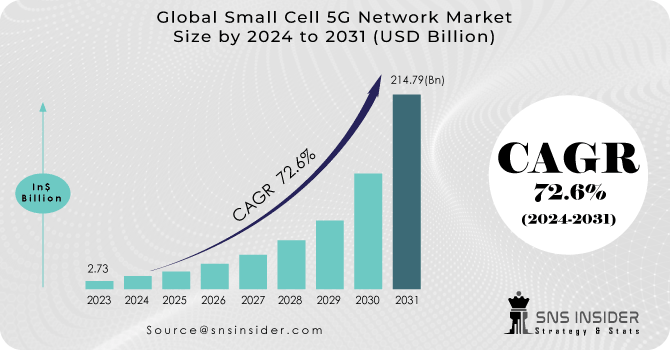

The Small Cell 5G Network Market size was valued at USD 2.73 billion in 2023 and is expected to grow to USD 214.79 billion by 2031 and grow at a CAGR of 72.6% over the forecast period of 2024-2031.

The demand for small cell 5G networks has been driven by increasing data traffic and an increase in the number of internet users around the world, which has contributed to market growth. Increasing investments in 5G infrastructure and increased funding for high-speed networks in a number of countries around the world are expected to increase demand for small cell 5G networks. The growth of the market share of small cell 5G networks is expected to be supported by this factor. In order to increase coverage capacity at an affordable price, the number of small cells 5G networks is increasing in industrial, business and residential applications.

Get more information on Small Cell 5G Network Market - Request Sample Report

Key Drivers:

Mobile data traffic is the transfer of Internet content to different mobile consumer electronics, e.g. smartphones and tablet computers. The growth of the market is driven by an ongoing increase in data traffic on cell phones worldwide. By 2024, global mobile traffic is projected to increase by a factor of 5 and account for 136 billion dollars per month. Moreover, almost one third of global mobile data traffic is estimated to be carried on 5G networks by 2024. As a result, there has been a significant increase in mobile data traffic.

Restraints:

Due to the limited availability of fiber networks in many countries, it is a critical challenge for telecommunications operators to deploy fibre backhaul networks on small cells which will allow low latency and high data rates. It is also not cost effective to install fibre backend, so operators should look into wireless backhaul options for certain countries. In this case, in addition to fibre, consideration should be given to a wide range of wireless technologies such as mm Wave, PMP and satellite.

Opportunities:

The development of 5G technologies and its growing deployment rate have led to a growth in the small cell market. The market for small cells in 5G networks is supported by the high speeds and low latencies of this network. In order to address the problem of mobile traffic congestion, it will be necessary to build a next generation network. Governments around the world have adopted support policies to help industry in research and development and pursue 5G commercialisation.

Although 4G solutions are being deployed to meet the needs of the Internet of Things, applications with low latency, bandwidth and reliability constraints can best benefit from them. The current 4G Internet of Things performance and scale is lower than the 5G targets, but sufficient to create new connections and business models. In order to support 5G Internet of Things applications, it will be essential that tiny cells are placed at a density sufficient for deployment.

Challenges:

The growth of the market is also supported by an increasing number of enterprises and telecommunications operators deploying RAN small cell networks. These factors suggest a strong demand for small cell 5G networks, which could mitigate some of the negative effects of the global economic slowdown. The market for small cell 5G networks is facing challenges due to the global economic slowdown, particularly in terms of high deployment costs, the market is still on a rapid growth path. Various sectors, such as the small cell 5G network market, are facing challenges in a global economy that is being slowed down by factors such as higher deployment costs. In particular, it is particularly costly to set up 5G infrastructure, especially in its early stages, and the costs vary widely from one geographical area to another. These costs may be further increased due to the lack of available resources within more rural areas.

Several factors are driving growth, including the increasing demand for mobile data traffic, the emergence of new technologies such as Internet of Things IoT and Machine to machine communication which is also being rolled out in 5G networks. In addition, significant developments are taking place in the market, such as the increasing adoption of Internet of Things IoT devices, which increases the demand for reliable internet connections.

