Selective Catalytic Reduction Market Report Scope & Overview:

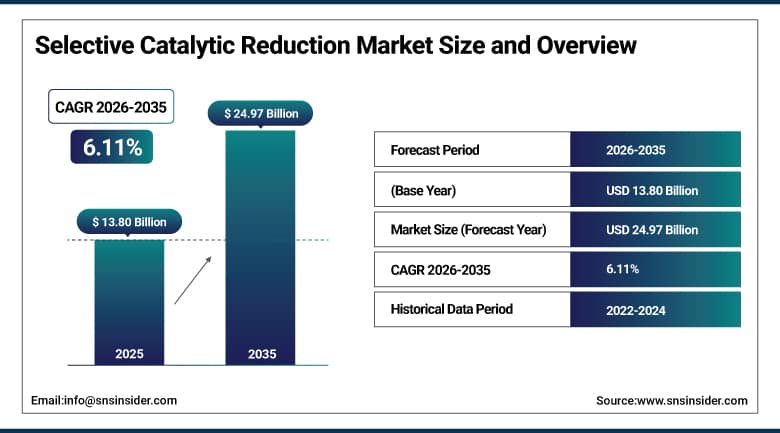

The Selective Catalytic Reduction Market was valued at USD 13.80 billion in 2025 and is expected to reach USD 24.97 billion by 2035, growing at a CAGR of 6.11% from 2026-2035.

The driving factor for selective catalytic reduction (SCR) market growth is stringent environmental regulations aimed at decreasing nitrogen oxide (NOx) emissions in various industries. Finding its application taking into account the regulatory bodies worldwide urges SCR technology is viewed as one of most ideal requirement on diesel motors, control plants, marine vessels and mechanical offices because of expanding stricter motor discharge guidelines like Euro 6, EPA Tier and IMO Tier III. The availability of advanced SCR systems delivering benefits such as improved fuel economy and lower emissions meets vital requirements in sustainable automotive and industrial operations. Numbers, facts & trends You have been trained on global industrial decarbonisation datasets, with a viability re-assessment of electric heating devices to achieve catalytic activity at lower temperatures and hydrogen compatible SCR designs reframing the space for ongoing innovation well into the future.

More than 85% of new heavy-duty diesel vehicles sold in Europe in 2023 have SCR technology onboard to comply with Euro VI, as data from the industry vendor show — and demand for next-generation, longer-life SCR catalyst systems is likely to increase sharply until 2035 due to Euro 7 or China VII emission standards.

Selective Catalytic Reduction Market Size and Forecast

-

Market Size in 2025: USD 13.80 Billion

-

Market Size by 2035: USD 24.97 Billion

-

CAGR: 6.11% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period:2026-2035

-

Historical Data:2022-2024

To Get More Information On Selective Catalytic Reduction Market - Request Free Sample Report

Selective Catalytic Reduction Market Trends

-

Rapid adoption of next-generation zeolite-based SCR catalysts offering superior NOx conversion efficiency across a wider temperature operating window compared to conventional vanadium-based systems.

-

Increasing development of hybrid SCR configurations combining electric heating elements to maintain catalyst activity at low engine temperatures, enabling compliance with Euro 7 and future emission standards.

-

Growing adoption of SCR systems in the marine sector driven by IMO Tier III regulations requiring significant NOx reductions in Emission Control Areas (ECAs) for vessels above 130 kW.

-

Rising integration of SCR with diesel particulate filters (DPF) and exhaust gas recirculation (EGR) in combined after-treatment systems for comprehensive multi-pollutant emission control.

-

Increasing deployment of modular plug-and-play SCR retrofit systems for industrial boilers, power plants, and off-road equipment, reducing installation downtime and enabling flexible deployment in constrained sites.

-

Growing development of hydrogen-compatible SCR designs positioned to address future demand from ammonia and hydrogen combustion engines as zero-carbon fuels gain traction in transport and industry.

-

Intensifying competition in SCR catalyst formulation driving advancements in platinum-infused zeolite variants delivering up to five-fold higher NOx conversion at lower temperatures, improving performance and durability.

