Semiconductor Fabless Market Size & Trends:

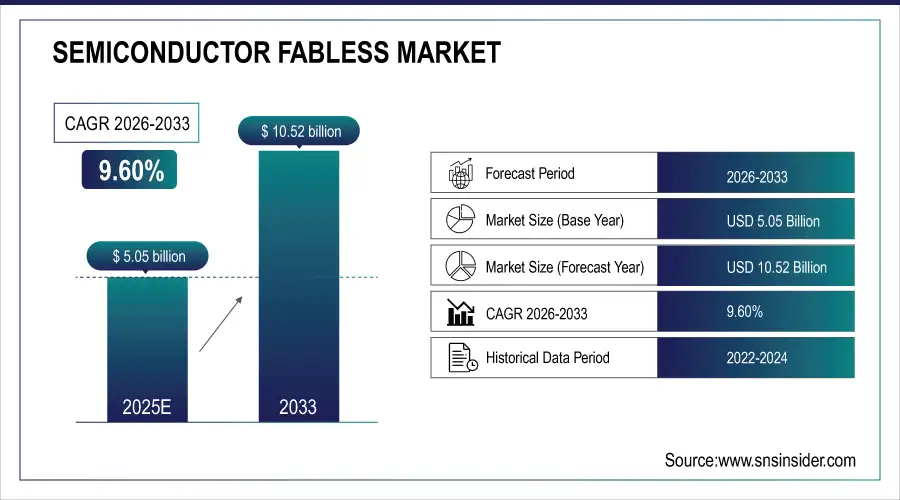

The Semiconductor Fabless Market Size was valued at USD 5.05 Billion in 2025E and is expected to reach USD 15.17 Billion by 2035 and grow at a CAGR of 9.60% over the forecast period 2026-2035.

Increasing demand for fabless semiconductor is attributed to the growing usage of advanced semiconductor devices in consumer electronics, healthcare, and automotive electronics. Improving manufacturing techniques for semiconductors are also working in favor of the growth of the semiconductor market. As the semiconductor demand is rising due to increasing digital transformation in industries, it is a key growth engine for the market.

Semiconductor Fabless Market Size and Growth Projection:

-

Market Size in 2025E: USD 5.05 Billion

-

Market Size by 2035: USD 15.17 Billion

-

CAGR: 9.60% from 2026 to 2035

-

Base Year: 2025E

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

Semiconductor Fabless Market Trends Highlights:

-

Fabless companies focus on chip design and sales while leaving manufacturing to foundries, enabling innovation and reducing capital expenditure

-

The US is projected to triple semiconductor manufacturing capacity by 2032 and account for 28% of global capital expenditures on semiconductor manufacturing

-

New fabless ventures such as iVP Semiconductor in India target domestic markets for power electronics, EV charging, and renewable energy with government partnerships and funding

-

Expansion of IoT applications across smart homes, industrial automation, and wearables is boosting demand for integrated, low-power, and efficient semiconductor components

-

Large-scale 5G rollouts are driving growth in high-speed, low-latency semiconductors including RF components, transceivers, and network processors

-

Increasing design complexity, reliance on third-party foundries, supply chain vulnerabilities, intense competition, and regulatory hurdles are constraining growth and innovation

Get More Information on Semiconductor Fabless Market - Request Sample Report

The fabless semiconductor market is an extremely important part of the semiconductor industry because here companies only design and sell chips and leave manufacturing to specialized foundries. This business model departs from the traditional IDM way of doing things: Fabless companies are free to innovate and reduce capital expenditures tied to ownership and operating fabrication facilities. With technological advancement continuing to fill every nanosecond, the fabless model has come to the fore especially in the development of next-generation chips that run different applications involving consumer electronics, automobile, industry, telecom, and medical sectors.

July 2024 Semiconductor veteran starts fabless chip company with design & testing facility The semi-fabless chip startup is aimed exclusively at the domestic power electronics, renewable energy, electric vehicle charging, and battery management market for India. Raja Manickam, who has just entered into industry life after serving as the CEO of Tata Electronics' OSAT unit, leads the new venture. The company plans to set up in Chennai a 20,000 sq. Ft chip and module testing facility in partnership with Tamil Nadu Industrial Development Corporation, or TIDCO, according to sources. This facility will be available to all other semiconductor companies also.