The Russia-Ukraine crisis may heighten cybersecurity concerns related to 5G networks. There could be an increased focus on protecting critical infrastructure from cyberattacks, including small cell networks, particularly if there are fears of state-sponsored cyber threats or espionage activities. The Russian 5G trajectory is uncertain due to the reluctance of Russia. The Ministry of Defence shall surrender its rights in the contested 3.4 to 3.8 GHz bands. For countries such as Lithuania, regulatory problems in Russia with 5G are a problem. trying to cultivate 5G networks. NATO Organization North Atlantic Treaty Organisation governments feel the need to abide by international agreements governing spectrum And NATO military forces can't use the 5G infrastructure in peacetime, remains.

The Ukrainian Mobile Operators' Community has taken a series of massive and important steps in order to protect its mobile networks as well as guarantee their resilience, even before the new invasion that took place in 2022. First, we need to know the extent of mobile penetration in Ukraine before going into detail on this. The proportion of the population who own a cell phone is 130%, meaning that more than 80% of the population have one. On Vodafone Ukraine outside of Kyiv – and is the mobile wing of the fixed line incumbent. Any geopolitical tension may result in increased scrutiny and potential restriction of policies for companies which are active or with a link to the regions concerned as regards the strategic importance of 5G technology on domestic infrastructure. The strategies of the main market players and the possible deployment of small cell 5G networks in sensitive or strategic areas could be affected.

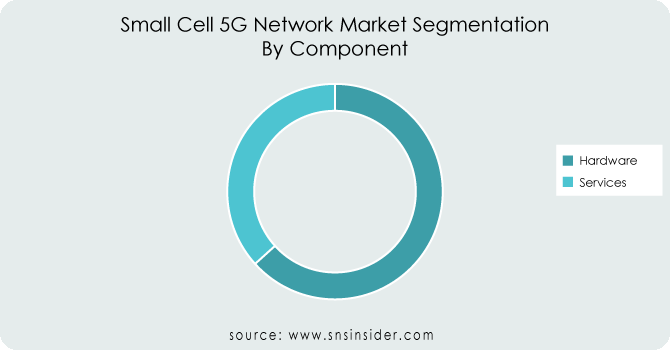

By Component

Hardware

Picocell

Femtocell

Microcell

Services

Consulting

Deployment & Integration

Training and Support & Maintenance

The hardware segment dominated the market as regards revenues by 2023. Picocell, Femtocell and Microcell are also part of the hardware segment. The femtocell segment accounted for more than 63.3% of market share by volume between 2022 and 2023. This is due to the growing demand from a number of enclosed applications, e.g. shopping malls, homes, offices and hospitals for coherent network coverage.

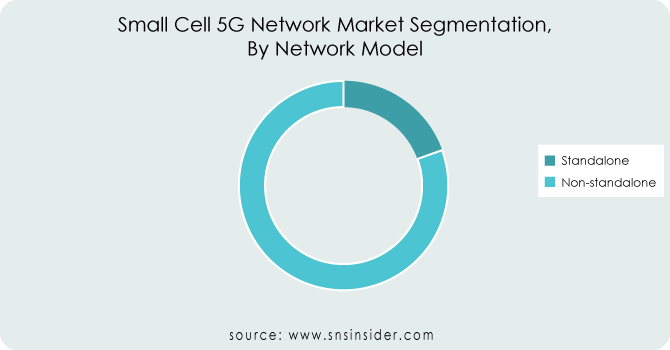

By Network Model

Standalone

Non-standalone

In terms of revenue, the non-standalone NSA network model dominated the market and accounted for more than 81.3% of the market in 2023. This is due to the rapid deployment of a network which does not exist in isolation around the world. In order to integrate with existing legacy network infrastructure, the non-stand-alone network is generally used because it is a time and cost-efficient option.

