Sleep Tech Market Report Scope & Overview:

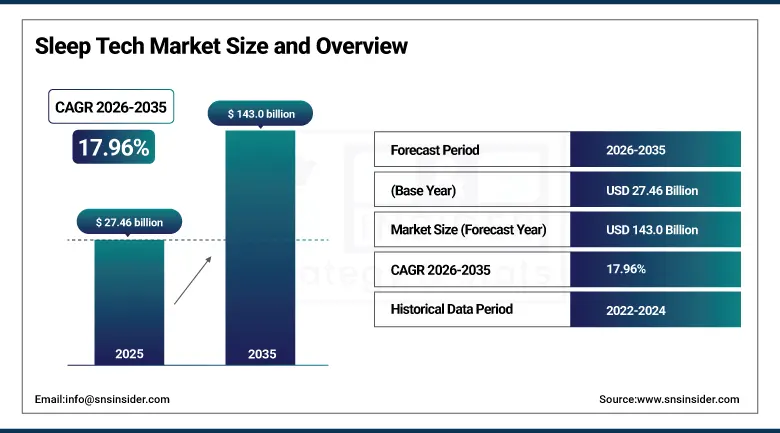

The Sleep Tech Market was valued at USD 27.46 billion in 2025 and is expected to reach USD 143.0 billion by 2035, growing at a CAGR of 17.96% from 2026–2035.

Sleep technology encompasses the rapidly expanding ecosystem of digital health devices, intelligent bedding systems, environmental control technologies, pharmacological alternatives, and AI-powered data analysis platforms designed to monitor, understand, and actively improve the quantity, quality, and restorative value of human sleep, addressing what the Centers for Disease Control and Prevention classifies as a public health epidemic where approximately one in three American adults and comparable proportions of adults in other developed economies fail to obtain the seven to nine hours of sleep per night that medical research consistently associates with optimal cognitive performance, cardiovascular health, metabolic function, immune system resilience, and mental wellness. The category spans a remarkable technological breadth from the consumer wearable sleep tracker worn on the wrist that passively monitors sleep duration and stage distribution using photoplethysmography and accelerometry, through FDA-cleared continuous positive airway pressure devices treating obstructive sleep apnea in the clinical medical device segment, to AI-powered smart mattresses from Eight Sleep and Sleep Number that actively adjust sleeping surface temperature and firmness in response to detected sleep stage and physiological data, creating an automated physical environment optimization layer on top of the monitoring function that most sleep devices provide.

The American Academy of Sleep Medicine's 2025 estimate that sleep disorders including obstructive sleep apnea, insomnia, restless leg syndrome, and circadian rhythm disorders affect over 70 million Americans annually, with global prevalence rates suggesting over 900 million adults worldwide suffer from obstructive sleep apnea alone, provides the clinical demand foundation that anchors the sleep tech market's growth trajectory independent of the lifestyle wellness consumer segment that constitutes its most visible growth driver.

Market Size and Forecast

-

Market Size in 2026E: USD 32.39 Billion

-

Market Size by 2035: USD 143.0 Billion

-

CAGR: 17.96% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Sleep Tech Market - Request Free Sample Report

Sleep Tech Market Trends

-

Rapid integration of AI-powered sleep coaching and recommendation engines within wearable sleep tracker companion applications that translate raw sleep measurement data into personalized behavioral recommendations addressing sleep hygiene, bedtime consistency, caffeine timing, exercise scheduling, and stress management practices that clinical evidence identifies as primary modifiable determinants of sleep quality.

-

Growing development and clinical validation of FDA-authorized digital therapeutics for insomnia that deliver cognitive behavioral therapy for insomnia protocols through smartphone applications, addressing the treatment gap between the millions of adults with chronic insomnia and the limited availability of trained CBT-I therapists whose clinical time cannot scale to meet population-level treatment demand.

-

Increasing adoption of non-contact sleep monitoring technology including under-mattress radar sensors, bedside sonar devices, and smart speaker microphones that detect breathing rate, body movement, and sleep stage transitions without requiring wearable device adherence, expanding sleep monitoring accessibility to individuals who cannot or prefer not to wear devices during sleep.