U.S. Semiconductor Fabless Market Size Outlook

The U.S. Semiconductor Fabless Market size is projected to grow from USD 3.03 Billion in 2025E to reach USD 9.10 Billion by 2035. Growth is driven by relentless demand for AI and HPC chips, the proliferation of edge computing and IoT devices, sustained innovation in data center GPUs and CPUs, and the strategic dominance of U.S.-based design houses in cutting-edge process nodes and advanced chip architectures.

Semiconductor Fabless Market Drivers:

-

IoT Expansion to Boost Demand for Semiconductor Fabless Components

The adoption of Internet of Things devices will be highly supportive of the growth of semiconductor components. Varying from smart home appliances to industrial automation and wearables, many IoT applications require different semiconductor components. Thus, a rapidly growing requirement for highly integrated, efficient chips in the chip industry for IoT applications such as low-power microcontrollers, sensors, and communication modules are one of the major contributors in driving the market. Chennai, Jul 6, 2024 Fabless semiconductor startup iVP Semiconductor Pvt Ltd is scouting for a location to set up a production test facility as part of its efforts to manufacture semiconductor chips for the domestic market, said a senior official. Co-founder and CEO Raja Manickam said the company has raised USD 5 million in pre-series A funding to help it advance its growth plans.

-

5G Expansion Fuels Semiconductor Fabless Market Growth

The actual driving factor in this growth is the large-scale rollout of 5G networks. This technology needs semiconductors with highly advanced speed factors for data transmission, low latency, and enhanced connectivity. Companies around the world in the semiconductor sector design advanced RF components, high-bandwidth transceivers, and network processors that are necessary in any successful deployment of 5G infrastructure. In July 2024, A leader in advanced 5G and 4G semiconductor solutions partnered with Kyocera to jointly develop a 5G reference platform to support customer premise equipment (CPE) and fixed wireless access (FWA) devices. It includes a GCT 5G chipset integrated with a Kyocera 5G mmWave antenna module, through which Kyocera can develop products and GCT can develop 5G mmWave CPE devices.

Semiconductor Fabless Market Restraints:

-

Challenges Hindering Semiconductor Fabless Market Growth

There is the increasing complexity and cost of designing semiconductors, which is a major challenge to market growth. Companies in this space also are highly reliant on third-party foundries, which, by itself, creates vulnerabilities in the supply chain and potential disruptions from constrained foundry capacity or geopolitical issues that impact international trade. The rapid pace of technological development has also led to the demand for continuous innovation, which calls for challenges for companies that cannot compete against changing trends and standards. The aspects may call for difficulty in the environment of semiconductor fabless companies, thereby limiting their scope for growth and capturing emerging opportunities.

Quality assurance issues and delivery delays would manifest as a result of limited control over manufacturing. Healthy competition puts mounting pressure on margins thus shaving off market shares. Competition against heavy regulations complicates operations and ponders costs to transactions while fluctuating economies reduces outlays in what can be core sectors lowering demand for semiconductor technologies.

Semiconductor Fabless Market Segment Analysis:

