Screw Compressor Market Report Scope & Overview:

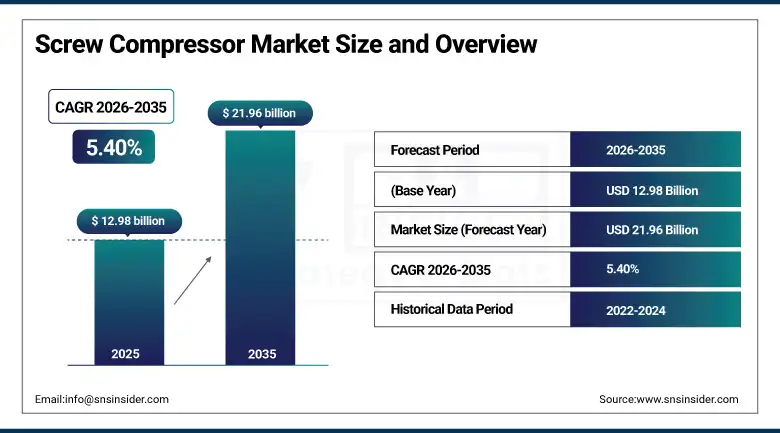

The Screw Compressor market was valued at USD 12.98 billion in 2025 and is expected to reach USD 21.96 billion by 2035, growing at a CAGR of 5.40% from 2026–2035.

Screw compressors are rotary positive-displacement compressors where gas compression is performed by the interaction of two helical rotors. They are extensively employed in several industries including manufacturing, oil & gas, food processing, healthcare, and energy sectors. Screw compressors offer reliable compressed air supply without pulsations. Such features have made screw compressors popular amongst industries needing constant supply of compressed air. The rise in demand for automated production systems is contributing to increased compressed air demand at manufacturing plants worldwide. Energy saving has become the main emphasis of innovations related to screw compressors among screw compressor manufacturers across the world. Application of variable speed drives has greatly contributed to energy savings especially during part load operation. Market growth is steadily increasing due to industrialization in Asia and infrastructure development in emerging markets. The current global inventory of screw compressors stands over 10 million units across various industrial applications.

Industrial automation deployments increased by 18% globally in 2025. This growth is creating proportionally higher demand for reliable, energy-efficient compressed air systems in automated manufacturing environments.

Market Size and Forecast

-

Market Size in 2026E: USD 13.68 Billion

-

Market Size by 2035: USD 21.96 Billion

-

CAGR: 5.40% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Screw Compressor Market - Request Free Sample Report

Screw Compressor Market Trends

-

The use of variable speed drives is becoming a norm in high-end screw compressor lines. The VSD helps save up to 30-50% energy when compared to fixed speed compressors.

-

The market for oil-free screw compressors is rising rapidly in the food, pharmaceuticals, and electronics industries due to strict contamination standards that make them a necessary feature.

-

The introduction of IoT-based predictive maintenance is revolutionizing fleet management of screw compressors. Systems monitor performance decline and predict failures to minimize downtime.

-

Screw compressor companies are looking into hydrogen compression as an area with untapped potential. Hydrogen-friendly screw compressors can be used to generate electricity via fuel cells.

-

Energy recovery is another innovative system now being deployed in screw compressors. Energy from the compression process is recycled to heat the building.

