Managed Security Services market Report Scope & Overview:

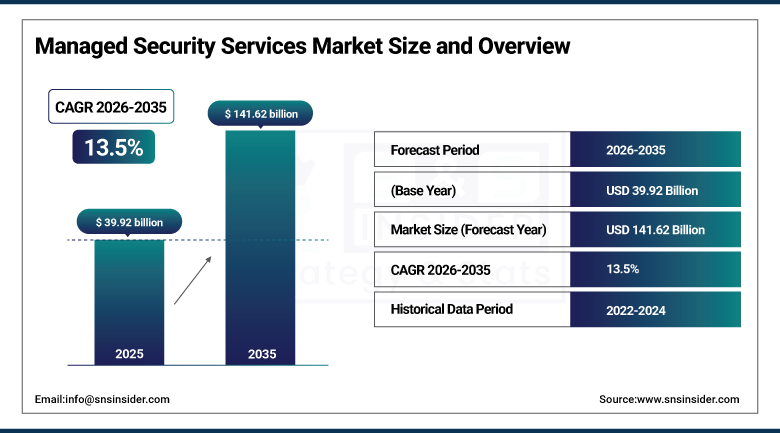

The Managed Security Services Market was valued at USD 39.92 billion in 2025 and is expected to reach USD 141.62 billion by 2035, growing at a CAGR of 13.5% from 2026-2035.

The Managed Security Services Market is anticipated to grow owing to the growing number of cyberattacks, ransomware attacks, and data breaches within businesses globally. Increased adoption of cloud computing, remote working spaces, and IoT-enabled devices is leading to an increased requirement for continuous network monitoring and threat detection. Additionally, stringent data protection regulations, shortage of skilled professionals, and advancements in artificial intelligence-powered security solutions have compelled organizations to opt for managed security services.

According to the Microsoft Digital Defense Report 2025, Microsoft processes 100 trillion security signals daily, blocks 4.5 million malware attempts every day, and analyzes 38 million identity risk detections per day, highlighting the unprecedented scale of modern cyberattacks and the need for continuous managed monitoring and response capabilities.

Further, the UK Government Cyber Security Breaches Survey 2025 reported that around 38% of businesses experienced phishing attacks, while ransomware continues to remain a persistent threat to critical systems, even as detection and response capabilities continue to improve.

Managed Security Services Market Size and Forecast

-

Managed Security Services Market Size in 2025: USD 39.92 Billion

-

Managed Security Services Market Size by 2035: USD 141.62 Billion

-

CAGR: 13.5% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Managed Security Services Market - Request Free Sample Report

Managed Security Services Market Trends

-

Rising frequency of cyberattacks, ransomware incidents, and data breaches is driving the managed security services market.

-

Growing adoption of outsourced cybersecurity solutions across BFSI, healthcare, government, and IT sectors is boosting market growth.

-

Expansion of cloud computing, remote work environments, and connected devices is fueling demand for continuous security monitoring.

-

Increasing focus on threat detection, incident response, compliance management, and risk mitigation is shaping adoption trends.

-

Advancements in AI-driven security analytics, zero-trust architectures, and managed detection and response (MDR) services are enhancing protection capabilities.

-

Rising shortage of skilled cybersecurity professionals and growing regulatory requirements are supporting market expansion.

-

Collaborations between cybersecurity vendors, cloud providers, and enterprises are accelerating innovation and global adoption.

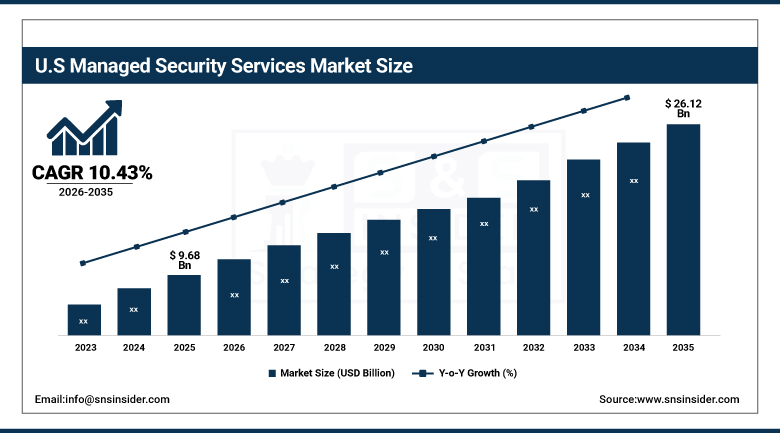

U.S. Managed Security Services Market was valued at USD 9.68 billion in 2025 and is expected to reach USD 26.12 billion by 2035, growing at a CAGR of 10.43% from 2026-2035.