By Type

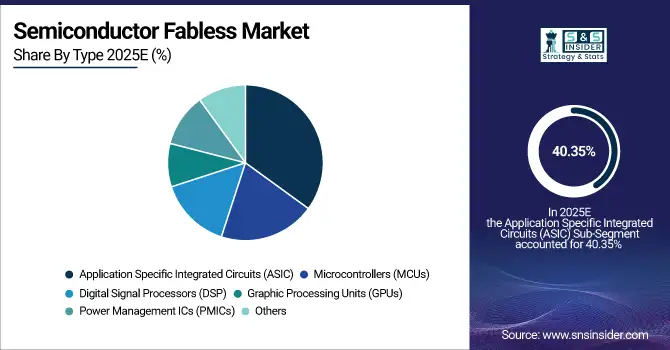

In 2025, the ASIC market had the highest share, which is nearly 40.35% of the revenues globally. It is because this kind of industry calls for custom-made products, and along with these, technologies such as AI, ML, and 5G are developing, due to which heavy investments in ASIC development take place by sectors like automotive, consumer electronics, and telecommunications. Cyient is setting up a wholly-owned subsidiary in July 2024 that will help improve its capabilities in the areas of ASIC turnkey design and manufacturing on a fabless model, with an eye on analog mixed-signal chips. Investment: shares of Cyient closed at ₹1,836.30 on the BSE, up by 3.41%. The new subsidiary would focus on delivering specialized turnkey ASIC designs and chip sales, thus enabling Cyient to adapt itself to the market cycles and meet the industry's technology and capital needs.

The GPUs segment is expected to display strong CAGR growth of 10.56% from 2025 to 2032. This can be mainly attributed to the increasing requirements for high-performance computing and graphics rendering. Today, GPUs have moved beyond their original uses in gaming to become omnipresent in applications such as artificial intelligence, data centers, and cryptocurrency mining. The more data-intensive nature of workloads will compel increasingly strong GPUs to handle huge volumes of information. Further fuelling demand, technology trends include gaming, virtual reality, and augmented reality. Users want immersive experiences in all these technologies, with advanced graphical capabilities being the only possibility. Actions Technology, today announced that it, a fabless semiconductor company focused on low-power AIoT solutions, has integrated VeriSilicon's power-efficient and feature-rich 2.5D Graphics Processor Unit IP into its family of integrated dual-mode Bluetooth smartwatch SoCs, ATS3085S, and ATS3089.

By End User

In 2025, consumer electronics will lead the market with an account of 37.78% of revenue of the world with the increased demand of advance and feature-rich electronic devices. With the latest evolutions in technology, consumer electronics such as smartphones, tablets, smartwatches, and smart home devices are increasing the need for sophisticated and more efficient semiconductor solutions. The trend has also picked up with IoT devices and wearable technology, increasing the demand for specific semiconductor solutions. Many semiconductor companies are developing new components for consumer products, thereby driving the growth of the industry; consumers highly have a desire to use products with modern technology.

Automotive is expected to be the fastest-growing segment, with a CAGR of 10.41% from 2025 to 2032, due to the adoption of technologies such as advanced driver-assistance systems (ADAS) electric vehicles (EVs), and autonomous driving technologies within the automotive industry, thereby significantly raising demand for advanced semiconductor solutions that facilitate these disruptive and emerging innovations. Jio Platforms is foraying into the two-wheeler technology platform market in India's automotive sector by forming an alliance with Taiwanese fabless semiconductor firm MediaTek. On Thursday, the Taiwan-based chipmaker and the wholly-owned subsidiary of Jio Platforms, JioThings, launched their joint venture-an IoT platform for the electric two-wheeler market that will have a Smart Digital Cluster and a Smart Module.

Semiconductor Fabless Market Regional Analysis:

Asia-Pacific Semiconductor Fabless Market Trends:

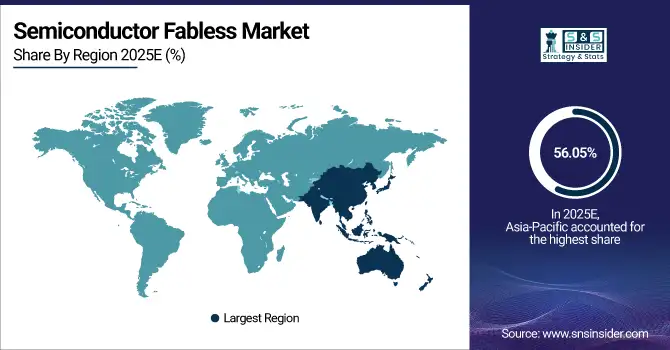

Asia Pacific dominated the global semiconductor fabless market share in 2025 with 56.05%. The growth in this region is further accelerated due to high stress on electronics manufacturing and innovative technological advancements. China, South Korea, Japan, and India account for a large percentage of these fabless companies and end-use industries within the region. Growing consumer electronics, rising IoT applications, and coming of 5G technology are driving the demand for innovative semiconductor components in the region. Investment will be required in a very significant manner in R&D and skilled workforce to grow the country's semiconductor design. Growth will come from emerging technologies 5G and AI, in growing importance in addition to initiatives to promote domestic capabilities in semiconductor manufacturing.