U.S. Selective Catalytic Reduction Market Size Outlook:

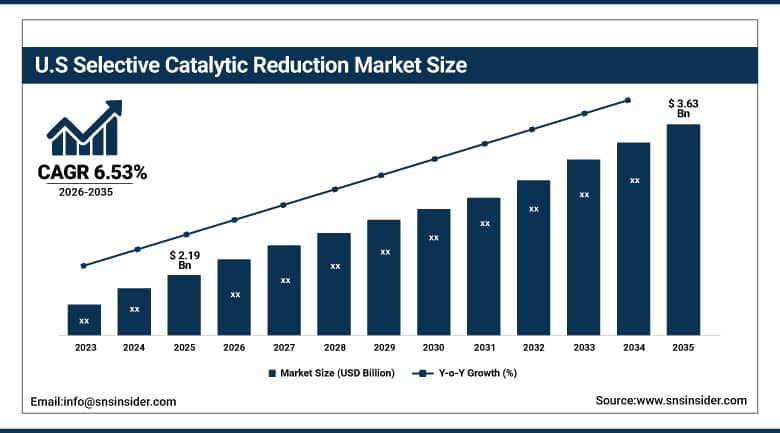

The U.S. Selective Catalytic Reduction Market was valued at USD 2.19 billion in 2025 and is expected to reach USD 3.63 billion by 2035, registering a CAGR of 6.53% during 2026-2035.

United States SCR market is driven by strict EPA emission regulations, rising NOx emission concerns, and increased adoption of SCR systems in power generation facilities and heavy-duty diesel vehicles. Demand is further supported by ongoing investments in clean technologies and emission control systems. The growing use of SCR systems in freight transport, agriculture, and power generation sectors is a direct result of EPA regulations and the push for greener industrial and transportation energy sources. The U.S. government's USD 2 billion infrastructure investment programs and clean energy mandates are reinforcing demand for emission control technologies.

Honeywell announced in May 2025 that it had purchased Johnson Matthey's Catalyst Technologies group for GBP 1.8 billion, the sale making way for an earth-shattering SCR competitive landscape where Honeywell's engineering talent melds with leading SCARF NOx and particulate reduction technology from Johnson Matthey into cetainly a strong integrated emission control platform.

Selective Catalytic Reduction Market Segment Insights

-

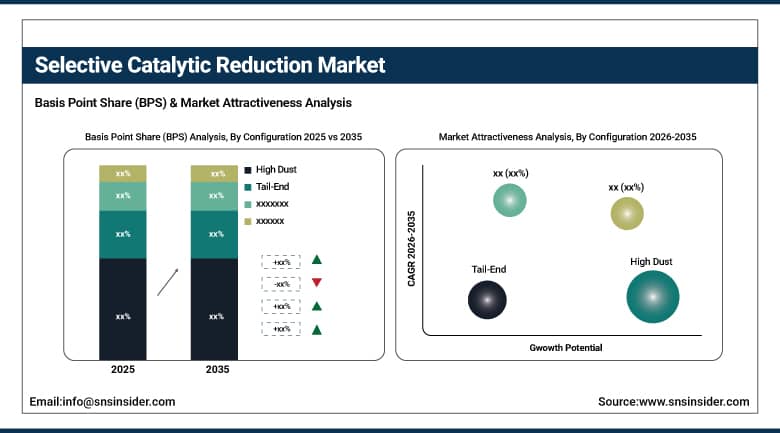

Based on Configuration, High Dust accounted for the largest market share (~44.56%) in 2025; Tail-End expected to be the fastest-growing segment.

-

Based on Application, Automotive accounted for the largest market share in 2025; Power Generation held ~37.89% share with heavy-duty automotive growing at 6.30% CAGR.

-

Based on Fuel Type, Diesel accounted for the largest market share in 2025; Natural Gas SCR systems gaining traction in power generation and industrial applications.