-

Rising integration of smart home ecosystem connectivity with sleep technology, where smart mattress temperature controllers, automated blackout curtain systems, smart speaker wake routines, and circadian-aligned smart lighting programmes coordinate as unified sleep environment optimization systems controlled through unified smartphone applications or voice AI platforms.

-

Expanding employer and corporate wellness programme investment in employee sleep health technology including subsidized sleep tracker provision, sleep health coaching programme access, and sleep disorder screening through occupational health partnerships that recognize sleep deprivation's documented impact on workplace safety incident rates, absenteeism, productivity, and healthcare cost utilisation.

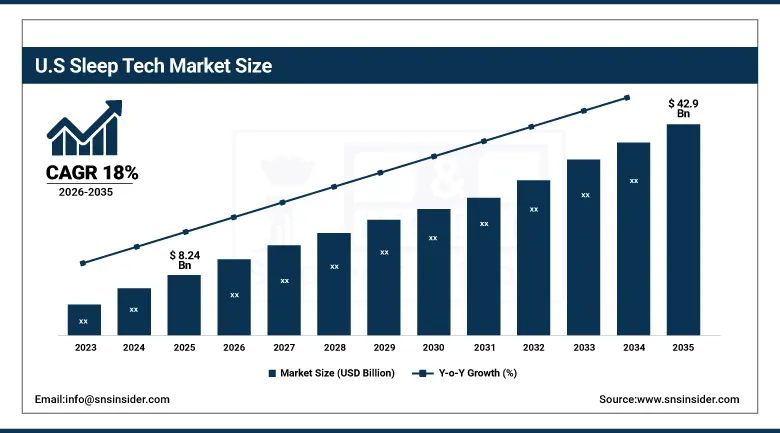

The U.S. Sleep Tech Market Outlook

The U.S. Sleep Tech Market was valued at approximately USD 8.24 billion in 2025 and is expected to reach approximately USD 42.9 billion by 2035, growing at a CAGR of approximately 18%.

The United States commands the largest national sleep tech market through the extraordinary convergence of the world's most acute documented sleep health crisis, with 35% of American adults sleeping fewer than seven hours nightly according to CDC survey data, with the most developed consumer health technology adoption culture and highest average consumer willingness to pay for wellness technology that delivers measurable personal health value. American consumer adoption of wearable fitness trackers and smartwatches has created a massive installed base of devices with sleep tracking capability, and the upgrade cycle from basic step-counting devices to advanced health monitoring platforms is driving consumer adoption of higher-quality sleep measurement features that create data-informed awareness of sleep health status and motivation for sleep improvement investment.

The FDA's Digital Health Centre of Excellence's Predetermined Change Control Plan framework, which enables AI-powered sleep analysis algorithm developers to update their clinical decision algorithms based on accumulating real-world device data without requiring new device applications, creates an innovation-friendly regulatory environment that is accelerating the development of clinically validated sleep monitoring and sleep disorder screening features for consumer wearable platforms.

Sleep Tech Market Segment Analysis

-

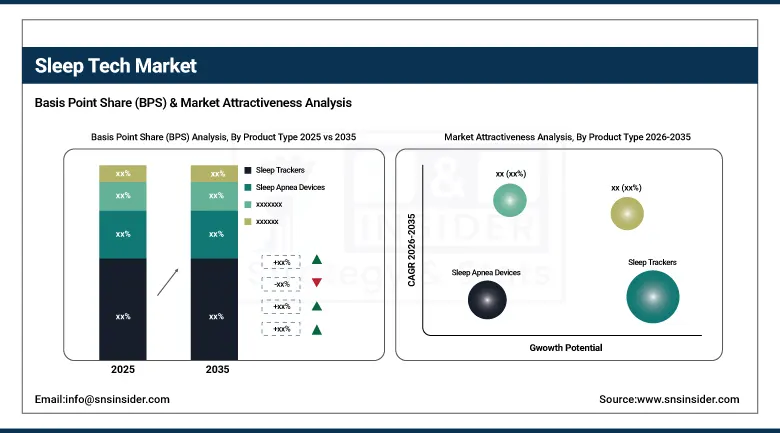

By Product Type, Sleep Trackers dominated with approximately 35.42% in 2025; Smart Mattresses are the fastest-growing at a CAGR of 19.23%.

