Remote Home Monitoring Systems Market Report Scope & Overview:

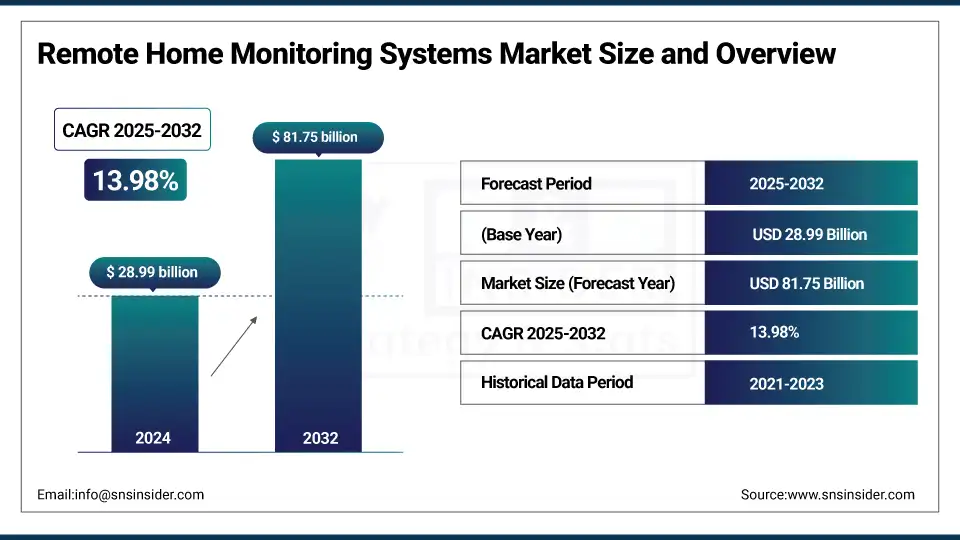

Remote Home Monitoring Systems Market was valued at USD 28.99 billion in 2024 and is expected to reach USD 81.75 billion by 2032, growing at a CAGR of 13.98% from 2025-2032.

The Remote Home Monitoring Systems Market is witnessing rapid growth due to increasing consumer demand for enhanced home security and automation solutions. Rising adoption of smart home devices, including sensors, alarms, and cameras, coupled with growing awareness about property and personal safety, is driving market expansion. A study published in the National Library of Medicine found that 68% of respondents reported using smart home devices, highlighting widespread consumer adoption.

To Get more information On Remote Home Monitoring Systems Market - Request Free Sample Report

Integration of advanced technologies such as AI, IoT, and cloud-based monitoring enables real-time surveillance, remote control, and predictive alerts, enhancing user convenience. Additionally, urbanization and smart city initiatives are fueling market adoption across residential and commercial sectors.

For instance, the U.S.-China Economic and Security Review Commission reported that Chinese government officials are leveraging smart cities technologies including IoT, mobile internet, cloud computing, and big data to expand, improve, and automate information collection and analysis, further demonstrating the push for integrated, technology-driven monitoring solutions. Rising disposable incomes and the need for energy-efficient, automated home management solutions are accelerating revenue growth globally.