The U.S. Screw Compressor Market Outlook

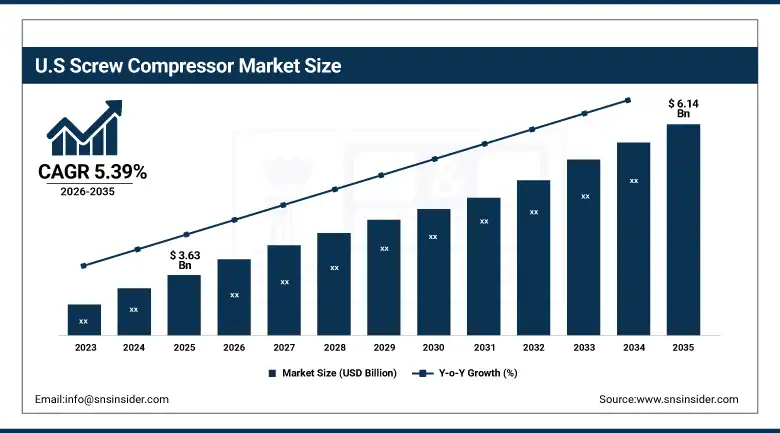

The U.S. Screw Compressor Market was valued at approximately USD 3.63 billion in 2025 and is expected to reach approximately USD 6.14 billion by 2035, growing at a CAGR of 5.39%.

The U.S. represents one of the most advanced screw compressor markets globally. It is fueled by a broad and diverse manufacturing industry base in the fields of automotive, aerospace, chemical engineering, and food processing. Manufacturing reshoring is driving demand for compressed air systems installations in various industries. The energy efficiency benefits associated with the Investment Tax Credit provided by the Inflation Reduction Act drive demand for energy-efficient compressor models throughout the country. The healthcare and pharmaceutical industries have the need for high-grade oil-free compressed air throughout their manufacturing process. Energy costs in the U.S. make variable speed drive screw compressors very attractive from a TCO perspective. Atlas Copco, Ingersoll Rand, and Kaeser Compressors dominate the market owing to well-established service networks. Aftermarket sales of replacement parts and service represent a lucrative source of revenue each year. New semiconductor and battery manufacturing plants create demand for large-scale compressed air installations.

U.S. manufacturing energy costs represent on average 30% of total production cost across industrial sectors. Screw compressor upgrades to variable speed drive technology demonstrate payback periods of 18 to 36 months across most industrial applications.

Screw Compressor Market Segment Analysis

-

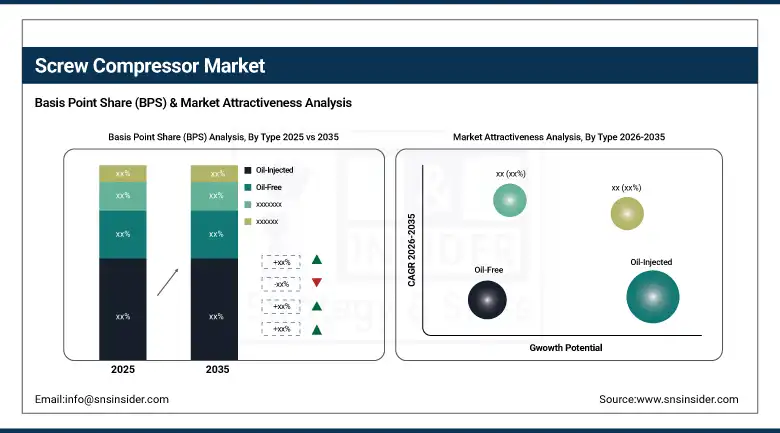

By Type: Oil-Injected had the largest market share of 62.37% in 2025 due to widespread usage in manufacturing industries, constructions, and power plants; Oil-Free is the fastest-growing segment at a CAGR of 6.12%, driven by the requirement of cleanliness in food manufacturing, pharma, and electronic components manufacturing.

-

By Screw Type: Twin-Screw had the largest market share of 57.21% in 2025 due to its robustness and efficiency in providing constant high-pressure output; Single-Screw is useful only in certain applications.

-

By Power Range: 101 – 500 kW had the largest market share of 54.85% in 2025 due to its wide applicability in industrial applications and relatively lower costs; Above 500 kW is the fastest-growing segment at a CAGR of 6.45%, driven by industrial, energy, and mining sector applications.

-

By End-Use: Manufacturing was the dominant end-use application due to the extensive requirement of compressed air in manufacturing processes; Oil & Gas is another major end-use application.

