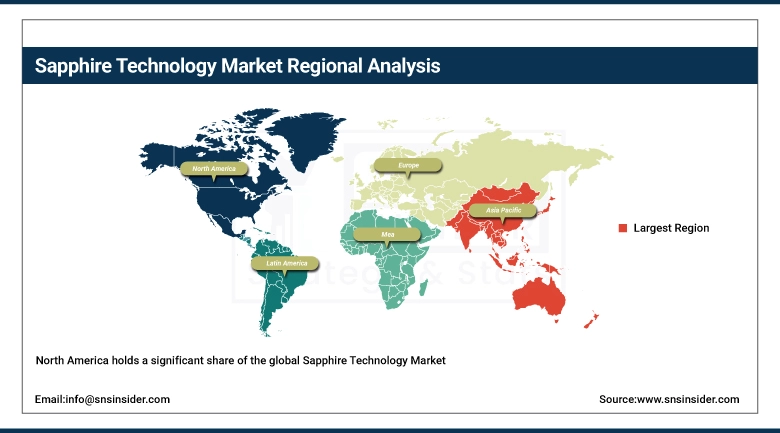

North America holds a significant share of the global Sapphire Technology Market due to strong demand from the semiconductor, aerospace, defense, and optoelectronics industries. The United States leads regional growth with increasing adoption of sapphire substrates in LEDs, RF devices, optical windows, and advanced sensor applications. Increasing investment in semiconductor production and photonic technology will drive market growth. Government programs such as CHIPS Act will help in improving semiconductor value chain domestically and foster advancements in materials processing capabilities throughout the region. Besides, rising adoption of sapphire in the field of defense optics, military sensors, and industrial applications will increase the demand for sapphire. Companies like Coherent and Rubicon Technology are working on improving technological developments and expanding regional capacities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Sapphire Technology Market Insights

Asia Pacific dominates the global Sapphire Technology Market due to strong semiconductor manufacturing capabilities, large-scale LED production, and expanding consumer electronics industries across China, Japan, South Korea, and Taiwan. The region is witnessing rising demand for sapphire substrates used in LEDs, smartphone components, optical sensors, and semiconductor applications. China continues to be an important manufacturing base owing to its well-developed electronics manufacturing facilities and increasing investments in advanced materials. Japan and South Korea are at the forefront of optoelectronic innovations and advances in sapphire machining technology. Increasing adoption of sapphire materials in automotive electronics, industrial optics, and 5G infrastructure is further accelerating regional market growth. Strong government support for semiconductor self-sufficiency and expanding electronics exports continue to strengthen Asia Pacific’s market leadership.

Europe Sapphire Technology Market Insights

Europe is seeing continuous growth in its Sapphire Technology Market due to the rising demand from the aerospace industry, defense sector, medical devices industry, and industrial optics industry. Several countries in Europe, such as Germany, France, and the UK, have started investing in semiconductor technology development, photonics research, and high precision optical technology systems using sapphire technology components. The rising use of sapphire technology components in the production of defense products and industrial lasers is propelling the growth of the region's market. Furthermore, the increasing investments in electric vehicles, sensor technology, and medical imaging technology are presenting opportunities for the companies producing sapphire technology components in the region.

Middle East & Africa and Latin America Sapphire Technology Market Insights

The market for sapphire technology solutions in the Middle East & Africa is in its nascent stages due to factors including defense upgrades, telecommunication infrastructure development, and industrial diversification. Some of the nation’s using sapphire optical materials include the UAE, Saudi Arabia, and Israel. Government programs aimed at fostering digital transformation and diversification have been contributing to technological advances.

Latin America is considered to be at the beginning phase of the growth of the industry dealing in sapphire technology due to the emerging importance of advanced materials in electronic devices and other machinery. Among the primary markets in Latin America include Brazil and Mexico, buoyed by the emergence of smartphone production facilities and the establishment of fourth- and fifth-generation telecommunications networks.

Sapphire Technology Market Growth Drivers:

Technological Advancement and Multi-Sector Demand Driving Sapphire Technology Market Expansion

The Sapphire Technology Market is witnessing robust growth owing to consistent innovations in the growth of sapphire crystals and increased adoption in various high-growth sectors. Increasing applications of sapphire substrates in 5G network infrastructure, LED lighting systems, and power electronics have been driving the global market. Moreover, there is growing integration of sapphire technology in aerospace & defense equipment and medical devices because of its superior properties such as thermal stability, optical clarity, and resistance to wear and tear. The trend toward bigger wafer diameters and higher manufacturing efficiencies is optimizing the production process. Additionally, artificial intelligence-based sapphire crystal growth methodologies and precise fabrication technologies are enhancing the quality and scalability of the material. Applications of sapphire technology in semiconductor devices, optoelectronic devices, and highly sensitive sensors are making the technology one of the most crucial advanced materials segments.