The U.S. Managed Security Services Market is witnessing steady growth owing to the increase in cybercrime occurrences, greater enterprise use of cloud-based infrastructure, and high demand for advanced threat management systems. Moreover, stringent regulations, increasing remote working trends, and substantial investments in AI-powered security systems are contributing to market growth.

Managed Security Services Market Segment Highlights

-

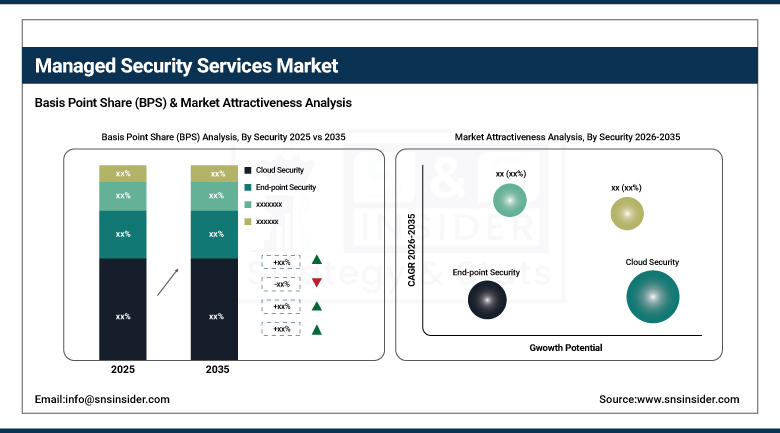

By Security, Cloud Security segment dominated the Managed Security Services Market in 2025 with 34% market share; End-point Security segment fastest growing (CAGR).

-

By Security Services, Managed SIEM segment dominated the Managed Security Services Market in 2025 with 29% market share; Managed XDR segment fastest growing (CAGR).

-

By Enterprise Size, Large Enterprises segment dominated the Managed Security Services Market in 2025 with 68% market share; SMEs segment fastest growing (CAGR).

-

By Vertical, BFSI segment dominated the Managed Security Services Market in 2025 with 24% market share; Healthcare segment fastest growing (CAGR).

Managed Security Services Market Segment Analysis

By Security, Cloud Security segment dominates the Managed Security Services Market, End-point Security segment expected to grow fastest

Cloud Security held a largest market share in the Managed Security Services Market during 2025 because of the growing usage of cloud computing, hybrid working models, and multi-cloud systems by enterprises. There was an increased need for managing cloud security among companies because of the increasing usage of cloud solutions that needed protection against cyber security risks and unauthorized access. The increase in reliance on SaaS, regulations regarding cloud security, and cyber-attacks in the cloud were some reasons behind the growth in demand for cloud security.

Endpoint Security is predicted to be the fastest-growing segment in the forecasted period due to factors like the growing number of connected devices and cyber-attacks on endpoints such as laptops, smartphones, and IoT devices. Companies are spending significantly on endpoint protection services to protect their businesses against cyber security threats. Increasing use of machine learning and real-time monitoring technologies has driven the demand for managed endpoint security services.

By Security Services, Managed SIEM segment dominates the Managed Security Services Market, Managed XDR segment expected to grow fastest

The Managed SIEM Segment emerged as the leader in the Managed Security Services Market in 2025 due to its capacity to enable centralized monitoring, threat analysis, and incident response for corporate networks. Organizations have opted for managed SIEM offerings to enhance their visibility regarding security incidents, improve compliance management, and bolster their cybersecurity operations. The escalating intricacy of cyberattacks and increasing demands for continuous monitoring have been significant factors in the adoption of managed SIEM services.

The Managed XDR segment will witness rapid expansion during the forecast period thanks to its superior ability to correlate and integrate threat information from a range of channels including endpoint systems, networks, clouds, and emails. Enterprises are increasingly adopting managed XDR offerings to improve threat detection and automate the entire process of threat responses and mitigation. Growing complexities and increasing sophistication of cyberattacks are fueling the rapid rise of this segment.

By Enterprise Size, Large Enterprises segment dominates the Managed Security Services Market, SMEs segment expected to grow fastest

The Large Enterprises segment was the dominant one in the Managed Security Services Market in 2025 due to their well-developed IT infrastructure, huge amounts of business data, and high vulnerability to highly developed cyber attacks. This segment of enterprises made substantial investments in managed security solutions to ensure their compliance with regulations, maintain business continuity, and counter emerging cyber threats. High budgets for cybersecurity and the increasing popularity of complex digital transformations have contributed to this segment's market dominance.

SMEs segment is expected to experience the highest growth rate in the forecast period due to increasing awareness about the cybersecurity risk and the rise in attacks on smaller companies. SMEs use managed security services to get access to highly developed threat prevention without the maintenance of expensive internal cybersecurity teams. Rapid digitalization, adoption of cloud technologies, and affordability of subscription security services will be driving market growth in this segment.