By Type, Oil-Injected dominates, Oil-Free is expected to grow fastest

In 2025, Oil-Injected Screw Compressors continued their market leadership with about 62.37% share in terms of revenue. The oil injection system acts as both a lubricating and cooling agent in the compression chamber. The ease of operation results in low production costs and high reliability with long-standing use in industrial operations. Oil-Injected Screw Compressors are versatile in meeting the needs of manufacturing, construction, and process industries. It is the least expensive compressed air solution for general industrial application. There is an enduring demand in the developing economies due to the importance placed on cost-efficiency. The widespread usage also leads to lucrative spare parts and service revenues.

The fastest-growing category is Oil-Free Screw Compressors with a compound annual growth rate of 6.12% up to 2035. The food and beverage industry uses Class 0 Oil-Free Air to ensure there is no product contamination. Oil-free air is compulsory in pharmaceuticals to guarantee purity throughout the entire production process. Electronics Manufacturing relies on Oil-Free Air to safeguard sensitive components during assembling. Increased adoption of Medical Gas Systems in the health industry increases demand for Oil-Free Screw Compressors. Stricter quality regulation in these sectors has increased pressure for oil-free air specifications to become mandatory.

By Power Range, 101–500 kW dominates, Above 500 kW is expected to grow fastest

The 101 to 500 kW power range retained the dominant position with approximately 54.85% of revenues in 2025. This range covers the majority of medium to large-scale industrial compressed air applications. It serves automotive assembly, food processing, chemical manufacturing, and general industrial compressed air systems. Compressors in this range offer the best balance between capacity, efficiency, and commercial price point. Variable speed drive retrofits are most commercially prevalent in this power range. Most major compressor manufacturers have the strongest product portfolios and dealer networks serving this segment.

Above 500 kW is the fastest-growing power range at a CAGR of 6.45% through 2035. Large-scale industrial plants, LNG terminals, gas processing facilities, and mining operations require high-capacity compression. New refinery construction in Asia and the Middle East is creating significant above-500-kW compressor demand. Petrochemical plant expansions require high-capacity oil-free gas compression for process applications. Data centre cooling and large HVAC systems increasingly use industrial-scale screw compression. The infrastructure investment cycle across developing economies is sustaining demand in this segment throughout the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

81.7% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

China |

52.4% |

|

Middle East & Africa |

Saudi Arabia |

31.6% |

|

Latin America |

Brazil |

43.3% |

North America Screw Compressor Market Insights

North America is the second-largest screw compressor market globally. The U.S. accounts for approximately 81.7% of North American revenues across all compressor segments. The region benefits from a large and diverse industrial manufacturing base creating consistent compressed air demand. Manufacturing reshoring following supply chain disruptions is creating new compressor installation opportunities across sectors. Energy efficiency incentives under the Inflation Reduction Act are accelerating variable speed drive adoption nationally. Canada contributes through its large oil sands, mining, and manufacturing compressed air requirements. The North American aftermarket for maintenance, parts, and retrofitting is a material and growing revenue stream. Pharmaceutical and semiconductor manufacturing growth in the U.S. is creating strong oil-free compressor demand. North America is expected to maintain its position as the second-largest regional market through 2035.

Europe Screw Compressor Market Insights

Europe is a technically advanced screw compressor market. Germany accounts for approximately 26.8% of European revenues as the region's largest industrial economy. European energy price volatility following geopolitical disruptions has intensified the focus on compressor energy efficiency. Atlas Copco and Kaeser, headquartered in Sweden and Germany respectively, maintain strong home market positions. EU industrial energy efficiency regulations are driving replacement of older fixed-speed compressors with VSD-equipped units. The pharmaceutical and food sectors are driving oil-free segment growth across Western European markets. Eastern European industrial expansion is creating new compressor demand across manufacturing and infrastructure.