Need any customization research on Semiconductor Fabless Market - Enquiry Now

North America Semiconductor Fabless Market Trends:

North America accounted for a significant share of the global semiconductor fabless market in 2025. The growth is driven by advanced technology adoption, strong R&D infrastructure, and the presence of leading fabless companies in the U.S. The region focuses on high-performance computing, AI, and automotive semiconductor solutions. Investments in innovative chip design, AI integration, and next-generation communication technologies, including 5G and edge computing, are accelerating market growth.

Europe Semiconductor Fabless Market Trends:

Europe holds a notable share of the global semiconductor fabless market. Growth is supported by strong automotive, industrial, and telecommunications sectors, along with government initiatives promoting semiconductor innovation. The demand for energy-efficient and high-performance semiconductor components, AI-driven applications, and increasing IoT deployment is driving the fabless industry. Collaborative R&D and strategic partnerships enhance Europe’s technological capabilities.

Latin America Semiconductor Fabless Market Trends:

Latin America’s fabless market is gradually expanding due to increasing consumer electronics consumption, automotive electronics growth, and government initiatives supporting innovation. Companies are focusing on AI, IoT, and telecommunications solutions. Investment in R&D, talent development, and partnerships with global semiconductor firms are driving regional growth.

Middle East & Africa Semiconductor Fabless Market Trends:

The Middle East & Africa region is witnessing steady growth in the semiconductor fabless market. Expansion is fueled by increasing electronics adoption, smart city initiatives, and infrastructure development. Investments in skilled workforce, technology transfer, and R&D are critical to support domestic semiconductor design and production. Demand for IoT, AI-enabled devices, and telecommunication upgrades including 5G is rising.

Key Semiconductor Fabless Companies are:

-

Qualcomm (Snapdragon 8 Gen 1, Snapdragon 888)

-

NVIDIA (GeForce RTX 3080, Jetson Xavier NX)

-

Broadcom (BCM43684 Wi-Fi Chip, BCM5880 Secure Microcontroller)

-

AMD (Advanced Micro Devices) (Ryzen 5000 Series, EPYC 7003 Series)

-

MediaTek (Dimensity 1200, Helio G95)

-

Texas Instruments (LMX2572 Frequency Synthesizer, Sitara AM57x Processor)

-

Marvell Technology (Octeon TX2 Processor, 88Q2112 Ethernet Switch)

-

Xilinx (now part of AMD) (Zynq UltraScale+ MPSoC, Kintex UltraScale FPGA)

-

Skyworks Solutions (SKY85310-11 Power Amplifier, SKY66420-21 RF Front-End Module)

-

Cirrus Logic (CS42L83 Audio Codec, CS47L35 Audio Hub)

-

Infineon Technologies (AURIX TC3xx Microcontroller, EiceDRIVER Gate Driver)

-

Analog Devices (ADXL345 Accelerometer, ADAU1701 Audio Processor)

-

NXP Semiconductors (LPC5500 Microcontroller, i.MX 8M Application Processor)

-

STMicroelectronics (STM32F4 Microcontroller, LSM6DSO Inertial Measurement Unit)

-

Dialog Semiconductor (now part of Renesas) (DA14531 Bluetooth Low Energy SoC, SmartBond Bluetooth Solutions)

-

Silicon Labs (EFR32MG21 Wireless Gecko, Si5351 Clock Generator)

-

Lattice Semiconductor (MachXO3 FPGA, ECP5 FPGA)

-

Inphi (now part of Marvell Technology) (800G ZR Optical DSP, 100G CDR IC)