By Vertical, BFSI segment dominates the Managed Security Services Market, Healthcare segment expected to grow fastest

The BFSI segment accounted for the largest share of the Managed Security Services Market in 2025 owing to the large amount of confidential financial data, stringent compliance regulations, and rising cyber frauds and ransomware attacks. BFSI organizations made significant use of managed security services to facilitate safe digital transactions, safeguard customer data, and ensure business continuity. The quick uptake of digital banking and development of online payment platforms increased cybersecurity spending in the BFSI industry.

The healthcare sector is anticipated to register the highest growth rate in the forecast period owing to the rapid digitalization of the healthcare ecosystem, rising implementation of electronic medical records, and growing number of cyber threats to the healthcare information. Hospitals and clinics have started adopting managed security services for safeguarding critical medical information, connected devices, and cloud-enabled healthcare applications. Compliance requirements and telehealth offerings have played a pivotal role in driving the deployment of cybersecurity solutions in the healthcare industry.

Managed Security Services Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90.9% |

|

Europe |

United Kingdom |

24.8% |

|

Asia Pacific |

Australia |

8.7% |

|

Middle East & Africa |

UAE |

18.2% |

|

Latin America |

Brazil |

53.1% |

North America Managed Security Services Market Insights

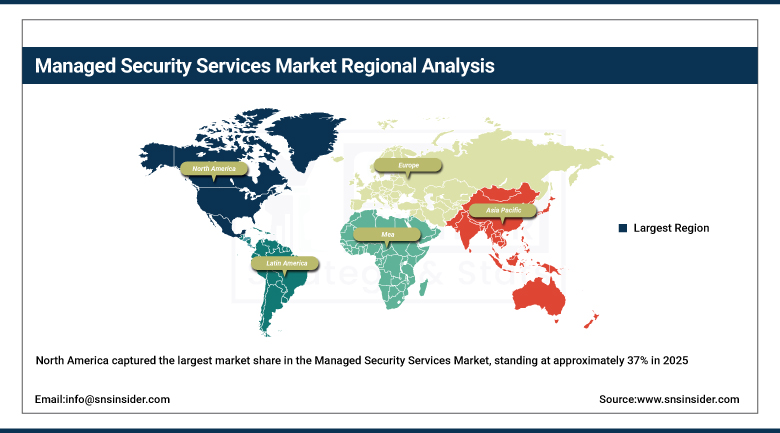

North America captured the largest market share in the Managed Security Services Market, standing at approximately 37% in 2025, owing to the high penetration of cybersecurity players, robust digital infrastructure, and significant enterprise cybersecurity expenditure. BFSI, healthcare, government, and IT industries are increasingly opting for managed SIEM, cloud security, and threat intelligence services owing to the growing prevalence of cyber threats. The increased pressure from strict data protection laws, ransomware attacks, and hybrid working conditions is also boosting the regional market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Managed Security Services Market Insights

Asia Pacific is experiencing the highest growth rate among all regions because of high digitalization, adoption of cloud computing solutions, and increased awareness of the need for cybersecurity measures among businesses. Investment in technologies, e-commerce platforms, and digital banking solutions has generated an increased need for managed security solutions in the region. Increased cyberattacks, SMEs' adoption of outsourcing security solutions, and government efforts to develop cybersecurity infrastructure have encouraged companies to adopt managed detection, endpoint security, and compliance management solutions.

Europe Managed Security Services Market Insights

In 2025, the Europe plays a vital role in the Managed Security Services Market because of the presence of strict data privacy laws such as GDPR and the rising number of cybersecurity threats. Strict data privacy laws and increased importance placed on securing critical infrastructure. Germany is the leading nation due to the robust industrial landscape and the need for cybersecurity measures for critical infrastructures. European organizations have been increasingly turning towards MSS solutions to meet their regulatory requirements and safeguard intellectual property.

Middle East & Africa and Latin America Managed Security Services Market Insights

In 2025, the Middle East & Africa and Latin America regions are emerging markets for Managed Security Services. Digitalization, cyber risks, and increased awareness regarding data security will spur the growth of the managed security services market. In the Middle East & Africa and Latin America regions, governments have been focusing on establishing cybersecurity policies that promote MSS within businesses. Banking institutions, government organizations, and telecommunication firms present significant opportunities for the growth of MSS market.

Managed Security Services Market Growth Drivers:

-

Rising Cybersecurity Threats and Regulatory Compliance Drive Growth in the Managed Security Services Market

The growth in the Managed Security Services market can be attributed to the increasing occurrence of cyberattacks. Companies from all sectors are facing threats in the form of ransomware attacks and phishing, which are pushing them towards implementing round-the-clock security measures. Furthermore, there are increasing regulations that require companies to maintain high standards of data security and compliance. MSS service providers assist companies in achieving this objective through their continuous monitoring, detection, and incident response services. This not only reduces the workload for companies but also enhances their security position. With more companies embracing hybrid work environments and transferring critical processes to digital platforms, the risk exposure increases, and hence, MSS becomes a necessity.