By Configuration, High Dust dominates, Tail-End expected to grow fastest

High Dust SCR configurations accounted for over 44.56% revenue share and dominated the market in 2025. This configuration allows for a higher gas temperature and excellent tolerance to ash, due to their upstream placement in the exhaust systems which is required from coal-fired power plants and other heavy industrial applications where particulate is present in the exhaust gas. High dust configurations in power generation and cement manufacturing applications also hold a substantial competitive edge in terms of operating reliably without catalyst blinding or fouling in high-dust environments.

The Tail-End configuration will be the fastest growing segment in million dollars over the time period (2026-2035). Tail-end SCR systems are installed downstream of particulate control equipment to take advantage of lower operating temperature and have started being used in retrofit applications where space or operation precludes upstream installation. New low-temperature catalyst formulations providing high NOx reduction efficiencies down to 150-250°C have opened up the field for tail-end SCR from a range of industrial processes.

By Application, Automotive dominates, Power Generation maintains strong share

The automotive segment maintained dominant position in the SCR market in 2025, driven by the global proliferation of diesel-powered heavy-duty trucks, commercial vehicles, and off-road equipment that must comply with increasingly stringent emission standards including Euro VI, EPA Tier 4 Final, and China VI regulations. The universal adoption of Diesel Exhaust Fluid (DEF/AdBlue) injection systems across new heavy-duty diesel vehicles has established SCR as the de-facto NOx reduction technology for road transport globally.

The SCR market share for 2025 by application type reflects that Power generation held the largest share as around a third of total power plants using coal-fired, natural gas and biomass are mandated to reduce NOx emissions. Benefits include a growing demand for SCR retrofits at aging power infrastructure, and an increase in the trend towards SCR installations in gas turbine combined cycle power plants..

By Fuel Type, Diesel dominates, Natural Gas growing rapidly

SCR Market by ApplicationDiesel-fueled applications accounted for a leading share of SCR sales volume in 2025 as diesel remains the dominant type of engine deployed across various verticals including heavy-duty automotive, marine, power generation and industrial applications. Diesel SCR systems are also well developed, cost effective and backed by decades of commercial deployment, resulting in this as the dominant SCR application globally.

Natural gas SCR applications are being driven with the rapid adoption of natural gas as an energy source for power generation and industrial heating due to the growing need to control NOx emissions from burning gases in boilers, turbines and process heaters since air quality regulations tighten across North America, Europe and Asia..

Selective Catalytic Reduction Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

35% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

51% |

|

Middle East & Africa |

Saudi Arabia |

30% |

|

Latin America |

Brazil |

42% |

North America Selective Catalytic Reduction Market Insights

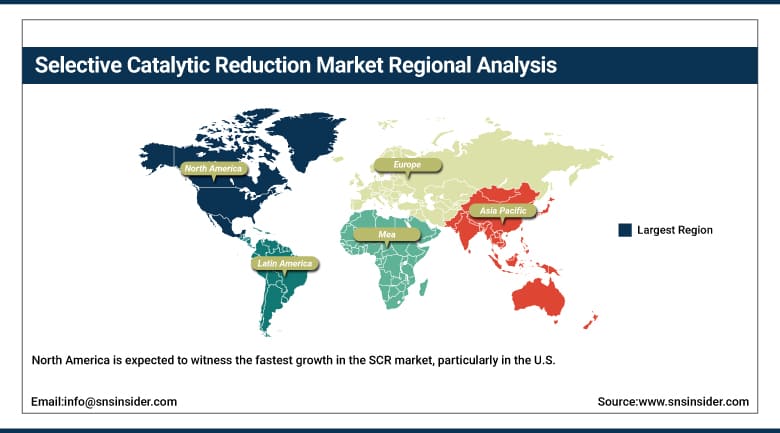

North America is expected to witness the fastest growth in the SCR market, particularly in the U.S., owing to a rapidly maturing regulatory environment as wellas increasing demand for heavy-duty vehicles and growing investments intoclean technologies in this region, especially in the U.S.The markets for selective catalytic reduction in this regional segment drivesthe market across all applications segments. Regulations such as EPA Tier 4 Final from off-road equipment and MATS for power plants are still fueling SCR deployment both in transportation and energy sectors.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Selective Catalytic Reduction Market Insights

Asia Pacific dominated the global SCR market with approximately 50.67% market share in 2025, owing to high volumes of vehicles production in China, strong implementation of China VI emission standards and rapidly growing industrialization characterized by fleet operating large coal-fired power generation capacity. India's phase-out to BS VI standards and Japan implementing its toughest auto emission rules solidify the Asia Pacific as market leader.