Sapphire Technology Market Restraints

High Production Complexity and Cost Constraints Limiting Large-Scale Adoption

The Sapphire Technology Market is subject to some serious restraints owing to the expensive nature and complex process involved in the production of sapphire crystals. Producing quality sapphire wafers is not an easy task, as it involves highly energy-consuming procedures, the use of sophisticated equipment, and stringent environmental conditions, hence higher costs when compared to other materials. Additionally, it is difficult to upscale larger diameter wafers along with yield loss during the cutting and polishing stage, which further contributes to increased costs. Moreover, reliance on advanced manufacturing facilities acts as an obstacle in entering the market for new entrants. Furthermore, issues with supply chain management pertaining to pure raw materials and lengthy production timelines also pose a challenge in commercializing products.

Sapphire Technology Market Opportunities

Expanding Semiconductor, 5G, and Advanced Optics Applications Creating Strong Growth Potential

There are several promising prospects in the Sapphire Technology Market owing to various applications ranging from semiconductors, 5G technology, optoelectronic components, aircraft and spacecraft, and medical technologies. Increased requirements for substrates that perform well in LED lighting, radiofrequency, and advanced sensing technologies will boost market performance. In parallel, growing developments within electric vehicles and power electronics can significantly contribute to the development of sapphire products because of their durability. Apart from that, increased funding for photonics, defense optics, and medical imaging can open up more avenues of higher value in the market. Further improvements of technologies in producing large-size wafers and low-cost crystals are anticipated in the future. Finally, more and more incorporation of AI-based processes and next-generation semiconductor materials creates potential in terms of expanding sapphire applications.

Recent Developments:

-

2026: Coherent Corp. expanded sapphire substrate and optical material capabilities for semiconductor and defense applications, focusing on high-purity sapphire wafers used in RF devices, aerospace optics, and advanced photonics systems amid rising U.S. CHIPS Act-driven demand.

-

2026: Rubicon Technology advanced production of large-diameter sapphire wafers for LED, defense, and semiconductor applications, with continued focus on improving yield efficiency and scaling optical-grade sapphire substrates for industrial and electronic markets.

-

2026: Kyocera Corporation Strengthened sapphire component integration in electronic and industrial ceramics, expanding use in high-durability optical windows and semiconductor equipment components for automotive and 5G infrastructure systems.

Sapphire Technology Market Key Players

Some of the Sapphire Technology Market Companies are:

-

Coherent Corp.

-

Rubicon Technology

-

Kyocera Corporation

-

Monocrystal Inc.

-

GT Advanced Technologies

-

Sapphire Technology Co., Ltd.

-

Namiki Precision Jewel Co., Ltd.

-

Tera Xtal Technology Corporation

-

DK Aztec Co., Ltd.

-

Sumitomo Chemical Co., Ltd.

-

Fraunhofer-Gesellschaft

-

Cyberstar

-

ACME Electronics Corporation

-

Saint-Gobain Crystals

-

Adamant Namiki Precision Jewel

-

Everlight Electronics

-

Cree

-

Veeco Instruments

-

Advanced Energy Industries

-

Precision Sapphire Technologies

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.32 Billion |

| Market Size by 2035 | USD 17.76 Billion |

| CAGR | CAGR of 12.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Substrate Wafer (Substrate Wafer, Patterned Wafer, Wafer Size) • By Devices (Opto-Semiconductor, Power Semiconductor, Others) • By Application (Consumer Electronics, Aerospace & Defense, ICT, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Coherent Corp., Rubicon Technology, Kyocera Corporation, Monocrystal Inc., GT Advanced Technologies, Sapphire Technology Co., Ltd., Namiki Precision Jewel Co., Ltd., Tera Xtal Technology Corporation, DK Aztec Co., Ltd., Sumitomo Chemical Co., Ltd., Fraunhofer-Gesellschaft, Cyberstar, ACME Electronics Corporation, Saint-Gobain Crystals, Adamant Namiki Precision Jewel, Everlight Electronics, Cree, Veeco Instruments, Advanced Energy Industries, Precision Sapphire Technologies |

Frequently Asked Questions

Ans: Asia Pacific holds the largest share of the Sapphire Technology Market, driven by China's dominant LED manufacturing ecosystem, Japan and South Korea's advanced semiconductor industries, and the region's massive consumer electronics production base.

Ans: The Consumer Electronics segment dominated the Sapphire Technology Market in 2025 with approximately 41% revenue share, driven by heavy usage of sapphire in smartphone camera lens covers, screen protection glass for wearables, and optical components in premium consumer devices.

Ans: The Substrate Wafer segment dominated the Sapphire Technology Market in 2025, accounting for approximately 42.31% of global revenue, owing to the widespread deployment of single-crystal sapphire substrates in LED, semiconductor, and optoelectronic device fabrication.

Ans: Rapid technological advancement in sapphire crystal growth methods — combined with expanding adoption across LEDs, 5G infrastructure, power semiconductors, aerospace optics, and consumer electronics — is the primary structural driver of sustained market growth through 2035.

Ans: The Sapphire Technology Market was valued at USD 5.32 billion in 2025.

Ans: The Sapphire Technology Market is expected to grow at a CAGR of 12.8% from 2026 to 2035.

Get in Touch