Managed Security Services Market Restraints:

-

High Implementation Costs and Integration Challenges Restrain the Growth of the Managed Security Services Market

The implementation and integration of MSS services can prove costly at the onset, considering that considerable resources must be invested in the software and platforms used, as well as the process of onboarding personnel. This problem is compounded by the financial constraints of small and medium-sized enterprises that have little money allocated for cybersecurity purposes. The integration of MSS services within the current information technology and security framework of firms is another issue. This process can be complicated and might even disrupt daily operations. Customization of the services according to the requirements of the firm can also pose problems.

Managed Security Services Market Opportunities:

-

Expansion of Cloud Services and Remote Work Environments Presents Opportunities for Managed Security Services Market Growth

Cloud computing and the move to remote working have created great opportunities for the Managed Security Services market. With organizations moving towards a distributed IT environment where data resides in multiple places, issues such as data privacy, security of information, and compliance with security regulations become critical. In order to fill this gap, MSS players can provide services that offer security against breaches related to cloud and endpoint systems. Such services help organizations manage access, ensure anomaly detection, and comply with security policies in complex and constantly changing IT landscapes. The adoption of remote working makes organizations more vulnerable and therefore makes them susceptible to attacks and cybercrimes.

Recent Developments:

-

2026: Palo Alto Networks unveiled Prisma AIRS 2.0 and Cortex Cloud 2.0 to strengthen AI-powered managed security operations in 2026. The platforms enhanced automated cloud threat monitoring, AI application security, and SOC orchestration capabilities.

-

2025: IBM launched Sovereign Core, a platform enabling governments and enterprises to manage AI data securely within regulated jurisdictions. The solution strengthened managed security and compliance capabilities supporting sovereign cloud and AI infrastructure protection.

-

2025: Palo Alto Networks introduced Cortex Cloud ASPM, a prevention-first application security platform improving managed cloud security operations. The solution unified AppSec visibility and automated risk prevention across enterprise cloud and AI application infrastructures.

-

2024: HCLTech partnered with CrowdStrike to strengthen MDR services using the AI-native Falcon XDR platform. The collaboration expanded cybersecurity transformation services across cloud, identity, data, and next-generation SIEM operations for enterprise customers worldwide.

-

2023: Palo Alto Networks partnered with IBM to enhance AI-driven managed cybersecurity offerings. The agreement combined Palo Alto’s Cortex security operations capabilities with IBM consulting expertise, improving enterprise-wide MDR and SOC transformation services for global customers.

Key Players

Some of the Managed Security Services Market Companies

-

IBM Corporation

-

Accenture plc

-

Cisco Systems Inc.

-

Palo Alto Networks

-

CrowdStrike Holdings Inc.

-

Fortinet Inc.

-

Secureworks Inc.

-

Check Point Software Technologies Ltd.

-

Rapid7 Inc.

-

Sophos Ltd.

-

Arctic Wolf Networks Inc.

-

SentinelOne Inc.

-

AT&T Cybersecurity

-

Verizon Business

-

NTT DATA Group Corporation

-

Tata Consultancy Services

-

Infosys Limited

-

Wipro Limited

-

HCLTech

-

DXC Technology

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.92 Billion |

| Market Size by 2035 | USD 141.62 Billion |

| CAGR | CAGR of 13.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Security (Cloud Security, End-point Security, Network Security, Data Security, Others) • By Services (Managed SIEM, Managed UTM, Managed DDoS, Managed XDR, Managed IAM, Managed Risk & Compliance) • By Enterprise Size (Large enterprises, SMEs) • By Vertical (BFSI, Healthcare, Manufacturing, IT & Telecommunications, Retail, Defense/Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Accenture plc, Cisco Systems Inc., Palo Alto Networks, CrowdStrike Holdings Inc., Fortinet Inc., Secureworks Inc., Check Point Software Technologies Ltd., Rapid7 Inc., Sophos Ltd., Arctic Wolf Networks Inc., SentinelOne Inc., AT&T Cybersecurity, Verizon Business, NTT DATA Group Corporation, Tata Consultancy Services, Infosys Limited, Wipro Limited, HCLTech, DXC Technology |

Frequently Asked Questions

Ans: North America dominated the Managed Security Services Market in 2025.

Ans: The Large Enterprises segment dominated the Managed Security Services Market in 2025.

Ans: Rising Cybersecurity Threats and Regulatory Compliance Drive Growth in the Managed Security Services Market.

Ans: The Managed Security Services Market was valued at USD 39.92 billion in 2025.

Ans: The Managed Security Services Market is expected to grow at a CAGR of 13.5% from 2026 to 2035.

Get in Touch