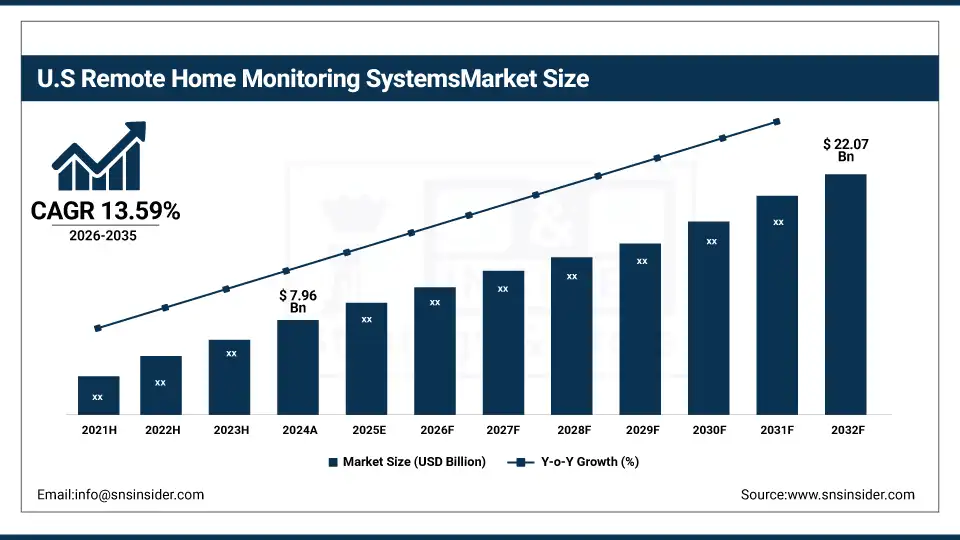

U.S. Remote Home Monitoring Systems Market was valued at USD 7.96 billion in 2024 and is expected to reach USD 22.07 billion by 2032, growing at a CAGR of 13.59% from 2025-2032.

The U.S. Remote Home Monitoring Systems Market is growing due to increasing demand for smart home security, adoption of IoT and AI-enabled devices, and rising awareness of property and personal safety. Convenience, real-time monitoring, and integration with mobile platforms are further driving widespread adoption across residential and commercial sectors.

Remote Home Monitoring Systems Market Dynamics

Drivers

-

Growing demand for continuous health monitoring driven by aging populations and rising chronic disease prevalence worldwide

The increasing global elderly population and rising cases of chronic illnesses such as diabetes, cardiovascular disorders, and respiratory conditions are fueling the adoption of remote home monitoring systems. In the United States, approximately 60% of adults have at least one chronic condition, and 40% have two or more, with chronic diseases accounting for about 90% of the nation’s USD 4.1 trillion in annual healthcare expenditures.

These technologies enable healthcare providers to track patients’ vital signs and health data in real time, ensuring timely interventions and reducing hospital readmissions. With healthcare systems under pressure to manage growing patient loads efficiently, remote monitoring provides a cost-effective solution that enhances patient outcomes. The growing focus on preventive care, early diagnosis, and long-term management of chronic diseases further accelerates demand for these systems across developed and emerging markets alike.

Restraints

-

Data privacy concerns and regulatory compliance complexities affecting system adoption across multiple markets

Remote home monitoring systems handle sensitive patient health data, making them vulnerable to cybersecurity threats, unauthorized access, and potential misuse. Stringent data protection regulations such as HIPAA in the U.S. and GDPR in Europe require strict compliance, adding operational complexity for providers. The challenge of ensuring secure transmission, storage, and sharing of data is compounded by varying regulatory requirements across regions. Healthcare providers must invest in robust encryption, authentication, and compliance measures, which increases operational costs. Persistent concerns about data breaches and patient confidentiality slow down user trust and widespread adoption, particularly among older or less tech-savvy populations.

Opportunities

-

Expanding adoption of AI-driven predictive analytics to improve health outcomes and personalize patient care plans

The integration of artificial intelligence into remote monitoring platforms is unlocking advanced capabilities for predictive health analytics and personalized care delivery. AI algorithms can analyze large volumes of real-time patient data to detect early signs of deterioration, predict potential health risks, and recommend timely interventions.

For instance, the U.S. Department of Veterans Affairs has collaborated with DeepMind to develop AI software that predicts acute kidney injury (AKI) in patients, utilizing 700,000 medical records to train AI algorithms on predicting AKI, a sudden kidney failure often linked with surgeries or infections. This enables proactive treatment strategies, reducing hospitalizations and improving patient outcomes. Personalized health plans based on continuous monitoring also enhance patient engagement and adherence. As AI technology matures, healthcare providers and payers increasingly see its potential to optimize care pathways, making it a key driver of market expansion in the coming years.

Challenges

-

Limited digital literacy among elderly patients and rural populations hindering effective system utilization and engagement

Many potential users of remote home monitoring systems, particularly elderly individuals and residents of rural areas, face difficulties in using digital health technologies. Limited familiarity with smartphones, wearable devices, and telemedicine applications reduces system effectiveness. Training programs and user-friendly designs are essential, but they require additional resources from healthcare providers. In rural regions, inconsistent internet connectivity further hampers adoption. These barriers can lead to poor compliance with monitoring protocols, reducing the accuracy of health data and diminishing the potential benefits of the system. Bridging this digital skills gap is critical for maximizing market growth potential.

Remote Home Monitoring Systems Market Segmentation Analysis

By Product

Security cameras dominated the market in 2024 with a 30% revenue share due to their effectiveness in real-time surveillance, crime deterrence, and evidence collection. Enhanced by AI-based analytics, remote access, and high-resolution imaging, they remain a primary choice for homeowners. Increasing affordability, easy installation, and integration with other home monitoring devices further boost demand, making them a critical component of comprehensive residential and commercial security systems globally.