-

By Technology, Wearable Devices held the largest share of 40.33% in; AI-Enabled Solutions are the fastest-growing at a CAGR of 21.07%.

-

By End User, Residential/Household accounted for the highest market share of 48.19% in 2025; Wellness & Fitness Centers are the fastest-growing at a CAGR of 20.01%.

-

By Distribution Channel, Online Retail led with the largest share of 38.92% in 2025; Specialty Stores are the fastest-growing at a CAGR of 20.55%.

By Product Type, Sleep trackers dominate, smart mattresses are expected to grow fastest

Sleep Trackers retained the dominant product type position with approximately 35.42% of the Sleep Tech Market in 2025, driven by the 150 million or more sleep tracking devices actively monitoring user sleep globally through a combination of dedicated sleep tracker devices and the sleep tracking features integrated into mass-market fitness wearables and smartwatches from Apple, Samsung, Garmin, and Fitbit whose enormous installed base makes sleep monitoring a default rather than a premium feature for hundreds of millions of regular wearable users.

Smart Mattresses are the fastest-growing product type at a CAGR of 19.23% through 2035, representing the convergence of premium comfort technology with biometric monitoring and AI-powered environmental optimization in a product whose price point, typically USD 2,000 to 10,000 for premium models from Eight Sleep and Sleep Number, signals the premium consumer wellness investment category that is growing rapidly as awareness of sleep's importance to cognitive and physical performance elevates mattress selection from a durability and comfort decision to a health optimization investment.

By Technology, Wearable Devices dominate, ai-enabled solutions are expected to grow fastest

Wearable Devices retained the dominant technology position with approximately 40.33% of Sleep Tech Market revenues in 2025, as the extraordinary global penetration of smartwatches and fitness trackers with integrated sleep monitoring capability has created the world's largest distributed sleep monitoring network whose collective data generates population-level sleep health insights alongside the individual user data that motivates continued device use and upgrade investment.

AI-Enabled Solutions are the fastest-growing technology at a CAGR of 21.07% through 2035, reflecting the transformative potential of machine learning algorithms to convert the enormous streams of raw physiological measurement data generated by sleep monitoring devices into clinically meaningful and actionable health insights that pure data collection without interpretation cannot deliver.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.6% |

|

Europe |

United Kingdom |

23.7% |

|

Asia Pacific |

China |

41.3% |

|

Middle East & Africa |

UAE |

28.4% |

|

Latin America |

Brazil |

43.2% |

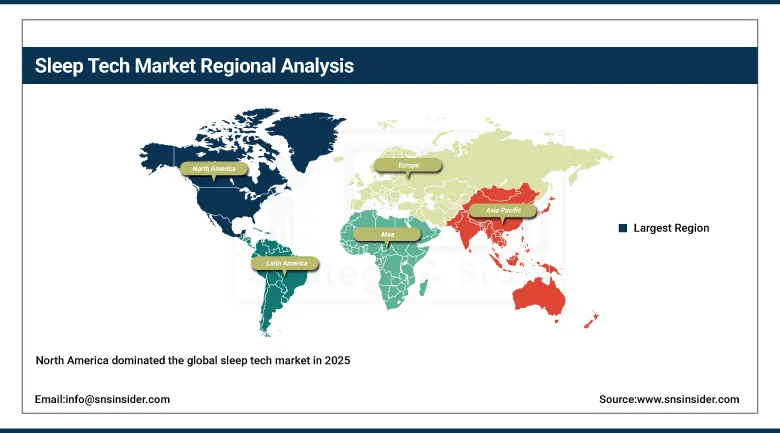

North America Sleep Tech Market Insights

North America dominated the global sleep tech market in 2025, with the United States accounting for approximately 85.6% of North American revenues. The region's leadership reflects the most acute documented consumer sleep health crisis creating the strongest awareness-driven technology adoption motivation, the world's highest wearable consumer technology penetration creating a device ecosystem within which sleep monitoring features have near-universal adoption, and the most developed digital health regulatory environment that has created pathways for clinically validated sleep technology features that premium device brands are investing to develop. The U.S. sleep disorder treatment market's integration of consumer sleep technology into clinical assessment workflows at progressive healthcare institutions is validating the medical relevance of consumer sleep monitoring that sustains premium technology investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Sleep Tech Market Insights