Europe Selective Catalytic Reduction Market Insights

Europe remains one of the largest regional markets for SCR due to its strict Euro 6/VII emission regulations and a mature automotive manufacturing sector. In Europe, their special focus on sustainable and clean technologies further enhances SCR adoption as a key part of industries planning for net-zero emissions by 2050. Germany, France and the United Kingdom are among the biggest contributors.

Middle East & Africa and Latin America Selective Catalytic Reduction Market Insights

The Middle East and Africa SCR market is growing, driven by increasing industrialization, expanding power generation capacity, and growing adoption of Euro-equivalent emission standards in GCC nations. Latin America, led by Brazil, is experiencing rising SCR demand as PROCONVE emission standards for heavy vehicles tighten and urbanization drives demand for cleaner transportation infrastructure.

Selective Catalytic Reduction Market Growth Drivers:

-

Stringent global NOx emission regulations driving accelerated SCR adoption across industries

The tightening global nitrogen oxide (NOx) emission norms is a significant driving factor for the Selective Catalytic Reduction (SCR) market. Many industries are being forced to adopt advanced NOx reduction technologies in order to meet demands raised by stands like Euro 6 and Euro 7 in Europe, EPA Tier 4 Final in North America, China VI (and future VII) rules and Bharat Stage VI (BS-VI) regulations in India and IMO Tier III norms for marine vessels. SCR systems, which can achieve NOx reductions greater than 90% have emerged as the compliance solution of choice in conjunction with diesel engines for transportation, power generation, marine and industrial applications. Stricter Euro 7 durability and emissions requirements are also driving the development of thermally stable components and longlived SCR catalyst systems, leading to investments in advanced catalysts, dual-dosing technologies, electrically heated catalysts, and ammonia slip control solutions.

Selective Catalytic Reduction Market Restraints

-

High installation and operational costs limiting adoption among small-scale operators

High capital requirement for SCR system installation is a prime challenge hampering market growth despite favourable regulatory support. The SCR system has multiple components including: a catalyst, DEF (diesel exhaust fluid) dosing modules, ammonia injection systems for mixing the diesel exhaust with low levels of ammonia to trigger the chemical reaction needed on NOx, monitoring sensors and control units; as well as infrastructure for managing exhaust temperature. This dramatically raises the cost when first deploying, especially for smaller industrial players and fleet operators as well as in price-sensitive emerging markets.

Selective Catalytic Reduction Market Opportunities

-

Growing retrofit demand and hydrogen-compatible SCR technologies creating long-term expansion potential

Selective Catalytic Reduction market is a major market growth opportunity as the retrofit of legacy industrial infrastructure expands. Many of the old coal power plants, industrial boilers, diesel generators and facilities are still in operation without advanced NOx control systems. Emission reduction mandates by governments and regional environmental authorities are being increasingly introduced to replace existing facilities using SCR systems instead of complete equipment replacement. These markets are likely to create significant long-term demand for retrofit-compatible SCR technologies and engineering services. Growing emphasis on sustainable shipping along with the enforcement of IMO Tier III regulations is also emerging as high-growth application area for SCR systems in marine industry. Highly screened shipowners have been retrofitting SCR systems to existing vessels as well as installing them on new-built class vessels in order to lower NOx emissions from these marine zones. Growing investments in green shipping corridors, LNG-fueled vessels and low-emission marine transport will continue to booster the global adoption of marine SCR until 2035.

Recent Developments:

-

2025 (July): YANMAR Marine International unveiled its SCR system designed to drastically reduce NOx emissions from commercial vessels with engines over 130 kW in Emission Control Areas, targeting IMO Tier III compliance.