-

Rambus (Rambus Cryptographic Engine, Rambus DDR4 Memory Controller

-

ON Semiconductor (NCP81174 Power Management IC, FUSB302 USB Type-C Controller)

Semiconductor Fabless Market Competitive Landscape:

VanEck, established in 1955 by John van Eck, is a privately held investment management firm headquartered in New York City. The firm specializes in exchange-traded funds (ETFs), mutual funds, and separately managed accounts, with a focus on innovative investment strategies across various asset classes. As of March 2024, VanEck manages approximately USD 101.9 billion in assets under management (AUM)

-

In August 2024, VanEck, a global investment management firm, introduced the VanEck Fabless Semiconductor ETF (SMHX), the newest addition to its lineup of thematic equity ETFs. SMHX targets fabless semiconductor companies that emphasize design and R&D rather than manufacturing.

Mindgrove Technologies, founded in 2021 by Shashwath T.R. and Sharan Srinivas J., is a Chennai-based fabless semiconductor startup incubated at IIT Madras. The company specializes in designing secure, scalable, and cost-effective System-on-Chips (SoCs) tailored for applications in IoT, automotive, consumer electronics, and defense sectors. Their flagship products include the "Secure IoT" and "Vision SoC" chips, developed using India's first industrial-grade RISC-V core, Shakti. Mindgrove has secured funding from investors such as Sequoia Capital India and Mela Ventures, and has partnered with Bosch Global Software Technologies to co-develop advanced SoC solutions.

-

In May 2024, Mindgrove Technologies, a fabless semiconductor startup supported by Peak XV Partners, launched India’s first commercial high-performance system on chip (SoC) called Secure IoT.

Larsen & Toubro Limited (L&T), established in 1946, is a prominent Indian multinational conglomerate headquartered in Mumbai, Maharashtra. The company specializes in engineering, construction, manufacturing, information technology, and financial services, operating across over 50 countries. L&T is listed on the Bombay Stock Exchange and the National Stock Exchange of India, and is a constituent of the BSE SENSEX and NSE NIFTY 50 indices.

-

In September 2024, Larsen & Toubro Ltd. intends to invest more than USD 300 million in a fabless chip company, with plans to design 15 products by the end of the year and begin sales in 2027. This initiative aligns with India's efforts to enhance domestic semiconductor capacity and decrease imports, backed by government subsidies.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 5.05 Billion |

| Market Size by 2035 | USD 15.17 Billion |

| CAGR | CAGR of 9.60% From 2026 to 2035 |

| Base Year | 2025E |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Microcontrollers (MCUs), Digital Signal Processors (DSP), Graphic Processing Units (GPUs), Application Specific Integrated Circuits (ASIC), Power Management ICs (PMICs), Others), • By End Use (Consumer Electronics, Automotive, Industrial, Telecommunication, Healthcare, Others.), |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Qualcomm, NVIDIA, Broadcom, AMD (Advanced Micro Devices), MediaTek, Texas Instruments, Marvell Technology, Xilinx (now part of AMD), Skyworks Solutions, Cirrus Logic, ON Semiconductor, Infineon Technologies, Analog Devices, NXP Semiconductors, STMicroelectronics, Dialog Semiconductor (now part of Renesas), Silicon Labs, Lattice Semiconductor, Inphi (now part of Marvell Technology), Rambus. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Semiconductor Fabless Market in 2025.

Ans: The Application Specific Integrated Circuits (ASIC) segment dominated the Semiconductor Fabless Market in 2025.

Ans: The major growth factor of the Semiconductor Fabless Market is the increasing demand for advanced semiconductor solutions across various industries, particularly driven by the rise of emerging technologies such as 5G, artificial intelligence (AI), the Internet of Things (IoT), and electric vehicles (EVs)

Ans: Semiconductor Fabless Market size was USD 5.05 billion in 2025E and is expected to Reach USD 15.17 billion by 2035.

Ans: The Semiconductor Fabless Market is expected to grow at a CAGR of 9.60% during 2026-2035.

Get in Touch