Europe is a sophisticated sleep tech market driven by high consumer health consciousness, well-developed wearable technology adoption across the United Kingdom, Germany, France, and the Nordic countries, and the progressive integration of digital health tools into healthcare system preventive health programmes. The United Kingdom accounts for approximately 23.7% of European revenues through its combination of high smartwatch and fitness wearable adoption, the NHS's engagement with digital health tools including sleep health applications in its digital therapeutic prescribing programme, and the presence of major sleep technology brand operations in London serving both UK and European markets. European regulatory engagement with AI-powered medical device classification for sleep disorder screening features is creating clarity for premium sleep technology developers seeking to validate clinical claims in European markets.

Asia Pacific Sleep Tech Market Insights

Asia Pacific is the fastest-growing sleep tech market, driven by the extraordinary combination of the world's highest rates of sleep deprivation in major Asian economies including Japan, South Korea, and China where cultural and professional pressures create structural sleep health challenges at population scale, combined with extremely high smartphone and wearable technology adoption rates that provide the digital infrastructure for sleep technology engagement, and rapidly rising health consciousness particularly among younger urban professional demographics who actively invest in quantified self-monitoring technology for performance and wellness optimization. China accounts for approximately 41.3% of Asia Pacific revenues through its massive consumer technology market, rapidly growing premium wearable adoption, and growing healthcare system investment in digital health solutions for the chronic disease prevention programmes that include sleep health optimization as a recognized cardiovascular and metabolic risk modifier.

MEA & Latin America Sleep Tech Market Insights

The Middle East and Africa and Latin America are growing sleep tech markets where high smartphone penetration enabling app-based sleep monitoring adoption, rising consumer health consciousness particularly among affluent urban professional demographics, and growing wellness sector development are creating initial but expanding commercial opportunities for sleep technology products across price tiers from affordable consumer applications through premium smart bedding. UAE leads MEA sleep tech revenues at approximately 28.4% of regional revenues through its high per-capita income, premium consumer electronics adoption culture, and corporate wellness programme development among the Emirates' large professional workforce in financial services and technology sectors. Brazil leads Latin American revenues at approximately 43.2% through its large urban population with high smartphone penetration and growing wellness culture.

Market Dynamics

Growth Drivers: Rising sleep health awareness, increasing adoption of AI-powered sleep monitoring technologies, and demand for personalized wellness solutions are driving market growth.

The primary structural growth drivers for the Sleep Tech Market are the extraordinary global scale of sleep health challenges, where the WHO's characterization of insufficient sleep as a global epidemic affecting over two thirds of adults in developed nations and growing proportions of adults in emerging economies creates a vast aware and motivated consumer market for technology offering measurable sleep improvement, combined with the AI-powered transformation of sleep monitoring from passive data recording into active personalized coaching that is resolving the historically most significant commercial limitation of consumer sleep technology: the gap between data availability and actionable insight that caused many users to abandon sleep tracking engagement after the novelty of initial data visualization wore off without translating into sleep behaviour change. The convergence of increasingly accurate and comfortable wearable sensors, smartphone application ecosystem maturity, and AI coaching capability is creating a genuine consumer sleep health improvement technology that sustains long-term engagement and generates demonstrated health outcomes.

Restraints: Limited clinical accuracy, high product costs, and data privacy concerns are restraining adoption of advanced sleep monitoring technologies.

A significant restraint on the Sleep Tech Market is the accuracy gap between consumer wearable sleep monitoring devices and the polysomnography reference standard used in clinical sleep medicine, where current consumer devices achieve approximately 80% accuracy in sleep stage classification that is valuable for population health trend tracking and lifestyle guidance but insufficient for the definitive diagnosis of specific sleep disorders including narcolepsy, parasomnia, and precise characterization of sleep apnea severity that clinical management decisions require. This accuracy limitation constrains the clinical credibility of consumer sleep technology in formal healthcare contexts and creates a regulatory boundary between wellness monitoring devices and medical devices that limits the sleep disorder management features that consumer brands can market without pursuing FDA clearance through clinical validation programmes.

Opportunities: Digital sleep therapeutics, wearable-based sleep disorder screening, and corporate wellness programs are creating new market growth opportunities.