Electronic and smart locks are projected to grow at an exceptional CAGR of 15.93% from 2025 to 2032, driven by rising adoption of keyless entry, mobile app-based control, and integration with broader smart home ecosystems. The increasing need for convenience, enhanced safety, and real-time access monitoring in residential and commercial spaces supports their rapid uptake. Growing IoT adoption and rising consumer preference for advanced, connected security solutions further accelerate their global market expansion.

By Sensor Type

Motion sensors led the market in 2024 with a 29% share owing to their vital role in detecting unauthorized movement and triggering alarms or camera activation. Their affordability, ease of integration, and reliability make them essential in modern security setups. Advancements in sensor accuracy, wireless technology, and energy efficiency have further solidified their adoption. Rising consumer demand for proactive intrusion detection drives their strong position in home monitoring solutions.

Environmental sensors are set to grow at the fastest CAGR of 16.84% between 2025 and 2032, fueled by rising awareness of hazards such as smoke, gas leaks, flooding, and poor air quality. Their ability to provide early alerts enhances safety in homes and businesses. Increasing integration with connected systems, combined with growing health and environmental safety concerns, is spurring adoption across residential, industrial, and commercial applications worldwide.

By Operating System

Android dominated the market in 2024 with a 53% revenue share, benefiting from its global smartphone leadership, affordability, and compatibility with diverse remote monitoring applications and IoT devices. Its open-source nature facilitates rapid innovation and integration with multiple hardware systems. Strong penetration in emerging and developed markets, combined with a wide range of cost-effective devices, continues to make Android the preferred platform for home monitoring solutions worldwide.

iOS is expected to grow at the fastest CAGR of 14.96% from 2025 to 2032 due to rising adoption of Apple’s smart home ecosystem, strong brand loyalty, and premium device performance. Seamless interoperability with HomeKit-enabled security devices and high data security standards attract affluent consumers. Increasing use of advanced monitoring apps optimized for iOS, coupled with growing smart home penetration in high-income households, supports robust growth in the coming years.

By Platform

The mobile segment dominated in 2024 with a 69% revenue share and is projected to grow at the fastest CAGR of 14.77% from 2025 to 2032 due to its central role in enabling real-time access, control, and monitoring of home security systems through smartphones and tablets. Increasing smartphone penetration, user-friendly mobile applications, and seamless integration with IoT-enabled devices drive adoption. The convenience of remote alerts, live video feeds, and instant notifications enhances user engagement, while continuous app innovations and 5G connectivity further accelerate demand across both developed and emerging markets.

Regional Analysis

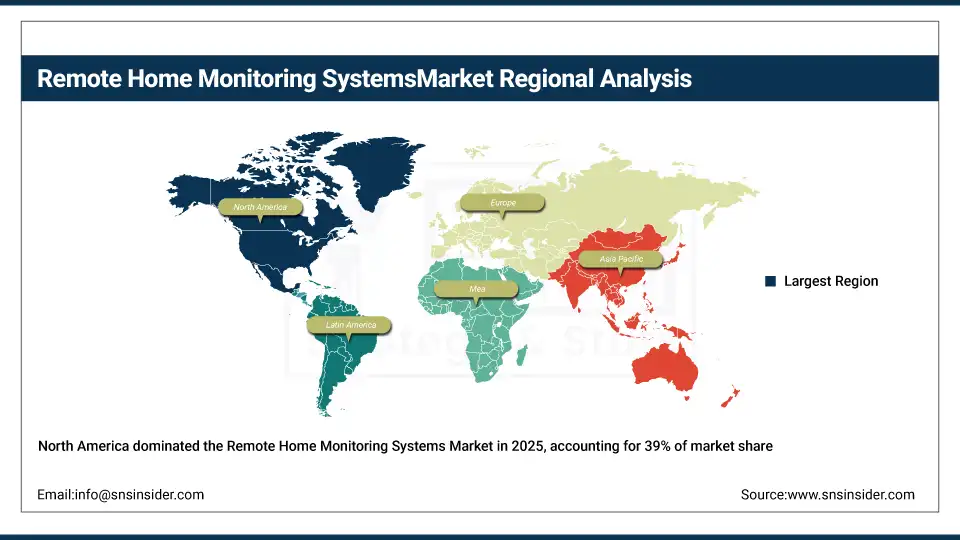

North America dominated the market in 2024 with a 39% revenue share due to advanced smart home adoption, strong presence of leading technology providers, and high consumer awareness regarding security solutions. Widespread broadband connectivity, robust IoT infrastructure, and supportive government initiatives for smart city development further strengthened regional growth. High disposable incomes and early adoption of innovative home monitoring technologies have made North America a key hub for market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States is dominating the Remote Home Monitoring Systems Market, driven by high smart home adoption, advanced IoT infrastructure, and strong consumer security awareness.