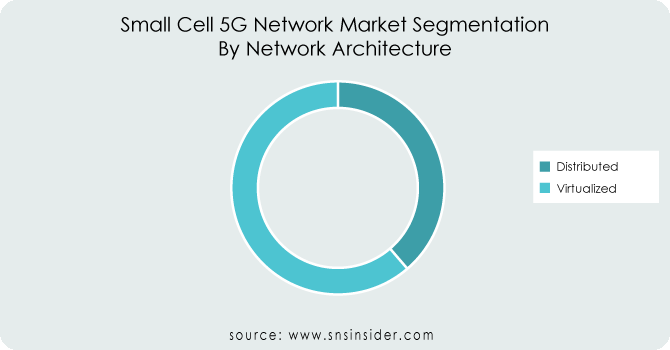

By Network Architecture

Distributed

Virtualized

Virtualised Network architecture accounted for more than 61.3% of the market value from 2023 onwards. A strong deployment of 5G small cell networks with a centralised baseband unit control architecture can be attributed to the dominant share in this segment. As a result, by managing virtually all small cell base stations, service providers can reduce the total cost of ownership TCO and increase the overall flexibility of the network.

Need any customization reseaech on Small Cell 5G Network Market - Enquiry Now

By Deployment Mode

Indoor

Outdoor

By Frequency Type

Sub-6 GHz

mmWave

Sub-6GHz + mmWave

By End-Use

Residential

Commercial

Corporates/ Enterprises

Hospitals

Hotels & Restaurants

Malls/Shops

Stadiums

Others

Industrial

Smart Manufacturing

Energy & Utility

Oil & Gas and Mining

Smart City

Transportation & Logistics

Government & Defense

Others

In 2023, due to the increasing adoption of advanced technologies and investments in 5G technology by the leading players in the high-speed internet market, Asia Pacific dominated the market for small cell 5G networks. The market for networking and 5G infrastructure in the region is being driven by rapidly evolving technology in China, Japan or South Korea.

During the forecast period, healthy market growth is expected in North America. This growth is driven by increased investments and growth strategies of the IT & telecommunications industry's leading players and governments. The Forum for Small Cells reports that North America has played a key role in facilitating the deployment of smaller cells and is projected to reach its peak yearly use rate by 2023.

To meet the increasing demand for Internet of the latest and fastest speeds, European governments have made a significant investment to deploy 5G networks. In order to support digital transformation, the European Commission allocated 20% of its resilience and recovery facilities from each Member State in collaboration with national IT players.

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Nokia Corporation, Telefonaktiebolaget LM Ericsson, ZTE Corporation, Fujitsu Limited, CommScope Inc., Comba Telecom Systems Holdings Ltd., Altiostar, Airspan Networks, Ceragon

May 2023 – Nokia Corporation announced a trial with Chunghwa Telecom Laboratories (CHT-TL) that verified the capability of 25G PON technology for small cell fronthaul in 5G. The trial demonstrated that this technology could meet the strict capacity requirements of fronthaul and lower latency, which would allow operators to reduce their costs significantly and bring about network convergence.

In February 2023, Maxlinear, Inc. announced that it had entered into a collaboration with EdgeQ on the design of an allinone small cell connection converging 4G, 5G, and computing on a single software defined platform. Incorporating EdgeQ’s 5G Base Station-on-a-chip with Maxlinear’s MXL1600 RF transceiver and Maxlin wideband digital pre-distortion (DPD) solution creates a new software-programmable paradigm that lets creators scale rapidly and dynamically across the wide range of small cell applications.

September 2022, Samsung has entered into a strategic partnership with Comcast to improve 5G connectivity for Xfinity Mobile and the comcast Business mobile customers within its service area. It supplied 50 RAN solutions, including baseband units, CBRS, 600 MHz radios, and compact CBRS Strand small cells. Comcast has been able to provide a seamless cellular connection thanks to this partnership.