The FDA's approval of Somryst, the prescription digital therapeutic delivering cognitive behavioral therapy for insomnia through a smartphone application, has established the regulatory and reimbursement precedent for digital sleep health interventions that represent a potential breakthrough in the sleep tech market's commercial model, as clinical reimbursement of evidence-based digital therapeutics creates a new payer-funded revenue stream alongside the direct consumer purchase model that has characterised the category to date. Sleep disorder screening integration in consumer wearables, where Apple's Apple Watch irregular rhythm notification feature demonstrated the template for FDA-authorized health screening functionality in mass-market wearables, suggests a comparable pathway for obstructive sleep apnea screening features in consumer devices that could enable population-scale identification of the hundreds of millions of undiagnosed sleep apnea patients whose condition currently goes undetected until cardiovascular or metabolic consequences prompt clinical attention.

Recent Developments:

-

August 2025: Fitbit released a major update to its sleep tracking algorithm, increasing sleep stage detection accuracy by more effectively identifying short awakenings and micro-arousals that previous algorithm versions missed, improving the clinical comparability of Fitbit sleep data and addressing one of the most frequently cited accuracy limitations in consumer sleep tracker validation studies.

-

2025: Eight Sleep launched the Pod 4 Ultra with enhanced biometric sensing, automated mattress temperature adjustment, and a new cardiovascular health monitoring feature providing resting heart rate variability and respiratory rate trending accessible through an updated companion application that introduces personalized sleep health coaching powered by AI analysis of accumulated user sleep data.

-

2025: Samsung expanded its Galaxy Ring's sleep monitoring capabilities with new sleep apnea detection functionality following FDA authorization, making Samsung the second major consumer wearable manufacturer after Apple to offer FDA-authorized sleep disorder screening features in a mass-market wearable platform available without prescription.

Sleep Tech Market Key Players

-

ResMed Inc.

-

Philips Healthcare (Philips Respironics)

-

Apple Inc.

-

Samsung Electronics Co. Ltd.

-

Garmin Ltd.

-

Fitbit (Google)

-

Oura Health

-

Eight Sleep Inc.

-

Sleep Number Corporation

-

Withings SA

-

Dreem (ResMed)

-

Nox Medical

-

SleepScore Labs

-

Beddr Inc.

-

Casper Sleep Inc.

-

Purple Innovation LLC

-

Tempur-Pedic (TP-Link)

-

Fisher & Paykel Healthcare

-

Inspire Medical Systems

-

Somnodent (SomnoMed)

Sleep Tech Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.46 Billion |

| Market Size by 2035 | USD 143.0 Billion |

| CAGR | CAGR of 17.96% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Sleep Trackers, Sleep Apnea Devices, Smart Mattresses, Smart Pillows & Bedding, Light Therapy Devices, Others) • By Technology (Wearable Devices, Non-Wearable Devices, AI-Enabled Solutions, Others) • By End User (Residential/Household, Hospitals & Healthcare Facilities, Wellness & Fitness Centers, Hospitality) • By Distribution Channel (Online Retail, Specialty Stores, Medical Equipment Stores, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ResMed Inc., Philips Healthcare (Philips Respironics), Apple Inc., Samsung Electronics Co. Ltd., Garmin Ltd., Fitbit (Google), Oura Health, Eight Sleep Inc., Sleep Number Corporation, Withings SA, Dreem (ResMed), Nox Medical, SleepScore Labs, Beddr Inc., Casper Sleep Inc., Purple Innovation LLC, Tempur-Pedic (TP-Link), Fisher & Paykel Healthcare, Inspire Medical Systems, and Somnodent (SomnoMed). |

Frequently Asked Questions

North America dominated the Sleep Tech Market in 2025.

Sleep Trackers dominated with approximately 35.42% of revenues in 2025.

The global sleep health crisis creating mass consumer awareness of sleep's health importance combined with AI technology transformation of raw device data into personalised actionable coaching that drives sustained premium technology adoption and measurable sleep health improvement outcomes.

The Sleep Tech Market was valued at USD 27.46 billion in 2025.

The Sleep Tech Market is expected to grow at a CAGR of 17.96% from 2026 to 2035.

Get in Touch