Asia Pacific Screw Compressor Market Insights

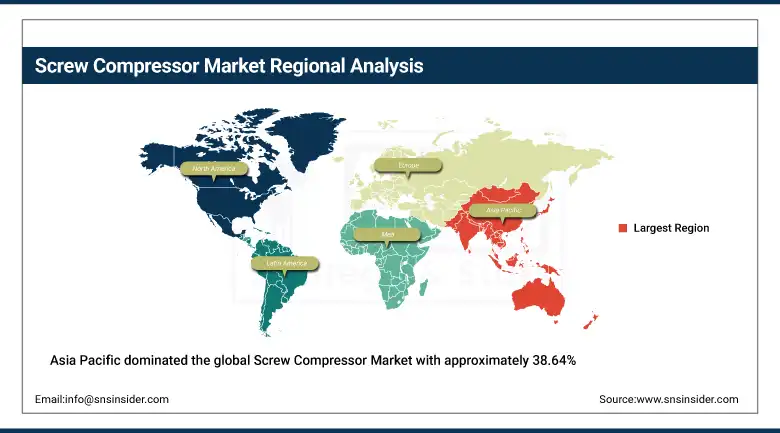

Asia Pacific dominated the global Screw Compressor Market with approximately 38.64% of revenues in 2025. China accounts for approximately 52.4% of Asia Pacific revenues through its vast industrial manufacturing base. Rapid industrialisation across India, Vietnam, Indonesia, and Thailand is creating strong sustained compressor demand. China's semiconductor, EV battery, and pharmaceutical manufacturing growth requires high-quality oil-free compressors. Japan and South Korea maintain sophisticated domestic compressor industries serving regional and global export markets. Government energy efficiency mandates across Asia are accelerating the upgrade cycle to variable speed drive technology. The region's manufacturing export competitiveness depends increasingly on compressed air system energy efficiency performance. Asia Pacific is expected to sustain its market leadership position throughout the 2026 to 2035 forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Screw Compressor Market Insights

MEA and Africa and Latin America represent some of the upcoming markets for screw compressors. Saudi Arabia represents the biggest revenue generator in MEA due to its oil and gas processing industries accounting for approximately 31.6% of the total MEA market. NEOM and the Saudi Vision 2030 industrial diversification programs have spurred demand in other areas besides oil and gas in the country. The UAE manufacturing and pharmaceutical industries have contributed to a steady rise in the number of oil-free screw compressors. Brazil generates the most revenues in Latin America due to its manufacturing and oil and gas industries, accounting for about 43.3%.

Market Dynamics

Growth Drivers: Industrial automation growth, energy efficiency mandates, and expanding manufacturing capacity in Asia are driving screw compressor market growth globally.

Industrial automation deployments are increasing compressed air demand across global manufacturing facilities consistently. Every automated production line, robotic assembly cell, and pneumatic tool system requires reliable compressed air supply. Energy efficiency mandates in Europe, North America, and Asia are driving replacement of older fixed-speed compressor units. Variable speed drive compressors reduce energy costs by 30 to 50% versus fixed-speed equivalents across comparable applications. Developing market industrialisation across Southeast Asia, India, and Africa is creating large new compressor installation demand. Oil and gas sector capital expenditure recovery is generating significant upstream and downstream compression equipment orders globally. Food and beverage sector expansion in developing economies is creating growing demand for oil-free compressor solutions. The semiconductor manufacturing boom is creating large-scale oil-free compressed air infrastructure investment across Asia Pacific.

Restraints: High equipment cost, complex maintenance requirements, and competition from alternative compression technologies are restraining screw compressor market growth.

Premium screw compressors constitute substantial capital expenditure by small industrial players. Cost of acquisition may become an issue in sensitive industrial applications in developing countries. Maintenance of compressors depends on the special skills to deal with complicated rotor geometry, which cannot always be found in all regions. Centrifugal and scroll compressors are competing in niche applications. Disruptions in supply chain impacting availability of rotor parts have resulted in uncertain delivery schedules. Unpredictable fluctuations in stainless steel and aluminium prices impact the cost structure of manufacturing compressors. Custom-designed high capacity compressors face lengthy delivery time. Upgrades of existing systems compete with purchasing new systems for limited capital.

Opportunities: Hydrogen compression applications, heat recovery integration, and IoT-enabled predictive maintenance create substantial screw compressor market growth opportunities.