Asia Pacific is expected to grow at the fastest CAGR of 16.45% from 2025 to 2032 driven by rapid urbanization, rising disposable incomes, and increasing adoption of smart home technologies in emerging economies like China and India. Expanding internet penetration, government-led digital infrastructure projects, and growing safety concerns in densely populated cities are fueling demand. The presence of cost-effective device manufacturers and expanding e-commerce channels further accelerates market growth in the region.

China is dominating the Remote Home Monitoring Systems Market in Asia Pacific, driven by rapid urbanization, strong manufacturing capabilities, and widespread adoption of smart home technologies.

Europe’s Remote Home Monitoring Systems Market is driven by growing smart home adoption, stringent security regulations, and advanced IoT infrastructure. Rising consumer focus on safety, energy efficiency, and integration of AI-powered monitoring solutions further supports strong market expansion across the region.

The United Kingdom is dominating the Remote Home Monitoring Systems Market in Europe, supported by strong smart home adoption, advanced connectivity, and high consumer investment in security technologies.

The Middle East & Africa market is growing due to increasing urbanization, rising security concerns, and expanding smart infrastructure projects. Latin America is witnessing growth driven by improving internet penetration, affordable device availability, and rising adoption of connected home security solutions.

Remote Home Monitoring Systems Market Key Players

Honeywell International Inc., Ooma, Inc., IBM Corporation, SimpliSafe, Inc., General Electric Company, Bosch Security Systems, Inc., Schneider Electric S.E., Tyco International Ltd, Nortek Security & Control, LLC., Control4 Corporation, Apple Inc., Google Inc., Samsung Electronics Co. Ltd, Visonic Limited, Siemens Corporation, LOREX Technology Inc., ADT Inc., Vivint, Inc., Ring LLC, Brinks Home Security.

Recent Developments:

-

2025: Google Home app added full compatibility for Nest Protect smoke and CO alarms, enabling emergency alerts, safety checkups, and control without the standalone Nest app.

-

2024: ADT Inc. Introduced ADT+ platform in 2024, unifying professional monitoring, smart devices, Google Nest integration, remote assistance, and the new Trusted Neighbor feature for secure, time-limited home access.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 28.99 Billion |

| Market Size by 2032 | USD 81.75 Billion |

| CAGR | CAGR of 13.98% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sensor Type (Motion Sensors, Water Sensors, Glass Sensors, Door Sensors, Environmental Sensors, Others) • By Product (Electronic and Smart Locks, Alarms, Security Cameras, Security Solutions, DIY Home Security, Sensors, Detectors, Others) • By Platform (Mobile, Desktop) • By Operating System (Android, iOS, Windows) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., Ooma, Inc., IBM Corporation, SimpliSafe, Inc., General Electric Company, Bosch Security Systems, Inc., Schneider Electric S.E., Tyco International Ltd, Nortek Security & Control, LLC., Control4 Corporation, Apple Inc., Google Inc., Samsung Electronics Co. Ltd, Visonic Limited, Siemens Corporation, LOREX Technology Inc., ADT Inc., Vivint, Inc., Ring LLC, Brinks Home Security |

Frequently Asked Questions

Ans: North America dominated the market in 2024, holding a 39% share due to advanced smart home adoption and strong IoT infrastructure.

Ans: The mobile platform segment dominated with 69% share in 2024 and is expected to grow at the fastest CAGR of 14.77% by 2032.

Ans: Increasing demand for enhanced home security, automation, and AI- and IoT-enabled smart devices is the primary factor driving the market’s rapid expansion.

Ans: The market size of the Remote Home Monitoring Systems Market in 2024 was valued at USD 28.99 billion globally across residential and commercial applications.

Ans: The Remote Home Monitoring Systems Market is expected to grow at a CAGR of 13.98% during the forecast period from 2025 to 2032.

Get in Touch