| Report Attributes | Details |

| Market Size in 2023 | US$ 2.73 Bn |

| Market Size by 2031 | US$ 214.79 Bn |

| CAGR | CAGR of 72.6% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Services) • By Network Model (Standalone, Non-standalone) • By Network Architecture (Distributed, Virtualized) • By Deployment Mode (Indoor, Outdoor) • By Frequency Type (Sub-6 GHz, mmWave, Sub-6GHz + mmWave) • By End-use (Residential, Commercial, Industrial, Smart City, Transportation & Logistics, Government & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Nokia Corporation, Telefonaktiebolaget LM Ericsson, ZTE Corporation, Fujitsu Limited, CommScope Inc., Comba Telecom Systems Holdings Ltd., Altiostar, Airspan Networks, Ceragon |

| Key Drivers | • A rise in mobile data traffic • Citizens Broadband Radio Service Band Emergence |

| Market Opportunities | • The Rise of IoT and M2M Communication • The potential emergence of 5G |

Ans: The Small Cell 5G Network Market was valued at USD 2.73 billion in 2023.

Ans: - A rise in mobile data traffic and Citizens Broadband Radio Service Band Emergence.

Ans: - North America dominates the small cell 5G network market.

Ans: - The major key players are Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Nokia Corporation, Telefonaktiebolaget LM Ericsson, ZTE Corporation, Fujitsu Limited, CommScope Inc., Comba Telecom Systems Holdings Ltd., Altiostar, Airspan Networks, Ceragon.

Ans: - Key Stakeholders Considered in the study are Raw material vendors, Regulatory authorities, including government agencies and NGOs, Commercial research, and development (R&D) institutions, Importers and exporters, etc.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Small Cell 5G Network Market Segmentation, By Component