The emergence of hydrogen economy is opening up new opportunities for screw compressors in the area of fuel cells and electrolysis technologies. Screw compressors that will be able to work with hydrogen are being developed by leading compressor manufacturers to meet the needs of the newly-emerging but strategically important market segment. The heat recovery systems designed to harvest the thermal energy from compression process improve the return on investment of the compressor replacement decision for commercial customers. Remote monitoring based on Internet of Things technologies opens the door for additional service revenue generation through predictive maintenance solutions. New markets in Sub-Saharan Africa, Southeast Asia, and Latin America present the opportunity to sell compressors to companies that need compressed air to support their operations. The development of pharmaceutical and food production industries in developing countries will drive the demand for oil-free compressors worldwide.

Recent Developments:

-

July 2025: Atlas Copco released its new generation of GA VSD+ compressors that featured 8% higher energy efficiency than its predecessor. This release was aimed at the industrial segment in terms of reducing costs for compressed air energy due to stringent efficiency standards.

-

June 2025: Kaeser Compressors introduced its SX 7.5 HP belt-driven rotary air compressor. It was made for industrial operations where reliable compressed air delivery is required.

-

2025: Ingersoll Rand extended its My Air service, which allowed for remote monitoring of its compressors’ performance, energy use, and preventive maintenance through the company’s global installed base.

-

2025: Gardner Denver introduced a new line of oil-free screw compressors aimed at the pharmaceuticals and food manufacturing industries that obtained ISO 8573-1 Class 0 oil-free air certification.

-

2025: Hitachi Industrial Equipment Systems commercialised its new hydrogen-compatible oil-free screw compressor for fuel cell vehicle refuelling station applications, entering the emerging clean energy compression market.

Screw Compressor Market Key Players are:

-

Atlas Copco AB

-

Ingersoll Rand Inc.

-

Kaeser Kompressoren SE

-

Gardner Denver (Ingersoll Rand)

-

Hitachi Industrial Equipment Systems

-

Siemens AG

-

Bitzer SE

-

Sullair LLC

-

Doosan Bobcat Inc.

-

Elgi Equipments Ltd.

-

Shanghai Screw Compressor Co. Ltd.

-

Hanbell Precise Machinery Co. Ltd.

-

Fusheng Industrial Co. Ltd.

-

GHH Compress

-

Kaishan Group

-

Mattei Compressors

-

CompAir (Gardner Denver)

-

Mann + Hummel Group

-

Parker Hannifin Corporation

-

SMC Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.98 Billion |

| Market Size by 2035 | USD 21.96 Billion |

| CAGR | CAGR of 5.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Oil-Injected, Oil-Free) • By Screw Type (Twin-Screw, Single-Screw) • By Power Range (Below 100 kW, 101–500 kW, above 500 kW) • By End-Use Industry (Manufacturing, Oil & Gas, Food & Beverage, Chemical, Healthcare, Energy & Power, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Atlas Copco AB, Ingersoll Rand Inc., Kaeser Kompressoren SE, Gardner Denver (Ingersoll Rand), Hitachi Industrial Equipment Systems, Siemens AG, Bitzer SE, Sullair LLC, Doosan Bobcat Inc., Elgi Equipments Ltd., Shanghai Screw Compressor Co. Ltd., Hanbell Precise Machinery Co. Ltd., Fusheng Industrial Co. Ltd., GHH Compress, Kaishan Group, Mattei Compressors, CompAir (Gardner Denver), Mann + Hummel Group, Parker Hannifin Corporation, SMC Corporation |

Frequently Asked Questions

Asia Pacific dominated with approximately 38.64% of revenues in 2025.

Oil-Injected dominated with approximately 62.37% of revenues in 2025.

Industrial automation growth and expanding manufacturing capacity in Asia are the primary drivers. Energy efficiency mandates are accelerating replacement of older fixed-speed compressors with VSD-equipped units.

The Screw Compressor Market was valued at USD 12.98 billion in 2025.

The Screw Compressor Market is expected to grow at a CAGR of 5.40% from 2026 to 2035.

Get in Touch