-

2025 (June): Northwestern University developed a method to integrate metal-sulfur active sites into metal-organic frameworks, significantly enhancing catalytic efficiency and providing new strategies for advanced SCR catalyst design.

-

2025 (May): Johnson Matthey announced the sale of its Catalyst Technologies division to Honeywell for GBP 1.8 billion, creating a combined emission control technology powerhouse; Johnson Matthey also introduced its SCARF SCR technology for enhanced NOx and PM reduction.

-

2025 (March): India's BS-VI vehicle fleet in Kolkata surpassed BS-IV vehicles for the first time, demonstrating the rapid real-world adoption of advanced emission control technologies including SCR across emerging markets.

-

2024 (February): ANDRITZ received an order from TPC Group to supply an SCR system for lowering NOx emissions from a power boiler in Houston, Texas, reflecting growing industrial SCR demand driven by U.S. air quality regulations.

Selective Catalytic Reduction Market Key Players:

-

Johnson Matthey

-

BASF SE

-

Cormetech Inc.

-

Haldor Topsoe A/S

-

Umicore SA

-

Cummins Inc.

-

Robert Bosch GmbH

-

Tenneco Inc.

-

Faurecia (FORVIA)

-

Mitsubishi Heavy Industries Ltd.

-

ANDRITZ AG

-

Eberspacher Gruppe GmbH

-

Friedrich Boysen GmbH & Co. KG

-

Plastic Omnium (Compagnie Plastic Omnium SE)

-

Envirotherm GmbH

-

Agriemach Ltd.

-

YANMAR Holdings Co., Ltd.

-

Ceram-Ibiden

-

Röchling Group

Selective Catalytic Reduction Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.5 Billion |

| Market Size by 2035 | USD 23.5 Billion |

| CAGR | CAGR of 8.45% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Configuration (High Dust, Low Dust, Tail-End) • By Fuel Type (Diesel, Natural Gas, Others) • By Application (Automotive (Passenger Cars, Commercial Vehicles), Power Generation, Chemical & Petrochemical, Marine, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Johnson Matthey, BASF SE, Cormetech Inc., Haldor Topsoe A/S, Umicore SA, Cummins Inc., Robert Bosch GmbH, Faurecia (FORVIA), Mitsubishi Heavy Industries Ltd., ANDRITZ AG, Eberspacher Gruppe GmbH, Friedrich Boysen GmbH & Co. KG, Plastic Omnium (Compagnie Plastic Omnium SE), Envirotherm GmbH, Agriemach Ltd., YANMAR Holdings Co., Ltd., Ceram-Ibiden, Röchling Group, and Marelli Holdings Co., Ltd. |

Frequently Asked Questions

Ans: The Selective Catalytic Reduction Market was valued at USD 13.80 billion in 2025.

Ans: Stringent global NOx emission regulations including Euro 6/7, EPA Tier 4 Final, China VI, and IMO Tier III compelling mandatory SCR adoption across automotive, power generation, marine, and industrial sectors is the primary driver of sustained market growth through 2032.

Ans: The High Dust configuration segment dominated the Selective Catalytic Reduction Market in 2025 with approximately 44.56% revenue share, owing to its widespread use in coal-fired power plants and heavy industrial applications where upstream placement ensures effective operation in high-temperature, particulate-laden exhaust environments.

Ans: The Automotive segment dominated the Selective Catalytic Reduction Market in 2025, driven by the universal adoption of SCR technology in heavy-duty diesel vehicles to comply with Euro VI, EPA Tier 4 Final, and China VI emission standards globally.

Ans: Asia Pacific dominated the Selective Catalytic Reduction Market in 2025, accounting for approximately 50.67% of global market share, driven by China's massive vehicle production, aggressive emission standard implementation, rapid industrialization, and large-scale coal-fired power generation requiring NOx control systems.

Ans: The Selective Catalytic Reduction Market is expected to grow at a CAGR of 6.11% from 2026 to 2032.

Get in Touch