9.1 Introduction

9.2 Trend Analysis

9.3 Hardware

9.3.1 Picocell

9.3.2 Femtocell

9.3.3 Microcell

9.4 Services

9.4.1 Consulting

9.4.2 Deployment & Integration

9.4.3 Training and Support & Maintenance

10. Small Cell 5G Network Market Segmentation, By Network Model

10.1 Introduction

10.2 Trend Analysis

10.3 Standalone

10.4 non-standalone

11. Small Cell 5G Network Market Segmentation, By Network Architecture

11.1 Introduction

11.2 Trend Analysis

11.3 Distributed

11.4 Virtualize

12. Small Cell 5G Network Market Segmentation, By Deployment Mode

12.1 Introduction

12.2 Trend Analysis

12.3 Indoor

12.4 Outdoor

13. Small Cell 5G Network Market Segmentation, By Frequency Type

13.1 Introduction

13.2 Trend Analysis

13.3 Sub-6 GHz

13.4 mmWave

13.5 Sub-6GHz + mmWave

14. Small Cell 5G Network Market Segmentation, By End-use

14.1 Introduction

14.2 Trend Analysis

14.3 Residential

14.4 Commercial

14.4.1 Corporates/ Enterprises

14.4.2 Hospitals

14.4.3 Hotels & Restaurants

14.4.4 Malls/Shops

14.4.5 Stadiums

14.4.6 Others

14.5 Industrial

14.5.1 Smart Manufacturing

14.5.2 Energy & Utility

14.5.3 Oil & Gas and Mining

14.6 Smart City

14.7 Transportation & Logistics

14.8 Government & Defense

14.9 Others

15. Regional Analysis

15.1 Introduction

15.2 North America

15.2.1 USA

15.2.2 Canada

15.2.3 Mexico

15.3 Europe

15.3.1 Eastern Europe

15.3.1.1 Poland

15.3.1.2 Romania

15.3.1.3 Hungary

15.3.1.4 Turkey

15.3.1.5 Rest of Eastern Europe

15.3.2 Western Europe

15.3.2.1 Germany

15.3.2.2 France

15.3.2.3 UK

15.3.2.4 Italy

15.3.2.5 Spain

15.3.2.6 Netherlands

15.3.2.7 Switzerland

15.3.2.8 Austria

15.3.2.9 Rest of Western Europe

15.4 Asia-Pacific

15.4.1 China

15.4.2 India

15.4.3 Japan

15.4.4 South Korea

15.4.5 Vietnam

15.4.6 Singapore

15.4.7 Australia

15.4.8 Rest of Asia Pacific

15.5 The Middle East & Africa

15.5.1 Middle East

15.5.1.1 UAE

15.5.1.2 Egypt

15.5.1.3 Saudi Arabia

15.5.1.4 Qatar

15.5.1.5 Rest of the Middle East

15.5.2 Africa

15.5.2.1 Nigeria

15.5.2.2 South Africa

15.5.2.3 Rest of Africa

15.6 Latin America

15.6.1 Brazil

15.6.2 Argentina

15.6.3 Colombia

15.6.4 Rest of Latin America

16. Company Profiles

16.1 Huawei Technologies Co., Ltd.

16.1.1 Company Overview

16.1.2 Financial

16.1.3 Products/ Services Offered

16.1.4 SWOT Analysis

16.1.5 The SNS View

16.2 Samsung Electronics Co., Ltd.

16.2.1 Company Overview

16.2.2 Financial

16.2.3 Products/ Services Offered

16.2.4 SWOT Analysis

16.2.5 The SNS View

16.3 Nokia Corporation

16.3.1 Company Overview

16.3.2 Financial

16.3.3 Products/ Services Offered

16.3.4 SWOT Analysis

16.3.5 The SNS View

16.4 Telefonaktiebolaget LM Ericsson

16.4.1 Company Overview

16.4.2 Financial

16.4.3 Products/ Services Offered

16.4.4 SWOT Analysis

16.4.5 The SNS View

16.5 ZTE Corporation

16.5.1 Company Overview

16.5.2 Financial

16.5.3 Products/ Services Offered

16.5.4 SWOT Analysis

16.5.5 The SNS View

16.6 Fujitsu Limited

16.6.1 Company Overview

16.6.2 Financial

16.6.3 Products/ Services Offered

16.6.4 SWOT Analysis

16.6.5 The SNS View

16.7 CommScope Inc.

16.7.1 Company Overview

16.7.2 Financial

16.7.3 Products/ Services Offered

16.7.4 SWOT Analysis

16.7.5 The SNS View

16.8 Comba Telecom Systems Holdings Ltd.

16.8.1 Company Overview

16.8.2 Financial

16.8.3 Products/ Services Offered

16.8.4 SWOT Analysis

16.8.5 The SNS View

16.9 Altiostar, Airspan Networks

16.9.1 Company Overview

15.9.2 Financial

15.9.3 Products/ Services Offered

16.9.4 SWOT Analysis

15.9.5 The SNS View

16.10 Ceragon

16.10.1 Company Overview

16.10.2 Financial

16.10.3 Products/ Services Offered

16.10.4 SWOT Analysis

16.10.5 The SNS View

17. Competitive Landscape

17.1 Competitive Benchmarking

17.2 Market Share Analysis

17.3 Recent Developments

17.3.1 Industry News

17.3.2 Company News

17.3.3 Mergers & Acquisitions

18. Use Case and Best Practices

19. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The CAD and PLM Software Market size was valued at USD 14.89 billion in 2022 and is expected to grow to USD 26.55 billion by 2030 and grow at a CAGR of 7.5 % over the forecast period of 2023-2030.

The Supply Chain Management Market was estimated to be worth USD 26.8 billion in 2022 and is projected to reach USD 62.20 billion by 2030, growing at a CAGR of 11.1% from 2023 to 2030.

The Facility Management Market size was valued at USD 48.2 billion in 2022 and is projected to reach USD 122.35 billion in 2030 with a growing CAGR of 12.35% Over the Forecast Period of 2023-2030.

The Digital Transformation Market was valued at USD 596 billion in 2022 and is expected to reach at USD 2738 billion by 2030, and grow at a CAGR of 21% over the forecast period of 2023-2030.

The Healthcare Cyber Security Market size was valued at USD 14.91 Bn in 2022 and is expected to reach USD 55.63 Bn by 2030, and grow at a CAGR of 17.89% over the forecast period 2023-2030.

The Web Real-Time Communication (webRTC) Market size was USD 6.2 Billion in 2023 and is expected to Reach USD 70.03 Billion by 2031 and grow at a CAGR of 35.4% over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd